Leading the Way Forward

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

AAWW Investor Slides

AAWW Investor Slides JUNE 2020 Index Page Page 3 Safe Harbor Statement 21 e-Commerce Growth 4 Continuing Leadership 22 Fleet Aligned with Express and e-Commerce 5 Operating a Vital Business 23 A Strong Leader in a Vital Industry 6 Shaping a Powerful Future 24 Appendix 7 2020 Objectives 25 Atlas Air Worldwide 8 1Q20 Highlights 26 Our Vision, Our Mission 9 1Q20 Summary 27 Executing Strategic Plan 10 Outlook 28 Global Operating Network 11 Business Developments – ACMI/CMI 29 North America Operating Network 12 Business Developments – Charter/Dry Leasing 30 Tailoring Airfreight Networks for e-Commerce 13 CARES Act Payroll Support Grant 31 Global Airfreight Drivers 14 Amazon Service 32 Large Freighter Supply Trends 15 Diversified Customer Base 33 Main Deck to Belly? 16 Our Fleet 34 Growth by Year 17 Global Presence 35 Net Leverage Ratio 18 Delivering a Strong Value Proposition 36 Financial and Operating Trends 19 International Global Airfreight – Annual Growth 37 2020 Maintenance Expense 20 The Key Underlying Express Market Is Growing 38 Reconciliation to Non-GAAP Measures 2 Safe Harbor Statement This presentation contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995 that reflect Atlas Air Worldwide Holdings Inc.’s (“AAWW”) current views with respect to certain current and future events and financial performance. Such forward-looking statements are and will be, as the case may be, subject to many risks, uncertainties and factors relating to the operations and business environments of AAWW and its subsidiaries that may cause actual results to be materially different from any future results, express or implied, in such forward-looking statements. -

IATA CLEARING HOUSE PAGE 1 of 21 2021-09-08 14:22 EST Member List Report

IATA CLEARING HOUSE PAGE 1 OF 21 2021-09-08 14:22 EST Member List Report AGREEMENT : Standard PERIOD: P01 September 2021 MEMBER CODE MEMBER NAME ZONE STATUS CATEGORY XB-B72 "INTERAVIA" LIMITED LIABILITY COMPANY B Live Associate Member FV-195 "ROSSIYA AIRLINES" JSC D Live IATA Airline 2I-681 21 AIR LLC C Live ACH XD-A39 617436 BC LTD DBA FREIGHTLINK EXPRESS C Live ACH 4O-837 ABC AEROLINEAS S.A. DE C.V. B Suspended Non-IATA Airline M3-549 ABSA - AEROLINHAS BRASILEIRAS S.A. C Live ACH XB-B11 ACCELYA AMERICA B Live Associate Member XB-B81 ACCELYA FRANCE S.A.S D Live Associate Member XB-B05 ACCELYA MIDDLE EAST FZE B Live Associate Member XB-B40 ACCELYA SOLUTIONS AMERICAS INC B Live Associate Member XB-B52 ACCELYA SOLUTIONS INDIA LTD. D Live Associate Member XB-B28 ACCELYA SOLUTIONS UK LIMITED A Live Associate Member XB-B70 ACCELYA UK LIMITED A Live Associate Member XB-B86 ACCELYA WORLD, S.L.U D Live Associate Member 9B-450 ACCESRAIL AND PARTNER RAILWAYS D Live Associate Member XB-280 ACCOUNTING CENTRE OF CHINA AVIATION B Live Associate Member XB-M30 ACNA D Live Associate Member XB-B31 ADB SAFEGATE AIRPORT SYSTEMS UK LTD. A Live Associate Member JP-165 ADRIA AIRWAYS D.O.O. D Suspended Non-IATA Airline A3-390 AEGEAN AIRLINES S.A. D Live IATA Airline KH-687 AEKO KULA LLC C Live ACH EI-053 AER LINGUS LIMITED B Live IATA Airline XB-B74 AERCAP HOLDINGS NV B Live Associate Member 7T-144 AERO EXPRESS DEL ECUADOR - TRANS AM B Live Non-IATA Airline XB-B13 AERO INDUSTRIAL SALES COMPANY B Live Associate Member P5-845 AERO REPUBLICA S.A. -

My Personal Callsign List This List Was Not Designed for Publication However Due to Several Requests I Have Decided to Make It Downloadable

- www.egxwinfogroup.co.uk - The EGXWinfo Group of Twitter Accounts - @EGXWinfoGroup on Twitter - My Personal Callsign List This list was not designed for publication however due to several requests I have decided to make it downloadable. It is a mixture of listed callsigns and logged callsigns so some have numbers after the callsign as they were heard. Use CTL+F in Adobe Reader to search for your callsign Callsign ICAO/PRI IATA Unit Type Based Country Type ABG AAB W9 Abelag Aviation Belgium Civil ARMYAIR AAC Army Air Corps United Kingdom Civil AgustaWestland Lynx AH.9A/AW159 Wildcat ARMYAIR 200# AAC 2Regt | AAC AH.1 AAC Middle Wallop United Kingdom Military ARMYAIR 300# AAC 3Regt | AAC AgustaWestland AH-64 Apache AH.1 RAF Wattisham United Kingdom Military ARMYAIR 400# AAC 4Regt | AAC AgustaWestland AH-64 Apache AH.1 RAF Wattisham United Kingdom Military ARMYAIR 500# AAC 5Regt AAC/RAF Britten-Norman Islander/Defender JHCFS Aldergrove United Kingdom Military ARMYAIR 600# AAC 657Sqn | JSFAW | AAC Various RAF Odiham United Kingdom Military Ambassador AAD Mann Air Ltd United Kingdom Civil AIGLE AZUR AAF ZI Aigle Azur France Civil ATLANTIC AAG KI Air Atlantique United Kingdom Civil ATLANTIC AAG Atlantic Flight Training United Kingdom Civil ALOHA AAH KH Aloha Air Cargo United States Civil BOREALIS AAI Air Aurora United States Civil ALFA SUDAN AAJ Alfa Airlines Sudan Civil ALASKA ISLAND AAK Alaska Island Air United States Civil AMERICAN AAL AA American Airlines United States Civil AM CORP AAM Aviation Management Corporation United States Civil -

Appendix 25 Box 31/3 Airline Codes

March 2021 APPENDIX 25 BOX 31/3 AIRLINE CODES The information in this document is provided as a guide only and is not professional advice, including legal advice. It should not be assumed that the guidance is comprehensive or that it provides a definitive answer in every case. Appendix 25 - SAD Box 31/3 Airline Codes March 2021 Airline code Code description 000 ANTONOV DESIGN BUREAU 001 AMERICAN AIRLINES 005 CONTINENTAL AIRLINES 006 DELTA AIR LINES 012 NORTHWEST AIRLINES 014 AIR CANADA 015 TRANS WORLD AIRLINES 016 UNITED AIRLINES 018 CANADIAN AIRLINES INT 020 LUFTHANSA 023 FEDERAL EXPRESS CORP. (CARGO) 027 ALASKA AIRLINES 029 LINEAS AER DEL CARIBE (CARGO) 034 MILLON AIR (CARGO) 037 USAIR 042 VARIG BRAZILIAN AIRLINES 043 DRAGONAIR 044 AEROLINEAS ARGENTINAS 045 LAN-CHILE 046 LAV LINEA AERO VENEZOLANA 047 TAP AIR PORTUGAL 048 CYPRUS AIRWAYS 049 CRUZEIRO DO SUL 050 OLYMPIC AIRWAYS 051 LLOYD AEREO BOLIVIANO 053 AER LINGUS 055 ALITALIA 056 CYPRUS TURKISH AIRLINES 057 AIR FRANCE 058 INDIAN AIRLINES 060 FLIGHT WEST AIRLINES 061 AIR SEYCHELLES 062 DAN-AIR SERVICES 063 AIR CALEDONIE INTERNATIONAL 064 CSA CZECHOSLOVAK AIRLINES 065 SAUDI ARABIAN 066 NORONTAIR 067 AIR MOOREA 068 LAM-LINHAS AEREAS MOCAMBIQUE Page 2 of 19 Appendix 25 - SAD Box 31/3 Airline Codes March 2021 Airline code Code description 069 LAPA 070 SYRIAN ARAB AIRLINES 071 ETHIOPIAN AIRLINES 072 GULF AIR 073 IRAQI AIRWAYS 074 KLM ROYAL DUTCH AIRLINES 075 IBERIA 076 MIDDLE EAST AIRLINES 077 EGYPTAIR 078 AERO CALIFORNIA 079 PHILIPPINE AIRLINES 080 LOT POLISH AIRLINES 081 QANTAS AIRWAYS -

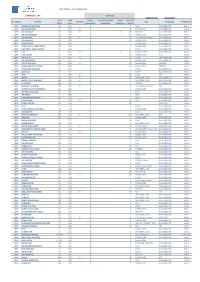

UPDATED ON: 18-03-2019 STATION AIRLINE IATA CODE AWB Prefix ON-LINE CARGO HANDLING FREIGHTER RAMP HANDLING RAMP LINEHAUL IMPORT

WFS CARGO - CUSTOMERS LIST DENMARK - CPH SERVICES UPDATED ON: 18-03-2019 IATA AWB CARGO FREIGHTER RAMP RAMP IMPORT STATION AIRLINE ON-LINE GSA TRUCKING TERMINAL CODE Prefix HANDLING HANDLING LINEHAUL EXPORT CPH AMERICAN AIRLINES AA 001 X E NAL WALLENBORN HAL 1 CPH DELTA AIRLINES DL 006 X X I/E PROACTIVE WALLENBORN HAL1 CPH AIR CANADA AC 014 X X X I/E HWF DK WALLENBORN HAL 1 CPH UNITED AIRLINES UA 016 X I/E NORDIC GSA WALLENBORN HAL1 CPH LUFTHANSA LH 020 X X I/E LUFTHANSA CARGO WALLENBORN HAL1 CPH US AIRWAYS US 037 X I/E NORDIC GSA WALLENBORN HAL1 CPH DRAGON AIR XH 043 X I NORDIC GSA WALLENBORN HAL1 CPH AEROLINEAS ARGENTINAS AR 044 X E CARGOCARE WALLENBORN HAL1 CPH LAN CHILE - LINEA AEREA LA 045 X E KALES WALLENBORN HAL1 CPH TAP TP 047 X X x I/E SCANPARTNER WALLENBORN HAL1 CPH AER LINGUS EI 053 X I/E NORDIC GSA N/A HAL1 CPH AIR France AF 057 X X I/E KL/AF KIM JOHANSEN HAL2 CPH AIR SEYCHELLES HM 061 X E NORDIC GSA WALLENBORN HAL1 CPH CZECH AIRLINES OK 064 X X I/E AviationPlus VARIOUS HAL1 CPH SAUDI AIRLINES CARGO SV 065 X I/E AviationPlus VARIOUS HAL1 CPH ETHIOPIAN AIRLINES ET 071 X E KALES WALLENBORN HAL1 CPH GULF AIR GF 072 X E KALES WALLENBORN HAL1 CPH KLM KL 074 X X I/E KL/AF JDR HAL2 CPH IBERIA IB 075 X X I/E UNIVERSAL GSA WALLENBORN HAL1 CPH MIDDLE EAST AIRLINES ME 076 X X E UNIVERSAL GSA WALLENBORN HAL1 CPH EGYPTAIR MS 077 X E HWF DK WALLENBORN HAL1 CPH BRUSSELS AIRLINES SN 020 X X I/E LUFTHANSA CARGO JDR HAL1 CPH SOUTH AFRICAN AIRWAYS SA 083 X E CARGOCARE WALLENBORN HAL1 CPH AIR NEW ZEALAND NZ 086 X E KALES WALLENBORN HAL1 CPH AIR -

Air Line Pilots Page 5 Association, International Our Skies

March 2015 ALSO IN THIS ISSUE: » Landing Your » Known Crewmember » Sleep Apnea Air Dream Job page 20 page 29 Update page 28 Line PilOt Safeguarding Official Journal of the Air Line Pilots page 5 Association, International Our Skies Follow us on Twitter PRINTED IN THE U.S.A. @wearealpa Sponsored Airline- Career Track ATP offers the airline pilot career training solution with a career track from zero time to 1500 hours sponsored by ATP’s airline alliances. Airline Career month FAST TRACK Demand for airline pilots and ATP graduates is soaring, Pilot Program with the “1500 hour rule” and retirements at the majors. AIRLINES Airlines have selected ATP as a preferred training provider to build their pilot pipelines Private, Instrument, Commercial Multi Also available with... & Certified Flight Instructor (Single, Multi 100 Hours Multi-Engine Experience with the best training in the fastest & Instrument) time frame possible. 225 Hours Flight Time / 100 Multi 230 Hours Flight Time / 40 Multi In the Airline Career Pilot Program, your airline Gain Access to More Corporate, Guaranteed Flight Instructor Job Charter, & Multi-Engine Instructor interview takes place during the commercial phase Job Opportunities of training. Successful applicants will receive a Airline conditional offer of employment at commercial phase of training, based on building Fly Farther & Faster with Multi- conditional offer of employment from one or more of flight experience to 1500 hours in your guaranteed Engine Crew Cross-Country ATP’s airline alliances, plus a guaranteed instructor CFI job. See website for participating airlines, Experience job with ATP or a designated flight school to build admissions, eligibility, and performance requirements. -

Air Transport Industry Analysis Report

Annual Analyses of the EU Air Transport Market 2016 Final Report March 2017 European Commission Annual Analyses related to the EU Air Transport Market 2016 328131 ITD ITA 1 F Annual Analyses of the EU Air Transport Market 2013 Final Report March 2015 Annual Analyses of the EU Air Transport Market 2013 MarchFinal Report 201 7 European Commission European Commission Disclaimer and copyright: This report has been carried out for the Directorate General for Mobility and Transport in the European Commission and expresses the opinion of the organisation undertaking the contract MOVE/E1/5-2010/SI2.579402. These views have not been adopted or in any way approved by the European Commission and should not be relied upon as a statement of the European Commission's or the Mobility and Transport DG's views. The European Commission does not guarantee the accuracy of the information given in the report, nor does it accept responsibility for any use made thereof. Copyright in this report is held by the European Communities. Persons wishing to use the contents of this report (in whole or in part) for purposes other than their personal use are invited to submit a written request to the following address: European Commission - DG MOVE - Library (DM28, 0/36) - B-1049 Brussels e-mail (http://ec.europa.eu/transport/contact/index_en.htm) Mott MacDonald, Mott MacDonald House, 8-10 Sydenham Road, Croydon CR0 2EE, United Kingdom T +44 (0)20 8774 2000 F +44 (0)20 8681 5706 W www.mottmac.com Issue and revision record StandardSta Revision Date Originator Checker Approver Description ndard A 28.03.17 Various K. -

Attachment F – Participants in the Agreement

Revenue Accounting Manual B16 ATTACHMENT F – PARTICIPANTS IN THE AGREEMENT 1. TABULATION OF PARTICIPANTS 0B 475 BLUE AIR AIRLINE MANAGEMENT SOLUTIONS S.R.L. 1A A79 AMADEUS IT GROUP SA 1B A76 SABRE ASIA PACIFIC PTE. LTD. 1G A73 Travelport International Operations Limited 1S A01 SABRE INC. 2D 54 EASTERN AIRLINES, LLC 2I 156 STAR UP S.A. 2I 681 21 AIR LLC 2J 226 AIR BURKINA 2K 547 AEROLINEAS GALAPAGOS S.A. AEROGAL 2T 212 TIMBIS AIR SERVICES 2V 554 AMTRAK 3B 383 Transportes Interilhas de Cabo Verde, Sociedade Unipessoal, SA 3E 122 MULTI-AERO, INC. DBA AIR CHOICE ONE 3J 535 Jubba Airways Limited 3K 375 JETSTAR ASIA AIRWAYS PTE LTD 3L 049 AIR ARABIA ABDU DHABI 3M 449 SILVER AIRWAYS CORP. 3S 875 CAIRE DBA AIR ANTILLES EXPRESS 3U 876 SICHUAN AIRLINES CO. LTD. 3V 756 TNT AIRWAYS S.A. 3X 435 PREMIER TRANS AIRE INC. 4B 184 BOUTIQUE AIR, INC. 4C 035 AEROVIAS DE INTEGRACION REGIONAL 4L 174 LINEAS AEREAS SURAMERICANAS S.A. 4M 469 LAN ARGENTINA S.A. 4N 287 AIR NORTH CHARTER AND TRAINING LTD. 4O 837 ABC AEROLINEAS S.A. DE C.V. 4S 644 SOLAR CARGO, C.A. 4U 051 GERMANWINGS GMBH 4X 805 MERCURY AIR CARGO, INC. 4Z 749 SA AIRLINK 5C 700 C.A.L. CARGO AIRLINES LTD. 5J 203 CEBU PACIFIC AIR 5N 316 JOINT-STOCK COMPANY NORDAVIA - REGIONAL AIRLINES 5O 558 ASL AIRLINES FRANCE 5T 518 CANADIAN NORTH INC. 5U 911 TRANSPORTES AEREOS GUATEMALTECOS S.A. 5X 406 UPS 5Y 369 ATLAS AIR, INC. 50 Standard Agreement For SIS Participation – B16 5Z 225 CEMAIR (PTY) LTD. -

Annual Report 2007

EU_ENTWURF_08:00_ENTWURF_01 01.04.2026 13:07 Uhr Seite 1 Analyses of the European air transport market Annual Report 2007 EUROPEAN COMMISSION EU_ENTWURF_08:00_ENTWURF_01 01.04.2026 13:07 Uhr Seite 2 Air Transport and Airport Research Annual analyses of the European air transport market Annual Report 2007 German Aerospace Center Deutsches Zentrum German Aerospace für Luft- und Raumfahrt e.V. Center in the Helmholtz-Association Air Transport and Airport Research December 2008 Linder Hoehe 51147 Cologne Germany Head: Prof. Dr. Johannes Reichmuth Authors: Erik Grunewald, Amir Ayazkhani, Dr. Peter Berster, Gregor Bischoff, Prof. Dr. Hansjochen Ehmer, Dr. Marc Gelhausen, Wolfgang Grimme, Michael Hepting, Hermann Keimel, Petra Kokus, Dr. Peter Meincke, Holger Pabst, Dr. Janina Scheelhaase web: http://www.dlr.de/fw Annual Report 2007 2008-12-02 Release: 2.2 Page 1 Annual analyses of the European air transport market Annual Report 2007 Document Control Information Responsible project manager: DG Energy and Transport Project task: Annual analyses of the European air transport market 2007 EC contract number: TREN/05/MD/S07.74176 Release: 2.2 Save date: 2008-12-02 Total pages: 222 Change Log Release Date Changed Pages or Chapters Comments 1.2 2008-06-20 Final Report 2.0 2008-10-10 chapters 1,2,3 Final Report - full year 2007 draft 2.1 2008-11-20 chapters 1,2,3,5 Final updated Report 2.2 2008-12-02 all Layout items Disclaimer and copyright: This report has been carried out for the Directorate-General for Energy and Transport in the European Commission and expresses the opinion of the organisation undertaking the contract TREN/05/MD/S07.74176. -

363 Part 238—Contracts With

Immigration and Naturalization Service, Justice § 238.3 (2) The country where the alien was mented on Form I±420. The contracts born; with transportation lines referred to in (3) The country where the alien has a section 238(c) of the Act shall be made residence; or by the Commissioner on behalf of the (4) Any country willing to accept the government and shall be documented alien. on Form I±426. The contracts with (c) Contiguous territory and adjacent transportation lines desiring their pas- islands. Any alien ordered excluded who sengers to be preinspected at places boarded an aircraft or vessel in foreign outside the United States shall be contiguous territory or in any adjacent made by the Commissioner on behalf of island shall be deported to such foreign the government and shall be docu- contiguous territory or adjacent island mented on Form I±425; except that con- if the alien is a native, citizen, subject, tracts for irregularly operated charter or national of such foreign contiguous flights may be entered into by the Ex- territory or adjacent island, or if the ecutive Associate Commissioner for alien has a residence in such foreign Operations or an Immigration Officer contiguous territory or adjacent is- designated by the Executive Associate land. Otherwise, the alien shall be de- Commissioner for Operations and hav- ported, in the first instance, to the ing jurisdiction over the location country in which is located the port at where the inspection will take place. which the alien embarked for such for- [57 FR 59907, Dec. 17, 1992] eign contiguous territory or adjacent island. -

Global Aviation Holdings: the KERP Is Back

Portfolio Media. Inc. | 860 Broadway, 6th Floor | New York, NY 10003 | www.law360.com Phone: +1 646 783 7100 | Fax: +1 646 783 7161 | [email protected] Global Aviation Holdings: The KERP Is Back Law360, New York (August 06, 2012, 1:11 PM ET) -- In a recent decision[1] involving Global Aviation Holdings Inc. and its affiliated debtors (collectively, the “debtors”), the United States Bankruptcy Court for the Eastern District of New York granted the debtors' motion for approval of a key employee retention plan (the “KERP motion”) pursuant to Sections 363(b) and 503(c)(3) of Title 11 of the United States Code over the objections of both the United States Trustee for Region 2 (the “UST”) and the official committee of unsecured creditors (the “committee”). In the objections, the committee and the UST argued the debtors were seeking to pay bonuses to insiders without satisfying the requirements set forth in Section 503(c)(1) of the Bankruptcy Code. The committee and the UST also argued, that to the extent the key employee retention plan recipients turned out to be non-insiders, the debtors did not establish whether the proposed key employee retention plan payments were “justified by the facts and circumstances of the case” as required by Section 503(c)(3) of the Bankruptcy Code. The debtors operate two airlines: North American Airlines Inc. and World Airways Inc. From the outset of their bankruptcy cases, the debtors planned to move North American’s headquarters from JFK International Airport in Jamaica, N.Y., to World’s headquarters in Peachtree City, Ga., in order to consolidate operations. -

North American Airlines Take Off by Alan Wise, Ketil Gjerstad, Marguerite Fitzgerald, and Jason Guggenheim

The 2017 Consumer Value Creators Series NorTh AmeriCAN AirliNeS TAke off By Alan Wise, Ketil Gjerstad, Marguerite Fitzgerald, and Jason Guggenheim he airline industry is dominating The Top Ten Tthe travel and tourism sector—out- Of the top ten performers on this year’s pacing hotels, cruise lines, and others in travel and tourism list, nine are in the air- the sector in terms of value creation. North line industry and seven are based in North American carriers in particular have bene- America. (See the exhibit.) That includes fited from restructuring, scale efficiencies, five US carriers: and consolidation over the past decade, giving them a strong position and lower • Hawaiian Holdings, parent company of costs in a robust market. Hawaiian Airlines (which finished first) In 2017, The Boston Consulting Group con- • Delta Air Lines (fourth) ducted its annual study of the total share- holder return (TSR) of more than 2,300 • Southwest Airlines (fifth) publicly traded companies in 33 industry sectors, including 80 companies in travel • Alaska Air Group (sixth) and tourism. (See “How Top Value Creators Outpace the Market—for Decades,” BCG • JetBlue Airways (tenth) article, July 2017.) It’s tempting to cite lower fuel costs as the From 2012 through 2016, the global travel reason for this collective strength, but and tourism sector delivered an average that’s likely a subordinate factor at best. annual return of 19%. It ranked ninth Lower fuel prices affect all carriers world- among the 33 sectors we analyzed and sec- wide, not only those in the US. ond among the five consumer segments.