Draft Water Resources Management Plan Anglian Water 2008

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

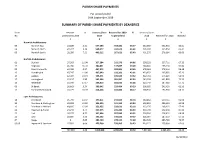

Parish Share Report

PARISH SHARE PAYMENTS For period ended 30th September 2019 SUMMARY OF PARISH SHARE PAYMENTS BY DEANERIES Dean Amount % Deanery Share Received for 2019 % Deanery Share % No Outstanding 2018 2019 to period end 2018 Received for 2018 received £ £ £ £ £ Norwich Archdeaconry 06 Norwich East 23,500 4.41 557,186 354,184 63.57 532,380 322,654 60.61 04 Norwich North 47,317 9.36 508,577 333,671 65.61 505,697 335,854 66.41 05 Norwich South 28,950 7.21 409,212 267,621 65.40 401,270 276,984 69.03 Norfolk Archdeaconry 01 Blofield 37,303 11.04 327,284 212,276 64.86 338,033 227,711 67.36 11 Depwade 46,736 16.20 280,831 137,847 49.09 288,484 155,218 53.80 02 Great Yarmouth 44,786 9.37 467,972 283,804 60.65 478,063 278,114 58.18 13 Humbleyard 47,747 11.00 437,949 192,301 43.91 433,952 205,085 47.26 14 Loddon 62,404 19.34 335,571 165,520 49.32 322,731 174,229 53.99 15 Lothingland 21,237 3.90 562,194 381,997 67.95 545,102 401,890 73.73 16 Redenhall 55,930 17.17 339,813 183,032 53.86 325,740 187,989 57.71 09 St Benet 36,663 9.24 380,642 229,484 60.29 396,955 243,433 61.33 17 Thetford & Rockland 31,271 10.39 314,266 182,806 58.17 300,933 192,966 64.12 Lynn Archdeaconry 18 Breckland 45,799 11.97 397,811 233,505 58.70 382,462 239,714 62.68 20 Burnham & Walsingham 63,028 15.65 396,393 241,163 60.84 402,850 256,123 63.58 12 Dereham in Mitford 43,605 12.03 353,955 223,631 63.18 362,376 208,125 57.43 21 Heacham & Rising 24,243 6.74 377,375 245,242 64.99 359,790 242,156 67.30 22 Holt 28,275 8.55 327,646 207,089 63.21 330,766 214,952 64.99 23 Lynn 10,805 3.30 330,152 196,022 59.37 326,964 187,510 57.35 07 Repps 0 0.00 383,729 278,123 72.48 382,728 285,790 74.67 03 08 Ingworth & Sparham 27,983 6.66 425,260 239,965 56.43 420,215 258,960 61.63 727,583 9.28 7,913,818 4,789,282 60.52 7,837,491 4,895,456 62.46 01/10/2019 NORWICH DIOCESAN BOARD OF FINANCE LTD DEANERY HISTORY REPORT MONTH September YEAR 2019 SUMMARY PARISH 2017 OUTST. -

Climate Change Adaptation Report Consultation

Climate Change Adaptation Report Consultation 1 Online questionnaire responses Please note: all consultation responses have been published verbatim without edits. Do you support Are there any further Do you agree our adaptation opportunities to Comments in response to further Type of with our Comments in response to Anglian Water’s Comments in response to Anglian Water’s Anglian Water’s (brief) response to Organisation strategy and collaborate and opportunities to collaborate and solve Organisation assessment of assessment of climate risks adaptation strategy and proposed actions consultation comments the actions we solve problems in problems in partnership climate risks? propose to take? partnership? University Cardiff University/ Y None Y An important element of future plans is Y Following on from our previous comment. We agree. For the past three years we have Centre for demand reduction. We strongly support this There is an opportunity to research how been trialling a second generation of smart Climate Change strategy. However, it also appears that a smart meters may help (or not) reduce meters, in two areas: Newmarket (Suffolk) and Social substantial section of demand reduction will water demand. It may also be interesting and part of Norwich. The Newmarket trial has Transformations be driven by smart metering. It is not clear to examine how different elements of the been combined with a whole-town focus on how successful this will be. Studies on energy demand reduction strategies can work in water efficiency and wider communications smart meters has shown that it may lead to parallel and therefore lead to greater savings about water. -

Contents of Volume 14 Norwich Marriages 1813-37 (Are Distinguished by Letter Code, Given Below) Those from 1801-13 Have Also Been Transcribed and Have No Code

Norfolk Family History Society Norfolk Marriages 1801-1837 The contents of Volume 14 Norwich Marriages 1813-37 (are distinguished by letter code, given below) those from 1801-13 have also been transcribed and have no code. ASt All Saints Hel St. Helen’s MyM St. Mary in the S&J St. Simon & St. And St. Andrew’s Jam St. James’ Marsh Jude Aug St. Augustine’s Jma St. John McC St. Michael Coslany Ste St. Stephen’s Ben St. Benedict’s Maddermarket McP St. Michael at Plea Swi St. Swithen’s JSe St. John Sepulchre McT St. Michael at Thorn Cle St. Clement’s Erh Earlham St. Mary’s Edm St. Edmund’s JTi St. John Timberhill Pau St. Paul’s Etn Eaton St. Andrew’s Eth St. Etheldreda’s Jul St. Julian’s PHu St. Peter Hungate GCo St. George Colegate Law St. Lawrence’s PMa St. Peter Mancroft Hei Heigham St. GTo St. George Mgt St. Margaret’s PpM St. Peter per Bartholomew Tombland MtO St. Martin at Oak Mountergate Lak Lakenham St. John Gil St. Giles’ MtP St. Martin at Palace PSo St. Peter Southgate the Baptist and All Grg St. Gregory’s MyC St. Mary Coslany Sav St. Saviour’s Saints The 25 Suffolk parishes Ashby Burgh Castle (Nfk 1974) Gisleham Kessingland Mutford Barnby Carlton Colville Gorleston (Nfk 1889) Kirkley Oulton Belton (Nfk 1974) Corton Gunton Knettishall Pakefield Blundeston Cove, North Herringfleet Lound Rushmere Bradwell (Nfk 1974) Fritton (Nfk 1974) Hopton (Nfk 1974) Lowestoft Somerleyton The Norfolk parishes 1 Acle 36 Barton Bendish St Andrew 71 Bodham 106 Burlingham St Edmond 141 Colney 2 Alburgh 37 Barton Bendish St Mary 72 Bodney 107 Burlingham -

Service Connections User Guide

Service connections user guide March 2021 Developer Services Service connection user guide About South Staffs and Cambridge Water South Staffordshire Water PLC (‘South Staffs Water’) is part of the South Staffordshire Plc group of companies, a privately-owned integrated services group concentrating on regulated water supply and complementary specialist service businesses. We operate across two regions under a single water supply licence, providing clean water services to more than 1.7 million people and around 43,000 businesses in Staffordshire, parts of the West Midlands, and in and around Cambridge. Our South Staffs region extends from Ashbourne in the north to Halesowen in the south, and from Burton-upon-Trent in the east to Kinver in the west. Our Cambridge region stretches from Ramsey in the north to beyond Melbourn in the south, and from Gamlingay in the west to the east of Cambridge city. Cambridge region South Staffs region 1 Developer Services Service connection user guide Contents About South Staffs and Cambridge Water ................................................................................ 1 Contents .................................................................................................................................... 2 1. Introduction ........................................................................................................................... 3 2. Who can complete this work?............................................................................................... 5 3. What is the process -

Completed Acquisition by South Staffordshire Plc of Cambridge Water Plc

Completed acquisition by South Staffordshire plc of Cambridge Water plc ME/5254/11 The OFT's decision on reference under section 32(b) given on 5 January 2012. Full text of decision published 9 January 2012. Please note that the square brackets indicate figures or text which have been deleted or replaced in ranges at the request of the parties or third parties for reasons of commercial confidentiality. PARTIES 1. South Staffordshire Plc ('South Staffordshire') is a public company limited by shares and incorporated in the United Kingdom. South Staffordshire owns South Staffordshire Water Plc ('South Staffordshire Water') and is the holding company for a number of non-regulated service businesses that operate predominantly in the UK water sector. South Staffordshire is an indirect wholly-owned subsidiary of investment funds management by Alinda Capital Partners LLC. 2. South Staffordshire Water is a water company whose assets include a network infrastructure (mains infrastructure, water treatment works and pumping stations) for the supply of water in the South Staffordshire area and does not have regulated sewerage businesses. South Staffordshire also has a number of subsidiaries providing non- regulated business activities. The turnover for the year ended 31 March 2011 for both South Staffordshire and South Staffordshire Water was £159.5 million and £87.8 million respectively. 1 3. Cambridge Water plc ('Cambridge Water') was a wholly-owned subsidiary of HSBC Bank Plc ('HSBC')1 (until its acquisition by South Staffordshire Plc on 3 October 2011). 4. Cambridge Water is also a water company that owns a network infrastructure (mains infrastructure, water treatment works and pumping stations) for the supply of water in the Cambridge area and does not have regulated sewerage businesses. -

The Stewards House, Binham

The Stewards House, Binham The Stewards House, Blacksmiths Yard, Binham, Norfolk, NR21 0AL North Norfolk Coast 2 miles, Norwich 20 miles Holt 7 miles A rare opportunity to acquire a Grade II listed traditional brick and flint house tucked away in a quiet location, just off the village centre. Having been tastefully re-furbished throughout, the property would make an excellent permanent or holiday home. Guide Price £450,000 The Property The property offered for sale is a Grade II listed traditional brick and flint house ACCOMMODATION under a pantile roof, delightfully situated in the heart of this popular North Norfolk village. The property enjoys a high degree of privacy being well set back from the The accommodation comprises - road. Having recently been fully refurbished to a very high standard whilst maintaining many of its original features, the property would make an ideal permanent or holiday home. The accommodation comprises an entrance hall, a Entrance Door double aspect sitting room with an open fireplace, a double aspect dining room Leading to:- and a handmade bespoke kitchen built and fitted by local craftsman Samphire Interiors, and a shower room. A first floor landing leads to three double bedrooms and a family bathroom. The double aspect features in many of the rooms make Entrance Hall the property light and airy. Outside there is a shingled parking area which in turn Oak flooring, radiator, coat pegs, staircase to the first floor. leads to a large detached garage, a particular feature of this property is the rear garden that is due south facing. The property is being sold with no upward chain. -

The Cromer Moraine

THE CROMER MORAINE - A STUDY OF ITS PROGRESSIVE RECLAMATION ELIZABETH LANGTON ProQuest Number: 10097240 All rights reserved INFORMATION TO ALL USERS The quality of this reproduction is dependent upon the quality of the copy submitted. In the unlikely event that the author did not send a complete manuscript and there are missing pages, these will be noted. Also, if material had to be removed, a note will indicate the deletion. uest. ProQuest 10097240 Published by ProQuest LLC(2016). Copyright of the Dissertation is held by the Author. All rights reserved. This work is protected against unauthorized copying under Title 17, United States Code. Microform Edition © ProQuest LLC. ProQuest LLC 789 East Eisenhower Parkway P.O. Box 1346 Ann Arbor, Ml 48106-1346 ilBSTRAGT The Cromer Moraine forms a distinctive geographical region near the coast of the northern part of the County of Norfolk. A pro nounced characteristic of this region is the vridespread cover of heatb-land, far less extensive than in former times. This heathland appears in its turn to have developed from an original woodland cover which was destroyed by the depredations of man and his domesticated animals . It has been necessary first to delimit the region as accurately as possible and this has been accomplished by means of a detailed study of local topography and of well-sections. The earliest evidence of the location of heathland comes from tlie Domesday Survey and this has been confirmed by references to heathland in various other documents dovm to 1750. By the middle of the eighteenth century the new developments in agriculture^ or ’Norfolk Husbandry’ as it was called, became widely known and practised, resulting in this region in a greatly accelerated reclama tion of heathland; so that by the time of the Tithe Survey (183S-42) less than a hundred years later over 4000 acres of heath had been reclaimed. -

North Norfolk District Council (Alby

DEFINITIVE STATEMENT OF PUBLIC RIGHTS OF WAY NORTH NORFOLK DISTRICT VOLUME I PARISH OF ALBY WITH THWAITE Footpath No. 1 (Middle Hill to Aldborough Mill). Starts from Middle Hill and runs north westwards to Aldborough Hill at parish boundary where it joins Footpath No. 12 of Aldborough. Footpath No. 2 (Alby Hill to All Saints' Church). Starts from Alby Hill and runs southwards to enter road opposite All Saints' Church. Footpath No. 3 (Dovehouse Lane to Footpath 13). Starts from Alby Hill and runs northwards, then turning eastwards, crosses Footpath No. 5 then again northwards, and continuing north-eastwards to field gate. Path continues from field gate in a south- easterly direction crossing the end Footpath No. 4 and U14440 continuing until it meets Footpath No.13 at TG 20567/34065. Footpath No. 4 (Park Farm to Sunday School). Starts from Park Farm and runs south westwards to Footpath No. 3 and U14440. Footpath No. 5 (Pack Lane). Starts from the C288 at TG 20237/33581 going in a northerly direction parallel and to the eastern boundary of the cemetery for a distance of approximately 11 metres to TG 20236/33589. Continuing in a westerly direction following the existing path for approximately 34 metres to TG 20201/33589 at the western boundary of the cemetery. Continuing in a generally northerly direction parallel to the western boundary of the cemetery for approximately 23 metres to the field boundary at TG 20206/33611. Continuing in a westerly direction parallel to and to the northern side of the field boundary for a distance of approximately 153 metres to exit onto the U440 road at TG 20054/33633. -

All Company Working Group Joint Document

Representations: Strategic regional water resource solutions joint statement Document Reference: J007a This document is the joint representation with the other companies with strategic water resources schemes: Affinity Water, Anglian Water, Severn Trent Water, Southern Water, South West, Thames Water, Wessex and Water Resources South East. In this document general matters, which reflects the agreed position of all the companies United Utilities Water Limited Strategic regional water resource solutions Affinity Water, Anglian Water, Severn Trent Water, Southern Water, South West, Thames Water, United Utilities, Wessex Water 30 August 2019 Joint Company Statement Following the Draft Determination (DD) the working group has met several times to continue to work collaboratively to optimise the processes for developing the next set of strategic water resource solutions. The DD has added some additional options into the mix of schemes as well as increasing the number of companies working across the schemes from six to eight. These additional companies and schemes are welcomed as they will help provide additional choices when deriving the best value plans for customers, stakeholders and the environment. Our engagement with the regulators during the development of the plan have continued to help and shape this response. The recent meetings with RAPID, EA and Ofwat (in July and August) have been very encouraging and we look forward to working collaboratively to align the gated processes, national framework timetables and statutory planning processes. We want to ensure that the timetables and processes are efficient and co-ordinated, and we believe we can achieve this through a few simple re-alignments of some of the gates during the process. -

Premises, Sites Etc Within 30 Miles of Harrington Museum Used for Military Purposes in the 20Th Century

Premises, Sites etc within 30 miles of Harrington Museum used for Military Purposes in the 20th Century The following listing attempts to identify those premises and sites that were used for military purposes during the 20th Century. The listing is very much a works in progress document so if you are aware of any other sites or premises within 30 miles of Harrington, Northamptonshire, then we would very much appreciate receiving details of them. Similarly if you spot any errors, or have further information on those premises/sites that are listed then we would be pleased to hear from you. Please use the reporting sheets at the end of this document and send or email to the Carpetbagger Aviation Museum, Sunnyvale Farm, Harrington, Northampton, NN6 9PF, [email protected] We hope that you find this document of interest. Village/ Town Name of Location / Address Distance to Period used Use Premises Museum Abthorpe SP 646 464 34.8 km World War 2 ANTI AIRCRAFT SEARCHLIGHT BATTERY Northamptonshire The site of a World War II searchlight battery. The site is known to have had a generator and Nissen huts. It was probably constructed between 1939 and 1945 but the site had been destroyed by the time of the Defence of Britain survey. Ailsworth Manor House Cambridgeshire World War 2 HOME GUARD STORE A Company of the 2nd (Peterborough) Battalion Northamptonshire Home Guard used two rooms and a cellar for a company store at the Manor House at Ailsworth Alconbury RAF Alconbury TL 211 767 44.3 km 1938 - 1995 AIRFIELD Huntingdonshire It was previously named 'RAF Abbots Ripton' from 1938 to 9 September 1942 while under RAF Bomber Command control. -

Wildlife-Sites-Guide.Pdf

o er’s A Guide t at Sites W life n ild Anglia W O io Our Sites Our Region ur Reg n 1 Alton Water p6 Holbrook Road, Stutton, Suffolk, IP9 2RY 14 2 Covenham Reservoir p9 Bull Bank, Louth, Lincolnshire, LN11 0PA 2 3 Dereham Rushmeadow p10 Rushmeadow Road, Dereham, Norfolk, NR19 2NW Foxcote Road, Buckingham, Buckinghamshire, 4 Foxcote Reservoir p13 MK18 1QQ Grafham Water Fishing Lodge, West Perry, Huntingdon, Grafham Water p14 5 Cambridgeshire, PE28 0BX 8 3 13 6 Hollowell Reservoir p17 Guilsborough Hill, Hollowell, Northampton NN6 8RN 12 7 Lexden Gathering Grounds p18 Cooks Lane, Colchester, Essex, CO3 4DB 6 11 10 8 Marham Fen p21 Hoggs Drove, Marham, King’s Lynn, Norfolk, PE33 9JW 5 9 1 Woodbridge Lane, Newbourne, Ipswich, Suffolk, 9 Newbourne Springs p22 IP12 4NY 4 7 Brixworth Rd, Northampton, Northamptonshire, 10 Pitsford Water p25 NN6 9BN Teeton Rd, Ravensthorpe, Northampton, Ravensthorpe Reservoir p26 11 Northamptonshire, NN6 8EJ Rutland Water Nature Reserve, Egleton, Oakham, 12 Rutland Water p29 Rutland, LE15 8BT Taverham Mill, Costessey Rd, Taverham, Norwich, Taverham Mill p30 13 Norfolk, NR8 6TA Key Icons Parking Cafe No dogs allowed Permit required 14 Tetney Blow Wells p33 Church Lane, Tetney, Grimsby, Lincolnshire, DN36 5JX Accomodation WC Toilets Guide Dogs Only Dogs on leads 2 Anglian Water Services Limited A Guide To Anglian Water’s Wildlife Sites Anglian Water Services Limited A Guide To Anglian Water’s Wildlife Sites 3 Whether you’re a keen explorer and bird watcher or just like getting out of the house, you may be surprised to hear about the number of sites we are responsible for. -

NCA Profile 42 Lincolnshire Coast and Marshes

National Character 42. Lincolnshire Coast and Marshes Area profile: Supporting documents www.gov.uk/natural-england 1 National Character 42. Lincolnshire Coast and Marshes Area profile: Supporting documents Introduction National Character Areas map As part of Natural England’s responsibilities as set out in the Natural Environment White Paper,1 Biodiversity 20202 and the European Landscape Convention,3 we are revising profiles for England’s 159 National Character Areas North (NCAs). These are areas that share similar landscape characteristics, and which East follow natural lines in the landscape rather than administrative boundaries, making them a good decision-making framework for the natural environment. Yorkshire & The North Humber NCA profiles are guidance documents which can help communities to inform West their decision-making about the places that they live in and care for. The information they contain will support the planning of conservation initiatives at a East landscape scale, inform the delivery of Nature Improvement Areas and encourage Midlands broader partnership working through Local Nature Partnerships. The profiles will West also help to inform choices about how land is managed and can change. Midlands East of Each profile includes a description of the natural and cultural features England that shape our landscapes, how the landscape has changed over time, the current key drivers for ongoing change, and a broad analysis of each London area’s characteristics and ecosystem services. Statements of Environmental South East Opportunity (SEOs) are suggested, which draw on this integrated information. South West The SEOs offer guidance on the critical issues, which could help to achieve sustainable growth and a more secure environmental future.