Telecommunications Predictions 2010

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Raketu to Add Mobility to Web-Based Voip | Infoworld | News | 2007-06-15 | by John Bl

Raketu to add mobility to Web-based VoIP | InfoWorld | News | 2007-06-15 | By John Bl... Page 1 of 4 HOME NEWS TECHNOLOGIES BLOGS/COLUMNS TEST CENTER AUDIO/VIDEO CAREERS IT EXEC-CONNEC Raketu to add mobility to Web-based VoIP New version of the Raketu application will let users make VoIP calls, send text messages, A and chat from cell phone By John Blau, IDG News Service Talkback E-mail Printer Friendly June 15, 2007 A Raketu Communications will add two new mobile phone features to its integrated communications, entertainment, and social networking service in a move to attract consumers on the go. Next week, Raketu will introduce a new domain, www.raketu.mobi, which will allow Free IT resource mobile phone users to more easily navigate the Raketu site and use services such as the company's RakWeb service launched earlier this week, said CEO Greg Learn about the energy Parker in an interview. efficiency in EMC's Pund- IT report on power conservation. By the end of the month, the company intends to launch a new mobile phone version of the Raketu application, which users can install on their phones to make VoIP calls, Sponsored by EMC send text messages, chat, and more, Parker said. Free IT resource Raketu, which is based in New York, is trying to carve out a niche in the highly competitive market for Web-based services by offering an integrated Download the Windows communications, online entertainment, and social networking service that can be Server(R) 2008 Beta: Join the global community. used on both desktop PCs and mobile phones. -

Uila Supported Apps

Uila Supported Applications and Protocols updated Oct 2020 Application/Protocol Name Full Description 01net.com 01net website, a French high-tech news site. 050 plus is a Japanese embedded smartphone application dedicated to 050 plus audio-conferencing. 0zz0.com 0zz0 is an online solution to store, send and share files 10050.net China Railcom group web portal. This protocol plug-in classifies the http traffic to the host 10086.cn. It also 10086.cn classifies the ssl traffic to the Common Name 10086.cn. 104.com Web site dedicated to job research. 1111.com.tw Website dedicated to job research in Taiwan. 114la.com Chinese web portal operated by YLMF Computer Technology Co. Chinese cloud storing system of the 115 website. It is operated by YLMF 115.com Computer Technology Co. 118114.cn Chinese booking and reservation portal. 11st.co.kr Korean shopping website 11st. It is operated by SK Planet Co. 1337x.org Bittorrent tracker search engine 139mail 139mail is a chinese webmail powered by China Mobile. 15min.lt Lithuanian news portal Chinese web portal 163. It is operated by NetEase, a company which 163.com pioneered the development of Internet in China. 17173.com Website distributing Chinese games. 17u.com Chinese online travel booking website. 20 minutes is a free, daily newspaper available in France, Spain and 20minutes Switzerland. This plugin classifies websites. 24h.com.vn Vietnamese news portal 24ora.com Aruban news portal 24sata.hr Croatian news portal 24SevenOffice 24SevenOffice is a web-based Enterprise resource planning (ERP) systems. 24ur.com Slovenian news portal 2ch.net Japanese adult videos web site 2Shared 2shared is an online space for sharing and storage. -

Private Placement Memorandum

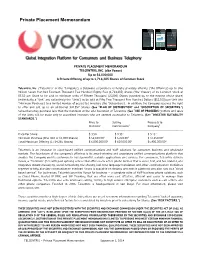

Private Placement Memorandum Global Integration Platform for Consumers and Business Telephony PRIVATE PLACEMENT MEMORANDUM TELCENTRIS, INC. (dba Voxox) Up to $6,000,000 A Private Offering of up to 1,714,285 Shares of Common Stock Telcentris, Inc. (“Telcentris” or the “Company”), a Delaware corporation, is hereby privately offering (“the Offering”) up to One Million Seven Hundred Fourteen Thousand Two Hundred Eighty Five (1,714,285) shares (“the Shares”) of its Common Stock at $3.50 per Share to be sold in minimum units of Fifteen Thousand (15,000) Shares (rounded up to the nearest whole share) (individually a “Unit” and collectively the “Units”) to be sold at Fifty Two Thousand Five Hundred Dollars ($52,500) per Unit (the “Minimum Purchase”) to a limited number of accredited investors (the “Subscribers”). In addition, the Company reserves the right to offer and sell up to an additional 342,857 Shares. (See “PLAN OF DISTRIBUTION” and “DESCRIPTION OF SECURITIES.”) Subscribers may purchase less than the minimum at the sole discretion of Telcentris. (See “USE OF PROCEEDS.”) Offers and sales of the Units will be made only to accredited investors who are deemed acceptable to Telcentris. (See “INVESTOR SUITABILITY STANDARDS.”) Price to Selling Proceeds to Investors1 Commissions2 Company3 -------------------------------------------------------------------------------------------------------------------------------------------- Price Per Share: $ 3.50 $ 0.352 $ 3.153 Minimum Purchase (One Unit or 15,000 Shares) $ 52,500.001 $ 5,250.002 $ 47,250.003 Total Maximum Offering (1,714,285 Shares) $ 6,000,000.001 $ 600,000.002 $5,400,000.003 -------------------------------------------------------------------------------------------------------------------------------------------- Telcentris is an innovator in cloud-based unified communications and VoIP solutions for consumer, business and wholesale markets. -

Through the Mobile Looking Glass

The Connected World Through the Mobile Looking Glass The Transformative Potential of Mobile Technologies The Boston Consulting Group (BCG) is a global management consulting firm and the world’s leading advisor on business strategy. We partner with clients from the private, public, and not-for- profit sectors in all regions to identify their highest-value opportunities, address their most critical challenges, and transform their enterprises. Our customized approach combines deep in sight into the dynamics of companies and markets with close collaboration at all levels of the client organization. This ensures that our clients achieve sustainable compet itive advantage, build more capable organizations, and secure lasting results. Founded in 1963, BCG is a private company with 78 offices in 43 countries. For more information, please visit bcg.com. The Connected World Through the Mobile Looking Glass The Transformative Potential of Mobile Technologies David Dean, Mark Louison, Hajime Shoji, Sampath Sowmyanarayan, and Arvind Subramanian April 2013 AT A GLANCE As mobile access overtakes fixed-line access as the world’s primary way of going online, numerous factors are converging to give mobile the capabilities, scale, and reach achieved by few other technological advances. Mobile Models Take Shape The global playing field is uneven, but this does not necessarily benefit rich coun- tries or nations with extensive telecommunications networks. Mobile is developing along different lines in different markets, driving new waves of innovation around the world. A Complex Policy Agenda Mobile and its impact are evolving faster than the ability of policymakers to deal with them. A Mobile Health Check for Companies Companies need to ask: Can consumers and employees engage with us through the device of their choosing, at a time and place of their determination, and come away from the experience satisfied and having accomplished what they set out to do? 2 Through the Mobile Looking Glass lice never dreamed of a world like this. -

IP Phones, Software Voip, and Integrated and Mobile Voip

Chapter 2 IP Phones, Software VoIP, and Integrated and Mobile VoIP Abstract In order to establish their technical, communication, and service affordances, this chapter explores and three types of VoIP tools: 1) IP Phones, 2) software VoIP, and 3) mobile and integrated VoIP. Type 1: IP Phones Another reply to my e-mail list call-out came from consul- tant Susan Knoer, who reflected: VoIP is an old technology now, and many people didn’t even realize that their “new” phone lines are VoIP. Even the smaller corporations I work with have ReportsLibrary Technology gone over. It might be more interesting to talk to campuses that don’t have VoIP and find out why.1 Figure 5 Cisco Ip phone handset. Excellent point, Susan. The first VoIP type I explore is the most institutionally established yet least obvious hardware externals they are also virtually indistinguish- form of networked calling: the mass-market carrier IP able from older phones (figure 5). Broadband IP calls are phones sitting inconspicuously on desks at a growing initiated with either specially made IP handsets or head- number of offices and homes. Digital voice is becoming sets or with existing handsets converted with adapters. standard for schools, organizations, and business, which Unlike the small-scale startup culture of software VoIP, still tend to rely on fixed-location communication. As IP IP phones tend to follow a more traditional provider- www.alatechsource.org phones are bundled with high-speed Internet and televi- subscriber customer service model. These characteristics sion subscriptions, individual consumers still interested make IP calling an easier conceptual leap for users who in landline service are steadily adopting them, as well. -

Form-20-F 2007

As filed with the Securities and Exchange Commission on February 28, 2008 UNITED STATES SECURITIES AND EXCHANGE COMMISSION Form 20-F È ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2007 Commission file number 001-14540 Deutsche Telekom AG (Exact Name of Registrant as Specified in its Charter) Federal Republic of Germany (Jurisdiction of Incorporation or Organization) Friedrich-Ebert-Allee 140, 53113 Bonn, Germany (Address of Registrant’s Principal Executive Offices) Guido Kerkhoff Chief Accounting Officer Deutsche Telekom AG Friedrich-Ebert-Allee 140, 53113 Bonn, Germany +49-228-181-0 [email protected] (Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person) Securities registered or to be registered pursuant to Section 12(b) of the Act: Title of each class Name of each exchange on which registered American Depositary Shares, each representing New York Stock Exchange one Ordinary Share Ordinary Shares, no par value New York Stock Exchange* Securities registered or to be registered pursuant to Section 12(g) of the Act: NONE (Title of Class) Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: NONE (Title of Class) Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report: Ordinary Shares, no par value: 4,361,297,603 (as of December 31, 2007) Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. -

Online Identifiers in Everyday Life

© 2010 by Benjamin M. Gross. All rights reserved. ONLINE IDENTIFIERS IN EVERYDAY LIFE BY BENJAMIN M. GROSS DISSERTATION Submied in partial fulfillment of the requirements for the degree of Doctor of Philosophy in Library and Information Science in the Graduate College of the University of Illinois at Urbana-Champaign, 2010 Urbana, Illinois Doctoral Commiee: Associate Professor Michael Twidale, Chair Professor Geof Bowker, University of Pisburgh Professor Chip Bruce Associate Professor Ann Bishop Abstract Identifiers are an essential component of online communication. Email addresses and instant messenger usernames are two of the most common online identi- fiers. is dissertation focuses on the ways that social, technical and policy fac- tors affect individual’s behavior with online identifiers. Research for this dissertation was completed in two parts, an interview-based study drawn from two populations and an examination of the infrastructure for managing identifiers in two large consumer services. e exploratory study ex- amines how individuals use online identifiers to segment and integrate aspects of their lives. e first population is drawn from employees of a financial ser- vice firm with substantial constraints on communication in the workplace. e second population is drawn from a design firm with minimal constraints on com- munication. e two populations provide the opportunity to explore the social, technical, and policy issues that arise from diverse communication needs, uses, strategies, and technologies. e examination of systems focuses on the infras- tructure that Google and Yahoo! provide for individuals to manage their iden- tifiers across multiple services, and the risks and benefits of employing single sign-on systems. -

Visual Advertising in Voice-Over-IP Calls

Master in Informatics Engineering Internship Final Report Visual Advertising in Voice-over-IP calls David Joaquim Monteiro Colaço Salvador [email protected] DEI Supervisor: Prof. Dr. Luís Cordeiro Wit-Software Supervisor: Eng. Rafael Maia Data: 28th January 2014 Abstract Nowadays, with the spread of Smartphones and Internet worldwide, a new way of communicate has arrived. A telephone is no longer an instrument to make calls. It is used for work, play or for fast access to news and other media content. With the increase speed of the Internet in mobile devices, some companies saw an opportunity to develop successful applications, known as Over-The-Top applications. Some of these OTTs offer the same products as the telecommunications companies at a lower price, or even for free. This lead to two major problems: a decrease in revenue on the Telecommunications market, and a demand for faster access to the internet. A response to OTTs emerged from the Telecommunications world with the creation of the Rich Communications Services (RCS). This specification provides the user new ways to communicate and share content. It was also clear to the telecommunications industry that an improvement to the network was needed and the migration from Circuit Switch to all IP networks was essential. From this need, the 3GPP group created the IP Multimedia Subsystem (IMS). This network architecture can deliver services and multimedia content using industry standards and provide compatibility across all operators and legacy networks. On this project, a new service is added to the IMS network, in order to deliver image and video advertisement to RCS clients. -

Cisco SCA BB Protocol Reference Guide

Review Draft - Cisco Confidential Cisco Service Control Application for Broadband Protocol Reference Guide Protocol Pack #55 November 28, 2016 Cisco Systems, Inc. www.cisco.com Cisco has more than 200 offices worldwide. Addresses, phone numbers, and fax numbers are listed on the Cisco website at www.cisco.com/go/offices. THE SPECIFICATIONS AND INFORMATION REGARDING THE PRODUCTS IN THIS MANUAL ARE SUBJECT TO CHANGE WITHOUT NOTICE. ALL STATEMENTS, INFORMATION, AND RECOMMENDATIONS IN THIS MANUAL ARE BELIEVED TO BE ACCURATE BUT ARE PRESENTED WITHOUT WARRANTY OF ANY KIND, EXPRESS OR IMPLIED. USERS MUST TAKE FULL RESPONSIBILITY FOR THEIR APPLICATION OF ANY PRODUCTS. THE SOFTWARE LICENSE AND LIMITED WARRANTY FOR THE ACCOMPANYING PRODUCT ARE SET FORTH IN THE INFORMATION PACKET THAT SHIPPED WITH THE PRODUCT AND ARE INCORPORATED HEREIN BY THIS REFERENCE. IF YOU ARE UNABLE TO LOCATE THE SOFTWARE LICENSE OR LIMITED WARRANTY, CONTACT YOUR CISCO REPRESENTATIVE FOR A COPY. The Cisco implementation of TCP header compression is an adaptation of a program developed by the University of California, Berkeley (UCB) as part of UCB’s public domain version of the UNIX operating system. All rights reserved. Copyright © 1981, Regents of the University of California. NOTWITHSTANDING ANY OTHER WARRANTY HEREIN, ALL DOCUMENT FILES AND SOFTWARE OF THESE SUPPLIERS ARE PROVIDED “AS IS” WITH ALL FAULTS. CISCO AND THE ABOVE-NAMED SUPPLIERS DISCLAIM ALL WARRANTIES, EXPRESSED OR IMPLIED, INCLUDING, WITHOUT LIMITATION, THOSE OF MERCHANTABILITY, FITNESS FOR A PARTICULAR PURPOSE AND NONINFRINGEMENT OR ARISING FROM A COURSE OF DEALING, USAGE, OR TRADE PRACTICE. IN NO EVENT SHALL CISCO OR ITS SUPPLIERS BE LIABLE FOR ANY INDIRECT, SPECIAL, CONSEQUENTIAL, OR INCIDENTAL DAMAGES, INCLUDING, WITHOUT LIMITATION, LOST PROFITS OR LOSS OR DAMAGE TO DATA ARISING OUT OF THE USE OR INABILITY TO USE THIS MANUAL, EVEN IF CISCO OR ITS SUPPLIERS HAVE BEEN ADVISED OF THE POSSIBILITY OF SUCH DAMAGES. -

Integrating Skype Within Microsoft

PDF hosted at the Radboud Repository of the Radboud University Nijmegen The following full text is a postprint version which may differ from the publisher's version. For additional information about this publication click this link. http://hdl.handle.net/2066/100589 Please be advised that this information was generated on 2021-10-01 and may be subject to change. 312-226-1 Integrating Skype within Microsoft Case Study Reference: NSM-2012-04 Associate Professor Olivier Furrer, Radboud University Nijmegen, prepared this case with the assistance of master students Lianne van Heeswijk and Emiel R. Hoffer. It is intended to be used as the basis for class discussion rather than to illustrate either the effective or ineffective handling of a management situation. The case was compiled from published sources. © 2012 Radboud University Nijmegen No part of this publication may be copied, stored, transmitted, reproduced, or distributed in any form or by any means without the permission of the copyright owner. Distributed by ecch, UK and USA North America Rest of the world www.ecch.com t +1 781 239 5884 t +44 (0)1234 750903 ecch the case for learning All rights reserved f +1 781 239 5885 f +44 (0)1234 751125 Printed in UK and USA e [email protected] e [email protected] 312-226-1 By combining the two leading e-commerce franchises, eBay and PayPal, with the leader in Internet voice communication, we will create an extraordinarily powerful environment for business on the Net. —Meg Whitman, eBay President and Chief Executive Officer (CEO), September 12, 2005 It’s clear that Skype has limited synergies with eBay and PayPal. -

November Issue of Total Telecom Plus

BUSINESS ANALYSIS FOR TELECOMS ProFESSIONALS November 2010 LEADER CONTENTS NEWS IN BRIEF MORE FOR LESS 3 Timeline A roundup of some of the As operators endeavour to squeeze more out of their existing major stories reported in our daily news service, networks, we look at transforming technologies and markets www.totaltele.com. CONTENT STRATEGIES elecoms operators share a (DSM) techniques that enable telcos common problem: end- to provide high-bandwidth services 6 Smartphone OS Tusers are increasingly over their copper networks. AT&T competition demanding. As customers call for was arguably the most vocal backer Google and Apple are more capacity and higher speeds, of DSM in Paris, having deployed making inroads in the operators are looking for new ways the technology as long ago as 2004 smartphone OS market. A to get the most out of their existing to support its IPTV rollout. fierce battle now looms in the face of rocketing networks and to keep capex down iDate’s figures show US FTTH/B Mary Lennighan growth and consolidation. Editor for new rollouts. And these chal- household penetration at over 7% Total Telecom lenges took centre stage at and growing, backing up the asser- NETWORK STRATEGIES Broadband World Forum (BBWF) tion by China’s ZTE that telcos will 10 Managed services in Paris late last month. continue to stretch the life of their China’s leading vendors Fibre access networks will give copper alongside rolling out fibre Huawei and ZTE are users significantly greater band- for some time to come. ZTE and making strong headway width to their homes, but new domestic rival Huawei feature in our into providing managed figures from iDate presented in analysis on p.10, which charts their services to operators. -

Voipreport Carlosnavarrete Guillermorodriguez

REPORT - Voice Over Internet Protocol - Carlos Navarrete Guillermo Rodríguez What is VOIP? VOIP is an acronym for Voice Over IP, or in more common terms phone service over the Internet. It’s based on giving the same service as the traditional telephony system but using the Internet to send the voice as packets over the net. This new service implies big advances in communications systems such as cost reduction or videoconference service. Nowadays VOIP is starting to get some followers that use VOIP in addition to their traditional phone service, since VOIP service providers usually offer lower rates than traditional phone companies. New software based on VOIP is being developed and currently there are many programs available to use for people with a reasonable quality Internet connection. VOIP programs don’t offer all the destinations as the traditional telephony but they can reach between 80 and 95 % of them. VOIP also allows, in addition to reaching fixed and cell telephone, to speak with another person that uses a computer with speakers and microphone. In the last years the evolution of VOIP is increasing exponentially and it is incorporating manufactures such as Cisco, Lucent, Intel, Quicknet, IBM and many other systems that support VOIP. Data Networks versus Voice Networks Traditional telephony networks are based on the concept of circuit commutation. This means that for making a communication there must be first a physic circuit establishment. A consequence of this is that during the time the communication lasts, it is not possible to share the resources that is using with another communication, even while nobody is speaking (but the communication is established).