RCS and Joyn: Keeping Operators at the Center of Communications

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Raketu to Add Mobility to Web-Based Voip | Infoworld | News | 2007-06-15 | by John Bl

Raketu to add mobility to Web-based VoIP | InfoWorld | News | 2007-06-15 | By John Bl... Page 1 of 4 HOME NEWS TECHNOLOGIES BLOGS/COLUMNS TEST CENTER AUDIO/VIDEO CAREERS IT EXEC-CONNEC Raketu to add mobility to Web-based VoIP New version of the Raketu application will let users make VoIP calls, send text messages, A and chat from cell phone By John Blau, IDG News Service Talkback E-mail Printer Friendly June 15, 2007 A Raketu Communications will add two new mobile phone features to its integrated communications, entertainment, and social networking service in a move to attract consumers on the go. Next week, Raketu will introduce a new domain, www.raketu.mobi, which will allow Free IT resource mobile phone users to more easily navigate the Raketu site and use services such as the company's RakWeb service launched earlier this week, said CEO Greg Learn about the energy Parker in an interview. efficiency in EMC's Pund- IT report on power conservation. By the end of the month, the company intends to launch a new mobile phone version of the Raketu application, which users can install on their phones to make VoIP calls, Sponsored by EMC send text messages, chat, and more, Parker said. Free IT resource Raketu, which is based in New York, is trying to carve out a niche in the highly competitive market for Web-based services by offering an integrated Download the Windows communications, online entertainment, and social networking service that can be Server(R) 2008 Beta: Join the global community. used on both desktop PCs and mobile phones. -

Uila Supported Apps

Uila Supported Applications and Protocols updated Oct 2020 Application/Protocol Name Full Description 01net.com 01net website, a French high-tech news site. 050 plus is a Japanese embedded smartphone application dedicated to 050 plus audio-conferencing. 0zz0.com 0zz0 is an online solution to store, send and share files 10050.net China Railcom group web portal. This protocol plug-in classifies the http traffic to the host 10086.cn. It also 10086.cn classifies the ssl traffic to the Common Name 10086.cn. 104.com Web site dedicated to job research. 1111.com.tw Website dedicated to job research in Taiwan. 114la.com Chinese web portal operated by YLMF Computer Technology Co. Chinese cloud storing system of the 115 website. It is operated by YLMF 115.com Computer Technology Co. 118114.cn Chinese booking and reservation portal. 11st.co.kr Korean shopping website 11st. It is operated by SK Planet Co. 1337x.org Bittorrent tracker search engine 139mail 139mail is a chinese webmail powered by China Mobile. 15min.lt Lithuanian news portal Chinese web portal 163. It is operated by NetEase, a company which 163.com pioneered the development of Internet in China. 17173.com Website distributing Chinese games. 17u.com Chinese online travel booking website. 20 minutes is a free, daily newspaper available in France, Spain and 20minutes Switzerland. This plugin classifies websites. 24h.com.vn Vietnamese news portal 24ora.com Aruban news portal 24sata.hr Croatian news portal 24SevenOffice 24SevenOffice is a web-based Enterprise resource planning (ERP) systems. 24ur.com Slovenian news portal 2ch.net Japanese adult videos web site 2Shared 2shared is an online space for sharing and storage. -

Private Placement Memorandum

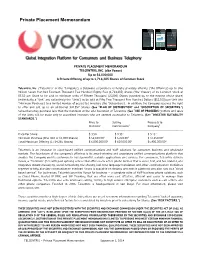

Private Placement Memorandum Global Integration Platform for Consumers and Business Telephony PRIVATE PLACEMENT MEMORANDUM TELCENTRIS, INC. (dba Voxox) Up to $6,000,000 A Private Offering of up to 1,714,285 Shares of Common Stock Telcentris, Inc. (“Telcentris” or the “Company”), a Delaware corporation, is hereby privately offering (“the Offering”) up to One Million Seven Hundred Fourteen Thousand Two Hundred Eighty Five (1,714,285) shares (“the Shares”) of its Common Stock at $3.50 per Share to be sold in minimum units of Fifteen Thousand (15,000) Shares (rounded up to the nearest whole share) (individually a “Unit” and collectively the “Units”) to be sold at Fifty Two Thousand Five Hundred Dollars ($52,500) per Unit (the “Minimum Purchase”) to a limited number of accredited investors (the “Subscribers”). In addition, the Company reserves the right to offer and sell up to an additional 342,857 Shares. (See “PLAN OF DISTRIBUTION” and “DESCRIPTION OF SECURITIES.”) Subscribers may purchase less than the minimum at the sole discretion of Telcentris. (See “USE OF PROCEEDS.”) Offers and sales of the Units will be made only to accredited investors who are deemed acceptable to Telcentris. (See “INVESTOR SUITABILITY STANDARDS.”) Price to Selling Proceeds to Investors1 Commissions2 Company3 -------------------------------------------------------------------------------------------------------------------------------------------- Price Per Share: $ 3.50 $ 0.352 $ 3.153 Minimum Purchase (One Unit or 15,000 Shares) $ 52,500.001 $ 5,250.002 $ 47,250.003 Total Maximum Offering (1,714,285 Shares) $ 6,000,000.001 $ 600,000.002 $5,400,000.003 -------------------------------------------------------------------------------------------------------------------------------------------- Telcentris is an innovator in cloud-based unified communications and VoIP solutions for consumer, business and wholesale markets. -

Elixir Journal

49022 Shabna. T.P and Priyanka.P / Elixir Library Sci. 112 (2017) 49022-49028 Available online at www.elixirpublishers.com (Elixir International Journal) Library Science Elixir Library Sci. 112 (2017) 49022-49028 Knowledge Sharing Over Instant Messaging Apps: A Study among IT Professionals, Malappuram, Kerala. Shabna. T.P1 and Priyanka.P2 1 Assistant Professor, Department of Library and Information Science, Farook College, Kozhikode, Kerala, India. 2 Head librarian, Scholars international academy, Sharjah, UAE. ARTICLE INFO ABSTRACT Article history: Advances in information technology have resulted in the development of various Received: 13 October 2017; computer-mediated communication tools of which the Instant messenger (IM) is one of Received in revised form: the most prevalent. Instant messaging apps are widely used today for information 11 November 2017; sharing. The present study “Knowledge sharing over instant messaging apps: a study Accepted: 20 November 2017; among Kinfra community, Malappuram” is based on the importance of instant messaging apps and the authenticity of the information sharing via those apps which helps the users Keywords to determine its reliability. The need to conduct a study based on trustworthiness of the Knowledge Sharing, information sharing is desirable and useful for the users. A structured questionnaire is Instant message, used for collecting data which are personally distributed or sent through mail. The Web 2.0 applications, collected data are classified, analyzed. The investigator‟s conclusion on whether or not IT Professionals. instant messaging has negative effects on real-life social networks is, well, inconclusive. People have varying opinions on the topic, and there is evidence that can demonstrate both the pros and cons of using instant messaging. -

OTT and Related On-Line Services in Arab Region

OTT and related on-line services in Arab Region Release 1.1 31/01/2017 Reality of OTTs in Arab Region The objective of the study is: 1- to have a global view on OTT and on-line services worldwide with the impact and trends of these services on national players and economies, 2- to have an overview on associated practices and relevant public policies worldwide and in the Region, 3- to propose recommendations on methods and approaches for preparation of associated policies and frameworks. _____________________________ The present document is the first release of the report. A draft questionnaire is proposed with this release and is intended to be submittedfor a survey to Regulators/policy Makers and Operators in the Region. The outcome of the survey with the related findings will be commented and included in a next version of this report. It is to note that, as the subject of OTT is being regularly debated in almost all regions with potential move and change in the related positions and decisions, some information reported in the present report may become outdated. __________________________________________________________________ OTT and related on-line services in Arab Region Executive Summary With the increase of global mobile broadband penetration, as well as the rapid adoption of connected devices, consumers have been provided with an access to a wide variety of on-line services which go beyond the traditional voice and messaging services provided by telecom operators (alias telcos *). These on-line services are reshaping the entire telecommunication eco-system, and are of great benefit to consumers worldwide, to the global economy and ubiquitous connectivity. -

Case No COMP/M.6281 - MICROSOFT/ SKYPE

EN Case No COMP/M.6281 - MICROSOFT/ SKYPE Only the English text is available and authentic. REGULATION (EC) No 139/2004 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 07/10/2011 In electronic form on the EUR-Lex website under document number 32011M6281 Office for Publications of the European Union L-2985 Luxembourg EUROPEAN COMMISSION Brussels, 07/10/2011 C(2011)7279 In the published version of this decision, some information has been omitted pursuant to Article MERGER PROCEDURE 17(2) of Council Regulation (EC) No 139/2004 concerning non-disclosure of business secrets and other confidential information. The omissions are shown thus […]. Where possible the information omitted has been replaced by ranges of figures or a general description. PUBLIC VERSION To the notifying party: Dear Sir/Madam, Subject: Case No COMP/M.6281 - Microsoft/ Skype Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/20041 1. On 02.09.2011, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which the undertaking Microsoft Corporation, USA (hereinafter "Microsoft"), acquires within the meaning of Article 3(1)(b) of the Merger Regulation control of the whole of the undertaking Skype Global S.a.r.l, Luxembourg (hereinafter "Skype"), by way of purchase of shares2. Microsoft and Skype are designated hereinafter as "parties to the notified operation" or "the parties". I. THE PARTIES 2. Microsoft is active in the design, development and supply of computer software and the supply of related services. The transaction concerns Microsoft's communication services, in particular the services offered under the brands "Windows Live Messenger" (hereinafter "WLM") for consumers and "Lync" for enterprises. -

Protocol Filter Planning Worksheet, V7.X

Protocol Filter Planning Worksheet Websense Web Security Solutions (v7.x) Protocol filter (name): Applies to (clients): In policy (name): At (time and days): Legend Action Bandwidth Permit Block Network Protocol (percentage) Protocol Name Action Log Bandwidth Database SQL Net P B N P % File Transfer FTP P B N P % Gopher P B N P % WAIS P B N P % YouSendIt P B N P % Instant Messaging / Chat AOL Instant Messenger or ICQ P B N P % Baidu Hi P B N P % Brosix P B N P % Camfrog P B N P % Chikka Messenger P B N P % Eyeball Chat P B N P % 1 © 2013 Websense, Inc. Protocol filter name: Protocol Name Action Log Bandwidth Gadu-Gadu P B N P % Gizmo Project P B N P % Globe 7 P B N P % Gmail Chat (WSG Only) P B N P % Goober Messenger P B N P % Gooble Talk P B N P % IMVU P B N P % IRC P B N P % iSpQ P B N P % Mail.Ru P B N P % Meetro P B N P % MSC Messenger P B N P % MSN Messenger P B N P % MySpaceIM P B N P % NateOn P B N P % Neos P B N P % Netease Popo P B N P % netFM Messenger P B N P % Nimbuzz P B N P % Palringo P B N P % Paltalk P B N P % SIMP (Jabber) P B N P % Tencent QQ P B N P % TryFast Messenger P B N P % VZOchat P B N P % Wavago P B N P % Protocol Filter Planning Worksheet 2 of 8 Protocol filter name: Protocol Name Action Log Bandwidth Wengo P B N P % Woize P B N P % X-IM P B N P % Xfire P B N P % Yahoo! Mail Chat P B N P % Yahoo! Messenger P B N P % Instant Messaging File Attachments P B N P % AOL Instant Messenger or ICQ P B N P % attachments MSN Messenger attachments P B N P % NateOn Messenger -

Annual Report 2010 N T Ann Rrepo P

AnnualAnn RReReportpop rtt 2010 The Naspers Review of Governance and Financial Notice of Annual Group Operations Sustainability Statements General Meeting 2 Financial highlights 22 Review of operations 42 Governance 74 Consolidated 198 Notice of AGM 4 Group at a glance 24 Internet 51 Sustainability and company 205 Proxy form 6 Global footprInt 30 Pay television 66 Directorate annual financial 8 Chairman’s and 36 Print media 71 Administration and statements managing corporate information director’s report 72 Analysis of 16 Financial review shareholders and shareholders’ diary Entertainment at your fingertips Vision for subscribers To – wherever I am – have access to entertainment, trade opportunities, information and to my friends Naspers Annual Report 2010 1 The Naspers Review of Governance and Financial Notice of Annual Group Operations Sustainability Statements General Meeting Mission To develop in the leading group media and e-commerce platforms in emerging markets www.naspers.com 2 Naspers Annual Report 2010 The Naspers Review of Governance and Financial Notice of Annual Group Operations Sustainability Statements General Meeting kgFINANCIAL HIGHLIGHTS Revenue (R’bn) Ebitda (R’m) Ebitda margin (%) 28,0 6 496 23,2 26,7 6 026 22,6 09 10 09 10 09 10 Headline earnings Core HEPS Dividend per per share (rand) (rand) share (proposed) (rand) 8,84 14,26 2,35 8,27 11,79 2,07 09 10 09 10 09 10 2010 2009 R’m R’m Income statement and cash flow Revenue 27 998 26 690 Operational profit 5 447 4 940 Operating profit 4 041 3 783 Net profit attributable -

Skype Modile Download

Skype modile download Connect your way. Download the Skype mobile app for free, and talk, text, instant message, or video chat whenever, wherever. Get started.Skype Android · Skype Blackberry · iPhone · iPod touch. Call mobile and landline numbers – use the Skype app for Android to keep in touch with low-cost calls and SMS even if your friends aren't on Skype. Chat with. Make free Skype to Skype video and voice calls as well as send instant messages to friends and family around the world. Features: Call friends and family. The Skype you know and love has an all-new design, supercharged with a ton of new features and new ways to stay connected with the people you care about. Skype latest version: Skype, the telephone of the 21st century. Skype is the most popular application on the market for making video calls, mobile calls, and sen. Download this app from Microsoft Store for Windows 10, Windows 10 Mobile, HoloLens, Xbox One. See screenshots, read the latest customer reviews, and. Download Skype apps and clients across mobile, tablet, and desktop and across Windows, Mac, iOS, and Android. this video shows [HOW TO] Install and Create Skype Account on Mobile Phone. Skype for mobile is just about the same as Skype for desktop. That by itself is high praise - high-quality voice calls, convenient messaging, and low-cost phone. Download Skype For Every Mobile. Download Skype for All Mobiles at one place iPhone, Android, Symbian, Windows Phone, BlackBerry. All this will be available for anyone to see on Skype, except for your mobile number, which will be restricted to your own contacts. -

A Scoping Review of AHP Interventions for People Living with Dementia, Their Families, Partners and Carers

Dementia A scoping review of AHP interventions for people living with dementia, their families, partners and carers Prepared for: Alzheimer Scotland: Action on Dementia 22 Drumsheugh Gardens Edinburgh Scotland EH3 7RN Prepared by: The Division of Occupational Therapy and Arts Therapies Queen Margaret University School of Health Sciences Edinburgh EH21 6UU Investigator: Duncan Pentland, D. Health Soc Sci Published: 03-December-2015 CONTENTS Contents ................................................................................................................................................... i List of figures and tables ........................................................................................................................ iv List of abbreviations, acronyms and symbols ......................................................................................... v 1. Introduction .................................................................................................................................... 1 1.1. Purpose ................................................................................................................................... 1 1.2. Approach ................................................................................................................................. 1 1.3. Methods .................................................................................................................................. 1 2. Cognitive interventions .................................................................................................................. -

Time-Resolved Terahertz Spectroscopy Of

TIME-RESOLVED TERAHERTZ SPECTROSCOPY OF SEMICONDUCTOR QUANTUM DOTS by GEORGI DAKOVSKI Submitted in partial fulfillment of the requirements For the degree of Doctor of Philosophy Thesis advisor: Dr. Jie Shan Department of Physics Case Western Reserve University January, 2008 CASE WESTERN RESERVE UNIVERSITY SCHOOL OF GRADUATE STUDIES We hereby approve the dissertation of ______________________________________________________ candidate for the Ph.D. degree *. (signed)_______________________________________________ (chair of the committee) ________________________________________________ ________________________________________________ ________________________________________________ ________________________________________________ ________________________________________________ (date) _______________________ *We also certify that written approval has been obtained for any proprietary material contained therein. Table of Contents List of figures……………………………………………………………………5 Abstract………………………………………………………………………..10 1. Introduction to optical pump/terahertz probe spectroscopy………………12 1.1 Generation and detection of THz radiation……………………….13 1.2 Applications of THz-TDS…………………………………………...19 1.3 Outline of the thesis………………………………………………...20 2. Localized THz generation via optical rectification in ZnTe………………..22 2.1 Difference-frequency generation…………………………………..24 2.2 Experimental setup………………………………………………….26 2.3 Results………………………………………………………………..27 2.4 Numerical simulation and discussion……………………………..30 2.5 Conclusions………………………………………………………….39 1 3. -

Annual Report 2006

ANNUAL TOWN REPORT OF THE YEAR 2006 MARBLEHEAD, MASSACHUSETTS MARBLEHEAD TOWN REPORT Table of Contents Board of Selectmen 4 Warrant for Annual Town Meeting 7 May 1, 2006 and Annual Town Election May 8, 2006 Results of Annual Town Election 23 May 8, 2006 Results of Annual Town Meeting 27 May 1 & 2, 2006 Warrant for State Primary 66 September 19, 2006 Results of State Primary 68 September 19, 2006 Warrant for State Election 74 November 7, 2006 Results of State Election 79 November 7, 2006 Officials Elected 83 Officials Appointed 86 Vital Records of 2006 98 Number of births, marriages, deaths and causes of death recorded Department Reports: Abbot Public Library 101 Board of Assessors 105 Board of Health 107 Building Commissioner and Inspectional 120 Services Cable TV Oversight Committee 122 Cemetery Department 123 Conservation Commission 125 Council on Aging 127 Department of Public Works 131 Engineering Department 133 Financial Services 134 Fire Department 136 2 TABLE OF CONTENTS Fort Sewall Oversight Committee 148 Harbors and Waters 149 Marblehead Cultural Council 151 Marblehead Historical Commission 153 Marblehead Housing Authority 155 Metropolitan Area Planning Council 162 Municipal Light Department 169 Old and Historic Districts Commission 177 Planning Board 178 Police Department 180 Recreation, Parks & Forestry 186 Sealer of Weights & Measures 199 Shellfish Constables 200 Veterans’ Agent 201 Water and Sewer Commission 203 Zoning Board of Appeals 211 School Reports Marblehead School Committee members 212 organization and meetings Marblehead