CLP Holdings 2019 Annual Results Highlights

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Patricipating Merchants Address

Patricipating Merchants Address City Super APM, LEVEL 2-XSITE, KWUN TONG 觀塘apm二樓-xsite B1/F ONE TIMES SQUARE, 1 MATHESON STREET, CAUSEWAY BAY 銅鑼灣時代廣場B1地庫 SHOP 204-21 4, 2/F NEW TOWN PLAZA PHASE 1 , 1 8 SHA TIN CENTRE ST, SHATIN 沙田新城巿廣場一期二樓204-214號舖 SHOP 3001, 3/F HARBOUR CITY, 3 CANTON ROAD, TSIM SHA TSUI 尖沙咀海港城港威商場三階3001號舖 SHOPS 1041-1049, 1/F IFC MALL, 8 FINANCE STREET, CENTRAL 中環國際金融中心商場一樓1041-1049號舖 Express UNITS H & I, LEVEL 1 , CATHAY PACIFIC HEADQUARTER BUILDING, CATHAY PACIFIC CITY, CHEK LAP KOK, LANTAU ISLAND 赤鱲角國泰城國泰總部大樓 H 及 I 號 Food Le Parc PORTION ON THE GROUND FLOOR, PORTION IN THE BASEMENT LEVEL ONE A AND PORTION IN THE BASEMENT LEVEL TWO, CHEUNG KONG CENTER, CENTRAL 中環長江中心地下入口、地庫L1A層 (部分) 及地庫L2層 (部分) 舖 SHOP NOS. 2 & 3, G/F, WESTLANDS CENTRE, 20 WESTLANDS ROAD, HONG KONG 香港華蘭路20號華蘭中心地下2號及3號室 Fortress 1 /F., KWONG WAH PLAZA, TAI TONG ROAD, YUEN LONG 豐澤電器 元朗大棠路光華廣場 1 樓 CHAU'S COMMERCIAL CENTRE, 57-63 CHUNG ON STREET, TSUEN WAN 荃灣眾安街 57 -63 號周氏商業中心地下 CKC18, CHEUNG KONG CENTER, B2, 2 QUEEN'S ROAD CENTRAL, CENTRAL 中環皇后大道中 2 號長江中心 CKC 18 地庫 B2 G/F, REAR PORTION, WAH MING CENTRE, 396 DES VOEUX ROAD WEST, HONG KONG 香港德輔道西 396 號華明中心地下後座 G/F YU SUNG BOON BLDG, 107-111 DES VOEUX ROAD, CENTRAL 中環德輔道中 107 -111 號余崇本大廈地下 SHOP 4-6 ON G/F & LOWER LEVELS 1 & 2, WAI FUNG PLAZA, 664 NATHAN ROAD, MONG KOK 旺角彌敦道 664 號惠豐中心地下 4-6 號舖 SHOP UNIT F70, POPCORN 2, 9 TONG CHUN STREET, TSEUNG KWAN O 將軍澳 PopCorn 2 F70 號舖 PORTION OF G/F & 1 /F, GREENWICH CENTRE, NO. -

Official Record of Proceedings

LEGISLATIVE COUNCIL ― 24 June 2020 8723 OFFICIAL RECORD OF PROCEEDINGS Wednesday, 24 June 2020 The Council met at Eleven o'clock MEMBERS PRESENT: THE PRESIDENT THE HONOURABLE ANDREW LEUNG KWAN-YUEN, G.B.S., J.P. THE HONOURABLE JAMES TO KUN-SUN THE HONOURABLE LEUNG YIU-CHUNG THE HONOURABLE ABRAHAM SHEK LAI-HIM, G.B.S., J.P. THE HONOURABLE TOMMY CHEUNG YU-YAN, G.B.S., J.P. PROF THE HONOURABLE JOSEPH LEE KOK-LONG, S.B.S., J.P. THE HONOURABLE JEFFREY LAM KIN-FUNG, G.B.S., J.P. THE HONOURABLE WONG TING-KWONG, G.B.S., J.P. THE HONOURABLE STARRY LEE WAI-KING, S.B.S., J.P. THE HONOURABLE CHAN HAK-KAN, B.B.S., J.P. THE HONOURABLE CHAN KIN-POR, G.B.S., J.P. DR THE HONOURABLE PRISCILLA LEUNG MEI-FUN, S.B.S., J.P. 8724 LEGISLATIVE COUNCIL ― 24 June 2020 THE HONOURABLE WONG KWOK-KIN, S.B.S., J.P. THE HONOURABLE MRS REGINA IP LAU SUK-YEE, G.B.S., J.P. THE HONOURABLE PAUL TSE WAI-CHUN, J.P. THE HONOURABLE CLAUDIA MO THE HONOURABLE MICHAEL TIEN PUK-SUN, B.B.S., J.P. THE HONOURABLE STEVEN HO CHUN-YIN, B.B.S. THE HONOURABLE FRANKIE YICK CHI-MING, S.B.S., J.P. THE HONOURABLE WU CHI-WAI, M.H. THE HONOURABLE YIU SI-WING, B.B.S. THE HONOURABLE MA FUNG-KWOK, S.B.S., J.P. THE HONOURABLE CHARLES PETER MOK, J.P. THE HONOURABLE CHAN CHI-CHUEN THE HONOURABLE CHAN HAN-PAN, B.B.S., J.P. -

Fanny Chan Fanny Chan Organizing Committee of Spring Dinner 2019 the Hong Kong Air Conditioning & Refrigeration Association

8 January 2019 TO: All ACRA Members ACRA Spring Dinner 2019 To celebrate the New Year of Pig, we would like to invite you to join our ACRA Spring Dinner 2019 on 1 March 2019 (Friday). Details are as follows: Date: 1 March 2019 (Friday) Venue: Laguna Palace Restaurant(海逸皇宮大酒樓) 1/F, The Laguna Mall, 8 Laguna Verde Avenue, Hung Hom (紅磡海逸道 8 號海逸坊 1 樓) Time: 6:00 p.m. – 7:30 p.m. Cocktail Reception 7:30 p.m. – 10:00 p.m. Dinner Please kindly confirm your attendance by returning the attached Reply Slip before 14 February 2019. The reservation will be at first come first served basis. Should you have any queries, please feel free to contact Ms Aris Chiu at 2598 0101. Look forward to seeing you. With Warmest Regards Fanny Chan Fanny Chan Organizing Committee of Spring Dinner 2019 The Hong Kong Air Conditioning & Refrigeration Association 8 January 2019 To : The Hong Kong Air Conditioning & Refrigeration Association Please return the reply slip to [email protected] Reply Slip ACRA Spring Dinner 2019 I will attend the 2019 Spring Dinner. ( ) HK$500/ per seat (1 seat to 5 seats) ( ) HK$2,800 for 6 seats ( ) HK$460/ per seat (7 seats to 11 seats) ( ) HK$5,000 for a table of 12 seats ~ I would like to reserve _____ seat(s) for the dinner with total amount HK$_____________. Payment Method: Please prepare a crossed cheque payable to ‘The Hong Kong Air Conditioning and Refrigeration Association Limited’ and send to Ms Aris Chiu at Room 1801, Tung Wai Commercial Building, 109-111 Gloucester Road, Wanchai, Hong Kong. -

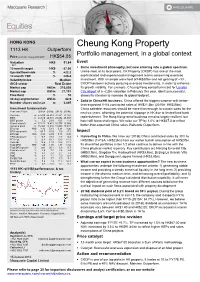

Cheung Kong Property 1113 HK Outperform Portfolio Management, in a Global Context Price (At 08:09, 12 Aug 2016 GMT) HK$54.85

HONG KONG Cheung Kong Property 1113 HK Outperform Portfolio management, in a global context Price (at 08:09, 12 Aug 2016 GMT) HK$54.85 Valuation HK$ 91.84 Event - DCF 12-month target HK$ 67.00 . Same investment philosophy, but now entering into a global spectrum. Upside/Downside % +22.2 Unlike most of its local peers, CK Property (CKOP) has one of the most 12-month TSR % +25.4 sophisticated and experienced management teams concerning overseas Volatility Index Medium investment. With an ample war-chest of HK$50bn and net gearing of ~3%, GICS sector Real Estate CKOP has been actively pursuing overseas investments, in order to enhance Market cap HK$m 210,898 its growth visibility. For example, Cheung Kong consortium’s bid for London Market cap US$m 27,191 City Airport at a ~£2bn valuation in February this year, albeit unsuccessful, Free float % 70 shows its intention to increase its global footprint. 30-day avg turnover US$m 42.9 . Solid in China/HK business. China offered the biggest surprise with better- Number shares on issue m 3,845 than-expected 1H16 contracted sales of HK$21.5bn (2015A: HK$25bn). Investment fundamentals China saleable resources should be more than enough to sustain sales for the Year end 31 Dec 2015A 2016E 2017E 2018E next six years, offsetting the potential slippage in HK due to limited land bank Revenue m 57,280 66,412 70,831 73,127 EBIT m 21,610 26,744 29,552 28,994 replenishment. The Hong Kong rental business remains largely resilient, but EBIT growth % 7.2 23.8 10.5 -1.9 hotel still faces challenges. -

Name of Buildings Awarded the Quality Water Supply Scheme for Buildings – Fresh Water (Plus) Certificate (As at 8 February 2018)

Name of Buildings awarded the Quality Water Supply Scheme for Buildings – Fresh Water (Plus) Certificate (as at 8 February 2018) Name of Building Type of Building District @Convoy Commercial/Industrial/Public Utilities Eastern 1 & 3 Ede Road Private/HOS Residential Kowloon City 1 Duddell Street Commercial/Industrial/Public Utilities Central & Western 100 QRC Commercial/Industrial/Public Utilities Central & Western 102 Austin Road Commercial/Industrial/Public Utilities Yau Tsim Mong 1063 King's Road Private/HOS Residential Eastern 11 MacDonnell Road Private/HOS Residential Central & Western 111 Lee Nam Road Commercial/Industrial/Public Utilities Southern 12 Shouson Hill Road Private/HOS Residential Central & Western 127 Repulse Bay Road Private/HOS Residential Southern 12W Commercial/Industrial/Public Utilities Tai Po 15 Homantin Hill Private/HOS Residential Yau Tsim Mong 15W Commercial/Industrial/Public Utilities Tai Po 168 Queen's Road Central Commercial/Industrial/Public Utilities Central & Western 16W Commercial/Industrial/Public Utilities Tai Po 17-19 Ashley Road Commercial/Industrial/Public Utilities Yau Tsim Mong 18 Farm Road (Shopping Arcade) Commercial/Industrial/Public Utilities Kowloon City 18 Upper East Private/HOS Residential Eastern 1881 Heritage Commercial/Industrial/Public Utilities Yau Tsim Mong 211 Johnston Road Commercial/Industrial/Public Utilities Wan Chai 225 Nathan Road Commercial/Industrial/Public Utilities Yau Tsim Mong Name of Buildings awarded the Quality Water Supply Scheme for Buildings – Fresh Water (Plus) -

Driving Services Section

DRIVING SERVICES SECTION Taxi Written Test - Part B (Location Question Booklet) Note: This pamphlet is for reference only and has no legal authority. The Driving Services Section of Transport Department may amend any part of its contents at any time as required without giving any notice. Location (Que stion) Place (Answer) Location (Question) Place (Answer) 1. Aberdeen Centre Nam Ning Street 19. Dah Sing Financial Wan Chai Centre 2. Allied Kajima Building Wan Chai 20. Duke of Windsor Social Wan Chai Service Building 3. Argyle Centre Nathan Road 21. East Ocean Centre Tsim Sha Tsui 4. Houston Centre Mody Road 22. Eastern Harbour Centre Quarry Bay 5. Cable TV Tower Tsuen Wan 23. Energy Plaza Tsim Sha Tsui 6. Caroline Centre Ca useway Bay 24. Entertainment Building Central 7. C.C. Wu Building Wan Chai 25. Eton Tower Causeway Bay 8. Central Building Pedder Street 26. Fo Tan Railway House Lok King Street 9. Cheung Kong Center Central 27. Fortress Tower King's Road 10. China Hong Kong City Tsim Sha Tsui 28. Ginza Square Yau Ma Tei 11. China Overseas Wan Chai 29. Grand Millennium Plaza Sheung Wan Building 12. Chinachem Exchange Quarry Bay 30. Hilton Plaza Sha Tin Square 13. Chow Tai Fook Centre Mong Kok 31. HKPC Buil ding Kowloon Tong 14. Prince ’s Building Chater Road 32. i Square Tsim Sha Tsui 15. Clothing Industry Lai King Hill Road 33. Kowloonbay Trademart Drive Training Authority Lai International Trade & King Training Centre Exhibition Centre 16. CNT Tower Wan Chai 34. Hong Kong Plaza Sai Wan 17. Concordia Plaza Tsim Sha Tsui 35. -

Gallery Was Founded by Ms

G A LLE R Y BLINK Gallery was founded by Ms. TK Chan and Mr. Albert Chung in 2013. Our dedicated gallery space is located in Kwun Tong and Happy Valley, Hong Kong. It can simultaneously hold exhibitions for three different artists. Our aim is to promote Hong Kong Artists and their art pieces at international art fairs. BLINK Gallery, 8/F, 135 Hoi Bun Road, Kwun Tong, Hong Kong www.blinkgalleryhk.com [email protected] +852 9646 6686 Mr. Albert Chung BLINK Gallery, 8/F, 135 Hoi Bun Road, Kwun Tong, Hong Kong www.blinkgalleryhk.com [email protected] +852 9646 6686 Mr. Albert Chung List of selected Exhibitions - 2017 Ink Asia, Hong Kong Convention and Exhibition Centre (Dec) Fine Art Asia, Hong Kong Convention and Exhibition Centre (Sept) HONG KONG Affordable Art Fair, Hong Kong Convention and Exhibition Centre (May) SINGAPORE Affordable Art Fair, F1 Pit Building (April) Asia Contemporary Art Show, Conrad Hong Kong (Mar & Sept) Art Stage Singapore, BLINK Gallery, Marina Bay Sands, Sands Expo & Convention Centre (Jan) Singapore Contemporary, BLINK Gallery, Suntec Singapore Convention & Exhibition Centre (Jan) - 2016 INK ASIA 2016, Hong Kong Convention and Exhibition Centre (Dec) SINGAPORE Affordable Art Fair, F1 Pit Building (Nov) SCOTTISH LANDSCAPE Solo Exhibition by TK CHAN, Hong Kong Cultural Centre (Nov) Affordable Art Fair Seoul, DDP, Korea (Sept) AURORA Solo Exhibition The Roaster, SteP by SteP Cafe, Shuen Wan, Hong Kong (Sept - Dec) Bazaar Art Jakarta 2016, The Ritz-Carlton Jakarta, Pacific Place (Aug) Asia Contemporary -

WORLD WING Wi-Fi サービスエリア 香港

WORLD WING Wi-Fi サービスエリア 香港 Webブラウザで ロケーション名 住所 市 カテゴリー SSID のログイン 28 Hennessy Road 1/F, 28 Hennessy Road, Wan Chai, Hong Kong Hong Kong - PCCW 対応 28 Hennessy Road 2/F, 28 Hennessy Road, Wan Chai, Hong Kong Hong Kong - PCCW 対応 28 Hennessy Road 28 Hennessy Road, Wan Chai, Hong Kong Hong Kong - PCCW 対応 4084-BN Outside Holiday Inn Golden Mile Hong Kong, Mody Road, Tsim Sha Tsui Hong Kong - PCCW 対応 Shop G48 & G49, G/F., New Century Plaza, Man On House, 151-163 Wanchai Road, Wan 7-11 Shop Hong Kong - PCCW 対応 Chai, Hong Kong 759 cafe Shop 1-3, The Graces, Providence Bay, 9 Fo Chun Road, Tai Po, New Territories Hong Kong - PCCW 対応 759 Kawaiiland G/F & 1/F No. 476 Lockhart Road, Causeway Bay, Hong Kong Hong Kong - PCCW 対応 759 Store G/F, 268 Lai Chi Kok Road, Lai Chi Kok Road, Kowloon Hong Kong - PCCW 対応 759 Store Mongkok Plaza, No. 794-802 Nathan Road, Mongkok, Kowloon Hong Kong - PCCW 対応 759 Store Shop 101, 1/F, 18 Upper East, Nos. 18-36 Shing On Street, Sai Wan Ho, Hong Kong Hong Kong - PCCW 対応 759 Store Shop 101, G/F, 18 Upper East, Nos. 18-36 Shing On Street, Sai Wan Ho, Hong Kong Hong Kong - PCCW 対応 759 Store Shop 120, G/F, Nam Lok House, Nam Shan Estate, Shamshuipo, Kowloon Hong Kong - PCCW 対応 759 Store Shop 24, G/F, Hopewell House, 169-197 Hip Wo Street, Kwun Tong, Kowloon Hong Kong - PCCW 対応 759 Store Shop 27, G/F, Site 2, Aberdeen Centre, Aberdeen, Hong Kong Hong Kong - PCCW 対応 759 Store Shop 3, 5, 7, 9, 11 & 13, 1/F, Exchange Tower, 33 Wang Chiu Road, Kowloon Bay, Kowloon Hong Kong - PCCW 対応 759 Store Shop 3, Free Standing Block (Near Mei Chuen House), Mei Tin Estate, Sha Tin, New Territories Hong Kong - PCCW 対応 759 Store Shop 3, G/F, Lido Avenue 41-63 Castle Peak Road, Sham Tseng, New Territories Hong Kong - PCCW 対応 759 Store Shop 350-352, Level 3, Ma On Shan Plaza, Sha Tin, New Territories Hong Kong - PCCW 対応 759 Store Shop 4 & 5, G/F, Kai Lok House, Kai Yip Estate, Kowloon Bay, Kowloon Hong Kong - PCCW 対応 759 Store Shop 5. -

List of Clinics Providing Live Attenuated Influenza Vaccines Under the Special Arrangement

List of clinics providing live attenuated influenza vaccines under the Special Arrangement Hong Kong Island and Outlying Islands Enquiry phone Name of clinic Address number Room 704, 7/F, Manning House, Atto Health 28896999 38-48 Queen's Road Central, CENTRAL, HONG KONG Christocare Health Centre G/F, 40 Hennessy Road, WAN CHAI, HONG KONG 28656656 Shop A3, 33 North Point Road, City Medical Healthcare Centre 34228763 NORTH POINT, HONG KONG Doctor Wong Chit Wah Shop 9, G/F, Odeon Plaza, 28 Shu Kuk Street, 25167283 Medical Clinic NORTH POINT, HONG KONG Room 2108, 21/F, Crawford House, Dr Ada Li Medical Practice 25223239 70 Queen's Road Central, CENTRAL, HONG KONG Shop B, G/F, 18 Factory Street, Dr Linda H Y Chan 23202330 SHAU KEI WAN, HONG KONG Flat E, 5/F, Tak Lee Commercial Building, Dr Ng Hee Liang Clinic 28360233 115 Wan Chai Road, WAN CHAI, HONG KONG Shop No P10, Po Shan Mansion, Tai Koo Shing, 25670336/ Dr Olivia K W Chow QUARRY BAY, HONG KONG 25670337 Shop 35, G/F, Lei Chak House, Ap Lei Chau Estate, Dr Phyllis Lee Kuen 25521321 AP LEI CHAU, HONG KONG Room 1603A, 16/F, Central Building, 1-3 Pedder Street, Dr Wilson Hui's Clinic 25252825 CENTRAL, HONG KONG Shop 6A, 5/F, Dr Wong Chun Chung Greenwood Terrace Commercial Complex, 25570463 Greenwood Terrace, CHAI WAN, HONG KONG Dr Wong Man Hung & Shop 21A, G/F, Belcher Court, 2 Sai Cheung Street, 28190167 Associates KENNEDY TOWN, HONG KONG Shop P-517, Podium, Ko On Mansion, Taikoo Shing, Dr Wong Pak Hoi's Office 25672796 QUARRY BAY, HONG KONG Room 602, 6/F, Kornhill Plaza-Office Tower, Dr Yip Yuk Pang's Clinic 25600015 1 Kornhill Road, QUARRY BAY, HONG KONG List of clinics providing live attenuated influenza vaccines under the Special Arrangement Hong Kong Island and Outlying Islands Enquiry phone Name of clinic Address number Shop G60-61, G/F, East Marina Square, Dr Yu Wai Cho Michael 25183230 South Horizons, AP LEI CHAU, HONG KONG Shop A71, G/F, Tai On Building, Dr Yu Wai Nam 57-87 Shau Kei Wan Road, 28862080 SAI WAN HO, HONG KONG Shop 8, Level 1 (Basement), Hong Kong Station, Dr. -

恒益物業管理有限公司(恒基兆業地產集團成員) - 1 - Mental Health Friendly Organisation 精神健康友善機構 Global Gateway Tower

《精神健康職場約章》簽署機構 (截至2021年8月31日止) Mental Health Workplace Charter - Chartered Signatories (As at 31 August 2021) Organisation Name 機構名稱 Title 嘉許稱號 恒益物業管理有限公司(恒基兆業地產集團成員) - 1 - Mental Health Friendly Organisation 精神健康友善機構 Global Gateway Tower 恒益物業管理有限公司(恒基兆業地產集團成員) - 2 - Mental Health Friendly Organisation 精神健康友善機構 城中匯 恒益物業管理有限公司(恒基兆業地產集團成員) - 3 - Mental Health Friendly Organisation 精神健康友善機構 威達工貿商業中心 恒益物業管理有限公司(恒基兆業地產集團成員) - 4 - Mental Health Friendly Organisation 精神健康友善機構 創匯國際中心 恒益物業管理有限公司(恒基兆業地產集團成員) - 5 - Mental Health Friendly Organisation 精神健康友善機構 逸華軒 恒益物業管理有限公司(恒基兆業地產集團成員) - 6 - Mental Health Friendly Organisation 精神健康友善機構 匯達商業中心 恒益物業管理有限公司(恒基兆業地產集團成員) - 7 - Mental Health Friendly Organisation 精神健康友善機構 源盛工業大廈 恒益物業管理有限公司(恒基兆業地產集團成員) - 8 - Mental Health Friendly Organisation 精神健康友善機構 嘉賢居 恒益物業管理有限公司(恒基兆業地產集團成員) - 9 - Mental Health Friendly Organisation 精神健康友善機構 福隆大廈 10 4M Industrial Development Limited 科文實業有限公司 Mental Health Friendly Supreme Organisation 精神健康友善卓越機構 11 Aberdeen Kai-fong Welfare Association Social Service 香港仔坊會社會服務 Mental Health Friendly Organisation 精神健康友善機構 12 AEM Technology Limited 創勢科技有限公司 Mental Health Friendly Supreme Organisation 精神健康友善卓越機構 13 AITIA (HK) CPA Limited 德正會計師事務所有限公司 Mental Health Friendly Supreme Organisation 精神健康友善卓越機構 14 AJA Joint Venture AJA聯營 Mental Health Friendly Organisation 精神健康友善機構 Acciona Agua SA 怡和機械和中國建築工程(香港) 15 AJC Joint Venture Mental Health Friendly Supreme Organisation 精神健康友善卓越機構 聯營 16 Allianz Worldwide Partners (Hong Kong) Limited 安世聯合(香港)有限公司 Mental Health Friendly Supreme Organisation -

QMS to Be Post to WSD Webpage As of Jan 20201 23022021.Xlsx

Name of Buildings awarded the Quality Water Supply Scheme for Buildings – Fresh Water (Management System) Certificate (as at 31 January 2021) Name of Building Types of Building District 1 Duddell Street Commercial/Industrial Central & Western 11 MacDonnell Road Private/HOS/Residential Central & Western 168 Queen's Road Central Commercial/Industrial Central & Western 299QRC Commercial/Industrial Central & Western 3 MacDonnell Road Private/HOS/Residential Central & Western 31 Robinson Road Private/HOS/Residential Central & Western 39 Conduit Road Private/HOS/Residential Central & Western 8 Queen's Road East Commercial/Industrial Central & Western 80 Robinson Road Private/HOS/Residential Central & Western Agricultural Bank of China Tower Commercial/Industrial Central & Western AIA Central Commercial/Industrial Central & Western Aigburth Private/HOS/Residential Central & Western Alexandra House Commercial/Industrial Central & Western Altamira Private/HOS/Residential Central & Western Azura Private/HOS/Residential Central & Western Bamboo Grove Block 74 Private/HOS/Residential Central & Western Bamboo Grove Block 76 Private/HOS/Residential Central & Western Bamboo Grove Block 78 Private/HOS/Residential Central & Western Bamboo Grove Block 80 Private/HOS/Residential Central & Western Bamboo Grove Block 82 Private/HOS/Residential Central & Western Bamboo Grove Block 84 Private/HOS/Residential Central & Western Bamboo Grove Clubhouse Commercial/Industrial Central & Western Bank of America Tower Commercial/Industrial Central & Western Bank of China -

Express 2018May Eng

Issue 59MAY 2018 Right the wrong Poverty is solvable — it is a problem rooted in injustice. Eliminate injustice and you can eliminate poverty. It will not be quick or easy, but it can be done. Together, let’s do what’s right. Photo: Albert González Farran/Oxfam Photo: Albert González World without poverty Empowering smallholder farmers to make food fair “I am from a backward caste. My father and mother in law don’t like me because of that. They always wanted to expel me from the family. I don’t have any job, I don’t own any land, and I am poor.’ — Suresho Aina, 39, a smallholder farmer in Uttar Pradesh, India. Photo: Ricky Wong/Oxfam What’s wrong? Women smallholder farmers in Uttar Pradesh make up 38 per cent of the total agricultural workforce. Due to traditional values and gender inequality, they are not recognised by men, by society, and by the government as farmers. As a result, they have very limited access to resources, government schemes and programmes, and micro credit. Worse still, most women farmers do not have access to or control over land, which seriously hinders their productivity and income. According to a study conducted by Oxfam, only six per cent of women in Uttar Pradesh own land, less than one per cent participate in government training programmes, and only eight per cent have control over agricultural income. What’s Oxfam doing? Oxfam is supporting women smallholder farmers in India to improve their yields and income by setting up 375 women groups (40 women per group) at the village level.