Relationship Between Risk and Return of Stocks Listed at the Nairobi Securities Exchange

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

An Evaluation of Factors Contributing to the Stock Market Liquidity Constraints Or Companies Listed on the Namibian Stock Exchange

International Journal of Accounting Research (IJAR) Vol. 2, No. 8, 2015 Publisher: ZARSMI, UAE, and Regent Business School, South Africa AN EVALUATION OF FACTORS CONTRIBUTING TO THE STOCK MARKET LIQUIDITY CONSTRAINTS OR COMPANIES LISTED ON THE NAMIBIAN STOCK EXCHANGE Albert Mutonga Matongela Graduate of the Regent Business School, Durban Republic of South Africa External Supervisor Attached to the Regent Business School, Durban, Republic of South Africa Anis Mahomed Karodia akarodia@regent,ac.za Professor, Senior Academic and Researcher, Regent Business School, Durban, Republic of South Africa Abstract In 1992, the Namibian Stock Exchange (NSX) was established, amongst others, to facilitate investment in capital markets. Stakeholders have raised concerns that liquidity is low on the NSX. The African Economic Outlook has pointed out that the NSX faces the challenge of few locally issued securities and low liquidity. On its part, the Ministry of Finance is of the view that the NSX is characterized by low levels of liquidity. The aim of this research was to evaluate factors contributing to the stock market liquidity constraints for companies listed on the NSX. Key Words: Evaluation, Factors, Stock Exchange, Liquidity, Regulatory, Corporate Governance, Capital Markets Introduction Stock market liquidity is linked to savings mobilization, long-term capital investment, risk diversification, stock market development and economic growth (Ahmed, Shahbaz and Ali, 2008: 191; Antonios, 2010: 8; Omet, 2011: 4). Lack of liquidity is a serious impediment to the efficient functioning of stock markets and impacts stock prices adversely (Bokpin (2013: 2143). Liquidity is the ability to trade financial securities easily and at a low cost (Yartey, 2008: 16). -

Apêndice a País Código MIC Identificação Do Mercado/MTF

Apêndice A Código País MIC Identificação do Mercado/MTF ALBANIA XTIR TIRANA STOCK EXCHANGE ALGERIA XALG ALGIERS STOCK EXCHANGE ARGENTINA XBUE BUENOS AIRES STOCK EXCHANGE ARGENTINA XMAB MERCADO ABIERTO ELECTRONICO S.A. ARGENTINA XMEV MERCADO DE VALORES DE BUENOS AIRES S.A. ARGENTINA XMTB MERCADO A TERMINO DE BUENOS AIRES S.A. ARGENTINA XBCM BOLSA DE COMMERCIO DE MENDOZA S.A. ARGENTINA XROS BOLSA DE COMERCIO ROSARIO ARMENIA XARM ARMENIAN STOCK EXCHANGE AUSTRALIA XNEC STOCK EXCHANGE OF NEWCASTLE LTD AUSTRALIA XASX ASX OPERATIONS PTY LIMITED AUSTRALIA XSFE SYDNEY FUTURES EXCHANGE LIMITED AUSTRALIA XYIE YIELDBROKER PTY LTD AUSTRIA XNEW NEWEX OESTERREICHISCHE TERMIN- UND AUSTRIA XOTB OPTIONENBOERSE, CLEARING BANK AG AUSTRIA XWBO WIENER BOERSE AG AZERBAIJAN XIBE BAKU INTERBANK CURRENCY EXCHANGE BAHAMAS XBAA BAHAMAS INTERNATIONAL STOCK EXCHANGE BAHRAIN XBAH BAHRAIN STOCK EXCHANGE BANGLADESH XCHG CHITTAGONG STOCK EXCHANGE LTD. BANGLADESH XDHA DHAKA STOCK EXCHANGE LTD BARBADOS XBAB SECURITIES EXCHANGE OF BARBADOS BELGIUM XBRU EURONEXT BRUSSELS BELGIUM XEAS NASDAQ EUROPE BERMUDA XBDA BERMUDA STOCK EXCHANGE LTD, THE BOLIVIA XBOL BOLSA BOLIVIANA DE VALORES S.A. BOTSWANA XBOT BOTSWANA STOCK EXCHANGE BRAZIL XBVP BOLSA DE VALORES DO PARANA BRAZIL XBBF BOLSA BRASILIERA DE FUTUROS BRAZIL XRIO BOLSA DE VALORES DO RIO DE JANEIRO SOCIEDADE OPERADORA DO MERCADO DE BRAZIL XSOM ATIVOS S.A. BRAZIL XBMF BOLSA DE MERCADORIAS E FUTUROS BRAZIL XBSP BOLSA DE VALORES DE SAO PAULO BULGARIA XBUL BULGARIAN STOCK EXCHANGE MONTREAL EXCHANGE THE / BOURSE DE CANADA XMOD MONTREAL -

Smes and Public Equity Financing: a New Dataset of SME Boards in Emerging-Market and Developing Economies

SMEs and Public Equity Financing: A New Dataset of SME Boards in Emerging-Market and Developing Economies John Schellhase and Jim Woodsome August 2017 Introduction In recent years, a number of stock exchanges in emerging-market and developing economies have established dedicated market segments for small and medium-sized enterprises (SMEs). The main purpose of these SME boards, as they are often called, is to expand access to equity finance for relatively small but growing firms with the potential, as a group, to significantly contribute to economic growth and employment. In some cases, SME boards also serve as feeder exchanges, incubating firms for later graduation to a stock exchange’s main board. Today, there around 30 dedicated SME boards in emerging-market and developing economies, the majority of which have been established in the last decade or so. Due to the role these firms can play in creating jobs and diversifying economies, improving access to finance for SMEs is a long-standing policy goal in developed and developing countries alike. As banks have curbed their lending to SMEs in the wake of the global financial crisis, policymakers and industry bodies are now increasingly emphasizing non-bank financing alternatives for SMEs. Public equity financing is one option that may be suitable for fast-growing SMEs with the capacity to meet the listing requirements. SME boards may contribute to expanding financial access for SMEs both directly, by facilitating access to public equity financing, and indirectly, by incentivizing listing firms to improve their financial reporting and corporate governance practices, which may, in turn, make them more appealing to credit-based lenders. -

Doing Data Differently

General Company Overview Doing data differently V.14.9. Company Overview Helping the global financial community make informed decisions through the provision of fast, accurate, timely and affordable reference data services With more than 20 years of experience, we offer comprehensive and complete securities reference and pricing data for equities, fixed income and derivative instruments around the globe. Our customers can rely on our successful track record to efficiently deliver high quality data sets including: § Worldwide Corporate Actions § Worldwide Fixed Income § Security Reference File § Worldwide End-of-Day Prices Exchange Data International has recently expanded its data coverage to include economic data. Currently it has three products: § African Economic Data www.africadata.com § Economic Indicator Service (EIS) § Global Economic Data Our professional sales, support and data/research teams deliver the lowest cost of ownership whilst at the same time being the most responsive to client requests. As a result of our on-going commitment to providing cost effective and innovative data solutions, whilst at the same time ensuring the highest standards, we have been awarded the internationally recognized symbol of quality ISO 9001. Headquartered in United Kingdom, we have staff in Canada, India, Morocco, South Africa and United States. www.exchange-data.com 2 Company Overview Contents Reference Data ............................................................................................................................................ -

Listing in Africa

LISTING IN AFRICA 2014/2015 kpmg.com/Africa Contents Introduction 04 Key De nitions 08 Summary of Listing Criteria 12 Botswana 24 Kenya 44 Mauritius 68 Namibia 88 Nigeria 114 South Africa 132 Zambia 160 Zimbabwe 186 Key sources 210 Contributors 211 Introduction Purpose of this publication There is an increasing interest in Africa as a potential investment destination due to the fact that the developed markets are not expected to grow as they have done previously. In addition, Africa is seen to be becoming more politically mature and easier to access and this, together with its growing population and rise in consumption, is adding to its attractiveness for foreign investors. Africa also has vast tracts of unutilised land and signicant mineral and other resources. The purpose of this document is to provide an overview of the considerations for listing, listing criteria, processes, documentation requirements and continuing obligations relating to certain African stock exchanges, as well as an overview of the composition and liquidity of the equity markets in these countries. This information will give potential investors and applicant issuers’ valuable insights into listing in these environments. Advantages and disadvantages of an equity listing Some of the advantages of listing equity on any stock exchange are set out below: › Enables the company to raise equity capital to fund existing projects and acquisition opportunities and/or to reduce current gearing levels in the company; › Provides a future and current exit route for the existing -

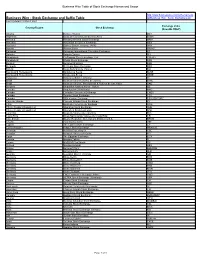

Stock Exchange and Suffix Table Ml/Business Wire Stock Exchanges.Pdf Last Updated 12 March 2021

Business Wire Table of Stock Exchange Names and Usage http://www.businesswire.com/schema/news Business Wire - Stock Exchange and Suffix Table ml/Business_Wire_Stock_Exchanges.pdf Last Updated 12 March 2021 Exchange Value Country/Region Stock Exchange (NewsML ONLY) Albania Bursa e Tiranës BET Argentina Bolsa de Comercio de Buenos Aires BCBA Armenia Nasdaq Armenia Stock Exchange ARM Australia Australian Securities Exchange ASX Australia Sydney Stock Exchange (APX) APX Austria Wiener Börse WBAG Bahamas Bahamas International Securities Exchange BS Bahrain Bahrain Bourse BH Bangladesh Chittagong Stock Exchange, Ltd. CSEBD Bangladesh Dhaka Stock Exchange DSE Belgium Euronext Brussels BSE Bermuda Bermuda Stock Exchange BSX Bolivia Bolsa Boliviana de Valores BO Bosnia and Herzegovina Banjalucka Berza BLSE Bosnia and Herzegovina Sarajevska Berza SASE Botswana Botswana Stock Exchange BT Brazil Bolsa de Valores do Rio de Janeiro BVRJ Brazil Bolsa de Valores, Mercadorias & Futuros de Sao Paulo SAO Bulgaria Balgarska fondova borsa - Sofiya BB Canada Aequitas NEO Exchange NEO Canada Canadian Securities Exchange CNSX Canada Toronto Stock Exchange TSX Canada TSX Venture Exchange TSX VENTURE Cayman Islands Cayman Islands Stock Exchange KY Chile Bolsa de Comercio de Santiago SGO China, People's Republic of Shanghai Stock Exchange SHH China, People's Republic of Shenzhen Stock Exchange SHZ Colombia Bolsa de Valores de Colombia BVC Costa Rica Bolsa Nacional de Valores de Costa Rica CR Cote d'Ivoire Bourse Regionale Des Valeurs Mobilieres S.A. BRVM Croatia -

Brvm Stock Market 2015 Year in Review

BRVM Stock Market 1 February 2015 BRVM STOCK MARKET 2015 YEAR IN REVIEW Cheikh Yakhoub Niang, CFA Tel: (+221) 33-869-3140 [email protected] BRVM, the African Leader in 2015 In a year full of difficulties and general disappointment, the West African stock market posted the best yearly performance of the continent at 17.7%. Over 2014 and 2015, the regional market two main indices, the BRVM 10 and the BRVM Composite, experienced cumulative increases of respectively 59% and 83%. Performing as well as the Côte d’Ivoire economy, all but one sector of the BRVM market displayed positive performances during 2015. Overall, it was a good year for the BRVM investors that enjoyed a significantly higher trading volume, with a far greater contribution of smaller cap stocks. Another Bullish Year Ahead Globally, the consensus is expecting another difficult year with low oil and commodities prices among other down trends. However, things are likely to stabilize towards the end of 2016. The BRVM should be able to benefit from its low correlation with other global markets and enjoy the expected growth in the WAEMU zone. Agriculture will still be enduring a down commodities market and make it hard for these companies to perform. 2015 Stock Performances UNXC; 257.5% BNBC; 142.5% PRSC; 139.6% ABJC; 118.5% ONTBF; 114.3% TTLC; 109.5% NTLC; -9.1% SOGC; -19.7% SVOC; -25.5% PALC; -29.0% UNLC; -32.4% SPHC; -34.6% Source: BRVM Data BRVM 2015 Year in Review | 1 TABLE OF CONTENTS GLOSSARY ......................................................................... 3 WHAT HAPPENED ON THE BRVM MARKET DURING 2015 . -

The Nigerian Stock Exchange 2020 Market Review and 2021 Outlook

Contents 1. Global Capital Market Review 2020__________________________________________________ 2 2. NSE Market Performance 2020 _____________________________________________________ 3 2.1. NSE Equity Market Review _____________________________________________________ 3 2.2. NSE Fixed Income Market Review _______________________________________________ 4 2.3. NSE ETF Market Review _______________________________________________________ 4 3. NSE Strategic Performance 2020 ____________________________________________________ 6 4. Outlook for 2021 ________________________________________________________________ 9 Appendix 1: NSE Index Performance ____________________________________________________ 10 Appendix 2: NSE Market Performance __________________________________________________ 11 The Nigerian Stock Exchange 2020 Market Recap and 2021 Outlook 1 1. Global Capital Market Review 2020 The year 2020 was indeed a historic one for global capital markets. Facing buffeting headwinds, including an unprecedented pandemic, a weak global economy leading to manufacturing recessions, historically low crude oil prices, elevated geopolitical risks and social unrest – to name just a few, world markets saw sharp swings and steep losses, but largely remained resilient and orderly amid rising uncertainty. The outbreak of the novel coronavirus disease (Covid-19) and its rapid spread across the globe in the first quarter of the year, triggered panic selling by global investors. According to the World Federation of Exchanges (WFE), global capital markets -

NAIROBI SECURITIES EXCHANGE 2015 Annual Results Announcement 24 March 2016

NAIROBI SECURITIES EXCHANGE 2015 Annual Results Announcement 24 March 2016 By Geoffrey O. Odundo Chief Executive Contents 3 9 Economic Market Environment Performance 13 Financial 22 Highlights Outlook & Strategy 19 Corporate Action Economic Environment 2015 Global Economic Review Global growth in 2015, slowed to 2.4% from 2.6% in 2014 due to: • U.S. monetary policy tightening. Federal Reserve Committee raised the target range for the federal funds rate to 0.25% to 0.5%; • Weakening commodity prices, global trade, and capital flows; • Gradual slowdown and rebalancing of economic activity in China away from investment and manufacturing toward consumption and services; and • Fragile liquidity conditions. 2015 Regional Economic Review GDP 5.5% 63 Listed Companies Market Capitalization: USD 26.4 Billion GDP 5.0% 16 Listed Companies $ Market Capitalization: USD 2.4 Billion GDP 6.9% 17 Listed Companies Market Capitalization: USD 11.4 Billion GDP 7.5% 7 Listed Companies Market Capitalization: USD 3.8 Billion Kenya Macro Economic Environment in 2015 •Benchmark interest rate was raised by 300 basis points to 11.5% in mid- •Firm GDP growth at 5.5% 2015) •Inflation rose to 8% above CBK upper limit of 7.5% + •Weakening Currency - •13% depreciation in exchange rate (USD/KES) Neutral Outlook •CBR rate at 11.50% •Continued money market liquidity tightness. •Most listed companies predicted to report stunted earnings growth NSE Strategic Plan 2015-2019 New Product Innovation • DRIVE REVENUE GROWTH AND Pillar 1 DIVERSIFICATION Technology Enhancement • BUILD REPUTATION AS A TRUSTED Our COMPANY AND AN INVESTMENT Strategic DESTINATION OF CHOICE Global Best Pillar 2 Drivers Practices • STRENGTHEN ORGANIZATIONAL CAPABILITIES & TALENT Pillar 3 MANAGEMENT NSE Organization Restructure Market Performance 2015-2014 Comparison Key Performance Indicators Market Indicator Jan- Dec 2014 Jan-Dec-2015 %Change NSE 20 Share Index 5,113 4,040 (20.99) NSE All Share Index (NASI) 170 145 (14.71) Market P/E Ratio 15 14 2.50 Market Capitalization (Kshs. -

Securities Reference File 5

Security Reference File Doing data differently V4.1 Company Overview Helping the global financial community make informed decisions through the provision of comprehensive, accurate, timely and affordable securities and economic data services With more than 25 years’ experience, we offer comprehensive and accurate securities reference, corporate actions and pricing data for derivatives, equities, fixed income, and investment funds around the globe. We also cover economic data extensively. We understand how crucial financial and economic data is and take a different ap- proach as to how we proceed: • We do not rent data, we sell it • We do not have onerous redistribution rules • We customize our services to meet your needs • We cover all countries - no matter how large or small • Finally, we are the cheapest As a result of our on-going commitment to providing cost-effective and innovative data solutions, while ensuring the highest standards, EDI has achieved the internationally recognized quality and security certifications ISO 9001 and ISO 27001. Headquartered in the United Kingdom, we have operations in Australia, Canada, Germany, India, Morocco, South Africa, and the United States. Our Support Team is available on +44 (0) 207 269 8915, 24 hours a day, Monday to Friday and closed on Christmas and New Year’s Day. www.exchange-data.com 1 Security Reference File Contents Different Types of Security Reference File Feeds 4 ISINs Format 4 Sedol Format 4 FIGIs Format 4 Bloomberg Format 4 Detailed Note File 4 Securities Reference File 5 PIT (Point -

CAPITAL RAISING OPPORTUNITIES for SMALL and MEDIUM ENTERPRISES (Smes) on STOCK EXCHANGES in AFRICA

CAPITAL RAISING OPPORTUNITIES FOR SMALL AND MEDIUM ENTERPRISES (SMEs) ON STOCK EXCHANGES IN AFRICA CONTENTS FOREWORD: ASEA 1 Enabling SMEs to fuel Africa's economic growth ABOUT THIS REPORT 2 INTRODUCTION 4 Unlocking the continent’s socio-economic growth potential through SMEs FINANCING OPPORTUNITIES FOR SMES 7 Financing SMEs through African Capital Markets ALTERNATIVE SOURCES OF FUNDING 17 What support can be provided to SMEs? WHAT NEEDS TO BE DONE 20 What needs to be done to making SMEs more attractive to investors? CONCLUSION 24 RECOMMENDATIONS 25 FOREWORD FOREWORD Enabling small and medium ENTERPRISES TO FUEL AFRICA’S economic growth mall and Medium Enterprises (SMEs) play a crucial role in the opportunities available for these SMEs to raise capital on promoting economic development, especially on the African exchanges. Scontinent. In both developed and developing countries, they contribute to the stability of national economies, enabling them to This report is a consolidation of survey responses of 15 ASEA cope with the shocks of economic cycles. member exchanges that participated in the survey, and it unpacks why SMEs list, the requirements for listing and the challenges facing On the continent, SMEs create close to 80% of the continent’s SMEs wanting to list. It also explores how governments and the employment1 and have contributed to the development of a new private sector can contribute meaningfully, in order to truly make middle class that is in turn fuelling demand for new goods and SMEs the engine for long-term growth in Africa. services. The group also requested that the participating exchanges provide Given the incredible potential that SMEs have to fuel growth, information on a listed SME, in order to give first-hand insight into especially in the developing world, the role of SMEs in economic their individual reasons for listing, the success of their listing and the development has been one of the most popular discussions challenges they face in staying listed. -

African Company Attendees (Confirmed As of July 30, 2014)

African Company Attendees (Confirmed as of July 30, 2014) Hosts • The Honorable Penny Pritzker, Secretary of Commerce • The Honorable Michael R. Bloomberg, Founder of Bloomberg LP & Bloomberg Philanthropies and 108th Mayor of New York City African Companies • Achat Service International (Niger) • Aeolus Kenya Ltd. (Kenya) • Africa Finance Corporation (Nigeria) • African Trans Services (A.T.S.) (Mali) • African Development Bank (Côte d'Ivoire) • African Rainbow Minerals (South Africa) • Air Burkina (Burkina Faso) • Air Traffic and Navigation Services (South Africa) • Amahoro Energy (Rwanda) • Amor Benamor (Algeria) • A-Post (Nigeria) • Attijari Wafa Bank (Morocco) • Banque Atlantique Niger (Niger) • Belstar Development LLC (Ghana) • Bidco Oil Refineries (Kenya) • BMCE Bank (Morocco) • Bok Group (Chad) • Burundi Chamber of Commerce, Industry, Agriculture & Handicrafts (Burundi) • Cabo Verde Shores (Cabo Verde) • Carbon Holdings (Egypt) • Casablanca Stock Exchange (Morocco) 1 Last Updated: 7/30/2014 • Central Bank of Nigeria (Nigeria) • Chamber of Commerce and Industry of Mali (Mali) • COMATRANS Group (Cameroon) • Compagnie Sahelienne d'Entreprises (Senegal) • Confédération Générale des Entreprises Marocaines (Morocco) • Dangote Industries (Nigeria) • Dar es Salaam Stock Exchange (Tanzania) • Doudou Tainamor (Comoros) • EA-Power Limited (Tanzania) • East Africa Capital Partners (Kenya) • East African Business Council (Tanzania) • Econet Wireless International (South Africa) • El Sewedy Group (Egypt) • Electricity Supply Corporation of Malawi