Alliance Facts & Figures

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

New Renault TRAFIC

New Renault TRAFIC November 2019 A TRAFIC for every profession Instantly distinguishing New Renault TRAFIC is a more expressive front-end design, with full-LED headlights incorporated into the C-shaped lighting signature that represents the identity of the Renault line. A bolder grille, with details such as a new holder for the Renault logo and chrome finishing strip, plus a new ‘Urban Grey’ colour complete the revised styling. Your everyday activity is unique. New Renault TRAFIC has been reinvented in order to meet your specific needs. In its various versions, from the Panel Van to the Crew Van, you will find the one which will help you achieve the best performance. In addition to its remarkable loading capacities, it now has an updated design, a 2.0 l engine and an automatic gearbox which makes for an even smoother driving experience. A Strong personality New Renault TRAFIC re-asserts its style and stands out from the outset. The front-end panel, front grille with chrome and C-shape light signature with full LED lighting combine dynamism and robustness. More than a van, New Renault TRAFIC is designed to improve your comfort and safety. A ‘Mobile Office’ on wheels The New Renault TRAFIC has been specifically designed to meet your professional needs and provide you the ability to have a truly ‘Mobile Office’, packed with clever solutions. From tablet and smartphone cradles, to hidden laptop storage, to our integrated MediaNav system, we aim to keep you connected even when on the go. The cabin area is spacious and comfortable, creating optimal driving conditions with ergonomic seats with lumbar adjustment, adjustable steering wheel and climate control all available. -

Renault Trafic 2014 - Present

Leading supplier of bonded glass and slider windows for van conversions. Renault Trafic 2014 - present For sales contact Autoglasinbouw www.autoglasinbouw.nl +31 (0) 23-5243810 [email protected] The information contained in this document is confidential, privileged and only for the benefit of the intended recipient. It may not be used, published or redistributed without the prior written consent of AM Auto Ltd or affiliated partners. Colors Types of windows Green ( Clear ) - 77% LT Product Range Privacy - 17% LT Fixed Dummy Half Slider L1 (SWB) L2 (LWB) Passenger’s side with a side loading door Passenger’s side with a side loading door Fixed : VV14-R2S Fixed : VV14-RS1 Fixed : VV14-R2L Fixed : VV14-RS1 Dummy : VV14-R2S-B Half Slider : VV14-R1-HS Dummy : VV14-R2L-B Half Slider : VV14-R1-HS Driver’s side without a side loading door Driver’s side without a side loading door Fixed : VV14-LS1 Fixed : VV14-L2S Fixed : VV14-LS1 Fixed : VV14-L2L Half Slider : VV14-L1-HS Dummy : VV14-L2S-B Half Slider : VV14-L1-HS Dummy : VV14-L2L-B Barn doors Tailgate H1 (Standard roof) Fixed +wires : VV-TB-W Fixed : VVNSFRRD4005 Fixed : VVNSFRRD4005 H2 (High roof) Barn doors Fixed : VV-HLB P Fixed : VV-HRB P AUTOGLASINBOUW | AM AUTO ©2020 | RENAULT TRAFIC ( 2014 - PRESENT ) | 2 Internal view Front Half Slider Rear Half Slider AUTOGLASINBOUW | AM AUTO ©2020 | RENAULT TRAFIC ( 2014 - PRESENT ) | 3 We stock windows for... Citroen Berlino Nissan NV200 2007 - present 2010 - present Citroen Jumpy Nissan NV300 1995 - 2007 / 2007 - 2016 / 2017 - present 2014 - present -

Tan Chong Motor Holdings Berhad

THIS CIRCULAR IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION. If you are in any doubt as to the course of action you should take, you should consult your stockbroker, bank manager, solicitor, accountant or other professional adviser immediately. If you have sold or transferred all your ordinary shares in Tan Chong Motor Holdings Berhad (“TCMH” or “Company”), you should at once hand this Circular, together with the attached Form of Proxy, to the agent through whom the sale or transfer was effected for transmission to the purchaser or transferee. The Notice of the Extraordinary General Meeting of TCMH and the Form of Proxy are enclosed. Malaysia Securities Exchange Berhad takes no responsibility for the contents of this Circular, makes no representation as to its accuracy or completeness and expressly disclaims any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this Circular. TAN CHONG MOTOR HOLDINGS BERHAD (Company No. 12969-P) (Incorporated in Malaysia) CIRCULAR TO SHAREHOLDERS IN RELATION TO · PROPOSED RENEWAL OF AUTHORITY FOR THE COMPANY TO PURCHASE ITS OWN ORDINARY SHARES; · PROPOSED RENEWAL OF SHAREHOLDERS’ MANDATE FOR RECURRENT RELATED PARTY TRANSACTIONS OF A REVENUE OR TRADING NATURE AND PROPOSED SHAREHOLDERS’ MANDATE FOR RECURRENT RELATED PARTY TRANSACTIONS OF A REVENUE OR TRADING NATURE WITH RENAULT S.A.S. GROUP; AND · PROPOSED ACQUISITION BY TAN CHONG & SONS MOTOR COMPANY SDN BHD, A WHOLLY- OWNED SUBSIDIARY OF TAN CHONG MOTOR HOLDINGS BERHAD, OF ALL THAT PARCEL OF LEASEHOLD LAND EXPIRING ON 31 DECEMBER 2796 SITUATED AT 2½ MILE, JALAN PENDING CONSISTING OF 6,410 SQUARE METRES, MORE OR LESS, AND DESCRIBED AS LOT 9378, SECTION 64, KUCHING TOWN LAND DISTRICT FROM TUNG PAO SDN BHD, A WHOLLY-OWNED SUBSIDIARY OF WARISAN TC HOLDINGS BERHAD FOR A CASH CONSIDERATION OF RM2,690,000. -

Sustainability Report 2016 Nissan Motor Corporation Sustainability Report 2016 01

SUSTAINABILITY REPORT 2016 NISSAN MOTOR CORPORATION SUSTAINABILITY REPORT 2016 01 CONTENTS VIEWING THIS REPORT 2 1 3 This Sustainability Report is an interactive PDF. You can easily access the information 5 7 you need by clicking on the navigation tabs and buttons. 4 6 8 ● Section Tabs BUILDING TOMORROW’S SUSTAINABLE CONTENTS INTRODUCTION CEO MESSAGE MOBILITY SOCIETY Sustainability Strategies Click the tabs to jump to the top page of each section. ● Navigation Buttons ● Link Buttons 02 16 Go back one page Jump to linked page Return to previously viewed page Jump to information on the web 03 43 Go forward one page Jump to information in CSR Data 04 53 ● Our Related Websites 07 62 14 70 ■ Editorial Policy ■ Third-Party Assurance Nissan publishes an annual Sustainability Report as a way of sharing Click the link at right to view the third-party assurance. information on its sustainability-related activities with stakeholders. 108 77 This year’s report reviews the progress and results achieved in fiscal page_136 2015, focusing on the concept of Building Tomorrow’s Sustainable Mobility Society and the eight sustainability strategies. ■ Forward-Looking Statements ■ Scope of the Report This Sustainability Report contains forward-looking statements 136 95 Period Covered: The report covers fiscal 2015 (April 2015 to March on Nissan’s future plans and targets and related operating 2016); content that describes efforts outside this period is indicated investment, product planning and production targets. There can in the respective sections. Organization: Nissan Motor Co., Ltd., be no assurance that these targets and plans will be achieved. foreign subsidiaries and affiliated companies in the Nissan Group. -

Communiqué De Presse

Communiqué De Presse 18 DÉCEMBRE 2014 The Renault Duster Team sets its sights on the Top 10 on the 2015 Dakar Rally For its third participation on the legendary event, the official Renault Duster Team will compete in the 2015 edition of the Dakar, from the 4th to 17th of January, with two allnew cars and a power plant from the RenaultNissan Alliance, with the objective of finishing in the Top 10. Since 2013, Renault Argentina has entered in one of the most demanding and exhilarating events in the world : the Dakar Rally. 29th in the general classification in its maiden participation, the team capitalized on its experience in 2014 to finish 14th overall and fourth in class. The two teams composed of Emiliano Spataro and Benjamín Lozada as well as José García and Mauricio Malano prepared for the Dakar by competing in three rounds of the Argentinian Rally CrossCountry Championship, taking a win and three runnerup results. This year, Renault Sport Technologies is more than ever before supporting the squad in bringing all its expertise and latest innovations in to order to offer the two Dusters the best assets to finish in the Top 10. To achieve this goal, the Renault Duster Team has two new Renault Dusters provided with cuttingedge technologies. More modern and powerful, the vehicles are equipped with V8 engines from the RenaultNissan Alliance, producing 380 brake horsepower. Renault Argentina is also reinforcing its logistics and its race team providing optimized technical support in Argentina, Chile and Bolivia, the countries that will be crossed for the 2015 edition. -

Pricing for the Period 1 December 2016 to 31 March 2017 5-Dec-16

Contract RT57/2016 to 2018 - Pricing for the period 1 December 2016 to 31 March 2017 5-Dec-16 Price Including New Price Incl. Ref # RT Number Category Decription Award Responder Name Make and Model Ranking VAT VAT RT57-00-01 Four/Five seater sedan or hatch 4/5 doors-piston Toyota SA Motors Pty Ltd Yaris Hybrid Xs (41N) displacement up to 1900cm3, Hybrid (pool vehicles only) 1 R 264,287.00 R 264,287.00 1 GP RT57-00-01 Four/Five seater sedan or hatch 4/5 doors-piston MAPLEY Trading (Pty) Limited Honda CR-Z 1.5 Hybrid Manual 3door 4Seater displacement up to 1900cm3, Hybrid (pool vehicles only) 2 R 361,000.00 R 361,000.00 2 GP RT57-00-01 Four/Five seater sedan or hatch 4/5 doors-piston BMW (SOUTH AFRICA) BMW I 3(REX) displacement up to 1900cm3, Hybrid (pool vehicles only) 3 R 570,420.00 R 574,125.35 3 GP RT57-00-01 Four/Five seater sedan or hatch 4/5 doors-piston NISSAN SOUTH AFRICA PTY LTD L10 Nissan Leaf Electric Vehicle displacement up to 1900cm3, Hybrid (pool vehicles only) 4 R 675,342.00 R 668,960.46 4 GP RT57-00-02 Four/Five seater sedan or hatch 4/5 doors-piston Toyota SA Motors Pty Ltd Auris XR HSD (27C) displacement 1901cm3 to 3000cm3, Hybrid (Pool vehicles 1 R 370,425.00 R 370,425.00 5 only) GP RT57-01-12-01 Four seater sedan 4 door or hatch 3-5 doors ,piston VUKANI MARKETING AND Chery QQ3 0.8TE A/C displacement up to 1250 cm (Petrol/Diesel) Petrol/Diesel) CONSULTING 1 R 91,794.00 R 89,675.82 6 (Pool and subsidised vehicles) GP/SUB RT57-01-12-01 Four seater sedan 4 door or hatch 3-5 doors ,piston VUKANI MARKETING AND Chery QQ3 0.8TX -

Renault Master Z.E. March 2018

Press Kit February 2018 Renault Master Z.E. © Thomas Motta / Prodigious Production (00142013) Renault MASTER Z.E. and Renault EASY CONNECT for Fleet: expertise at the service of professionals #LCVexpert, #MasterZE . Renault Pro+ is broadening its range of electric LCVs with the introduction of the Master Z.E. large electric van – the ideal workhorse for emissions-free access to city centres. Master Z.E. is ideally suited to last-mile deliveries. It's designed for everyone who believes environmental issues are fundamental. o Master Z.E. benefits from the know-how of Renault – Europe's leader in electric vehicles: a new-generation battery and a high energy efficiency engine give it a 74 mile real-world driving range and a charging time appropriate to its duties (fully charged in just 6 hours). o Master Z.E. offers many of the tailor-made solutions available from Renault Pro+ – Europe's leader in vans: a genuine workhorse, a large number of versions, a dedicated network and made-to-measure conversions. As part of Renault EASY CONNECT solutions, Renault Pro+ introduces Renault EASY CONNECT for Fleet, an ecosystem of connected services for business users that simplifies managing vehicle fleets and reduces running costs. o Renault EASY CONNECT for Fleet provides secure, affordable connectivity to report fleet data. o Renault Pro+ is working with the biggest names in fleet management to offer a broad range of services and meet business users' widest range of needs. o Renault EASY CONNECT for Fleet will be available on the entire range of Renault vehicles in Europe by mid-2018. -

IHS Automotive Supplying the Oems Supplierbusiness Supplying the Renault-Nissan Alliance

IHS Automotive Supplying the OEMs SupplierBusiness Supplying the Renault-Nissan Alliance 2014 edition supplierbusiness.com SAMPLE IHS Automotive SupplierBusiness | Supplying the Renault-Nissan Alliance Contents Overview .......................................................................................................................................................................... 6 Global market overview .............................................................................................................................................. 6 Financial data ............................................................................................................................................................... 6 Renault-Nissan alliance financial overview .............................................................................................................. 7 Product and platform strategy ...................................................................................................................................... 9 Company background and strategy review ............................................................................................................. 9 Major model programmes ....................................................................................................................................... 10 1. Renault Clio ............................................................................................................................................................ 10 2. Nissan -

Renault KANGOO ZE Hydrogen

RENAULT RUNS ON HYDROGEN WITH MASTER Z.E. HYDROGEN AND KANGOO Z.E. HYDROGEN Renault Press 1 Tel.: + 33 (0)1 76 84 63 36 media.renault.com groupe.renault.com Contents Groupe Renault introduces hydrogen in its light commercial vehicle range .................................... 3 Hydrogen a natural fit with Groupe Renault strategy ................................................................ 4 Renault and Symbio, making mobility progress together since 2014 .......................................... 5 Hydrogen as an ideal supplement to electric vehicles .................................................................... 6 Up to 3 times more range than 100% electric vehicles ............................................................... 6 Rapid charging: filled up in 10 minutes tops .............................................................................. 7 More sustainable and silent vehicles (70 db) ............................................................................. 7 Qualifying for aid for hydrogen vehicle purchases ..................................................................... 7 Certified vehicles ...................................................................................................................... 7 Designed for tomorrow’s cities ................................................................................................. 8 And easy maintenance ............................................................................................................. 8 Renault MASTER Z.E. Hydrogen ................................................................................................... -

Renault Laguna Coupé Press Release Renault Laguna Coupé Renault Laguna Coupé, Pleasure Through Sheer Beauty

RENAULT LAGUNA COUPÉ PRESS RELEASE RENAULT LAGUNA COUPÉ RENAULT LAGUNA COUPÉ, PLEASURE THROUGH SHEER BEAUTY Renault Laguna Coupé is the third vehicle launched in the Laguna III programme. It is undoubtedly the model that most readily conveys the feeling of driving pleasure and comfortable riding. Its genes are unmistakably inherited from the acclaimed Fluence concept car. This new model also shares the same qualities as the Laguna Coupé Concept show car such as the efficiency of its 4Control four-wheel steering chassis, the performance of the new V6 dCi engine and the elegant, uncluttered lines of its body. This new product also benefits from all the segment’s latest technologies, including a Bose® Sound System audio system, Carminat Bluetooth® DVD navigation and the keyless functions enabled by its hands-free card. Following its unveiling at the 2008 Paris Motor Show, Renault Laguna Coupé will progressively go on sale in its principal European markets from early October. The market’s best practices and toughest quality standards have been applied to its design and production, allowing customers to benefit from a three-year / 150,000km warranty. Meanwhile, the catalogue boasts of a comprehensive selection of equipment, engines, colours, materials and accessories which enable owners to go even further in their desire to customize their vehicle, and in their quest for pleasure; this pleasure brought by sheer beauty. "Beauty is even harder to express than happiness" Simone de Beauvoir 01 02 THE ESSENTIALS OF TIMELESS BEAUTY 4CONTROL CHASSIS WITH FOUR-WHEEL STEERING FOR UNMATCHED CONTROL 03 04 A CHOICE OF EIGHT ENGINES, WITH A HIGHLIGHT NEW PREMIUM AUDIO AND NAVIGATION TECHNOLOGIES ON PERFORMANCE 05 06 SALOON CAR COMFORT IN A COUPÉ BODY CUSTOMISED STYLE 07 08 EXCEPTIONAL QUALITY BEST-LEVEL SAFETY 09 A DEMANDING, EFFICIENTLY-MANAGED AND PROFITABLE PROJECT 01 THE ESSENTIALS OF TIMELESS BEAUTY The flowing lines of the Renault Laguna Coupé’s elegant and uncluttered design express timeless beauty and sheer motoring enjoyment. -

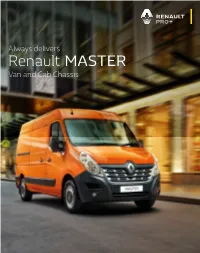

Renault MASTER Van and Cab Chassis ‘Master Stacks up Well on Just About Every Front.’

Always delivers Renault MASTER Van and Cab Chassis ‘Master stacks up well on just about every front.’ motoring.com.au Overseas model shown Overseas model shown The right choice for your business. Making the decisions that give the best outcomes for the least risk is what separates successful business owners from the rest. And that’s what makes Renault Master an easy choice. You’ll always find Renault vans amongst the market leaders for value, but that’s only part of the story – you spend a lot of time behind the wheel, so there’s also a comfortable and feature packed cabin that doubles as your office on the move. Large glass areas and standard sensors and cameras make working in restricted areas simpler and safer. And Master’s predictable handling makes for a safe and enjoyable drive no matter the load out back. Available in five body sizes and three body styles, in both front and rear wheel drive configurations, you’ll have no trouble finding a Master to suit your business. Overseas model shown 5 Your office on the road. Overseas model shown Open the driver’s door and you’ll find a spacious and functional cabin that’s made to measure for commercial vehicle drivers. The dash includes plenty of handy storage, and the passenger bench features a fold down centre seat with an integrated table that’s made for a lap-top or lunch. There’s an overhead storage shelf for your paperwork and optional under seat storage with 90L of space that’s perfect for a lunch cooler or valuable items you’d prefer not to leave out on display. -

Tan Chong Motors: Interesting Short Tenor MYR Bond Investment Idea at 5.935% YTM

Tan Chong Motors: Interesting Short Tenor MYR Bond Investment Idea at 5.935% YTM Issues Maturity Currency Amount Issued Ratings (RAM) TCMH 4.5% 22Nov2019 (MYR) 22/11/2019 MYR RM 250 Million A1 TCMH 4.7% 24Nov2021 (MYR) 24/11/2021 MYR RM 500 Million A1 In this article, we will explain the reasons why we think TCMH 4.5% 22Nov2019 (MYR) is an interesting investment idea in the MYR bond space. Figure 1: Edaran Tan Chong Motor's 3S centre in Kuching. Source: paultan.org Company Overview Tan Chong Motors Holdings Berhad (TCH) is listed on Bursa Malaysia with a market capitalization of RM 1.21 billion as of 9 April 2018. It is a conglomerate involved in a myriad of business activities locally and abroad; from assembly to marketing of motor vehicles and automotive parts manufacturing to property development. TCH derives most of its revenue from its automobile division. The company is the franchise holder and exclusive distributor of Nissan passenger and light commercial vehicles, as well as Renault vehicles in Malaysia. TCH’s vehicles sales enjoyed a market share of 4.7% of the total industry volume in 2017, according to data from the Malaysian Automotive Association (Chart 1 and Chart 2). Chart 1: TCH makes up 4.7% of the car sales market share in 2017 Malaysia car sales market share in 2017 (%) Perodua 16.4 Toyota 4.7 35.5 Honda Proton 12.3 Nissan Others 12.1 19 Source: Malaysian Automotive Association, iFAST compilations. Data as of 31 Dec 2017 Chart 2: Nissan’s tumbling market share in the past 3 years Market Share Number of Vehicle Sold 8.00% 47,235 50,000 40,706 7.00% 45,000 40,000 6.00% 35,000 27,154 5.00% 30,000 4.00% 25,000 7.10% 7% 4.70% 3.00% 20,000 15,000 2.00% 10,000 1.00% 5,000 0.00% 0 2015 2016 2017 Source: Malaysian Automotive Association, iFAST compilations.