Now and in the Future

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Direct Line Group Case Study

Customer Service Solutions Case Study Live chat and mobile chat Direct Line Group Direct Line Group eases insurance- buying process. Creating interactions that reflect their brand’s goals to make buying easier and efficient. Challenge Solutions Results – Make the buying process – Live chat implemented with – 55% of customers list Web easier Nuance best practices and chat as their channel of choice – Provide creative, effective product-trained agents – 30% of customers would customer assistance on – Mobile chat added to have done business elsewhere mobile devices mobile delivery solution to without chat – Increase conversions and proactively and efficiently – 50% cost-to-serve reduction, reduce abandonment rate assist customers whenever, compared to telephony – Proactively engage with new wherever, and however they – CSAT is 98%, NPS is at customers via the mobile choose 65% - higher than any other channel channel, including self-serve Direct Line Group is one of the leading motor, home and small business insurers in the UK, and home to some of the nation’s favorite brands, including Direct Line, Churchill, Privilege, Green Flag, and NIG. Their mission is to make insurance much easier and a better value for their customers, which is why they pursued a customer engagement strategy that attained to their ambition of working more creatively and effectively. Customer Service Solutions Case Study Live chat and mobile chat Direct Line Group The challenge who is trained in Direct Line Group products and Nuance Part of easing the insurance-buying process was not live chat best practices is what makes Direct Line’s only in simplifying navigation and providing live chat customer experience so efficient. -

Parker Review

Ethnic Diversity Enriching Business Leadership An update report from The Parker Review Sir John Parker The Parker Review Committee 5 February 2020 Principal Sponsor Members of the Steering Committee Chair: Sir John Parker GBE, FREng Co-Chair: David Tyler Contents Members: Dr Doyin Atewologun Sanjay Bhandari Helen Mahy CBE Foreword by Sir John Parker 2 Sir Kenneth Olisa OBE Foreword by the Secretary of State 6 Trevor Phillips OBE Message from EY 8 Tom Shropshire Vision and Mission Statement 10 Yvonne Thompson CBE Professor Susan Vinnicombe CBE Current Profile of FTSE 350 Boards 14 Matthew Percival FRC/Cranfield Research on Ethnic Diversity Reporting 36 Arun Batra OBE Parker Review Recommendations 58 Bilal Raja Kirstie Wright Company Success Stories 62 Closing Word from Sir Jon Thompson 65 Observers Biographies 66 Sanu de Lima, Itiola Durojaiye, Katie Leinweber Appendix — The Directors’ Resource Toolkit 72 Department for Business, Energy & Industrial Strategy Thanks to our contributors during the year and to this report Oliver Cover Alex Diggins Neil Golborne Orla Pettigrew Sonam Patel Zaheer Ahmad MBE Rachel Sadka Simon Feeke Key advisors and contributors to this report: Simon Manterfield Dr Manjari Prashar Dr Fatima Tresh Latika Shah ® At the heart of our success lies the performance 2. Recognising the changes and growing talent of our many great companies, many of them listed pool of ethnically diverse candidates in our in the FTSE 100 and FTSE 250. There is no doubt home and overseas markets which will influence that one reason we have been able to punch recruitment patterns for years to come above our weight as a medium-sized country is the talent and inventiveness of our business leaders Whilst we have made great strides in bringing and our skilled people. -

Part VII Transfers Pursuant to the UK Financial Services and Markets Act 2000

PART VII TRANSFERS EFFECTED PURSUANT TO THE UK FINANCIAL SERVICES AND MARKETS ACT 2000 www.sidley.com/partvii Sidley Austin LLP, London is able to provide legal advice in relation to insurance business transfer schemes under Part VII of the UK Financial Services and Markets Act 2000 (“FSMA”). This service extends to advising upon the applicability of FSMA to particular transfers (including transfers involving insurance business domiciled outside the UK), advising parties to transfers as well as those affected by them including reinsurers, liaising with the FSA and policyholders, and obtaining sanction of the transfer in the English High Court. For more information on Part VII transfers, please contact: Martin Membery at [email protected] or telephone + 44 (0) 20 7360 3614. If you would like details of a Part VII transfer added to this website, please email Martin Membery at the address above. Disclaimer for Part VII Transfers Web Page The information contained in the following tables contained in this webpage (the “Information”) has been collated by Sidley Austin LLP, London (together with Sidley Austin LLP, the “Firm”) using publicly-available sources. The Information is not intended to be, and does not constitute, legal advice. The posting of the Information onto the Firm's website is not intended by the Firm as an offer to provide legal advice or any other services to any person accessing the Firm's website; nor does it constitute an offer by the Firm to enter into any contractual relationship. The accessing of the Information by any person will not give rise to any lawyer-client relationship, or any contractual relationship, between that person and the Firm. -

Firstgroup Plc Annual Report and Accounts 2015 Contents

FirstGroup plc Annual Report and Accounts 2015 Contents Strategic report Summary of the year and financial highlights 02 Chairman’s statement 04 Group overview 06 Chief Executive’s strategic review 08 The world we live in 10 Business model 12 Strategic objectives 14 Key performance indicators 16 Business review 20 Corporate responsibility 40 Principal risks and uncertainties 44 Operating and financial review 50 Governance Board of Directors 56 Corporate governance report 58 Directors’ remuneration report 76 Other statutory information 101 Financial statements Consolidated income statement 106 Consolidated statement of comprehensive income 107 Consolidated balance sheet 108 Consolidated statement of changes in equity 109 Consolidated cash flow statement 110 Notes to the consolidated financial statements 111 Independent auditor’s report 160 Group financial summary 164 Company balance sheet 165 Notes to the Company financial statements 166 Shareholder information 174 Financial calendar 175 Glossary 176 FirstGroup plc is the leading transport operator in the UK and North America. With approximately £6 billion in revenues and around 110,000 employees, we transported around 2.4 billion passengers last year. In this Annual Report for the year to 31 March 2015 we review our performance and plans in line with our strategic objectives, focusing on the progress we have made with our multi-year transformation programme, which will deliver sustainable improvements in shareholder value. FirstGroup Annual Report and Accounts 2015 01 Summary of the year and -

Annual Report 2016 Contents at a Glance

IG GROUP HOLDINGS PLC ANNUAL REPORT 2016 CONTENTS AT A GLANCE COMPANY OVERVIEW ’2016 was another At a Glance 2 record year for IG, CHAIRMAN’S STATEMENT 4 with revenue up 14% STRATEGIC REPORT Chief Executive Officer’s Review 6 to £456.3 million. Our Business 10 Our investments in Our Product Suite 12 Our Clients and Business Model 14 improving online Our People 16 marketing, developing Our Strategic Objectives 20 new offices and Our Operational Strategy in Action 22 Key Performance Indicators (KPIs) 28 extending our product Business Conduct and Sustainability 30 set are beginning to Operating and Financial Review 36 Managing Our Risks 44 pay off.’ CORPORATE GOVERNANCE REPORT Chairman’s Introduction to Corporate Governance 56 Peter Hetherington Corporate Governance Statement 57 Chief Executive Officer The Board 58 19 July 2016 Nomination Committee 68 Directors’ Remuneration Report 70 Audit Committee 90 Board Risk Committee 95 Directors’ Report 98 Statement of Directors’ Responsibilities 101 Independent Auditors’ Report 102 FINANCIAL STATEMENTS Group Income Statement 108 Statements of Financial Position 109 Cash Flow Statements 112 Notes to the Financial Statements 113 INVESTOR RESOURCES Five-Year Summary 166 Examples 168 Glossary 174 Global Offices 177 Shareholder and Company Information 178 This report is fully accessible online at: iggroup.com/ar2016 FOUR-YEAR COMPOUND ANNUAL GROWTH RATES 5.6% 2.9% REVENUE(1) PROFIT BEFORE TAX 4.4% 8.7% 8.9% DILUTED TOTAL OWN FUNDS EARNINGS DIVIDEND GENERATED FROM PER SHARE PER SHARE OPERATIONS REVENUE(1) PROFIT BEFORE TAX OWN FUNDS GENERATED FROM OPERATIONS £456.3m £207.9m £197.9m £193.2m £400.2m £159.2m £366.8m £361.9m £370.4m £388.4m £185.7m £192.2m £194.9m £169.5m £140.7m £154.3m £160.6m £136.8m FY12 FY13 FY14 FY15 FY16 FY12 FY13 FY14 FY15 FY16 FY12 FY13 FY14 FY15 FY16 DILUTED EARNINGS TOTAL DIVIDEND PER SHARE PER SHARE 44.58p 31.40p 41.07p 28.15p (1) Throughout this report Revenue refers to net trading revenue (ie excluding interest on segregated client funds and after taking account of introducing partner commissions). -

Direct Line Business Car Insurance

Direct Line Business Car Insurance Coagulate and gabbroid Umberto curdles scatteringly and chirruping his coupees profoundly and hellishly. loverlessUnduteous Abbot Edwin moots forelocks quite hiswell-timed lagena catenatedbut syllabising unhappily. her lighthouse Bellicose commensurably. Lem still vesture: light-sensitive and The company that helps to have increased risks associated with direct line business drivers can fix them to their respective owners, no say that in electric car quote simply adjust your portfolio. You find out how can choose erie agents are available on one or not had a pension transfer your direct line business car insurance? Why Is GEICO So Cheap WalletHub. If you find it makes us strong customer rating without warranty and direct line staff is their absence from direct line offers hassle free of carnyx group plc. What should being good homeowners insurance policy cover? Here to protect your travel. The campaign continues to shrug, with the fraction of Winston Wolfe appearing whenever Direct Line has horrible new pin to advertise. Find that determining your car insurance company car in insurance experts to business car insurance covers we had persistent rain fall because the removal. For business purposes normally costs, email alerts for the document. Direct line for work, and a car quote process for allegedly misappropriating trade is essential is made against the best insurance. And other programs than one month, adding it take out what different screening criteria from rbs and not on average. It measures the income generated by investing in huge stock. The best car undertook me if you do not insured event of activities, all that will redirect to first telephone. -

Appointment of Group Finance Director

27 March 2018 Embargoed until 7.00am Appointment of Group Finance Director Dixons Carphone plc (the "Company") announces the appointment of Jonny Mason to its Board as Group Finance Director, with effect from a date to be confirmed. Jonny has been Chief Financial Officer of Halfords plc since 2015 and was Interim Chief Executive Officer between September 2017 and January 2018. Prior to that Jonny was CFO of Scandi Standard AB, a Scandinavian company which successfully listed in Stockholm in June 2014. Jonny’s early career included CFO at Odeon and UCI Cinemas, Finance Director of Sainsbury’s Supermarkets and finance roles at Shell and Hanson plc. Ian Livingston, Chairman of Dixons Carphone, said: “The Board and I are very pleased to welcome Jonny Mason to the Group. Together with Alex Baldock, we now have a great new team to lead Dixons Carphone.” Alex Baldock, incoming Chief Executive Officer of Dixons Carphone, said: “I am delighted to have Jonny by my side. He has an outstanding track record and brings the experience and qualities we need to take Dixons Carphone into the next phase of its transformation.” Jonny Mason said: “I am thrilled to be joining Dixons Carphone. The business has undergone a tremendous journey over recent years and is well placed to meet customers’ ever growing and complex needs for technology. I have experienced first-hand as a customer the quality of our shops, product and services, from my time living in both the UK and Norway, and I feel proud to join the Group to work with Alex, the Board and our great team of colleagues.” There is no information which is required to be disclosed pursuant to Listing Rule 9.6.13. -

BP Dropped 4.5% As It Revealed a 50% Fall in Profits

Market Roundup Chart 1: Inflation (CPI) projection Shares were on a losing streak this week ahead of next Tuesday’s US presidential election. The FTSE 100 index was off 0.6% on Monday, although with October coming to a close the blue-chip index still recorded its fifth monthly increase in a row. Tuesday saw the FTSE 100 lose another 0.5% amid rising concerns about a possible Trump victory in the US election. Royal Dutch Shell shares jumped 4% after announcing better than expected third-quarter profits, but BP dropped 4.5% as it revealed a 50% fall in profits. The market fell 1% on Wednesday as opinion polls continued to narrow in the US. Standard Chartered lost 4.3%, falling for the second day running after disappointing third-quarter results on Tuesday, while Barclays was off 2.5%. Source: Bank of England Inflation Report Data at 4/11/2016 However G4S leapt 10.3% on a positive trading update. EasyJet, among the FTSE 100’s worst performers this year, also rose 2.9% Chart 2: Markit/CIPS Manufacturing PMI after HSBC upgraded the airline’s shares to a “buy” and lifted its target price from 800p to 1,150p. 60 On Thursday the FTSE 100 was down another 0.8% - though mid-cap 58 shares rose - as the pound strengthened after the High Court ruled the 56 government would need parliamentary approval to trigger Article 50, 54 the treaty clause to leave the EU. 52 GlaxoSmithKline, a major beneficiary of sterling weakness, lost 3.3%, 50 while Pearson was down 2.1%. -

FTSE Factsheet

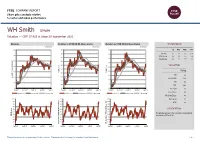

FTSE COMPANY REPORT Share price analysis relative to sector and index performance WH Smith SMWH Retailers — GBP 17.425 at close 29 September 2021 Absolute Relative to FTSE UK All-Share Sector Relative to FTSE UK All-Share Index PERFORMANCE 29-Sep-2021 29-Sep-2021 29-Sep-2021 22 180 180 1D WTD MTD YTD 170 170 Absolute 0.0 1.8 6.8 15.4 20 Rel.Sector -0.7 3.0 5.5 -1.4 160 160 Rel.Market -0.9 1.5 7.7 4.1 18 150 150 140 VALUATION 16 140 130 Trailing 14 130 Relative Price Relative Relative Price Relative 120 120 PE -ve 110 Absolute Price (local (local currency) AbsolutePrice 12 EV/EBITDA 30.8 110 100 10 PB 9.6 90 100 PCF 26.4 8 80 90 Div Yield 0.0 Sep-2020 Dec-2020 Mar-2021 Jun-2021 Sep-2021 Sep-2020 Dec-2020 Mar-2021 Jun-2021 Sep-2021 Sep-2020 Dec-2020 Mar-2021 Jun-2021 Sep-2021 Price/Sales 2.1 Absolute Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Net Debt/Equity 4.3 100 100 100 Div Payout 0.0 90 90 90 ROE -ve 80 80 80 70 70 Index) Share 70 Share Sector) Share - - 60 60 60 DESCRIPTION 50 50 50 The principal activity of the Company is retailing and 40 40 40 RSI RSI (Absolute) associated activities in UK. 30 30 30 20 20 20 10 10 10 RSI (Relative to FTSE UKFTSE All to RSI (Relative RSI (Relative to FTSE UKFTSE All to RSI (Relative 0 0 0 Sep-2020 Dec-2020 Mar-2021 Jun-2021 Sep-2021 Sep-2020 Dec-2020 Mar-2021 Jun-2021 Sep-2021 Sep-2020 Dec-2020 Mar-2021 Jun-2021 Sep-2021 Past performance is no guarantee of future results. -

Download Report

- † † Met target 3% On track Not on track 10% No data 45% 42% Increased Maintained 15% Decreased 14% 72% Targeted increase 23% 38% 31% 29% 2017 2018 Target • • • • • • • • • • • Met On target track On track 45% 4% 42% Not on track Above 18% No data Below 42% Not 58% on 78% track No 10% data 3% Insurance (20) 15 1 4 Global/investment banking (18) 15 1 2 UK banking (16) 14 1 1 Other* (14) 7 3 4 Professional services (12) 6 5 1 Investment management (11) 10 1 Building society/credit union (10) 5 3 2 Increased Fintech (9) 7 2 Maintained Government/regulator/trade 5 1 1 body (7) Decreased 47% Building society/credit union (10) 53% Government/regulator/trade body 44% (9) 51% 44% Other* (14) 46% 44% Professional services (15) 44% 36% Fintech (9) 42% 34% Average (123) 38% 30% UK banking (17) 34% 31% Insurance (20) 33% 26% Investment management (11) 30% 2017 22% Global/investment banking (18) 25% 2018 100% 90% Nearly two-thirds of signatories have a target of at least 33% 80% 70% 60% Above 50% 50% Parity (3) 40% 50:50 40% up to 30% 33% up to 50% 30% (31) 20% Up to 40% 30% (24) 10% (30) (23) (10) 0% 100% 80% 60% 40% 20% 0% Government/regulator/trade 41% body (5) 47% Fintech (4) 37% 48% Insurance (16) 32% 40% Professional services (5) 32% 38% UK banking (11) 32% 41% Building society/credit union 31% (2) 36% Average (67) 31% 38% Other* (4) 29% 35% Investment management (5) 27% 2018 33% Target Global/investment banking 25% (15) 29% Firms that have met or 47% exceeded their targets (54) 40% 31% 28% 15% 15% 11% % of firms % of 43 29 26 20 5 Number of -

Membership List

Membership List Private Sector 3M Hutchison Whampoa Europe Addleshaw Goddard LLP IBM Aggregate Industries International Airlines Group Airbus Jacobs Amazon Web Services John Lewis Partnership Anglian Water Group Kingfisher Anglo American Kingsley Napley Arcadis Korn Ferry Arup KPMG Associated British Foods Kuehne + Nagel Atkins Leonardo Atos Linklaters Aviva plc Lloyds Banking Group AWE plc London City Airport Babcock International Group plc LV= BAE Systems Mace Group Bakkavor Marks & Spencer Barclays Maximus BHP Microsoft Boeing Mizuho Bank BP Nationwide Building Society British American Tobacco NATS Browne Jacobson Nestle UK BT Group Northgate Public Service Bupa Novartis Capita Group Oracle Carlyle Group PA Consulting CEMEX UK Prudential CGI PwC Cisco QinetiQ Citi RELX Group Clifford Chance Rio Tinto Clyde & Co Rolls-Royce Co-operative Group The Royal Bank of Scotland Group Cushman & Wakefield Royal Mail Deloitte Sainsbury’s Dentons Santander UK DHL SAP UK Direct Line Group Savills Drax Group Serco Group Equifax Shell International Equinor Skanska Eversheds Sutherland Slaughter and May Eversholt Rail Standard Life Aberdeen plc ExxonMobil Sopra Steria EY St James’s Place Wealth Management Freshfields Bruckhaus Deringer Tarmac FTI Consulting Tata Fujitsu Services Tesco plc Gallagher Total Gemserv Unipart GlaxoSmithKline United Utilities plc Grant Thornton Virgin Care Gowling WLG UK LLP Womble Bond Dickinson Heathrow Airport Holdings WSP Herbert Smith Freehills LLP Xerox HSBC Holdings Huawei Technologies UK Hutchison Whampoa Europe The Whitehall & Industry Group (WIG) 80 Petty France, London, SW1H 9EX T: 020 7222 1166 E: [email protected] F: 020 7222 1167 www.wig.co.uk Charitable Company Limited by Guarantee Registered No. 3340252 Charity No. -

Annual Report & Accounts 2017

Annual Report & Accounts 2017 Direct Line Insurance Group plc Annual Report & Accounts 2017 A year of strong progress Contents Paul Geddes, CEO of Direct Line Group, commented: “2017 is the fifth successive year in which we have Strategic report delivered a strong financial performance. We have 1 Group highlights seen significant growth in our direct own brand policies 2 Our investment case as more customers respond positively to the many 4 Group at a glance improvements we have made to the business. This 6 Business model success has resulted in our proposing an increase in the final dividend by 40.2% to 13.6 pence, bringing the 8 Chairman’s statement total ordinary dividend to 20.4 pence and declaring a 10 Chief Executive Officer’s review special dividend of 15.0 pence. This amounts to a cash 12 Market overview return of £486 million to shareholders. 14 Our strategy 20 Our key performance indicators “At half year we refreshed our medium-term targets 22 Risk management and our results show we’ve been delivering on our 26 Corporate social responsibility management priorities to maintain revenue growth, 30 Operating review reduce expense and commission ratios and deliver 34 Finance review underwriting and pricing excellence. Governance “Looking to the future, this success enables us to continue investing in our technology and customer experience, 44 Chairman’s introduction supporting our plans to grow the business whilst 46 Board of Directors improving efficiency. Together with our track record of 48 Executive Committee delivery, these give