United Kingdom Minerals Yearbook 2008

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Accordance with the Generally Accepted Accounting Principles

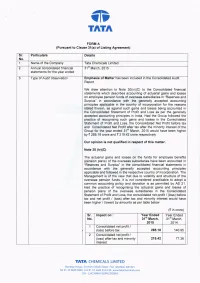

TI'I TNTN FORM A (Pu6uant to Clause 31(a) of Listing Agreement) Sr Particu lars Details No. 1 Name of the Company Tata Chemicals Limited 2. Annual consolidated financial 31 March, 2015 statements for the year ended 3. Type of Audit observation Emphasis of Matter has been included in the Consolidated Audit Report. We draw atlention to Note 3o(ivxc) to the Consolidated financial statements which describes accounting of actuarial gains and losses on employee pension funds of overseas subsidiaries in "Reserves and Surplus" in accordance with the generally accepted accounting principles applicable in the country of incorporation for the reasons stated therein, as against such gains and losses being accounted in the Consolidated Statement of Profit and Loss as per the generally accepted accounting principles in lndia. Had the Group followed the practice of recognising such gains and losses in the Consolidated Statement of Profit and Loss, the Consolidated Net Profit before tax and Consolidated Net Profit after tax after the minority interest of the Group for the year ended 31"r March, 2015 would have been higher by { 285.18 crore and { 219.42 crore respectively. Our opinion is not qualified in respect o, this matter. Note 30 (ivXC) The actuarial gains and losses on the funds for employee benefits (pension plans) of the overseas subsidiaries have been accounted in "ReseNes and Surplus" in the consolidated financial statements in accordance with the generally accepted accounting principles applicable and followed in the respective country of incorporation. The Management is of the view that due to volatility and structure of the overseas pension funds, it is not considered practicable to adopt a common accounting policy and deviation is as permifted by AS 21. -

Pleistocene and Flandrian Natural Rock Salt Subsidence at Arclid Green, Sandbach, Cheshire Peter Worsley

Pleistocene and Flandrian Natural Rock Salt Subsidence at Arclid Green, Sandbach, Cheshire Peter Worsley Abstract. This applied geological case study concerns the Quaternary geomorphological evolution of a small part of the lowland Cheshire characterised by ‘equifinal subsidence landforms’ resulting from the processes of rock salt dissolution and post Last Glacial Maximum glacial ice meltout. The context relates to environmental issues arising from the quarrying of Chelford Formation industrial ‘silica sands’. Problems related to natural and human induced rock salt dissolution are reviewed. The respective roles of Triassic bedrock halites, collapsed strata, periglacial alluvial sands and multiple glaciation in determining the local stratigraphy and allied landforms are discussed. The morphology and fill of a post glacial subsidence area is examined. It is concluded that natural rock salt dissolution is the principal process influencing the superficial deposits and geomorphology of the study area and that this process has been active over hundreds of thousand years. The deposition and survival of thick silica sands and the glacigenic sediments beneath is probably due to halite dissolution. In eastern Cheshire, a significant part of the lowland A further complicating factor is human induced salt geomorphology is characterised by an excellent subsidence exacerbated by historic shallow mining for example of what, in ‘General Systems Theory’ jargon, salt and wild brine pumping, for example, Ward, would be termed ‘equifinal behaviour’ (Chorley, (1887), Calvert (1915), Cooper (2002), Sherlock 1964), also known as polygenesis. Such behaviour in a (1922), Wallwork (1956, 1960), Waltham (1989), and geomorphological context envisages that different Waltham et al (2005). Following the near universal initial earth surface processes have resulted in similar enforced abandonment of these extraction techniques morphological outcomes. -

Feasibility Study of the Salt Mines Storage Route, Step 1

DT B 99 101 C Issue C : 7/2/00 (Issue B : 22/12/99) Page : 1 Feasibility Study of the Salt Mines Storage Route ------------------------ Step 1 report ------------------------ Appraisal of the salt mines storage route for residues from incineration Checking JACQUINOT Bernard Expert Senior ENVIGEPRO 21/12/99 Author KIRRMANN Clément Project Manager ENVIGEPRO 13/9/00 CK RESPONSABILITIES NOM Prénom Fonction Pole ou Société Date Visa Bertin Technologies DIFFUSION : Clément KIRRMANN ECVM Mr. De Grève (1 ex) Bernard Jacquinot Mrs Unni Musdalslien (1 ex) (by E-mail) ECVM (10 copies) Sept 13th, 2000 BC.001.A Centre de Tarnos • avenue du 1er Mai • Z.I. • F 40220 Tarnos • Tél. : (33) (0)5 59 64 86 48 • Fax (33) (0)5 59 64 49 64 Adresse commerciale : Parc Technologique de Bois d'Arcy - ZAC du Pas du Lac 10, avenue Ampère - BP 284 - 78053 St Quentin-en-Yvelines Cedex Tél : (33) (0)1 39 30 60 00 - Fax : (33) (0)1 39 30 09 50 y Société Anonyme au capital de 20 000 000 F y RCS Paris B 422 511 204 - Code APE 742 C DT B 99 101 C Page : 2 Référence interne DT B 99 101 B Système hôte WORD 6 (95) /CK Fonds documentaire Dossier d’affectation Général Nomenclature de gestion affaire 00559 lot 1 Document contractuel OUI HISTORIQUE DES EVOLUTIONS MODIFICATIONS Authors / Checking Indice Date (raisons principales, paragraphes et pages concernés, références des demandes de modification, ...) A 13/12/99 Création du document C.KIRRMANN Provisional version sent to Mrs Unni Musdalslien and M.De 15/12/99 Grève B 21/12/99 Completed version taking into account comments of -

Integrated-Annual-Report-Fy-2019-20

June 14, 2020 The General Manager The Manager, Listing Department Corporate Relations Department The National Stock Exchange of India Limited BSE Limited Exchange Plaza Phiroze Jeejeebhoy Towers Bandra-Kurla Complex Dalal Street Bandra (E) Mumbai - 400 001 Mumbai - 400 051 Scrip Code: 500770 Symbol: TATACHEM Dear Sir/Madam, Sub.: Annual Report under Regulation 34(1) of the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 (‘Listing Regulations’) This is in furtherance to our letter dated May 22, 2020 wherein the Company had informed that the 81st Annual General Meeting (‘AGM’) of the Company will be held on Tuesday, July 7, 2020 at 3.00 p.m. (IST) via two-way Video Conference / Other Audio Visual Means only, in accordance with the General Circular issued by the Ministry of Corporate Affairs dated May 5, 2020 read with General Circulars dated April 8, 2020 and April 13, 2020 and SEBI Circular dated May 12, 2020. Pursuant to Regulation 34(1) of the Listing Regulations, please find enclosed the Integrated Annual Report of the Company along with the Notice of the 81st AGM and other Statutory Reports for the Financial Year 2019-20, which is also being sent through electronic mode to those Members whose e-mail addresses are registered with the Company/Registrar and Transfer Agent/ Depositories. The same is also available on the website of the Company at https://www.tatachemicals.com/investors/financial-reports/Yearly-reports. This is for your information and records. Thanking you, Yours faithfully, For Tata Chemicals Limited Rajiv Chandan General Counsel & Company Secretary Encl.: as above Advancing Science. -

Saltscape Project, Northwich, Cheshire

Saltscape Project A8: The salt fields investigating the salt production landscape in Northwich’s historic saltscape SALTSCAPE PROJECT, NORTHWICH, CHESHIRE ASSESSMENT OF SITES FOR ARCHAEOLOGICAL FIELDWORK PROJECT A8: THE SALT FIELDS INVESTIGATING THE SALT PRODUCTION LANDSCAPE IN NORTHWICH’S HISTORIC SALTSCAPE REPORT NO 2015-001 Chris Hewitson Senior Environment Officer Regeneration and Culture Cheshire West and Chester [email protected] February 2015 Version 1 1 Saltscape Project A8: The salt fields investigating the salt production landscape in Northwich’s historic saltscape 1. Background prevalent. The site is currently appears to be used The project seeks to investigate using for recreational off-road vehicles. archaeological methods the salt production Risks and Issues landscape north-east of Northwich. This area The area is subsiding and collapses of the Trent and contains the tourist nodes of the Lion Salt Works Mersey Canal have occurred in the last two years. and the Anderton Boat Lift. Now, these represent Open areas of water are located centrally within the the only industrial structures from the 19th and area of the mine and public and volunteer access early 20th century in an essentially post-industrial may be limited because of the potential risks. landscape. The project seeks to re-associate the wider public with the earlier landscape and aims to The land is privately owned and clearly marked as reassert the link between the visible structures and such. There is a strong likelihood that access issues the buried past. In doing so the project will training will prevent archaeological work in this area. for volunteers in archaeological techniques, increase education in the historic industrial Site 2 – Alliance Works landscape and deliver a new and updated data set Location: Adjacent to the Trent and Mersey Canal on the historic environment of the ‘Saltscape’ and the Lion Salt Works (NGR SJ 671 754). -

United Kingdom Minerals Yearbook 2006 British Geological Survey

United Kingdom Minerals Yearbook 2006 British Geological Survey United Kingdom Minerals Yearbook 2006 Statistical data to 2005 By L E Hetherington, T J Brown, P A J Lusty, K Hitchen and T B Colman Keyworth, Nottingham: British Geological Survey 2007 BRITISH GEOLOGICAL SURVEY © NERC 2007 All rights reserved The full range of Survey publications is available from the Copyright in materials derived from the British Geological BGS Sales Desk at Nottingham, Edinburgh and London; Survey’s work is owned by the Natural Environment see contact details below or shop online at Research Council (NERC) and/or the authority that www.geologyshop.com commissioned the work. You may not copy or adapt this publication without first obtaining permission. Contact the The London Information Office also maintains a reference BGS Intellectual Property Rights Section, British Geological collection of BGS publications including maps for consultation. Survey, Keyworth, e-mail [email protected]. The Survey publishes an annual catalogue of its maps and You may quote extracts of a reasonable length without other publications; this catalogue is available from any prior permission, provided a full acknowledgement is given of the BGS Sales Desks. of the source of the extract. The British Geological Survey carries out the geological survey of Great Britain and Northern Ireland (the latter as All communications regarding the content of this an agency service for the government of Northern Ireland), publication should be addressed to the Programme and of the surrounding continental shelf, as well as its Manager, Economic Minerals, British Geological Survey, basic research projects. It also undertakes programmes of Keyworth, Nottingham NG12 5GG British technical aid in geology in developing countries as = 0115 936 3493 Fax 0115 936 3520 arranged by the Department for International Development e-mail: [email protected] and other agencies. -

United Kingdom Minerals Yearbook 2005 British Geological Survey United Kingdom Minerals Yearbook 2005

United Kingdom Minerals Yearbook 2005 British Geological Survey United Kingdom Minerals Yearbook 2005 Statistical data to 2004 By L E Taylor, T J Brown, P A J Lusty, K Hitchen, T B Colman and D E Highley Keyworth, Nottingham: British Geological Survey 2006 BRITISH GEOLOGICAL SURVEY © NERC 2006 All rights reserved The full range of Survey publications is available from the Copyright in materials derived from the British Geological BGS Sales Desk at Nottingham, Edinburgh and London; Survey’s work is owned by the Natural Environment see contact details below or shop online at Research Council (NERC) and/or the authority that www.geologyshop.com commissioned the work. You may not copy or adapt this publication without first obtaining permission. Contact the The London Information Office also maintains a reference BGS Intellectual Property Rights Section, British Geological collection of BGS publications including maps for consultation. Survey, Keyworth, e-mail [email protected]. The Survey publishes an annual catalogue of its maps and You may quote extracts of a reasonable length without other publications; this catalogue is available from any prior permission, provided a full acknowledgement is given of the BGS Sales Desks. of the source of the extract. The British Geological Survey carries out the geological survey of Great Britain and Northern Ireland (the latter as All communications regarding the content of this an agency service for the government of Northern Ireland), publication should be addressed to the Programme and of the surrounding continental shelf, as well as its Manager, Economic Minerals, British Geological Survey, basic research projects. It also undertakes programmes of Keyworth, Nottingham NG12 5GG British technical aid in geology in developing countries as ຜ 0115 936 3493 Fax 0115 936 3520 arranged by the Department for International Development e-mail: [email protected] and other agencies. -

Britishsalt.Pdf

Completed acquisition by British Salt Limited of New Cheshire Salt Works Limited The OFT’s decision on reference under section 22(1) given on 26 May 2005. Full text of decision published 24 June 2005. Please note square brackets indicate information excised or replaced by a range at the request of the parties for reasons of commercial confidentiality. PARTIES 1. British Salt Limited (British Salt) is a wholly-owned subsidiary of British Salt Holdings LLC. British Salt is based in Middlewich, Cheshire and is active in the production and sale of vacuum salt products. 2. New Cheshire Salt Works Limited (NCSW) is a family-owned business based in Northwich, Cheshire. NCSW is also active in the production and sale of vacuum salt products. In 2004, NCSW’s UK turnover was [ ]. TRANSACTION 3. On 24 February 2005, British Salt acquired the entire issued share capital of NCSW. The administrative deadline in this case expires on 27 May 2005. 4. On 30 March 2005, the OFT accepted initial undertakings from British Salt and British Salt Holdings LLC pursuant to section 71 of the Enterprise Act 2002 (the Act). JURISDICTION 5. As a result of this transaction British Salt and NCSW have ceased to be distinct. The parties’ combined UK shares of supply of each of Pure Dried Vacuum (PDV) salt and compacted salt exceed 25 per cent and the share of supply test in section 23 of the Act is therefore met. The OFT therefore believes that it is or may be the case that a relevant merger situation has been created. -

Parish Plan 2010

Wincham Parish Plan 2010 A Vision for Wincham… The Parish of Wincham,Cheshire 2010 database right and copyright Crown © data Survey Ordnance Contains Wincham Parish Plan 1 What is a Parish Plan? Contents 1 Introduction ............................................................... 2 A Parish Plan is a statement by a 2 History of Wincham ................................................ 3 community of the actions that will most 3 Local Geography ...................................................... 4 benefit the community. 4 Wincham Today ....................................................... 5 Parish Plans are developed from 5 Collecting Residents’ Views ................................. 7 widespread consultation, during which 6 The Environment .................................................. 10 all members of the community have the 7 Planning and Development .............................. 15 opportunity to express their opinions. 8 Leisure ...................................................................... 19 All aspects of the quality of life in a 9 Transport and Highways ................................... 24 community are considered in 10 Policing and Safety ............................................... 28 developing a Parish Plan, including 11 Communication ..................................................... 31 village facilities and services, and social, 12 Waste Treatment Facility .................................. 33 environmental, economic, transport, 13 Young People’s Questionnaire ........................ 35 housing, -

Wincham Word

WINCHAM WORD Edition 3 – 2019 to cover August, September and October 2019 From Wincham Parish Council Delivered free to every home & business in Wincham News and information about our village and close neighbours Stunning poppies at the Wincham War Memorial. These were planted on 11 November 2018 and were seen in their full glory to celebrate the 75th anniversary of D-Day Chairman’s Words by Councillor Ian Parr Wincham Parish Council Following the recent elections, you can see from the back page, I have been afforded the honour to continue as Chairman of Wincham Parish Council. We are delighted to welcome Andrew Webster to the Parish Council, and thank him for offering to help us care for and improve our village for its residents. We look forward to getting to know him and hope he will be happy working with us. We’re quite a nice bunch really, which is why (we hope) we welcome back so many of our returning Councillors. We thank them and hope they continue to give their time and efforts and ideas as they have done so generously in the past years. We still have a vacancy and so if you are interested in becoming a Parish Councillor, please do make contact with our Parish Clerk, Naomi. Her contact details are on the back page. The Parish Meetings take a break in August but resume again in September. If you would like to come to these monthly meetings you would be most welcome. Meanwhile, have a great summer and fingers crossed we get some lovely weather as well. -

Chemical Safety Data Sheet for All Grades Of

Chemical Safety Data Sheet New Cheshire Salt Works Ltd Wincham Lane, Wincham, Northwich, Cheshire CW9 6DD Tel: (01606) 389232 Fax: 0800 132 734 email: [email protected] www: http: //www.ncsw.co.uk All grades of Pure Dried Vacuum Salt (Sodium Chloride) including Pharmaceutical grades and compacted products. 1.1 Identification of the Substance Chemical Name : Sodium Chloride Synonyms : Halite, common salt, evaporated salt Formula : NaC1 CAS Number : 7647-14-5 EINECS Number : 231-598-3 1.2 Identification of the Company Details As Above 1.3 Emergency Telephone / Fax Tel: 01606 42361 (24 hrs) Fax: 01606 48333 (office hours) 2. Composition Composition by weight is 39.4% sodium and 60.6% chlorine. Some grades are treated with part per million levels of non-toxic anti-caking additive, Sodium hexacyanoferrate (II) - E535. 3. Hazard Identification Inhalation : Very high concentrations of salt dust may result in inflammations of the mucus membranes of the respiratory tract. Skin Contact : Dry salt and concentrated solutions can cause withdrawal of fluid from the skin and may, on prolonged contact, produce irritation. Eye Contact : Salt and salt solutions are not toxic to the eye but concentrations much above that of tears cause a stinging sensation. Ingestion : Acute and chronic toxic effects can result from the ingestion of excessive amounts of either salt or brine. Salt should not be used as an emetic to induce vomiting. High concentrations produce inflammatory reactions in the gastrointestinal tract and can cause vomiting, diarrhoea, convulsions and collapse. The ingestion of hypertonic solutions can cause fatal disturbance of body electrolyte and fluid balance particularly in the young and elderly. -

United Kingdom Minerals Yearbook 2005

United Kingdom Minerals Yearbook 2005 British Geological Survey United Kingdom Minerals Yearbook 2005 Statistical data to 2004 By L E Taylor, T J Brown, P A J Lusty, K Hitchen, T B Colman and D E Highley Keyworth, Nottingham: British Geological Survey 2006 BRITISH GEOLOGICAL SURVEY © NERC 2006 All rights reserved The full range of Survey publications is available from the Copyright in materials derived from the British Geological BGS Sales Desk at Nottingham, Edinburgh and London; Survey’s work is owned by the Natural Environment see contact details below or shop online at Research Council (NERC) and/or the authority that www.geologyshop.com commissioned the work. You may not copy or adapt this publication without first obtaining permission. Contact the The London Information Office also maintains a reference BGS Intellectual Property Rights Section, British Geological collection of BGS publications including maps for consultation. Survey, Keyworth, e-mail [email protected]. The Survey publishes an annual catalogue of its maps and You may quote extracts of a reasonable length without other publications; this catalogue is available from any prior permission, provided a full acknowledgement is given of the BGS Sales Desks. of the source of the extract. The British Geological Survey carries out the geological survey of Great Britain and Northern Ireland (the latter as All communications regarding the content of this an agency service for the government of Northern Ireland), publication should be addressed to the Programme and of the surrounding continental shelf, as well as its Manager, Economic Minerals, British Geological Survey, basic research projects. It also undertakes programmes of Keyworth, Nottingham NG12 5GG British technical aid in geology in developing countries as = 0115 936 3493 Fax 0115 936 3520 arranged by the Department for International Development e-mail: [email protected] and other agencies.