年報 Annual Report 目錄 CONTENTS

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Effective Inhibition of Mrna Accumulation and Protein Expression of H5N1 Avian Influenza Virus NS1 Gene in Vitro by Small Interfering Rnas

Folia Microbiol (2013) 58:335–342 DOI 10.1007/s12223-012-0212-8 Effective inhibition of mRNA accumulation and protein expression of H5N1 avian influenza virus NS1 gene in vitro by small interfering RNAs Hanwei Jiao & Li Du & Yongchang Hao & Ying Cheng & Jing Luo & Wenhua Kuang & Donglin Zhang & Ming Lei & Xiaoxiao Jia & Xiaoru Zhang & Chao Qi & Hongxuan He & Fengyang Wang Received: 18 June 2012 /Accepted: 7 November 2012 /Published online: 29 November 2012 # Institute of Microbiology, Academy of Sciences of the Czech Republic, v.v.i. 2012 Abstract Avian influenza has emerged as a devastating protein expressing HEK293 cell lines were established, four disease and may cross species barrier and adapt to a new small interfering RNAs (siRNAs) targeting NS1 gene were host, causing enormous economic loss and great public designed, synthesized, and used to transfect the stable cell health threats, and non-structural protein 1 (NS1) is a mul- lines. Flow cytometry, real-time quantitative polymerase tifunctional non-structural protein of avian influenza virus chain reaction, and Western blot were performed to assess (AIV) that counters cellular antiviral activities and is a the expression level of NS1. The results suggested that virulence factor. RNA interference (RNAi) provides a pow- sequence-dependent specific siRNAs effectively inhibited erful promising approach to inhibit viral infection specifi- mRNA accumulation and protein expression of AIV NS1 cally. To explore the possibility of using RNAi as a strategy in vitro. These findings provide useful information for the against AIV infection, after the fusion protein expression development of RNAi-based prophylaxis and therapy for plasmids pNS1-enhanced green fluorescent protein (EGFP), AIV infection. -

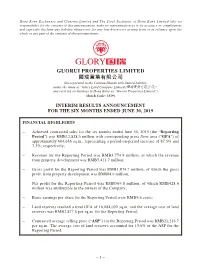

Guorui Properties Limited 國瑞置業有限公司

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. GUORUI PROPERTIES LIMITED 國瑞置業有限公司 (Incorporated in the Cayman Islands with limited liability under the name of “Glory Land Company Limited (國瑞置業有限公司)” and carrying on business in Hong Kong as “Guorui Properties Limited”) (Stock Code: 2329) INTERIM RESULTS ANNOUNCEMENT FOR THE SIX MONTHS ENDED JUNE 30, 2019 FINANCIAL HIGHLIGHTS – Achieved contracted sales for the six months ended June 30, 2019 (the “Reporting Period”) was RMB12,828.3 million with corresponding gross floor area (“GFA”) of approximately 604,636 sq.m., representing a period-on-period increase of 87.5% and 7.3%, respectively; – Revenue for the Reporting Period was RMB3,774.9 million, of which the revenue from property development was RMB3,411.7 million; – Gross profit for the Reporting Period was RMB1,074.7 million, of which the gross profit from property development was RM804.6 million; – Net profit for the Reporting Period was RMB569.8 million, of which RMB428.6 million was attributable to the owners of the Company; – Basic earnings per share for the Reporting Period were RMB9.6 cents; – Land reserves reached a total GFA of 16,084,092 sq.m. and the average cost of land reserves was RMB2,877.8 per sq.m. for the Reporting Period; – Contracted average selling price (“ASP”) for the Reporting Period was RMB21,216.7 per sq.m. -

Haikou Is a Tropical Coastal City, Situated on the Northern Coast of Hainan, by the Mouth of the Nandu River

Haikou is a tropical coastal city, situated on the northern coast of Hainan, by the mouth of the Nandu River. The northern part of the city is Haidian Island, which is separated from the main part of Haikou by the Haidian River, a branch of the Nandu. Haikou was originally a port city. Today, it’s the capital of Hainan province and the most populous city in the province. The city covers 2,280 square kilometers and is home to around 2 million inhabitants. Haikou is on the northern edge of the torrid zone, and is part of the inter-tropical Convergence Zone. April to October is the active period for tropical storms and typhoons, most of which occur between August and September. May to October is the rainy season with the heaviest rainfall occurring in September. Despite its location, the city has a humid subtropical climate, falling just short of a tropical climate, with strong monsoonal influences. Nevertheless, the area has hot summers and warm winters, usually with high humidity. Extremes temperatures have ranged from 2.8 to 39.6 °C (37 to 103 °F) From June to October torrential rains may occur, with 7.0 days annually receiving at least 50 mm (1.97 in) of rain; this period accounts for nearly 70 percent of the annual rainfall of 1,650 mm (65 in). With monthly percentage of possible sunshine ranging from 31% in February to 61% in July, the city receives 2,070 hours of bright sunshine annually. Haikou is a transport hub with flights to many cities and boats to nearby mainland cities such as Beihai and Zhanjiang. -

Info Bulletin.Pmd

The East Asian Seas Congress 2006 The year 2003 created new opportunities for the sustainable development of the seas of East Asia, as it heralded the birth of the first-ever East Asian Seas Congress. The five-day event, held from 8-12 December in Putrajaya, Malaysia, brought together various stakeholders from diverse disciplines to work hand-in-hand to uphold the welfare of the East Asian Seas and ensure the sustainability of their resources. It will be remembered as the occasion where the Sustainable Development Strategy for the Seas of East Asia (SDS-SEA) was endorsed by environment- and ocean- related ministers and senior officials from PEMSEA’s 12 participating countries, with the signing of the Putrajaya Declaration. This Congress, a follow-up to the Putrajaya event, promises to drive the wheels of sustainable development in continuous motion, thereby bringing East Asia closer and closer to ultimately achieving a healthy and bountiful future for its seas and its people. Designed to address pressing coastal and marine environmental issues in practical formats and against a multidisciplinary setting, the various Congress components provide participants the opportunity to take active roles in sustainable development. Features The EAS Congress 2006 features the: • Ministerial Forum on the Implementation of the SDS-SEA* 14–15 December; • International Conference on Coastal and Ocean Governance: One Ocean, One People, One Vision 12–14 December; • Meeting of the EAS Partnership Council* 16 December; and • Youth Forum, Exhibits, Poster Sessions, Field Trip and other Side Events. *By invitation only. Host/Local Organizing Committee The 2006 Congress is being hosted by the government of PR China and co-organized by the State Oceanic Administration (SOA). -

Evergrande Real Estate Group Limited 恒 大 地 產 集 團 有 限 公 司 (Incorporated in the Cayman Islands with Limited Liability) (Stock Code: 3333)

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. Evergrande Real Estate Group Limited 恒 大 地 產 集 團 有 限 公 司 (Incorporated in the Cayman Islands with limited liability) (Stock Code: 3333) DISCLOSEABLE TRANSACTION The Board announces that on 2 December 2015, Shengyu (BVI) Limited, a wholly-owned subsidiary of the Company, as the purchaser, entered into three agreements respectively with the Vendor, pursuant to which the Purchaser agreed to acquire the interests in the relevant shares in and loans to the target companies held by the Vendor. These target companies hold the interests in the Haikou Project, the Huiyang Project and two projects located in Wuhan. Since the Vendor is the seller in these three agreements, such agreements will be aggregated in accordance with Rule 14.22 of the Listing Rules. As the applicable percentage ratios for the Acquisition exceed 5% but are less than 25%, the Acquisition constitutes a discloseable transaction for the Company under Chapter 14 of the Listing Rules and is subject to the reporting and announcement requirements under Chapter 14 of the Listing Rules. 1. INTRODUCTION The Board announces that on 2 December 2015, Shengyu (BVI) Limited, a wholly-owned subsidiary of the Company, as the purchaser, entered into three agreements respectively with the Vendor, pursuant to which the Purchaser agreed to acquire the interests in the relevant shares in and loans to the target companies held by the Vendor. -

Hospitals – Guangzhou Responsible Area the Names and Contact Details

Contact List - Hospitals – Guangzhou Responsible Area The names and contact details of medical services in China appearing below have been compiled by the Department of Foreign Affairs and Trade (DFAT) from publicly-available information. DFAT does not endorse any of the medical services appearing in this list, provides no guarantees as to its currency and does not accept any liability if you choose to engage one of these medical services. Name Address Contact Details Guangzhou Elizabeth Women's No.484 Middle KangWang Road B: + 86 181 2230 0256 Hospital , Liwan District, Guangzhou M: + 86 135 7090 2100 Contact: Michelle Tam City.P .China Fax: +86 20 8132 8199 Email: [email protected] Languages: English, Chinese 广州市荔湾区康王中路484号 Speciality: obstetrics, general pediatrics water birth, Guangzhou gynecology, 4D ultrasound, Guangdong 510010 health check-up China Global Doctor Beijing Alarm Center B: +86 10 5815 1188 Contact: Zou Li 李敏静 M: Fax: +86 8775 9138 Languages: English, Chinese Email: [email protected] Speciality: Global Doctors escort Beijing China Global Doctor 环球医生 D1 2nd Annex, Tianyu Garden B: (86 200 3890-6699 (24 hours) No.136 Linhezhong Rd, Tianhe M: Emergency call: (86) 139-2400- Contact: Global Doctor 环球医生 District 1705 Languages: English, Chinese 广州市天河区林和中路136号天誉花 Fax: (86 20) 3890-6000 Speciality: through our Beijing Email: Alarm Centre, emergency house 园二期D1 [email protected] calls, pre-employment check ups, Tianhe Guangzhou Medical Green Channel, and Guangdong complimentary pick-up service for China patients -

A Mobile Device-Based Imaging Spectrometer for Environmental

www.nature.com/scientificreports OPEN A mobile device-based imaging spectrometer for environmental monitoring by attaching a Received: 31 August 2017 Accepted: 2 November 2017 lightweight small module to a Published: xx xx xxxx commercial digital camera Fuhong Cai1, Wen Lu2, Wuxiong Shi3 & Sailing He3 Spatially-explicit data are essential for remote sensing of ecological phenomena. Lately, recent innovations in mobile device platforms have led to an upsurge in on-site rapid detection. For instance, CMOS chips in smart phones and digital cameras serve as excellent sensors for scientifc research. In this paper, a mobile device-based imaging spectrometer module (weighing about 99 g) is developed and equipped on a Single Lens Refex camera. Utilizing this lightweight module, as well as commonly used photographic equipment, we demonstrate its utility through a series of on-site multispectral imaging, including ocean (or lake) water-color sensing and plant refectance measurement. Based on the experiments we obtain 3D spectral image cubes, which can be further analyzed for environmental monitoring. Moreover, our system can be applied to many kinds of cameras, e.g., aerial camera and underwater camera. Therefore, any camera can be upgraded to an imaging spectrometer with the help of our miniaturized module. We believe it has the potential to become a versatile tool for on-site investigation into many applications. In environmental monitoring felds, acquiring spectral and imaging information is essential to relate structure to function1–3. Imaging spectrometers are appealing instruments that provide a spectrally-resolved image of an object4,5. Tis spectrally-resolved image, also called a multispectral/hyperspectral image, is a promising tool cur- rently applied to numerous areas, including environmental monitoring6–8, disease diagnosis9, food quality con- trol10, ripeness testing11, etc. -

Status of Wintering Waterbirds on Hainan Island: Results of Annual Waterbird Surveys Between 2008−2020

FORKTAIL 36 (2020): 79–89 Status of wintering waterbirds on Hainan Island: results of annual waterbird surveys between 2008−2020 FEI LI, GANG LU, BOSCO PUI LOK CHAN, XI ZHENG, ZHI-QIN ZHOU & YAN-NI MO We conducted annual surveys on wintering waterbirds at a total of 81 wetland sites on China’s Hainan Island from 2008 to 2020. These surveys recorded 82 waterbird species. Little Egret Egretta garzetta, Lesser Sand Plover Charadrius mongolus and Kentish Plover C. alexandrinus were the most abundant species, while Little Egret, Chinese Pond Heron Ardeola bacchus and Common Sandpiper Actitis hypoleucos were the most widespread. We discovered a new and important wintering site for the endangered Black-faced Spoonbill Platalea minor in Danzhou Bay. Our data also suggest that Hainan may be a regular wintering site for a small number of Great Knot Calidris tenuirostris and Nordmann’s Greenshank Tringa guttifer. Sites of particular importance included Dongzhaigang, Houshui Bay, Danzhou Bay, Beili Bay, Changhuajiang River Estuary and Yinggehai Saltpans, but not all of them are formally protected at present. Our longitudinal data suggest an increasing trend in the total number of waterbirds counted, but this most likely reflects increased survey effort over the years, improving field skills of surveyors and a growing knowledge of important waterbird sites. The average annual count of waterbirds recorded during our 13-year survey period was relatively low compared with some nearby wetlands of importance on the mainland. Our surveys also detected continuous declines of waterbirds at some sites. To safeguard the future of Hainan’s waterbirds and their habitats, we recommend establishing new or expanding existing protected areas at key sites, and enhancing management and enforcement efforts throughout the island. -

Powerlong Real Estate Holdings Limited 寶龍地產控股有限公司 (於開曼群島註冊成立之有限責任公司) (股份代號: 1238)

香港交易及結算所有限公司以及香港聯合交易所有限公司對本公佈的內容概 不負責,對其準確性或完整性亦不發表任何聲明,並明確表示,概不會就因本 公佈全部或任何部分內容而產生或因倚賴該等內容而引致的任何損失承擔任 何責任。 本公佈不會直接或間接於或向美國(包括美國的領土及屬地、任何州以及哥倫 比亞特區)發表、發行、分派。本公佈以提供信息為目的並不構成在美國或任何 其他司法權區提呈出售任何證券的建議或招攬購買任何證券。倘未根據任何 該等司法權區的證券法例辦理登記或符合資格而於上述地區進行上述建議或 招攬或出售即屬違法。倘未經辦理有關登記或已獲適用豁免辦理有關登記規 定,證券一概不得在美國境內發售或出售。於美國境內公開發售任何證券將須 以招股章程形式作出。該份招股章程將載列關於提呈發售的公司以及其管理 層及財務報表的詳盡資料。本公司目前無意於美國境內公開發售證券。 POWERLONG REAL ESTATE HOLDINGS LIMITED 寶龍地產控股有限公司 (於開曼群島註冊成立之有限責任公司) (股份代號:1238) 海外監管公佈 本海外監管公佈乃根據香港聯合交易所有限公司(「聯交所」)證券上市規則(「上 市規則」)第 13.10B條而發表。 茲提述本公司日期為2019年 7 月 16日就發行票據而發表的兩份公佈(「該等公 佈」)。除另有界定外,本公佈所用的全部詞彙與該等公佈所界定者具有相同涵 義。 董事會欣然宣佈,購買協議項下所有先決條件已獲達成,而發行票據已於2019 年 7 月 23日完成。 請參閱隨附有關票據的發售通函(「發售通函」),發售通函已於2019年 7 月 25日同 步在新交所網站刊登。 – 1 – 在聯交所網站登載發售通函僅為促進向香港投資者平等發佈信息以及遵守上 市規則第13.10B條,概無任何其他目的。發售通函並不構成向任何司法權區的 公眾人士要約出售任何證券的招股章程、通知、通函、冊子、公佈或文件,亦非 邀請或招攬公眾人士作出收購、認購或購買任何證券的要約,且並非刻意邀請 或招攬公眾人士作出收購、認購或購買任何證券的要約。發售通函不得視為勸 誘認購或購買本公司任何證券,亦不擬作出有關勸誘。不應根據發售通函所載 資料作出任何投資決定。 承董事會命 寶龍地產控股有限公司 主席 許健康 香港,2019年 7 月 25日 於本公佈日期,執行董事為許健康先生、許華芳先生、肖清平先生、施思妮女士 及張洪峰先生;非執行董事為許華芬女士;及獨立非執行董事為魏偉峰博士、 梅建平博士及丁祖昱博士。 – 2 – IMPORTANT NOTICE THIS OFFERING IS AVAILABLE ONLY TO INVESTORS WHO ARE PERSONS OUTSIDE OF THE U.S. IMPORTANT: You must read the following before continuing. The following applies to the offering circular following this page, and you are therefore advised to read this carefully before reading, accessing or making any other use of the offering circular. In accessing the offering circular, you agree to be bound by the following terms and conditions, including any modifications to them any -

C I T Y G U I

HAIKOU CITY GUIDE INTRODUCTION Haikou is the capital and most populous city of the Chinese province of Hainan. It is situated on the northern coast of Hainan, by the mouth of the Nandu River. The northern part of the city is the district of Haidian Island, which is separated from the main part of Haikou by the Haidian River, a branch of the Nandu. Administratively, Haikou is a prefecture-level city, comprising four districts, and covering 2,280 square kilometres (880 sq mi). There are 2,046,189 inhabitants in the built up area all living within the 4 urban districts of the city. Haikou’s population as of 2018 is just over 12.8 million. The average temperature in the summer is usually around 26° in July. Winter is warm with an average of 18°. The total GDP of Haikou was over 71.3 billion Yuan in 2018. 12.8 million 26°C 18°C GDP 71.3 billion yuan (2017) 1 CONTENTS Culture History & Natural Cuisine Maps Popular Attractions Transport Housing Schools Doctors Shopping Nightlife Emergency Contacts 2 CULTURE Haikou was originally a port city, serving as the port for Qiongshan. Haikou was developed as a port during the Sino-Japanese War following Japanese occupation; after the war, Haikou and Hainan remained under Nationalist control until Landing Operation on Hainan Island, when it fell to Communist rule. Today, more than half of the island's total trade still goes through its ports. The city is home to Hainan University, which has its main campus on Haidian Island. The Temple of the Five Lords is located to the southeast of the city. -

Guorui Properties Limited 國瑞置業有限公司

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. GUORUI PROPERTIES LIMITED 國瑞置業有限公司 (Incorporated in the Cayman Islands with limited liability under the name of “Glory Land Company Limited (國瑞置業有限公司)” and carrying on business in Hong Kong as “Guorui Properties Limited”) (Stock Code: 2329) INTERIM RESULTS ANNOUNCEMENT FOR THE SIX MONTHS ENDED JUNE 30, 2020 FINANCIAL HIGHLIGHTS – Achieved contracted sales for the six months ended June 30, 2020 (the “Reporting Period”) was RMB7,478.8 million with corresponding gross floor area (“GFA”) of approximately 375,746 sq.m.; – Revenue for the Reporting Period was RMB3,322.4 million, of which the revenue from property development was RMB2,915.4 million; – Gross profit for the Reporting Period was RMB871.4 million, of which the gross profit from property development was RMB605.0 million; – Net profit for the Reporting Period was RMB281.0 million; – Basic earnings per share for the Reporting Period were RMB1.6 cents; – Land reserves reached a total GFA of 15,028,090 sq.m. and the average cost of land reserves was RMB2,890.0 per sq.m. as at June 30, 2020; – Contracted average selling price (“ASP”) for the Reporting Period was RMB19,904.0 per sq.m. The average cost of land reserves accounted for 14.5% of the ASP for the Reporting Period. -

Consultancy Study on Social, Economic and Political Developments in Pan-Pearl River Delta Region

CONSULTANCY STUDY ON SOCIAL, ECONOMIC AND POLITICAL DEVELOPMENTS IN PAN-PEARL RIVER DELTA REGION FIFTH MONTHLY REPORT COVERING FUJIAN, JIANGXI, HUNAN AND HAINAN SEPTEMBER 2006 Table of Contents I. Executive Summary i II. Topical Analysis 1 Logistics Development in the Pan-PRD: Opportunities and Challenges for Hong Kong 1 y An Overview of and Trends in Tourism Development in the Pan-Pearl River Delta Region 2 y Fujian Masterminds an Overall Layout of “Five Zones and Two Belts” for Tourism Development 9 y Jiangxi Actively Adopts “Red Tourism” Strategy 16 y Hunan Focuses on Developing Two Key Central Tourism Destination Cities 21 y Hainan Develops Overseas Source Markets Through a Multi-Channel and Multi-Means Approach 28 y Roles, Opportunities and Challenges for Hong Kong in the Future 36 III. Trends and Updates on the Four-Eastern Provinces 40 y Fujian to Develop into a Strong Province of Marine Economy 41 y Fuzhou Develops Harbour-Based Industry 44 y Jiangxi Promotes Urbanisation Construction 47 y Nanchang Strengthens the Convention and Exhibition Economy 49 y Consumption of Hunan Residents Grows Rapidly 52 y State-Owned Enterprise of Hunan Finishes 60% of the Reform 55 y Hainan Actively Develops the Development Zones 57 y Haikou Regulates Government Invested Projects 59 y Memorabilia of Pan-PRD Regional Cooperation 62 IV. Data and Trends 66 y Fujian 67 y Jiangxi 68 y Hunan 69 y Hainan 70 y Major Economic Indicators of Nine Pan-PRD Provinces/Region (Jan-Jun 2006) 71 y Nine Pan-PRD Provinces/Region: 10-year Economic Trend (1996-2005) 72 y Nine Pan-PRD Provinces/Region: Statistics at a Glance (2005) 73 V.