2019 Interim Results Guorui Properties Limited (2329.HK) August 2019

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Effective Inhibition of Mrna Accumulation and Protein Expression of H5N1 Avian Influenza Virus NS1 Gene in Vitro by Small Interfering Rnas

Folia Microbiol (2013) 58:335–342 DOI 10.1007/s12223-012-0212-8 Effective inhibition of mRNA accumulation and protein expression of H5N1 avian influenza virus NS1 gene in vitro by small interfering RNAs Hanwei Jiao & Li Du & Yongchang Hao & Ying Cheng & Jing Luo & Wenhua Kuang & Donglin Zhang & Ming Lei & Xiaoxiao Jia & Xiaoru Zhang & Chao Qi & Hongxuan He & Fengyang Wang Received: 18 June 2012 /Accepted: 7 November 2012 /Published online: 29 November 2012 # Institute of Microbiology, Academy of Sciences of the Czech Republic, v.v.i. 2012 Abstract Avian influenza has emerged as a devastating protein expressing HEK293 cell lines were established, four disease and may cross species barrier and adapt to a new small interfering RNAs (siRNAs) targeting NS1 gene were host, causing enormous economic loss and great public designed, synthesized, and used to transfect the stable cell health threats, and non-structural protein 1 (NS1) is a mul- lines. Flow cytometry, real-time quantitative polymerase tifunctional non-structural protein of avian influenza virus chain reaction, and Western blot were performed to assess (AIV) that counters cellular antiviral activities and is a the expression level of NS1. The results suggested that virulence factor. RNA interference (RNAi) provides a pow- sequence-dependent specific siRNAs effectively inhibited erful promising approach to inhibit viral infection specifi- mRNA accumulation and protein expression of AIV NS1 cally. To explore the possibility of using RNAi as a strategy in vitro. These findings provide useful information for the against AIV infection, after the fusion protein expression development of RNAi-based prophylaxis and therapy for plasmids pNS1-enhanced green fluorescent protein (EGFP), AIV infection. -

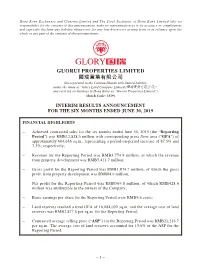

Guorui Properties Limited 國瑞置業有限公司

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. GUORUI PROPERTIES LIMITED 國瑞置業有限公司 (Incorporated in the Cayman Islands with limited liability under the name of “Glory Land Company Limited (國瑞置業有限公司)” and carrying on business in Hong Kong as “Guorui Properties Limited”) (Stock Code: 2329) INTERIM RESULTS ANNOUNCEMENT FOR THE SIX MONTHS ENDED JUNE 30, 2019 FINANCIAL HIGHLIGHTS – Achieved contracted sales for the six months ended June 30, 2019 (the “Reporting Period”) was RMB12,828.3 million with corresponding gross floor area (“GFA”) of approximately 604,636 sq.m., representing a period-on-period increase of 87.5% and 7.3%, respectively; – Revenue for the Reporting Period was RMB3,774.9 million, of which the revenue from property development was RMB3,411.7 million; – Gross profit for the Reporting Period was RMB1,074.7 million, of which the gross profit from property development was RM804.6 million; – Net profit for the Reporting Period was RMB569.8 million, of which RMB428.6 million was attributable to the owners of the Company; – Basic earnings per share for the Reporting Period were RMB9.6 cents; – Land reserves reached a total GFA of 16,084,092 sq.m. and the average cost of land reserves was RMB2,877.8 per sq.m. for the Reporting Period; – Contracted average selling price (“ASP”) for the Reporting Period was RMB21,216.7 per sq.m. -

Haikou Is a Tropical Coastal City, Situated on the Northern Coast of Hainan, by the Mouth of the Nandu River

Haikou is a tropical coastal city, situated on the northern coast of Hainan, by the mouth of the Nandu River. The northern part of the city is Haidian Island, which is separated from the main part of Haikou by the Haidian River, a branch of the Nandu. Haikou was originally a port city. Today, it’s the capital of Hainan province and the most populous city in the province. The city covers 2,280 square kilometers and is home to around 2 million inhabitants. Haikou is on the northern edge of the torrid zone, and is part of the inter-tropical Convergence Zone. April to October is the active period for tropical storms and typhoons, most of which occur between August and September. May to October is the rainy season with the heaviest rainfall occurring in September. Despite its location, the city has a humid subtropical climate, falling just short of a tropical climate, with strong monsoonal influences. Nevertheless, the area has hot summers and warm winters, usually with high humidity. Extremes temperatures have ranged from 2.8 to 39.6 °C (37 to 103 °F) From June to October torrential rains may occur, with 7.0 days annually receiving at least 50 mm (1.97 in) of rain; this period accounts for nearly 70 percent of the annual rainfall of 1,650 mm (65 in). With monthly percentage of possible sunshine ranging from 31% in February to 61% in July, the city receives 2,070 hours of bright sunshine annually. Haikou is a transport hub with flights to many cities and boats to nearby mainland cities such as Beihai and Zhanjiang. -

Spatiotemporal Patterns of Carbon Emissions and Taxi Travel Using GPS Data in Beijing

energies Article Spatiotemporal Patterns of Carbon Emissions and Taxi Travel Using GPS Data in Beijing Jinlei Zhang 1, Feng Chen 1,2, Zijia Wang 1,* ID , Rui Wang 1 and Shunwei Shi 1 1 School of Civil and Architectural Engineering, Beijing Jiaotong University, No.3 Shangyuancun, Haidian District, Beijing 100044, China; [email protected] (J.Z.); [email protected] (F.C.); [email protected] (R.W.); [email protected] (S.S.) 2 Beijing Engineering and Technology Research Center of Rail Transit Line Safety and Disaster Prevention, No.3 Shangyuancun, Haidian District, Beijing 100044, China * Correspondence: [email protected]; Tel.: +86-010-5168-8070 Received: 21 December 2017; Accepted: 19 February 2018; Published: 27 February 2018 Abstract: Taxis are significant contributors to carbon dioxide emissions due to their frequent usage, yet current research into taxi carbon emissions is insufficient. Emerging data sources and big data–mining techniques enable analysis of carbon emissions, which contributes to their reduction and the promotion of low-carbon societies. This study uses taxi GPS data to reconstruct taxi trajectories in Beijing. We then use the carbon emission calculation model based on a taxi fuel consumption algorithm and the carbon dioxide emission factor to calculate emissions and apply a visualization method called kernel density analysis to obtain the dynamic spatiotemporal distribution of carbon emissions. Total carbon emissions show substantial temporal variations during the day, with maximum values from 10:00–11:00 (57.53 t), which is seven times the minimum value of 7.43 t (from 03:00–04:00). Carbon emissions per kilometer at the network level are steady throughout the day (0.2 kg/km). -

Glorious Property Holdings Limited 囱 盛 地 產 控 股 有 限

非供於美國公佈 香港交易及結算所有限公司及香港聯合交易所有限公司對本公告的內容概不負責,對其準確性或 完整性亦不發表任何聲明,並明確表示,概不就因本公告全部或任何部份內容而產生或因依賴該 等內容而引致的任何損失承擔任何責任。 本公告並不構成在美國提呈證券出售的要約。在並無登記或不獲豁免登記下,證券不一定可在美 國提呈發售或出售。在美國進行的任何公開發售證券,將以可向本公司索取的發售章程進行,發 售通函將載有本公司及管理層的詳細資料以及財務報表。本公司不擬在美國註冊任何部分的票據。 Glorious Property Holdings Limited 囱盛地產控股有限公司 (於開曼群島註冊成立的有限公司) (股份代號:845) 建議的優先票據發行 本公司擬進行建議的票據發行。有關這次建議的票據發行,本公司將向若干機 構投資者提供有關本集團的最新企業及財務信息,包括已更新風險因素、本公 司業務的及本集團承辦項目的概況、管理層就財務狀況及經營業績的討論與分 析、近期發展、關聯方交易及債務資料,該等資料之前尚未公開過。該等最新 信息摘要隨附於本公告並在向機構投資者發放的相若時間,可於本公司網址 www.gloriousphl.com.cn瀏覽。 – 1 – 建議的票據發行的完成須受市況及投資者反應規限。建議的票據的定價,包括 總本金金額、發售價及息率將由唯一賬簿管理人及唯一牽頭經辦人渣打銀行透 過使用入標定價的方式釐定。在落實最終票據條款後,渣打銀行及本公司等將 訂立購買協議。倘票據予以發行,本公司現擬使用票據收益對新增及現有項目 提供資金(包括建造費用及土地成本)及供作一般公司用途。本公司或會因應變 動中的市況及情況調整上述計劃,並因此可能重新分配建議的票據發行的收益。 本公司已申請票據於新加坡交易所上市。票據是否獲納入新加坡交易所並不視 為本公司或票據價值之指標。本公司將不會尋求票據於香港上市。 由於於本公告日期尚未就建議的票據發行訂立具約束力的協議,故建議的票據 發行不一定會落實。投資者及本公司股東於買賣本公司證券時,務須審慎行事。 倘購買協議獲予訂立,本公司將就建議的票據發行作進一步公告。 建議的票據發行 緒言 本公司擬進行建議的票據發行。有關這次建議的票據發行,本公司將向若干機構 投資者提供有關本集團的最新企業及財務信息,包括已更新風險因素、本公司業 務及本集團承辦項目的概況、管理層就財務狀況及經營業績的討論與分析、近期 發展、關聯方交易及債務資料,該等資料之前尚未公開過。該等最新信息摘要隨 附於本公告並在向機構投資者發放的相若時間,可於本公司網址 www.gloriousphl.com.cn瀏覽。 – 2 – 建議的票據發行的完成須受市況及投資者反應規限。建議的票據的定價,包括總 本金金額、發售價及息率將由唯一賬簿管理人及唯一牽頭經辦人渣打銀行透過使 用入標定價的方式釐定。除非根據票據的條款予以提前贖回,票據(倘獲發行)將 具有一次性還款。於本公告日期,尚未釐定建議的票據發行的款額、條款及條件。 在落實最終票據條款後,渣打銀行及本公司等將訂立購買協議,據此,渣打銀行 將為票據的初步買方。倘購買協議獲予簽署,本公司將就建議的票據發行作進一 步公告。 建議的票據發行將僅供渣打銀行以要約形式於美國境外遵照證券法項下的S規例 發售。概無票據將於香港公開發售,及概無票據將配售予本公司的任何關連人士。 進行建議的票據發行的原因 本集團是專注在中國主要經濟城市發展及銷售優質物業的最大的房地產發展商之 一。於二零一零年六月三十日,本集團在全中國11個主要城市,包括3個直轄市 (上海、天津及北京)、5個省會城市(合肥、瀋陽、哈爾濱、南京及長春)及3個位 於長三角主要區域的經濟城市(無錫、蘇州及南通)有多個項目處於已開發或正在 -

Info Bulletin.Pmd

The East Asian Seas Congress 2006 The year 2003 created new opportunities for the sustainable development of the seas of East Asia, as it heralded the birth of the first-ever East Asian Seas Congress. The five-day event, held from 8-12 December in Putrajaya, Malaysia, brought together various stakeholders from diverse disciplines to work hand-in-hand to uphold the welfare of the East Asian Seas and ensure the sustainability of their resources. It will be remembered as the occasion where the Sustainable Development Strategy for the Seas of East Asia (SDS-SEA) was endorsed by environment- and ocean- related ministers and senior officials from PEMSEA’s 12 participating countries, with the signing of the Putrajaya Declaration. This Congress, a follow-up to the Putrajaya event, promises to drive the wheels of sustainable development in continuous motion, thereby bringing East Asia closer and closer to ultimately achieving a healthy and bountiful future for its seas and its people. Designed to address pressing coastal and marine environmental issues in practical formats and against a multidisciplinary setting, the various Congress components provide participants the opportunity to take active roles in sustainable development. Features The EAS Congress 2006 features the: • Ministerial Forum on the Implementation of the SDS-SEA* 14–15 December; • International Conference on Coastal and Ocean Governance: One Ocean, One People, One Vision 12–14 December; • Meeting of the EAS Partnership Council* 16 December; and • Youth Forum, Exhibits, Poster Sessions, Field Trip and other Side Events. *By invitation only. Host/Local Organizing Committee The 2006 Congress is being hosted by the government of PR China and co-organized by the State Oceanic Administration (SOA). -

Underground Space As a Connector

ARCHITECTURE DEPARTMENT CHINESE UNIVERSITY OF HONG KONG MASTER OF ARCHITECTURE PROGRAMME 2010-2011 DESIGN REPORT NEW MOBILITY HUB IN BEIJING UNDERGROUND SPACE AS A CONNECTOR SHEKWai Ling, Sophy May 2011 \ r 00 Thesis Statement 01 Background Study 02 Site Analysis 03 Underground Space 04 Design Strategy & Development i Thesis Statement The fast urbanization and urban sprawl in Beijing causes problematic conditions in many areas of city. The south-east area is a representative case for this development. To cope with the problem of increased traffic congestion and emission in Beijing, the government has planned to expand the subway system to cover most parts of the city and aiming at a 1km node-to-node walking distance within the 3rd ring road area by 2020, in order to encourage citizens to use public transport rather than automobiles and develop a more sustainable life- style. In addition to the subway system, the government has planned underground networks as an alternative way to ease ground traffic congestion and land use tensions in downtown areas. Along with the Beijing Government's emphasis on the subway system and underground space development, a new subway station will be built in Nanmofang in the east part of the capital bringing new opportunities to this area, south of the extending CBD. This thesis attempts to connect an increasingly fragmented urban fabric through the introduction of an underground space network. The underground space network provides a large flexibility to link different destinations directly by the all weather pedestrian connections and helps to reconnect Beijing's urban blocks divided by the large street grid for vehicular traffic. -

14 Guangzhou R&F Properties Co., Ltd

14 GUANGZHOU R&F PROPERTIES CO., LTD. Annual Report 2005 precise Market Positioning, satisfying customers’ needs GUANGZHOU R&F PROPERTIES CO., LTD. Annual Report 2005 15 R&F Property廣州 物業一覽 in China Heilongjiang Jilin Beijing Liaoning Xinjiang Neimenggu Hebai Tianjin Ningxia Shanxi Shandong Qinghai Gansu Xian Jiangsu Henan Shaanxi Tibet Anhui Hubei Sichuan Chongqing Zhejiang Shanghai Hunan Jiangxi Guizhou Fujian Guangzhou Yunnan Taiwan Guangxi Guangdong Hong Kong Macau Hainan No. of Project Land Bank Location under development Total GFA as at 14 March 2006 (sq. m.) (sq. m.) Guangzhou 11 1,143,000 4,128,000 Beijing 4 870,000 3,080,000 Tianjin 1 318,000 926,000 Xian 1 140,000 980,000 Chongqing 0 0 230,000 16 GUANGZHOU R&F PROPERTIES CO., LTD. Annual Report 2005 Business Review Overview of the PRC Property Market In 2005, China’s economy continued its rapid growth. The gross domestic product (“GDP”) in the People’s Republic of China (the “PRC”or “China”) reached RMB18,232.1 billion, which was a 9.9% surge over the previous year, while per capita disposable income of urban residents in cities and towns recorded a growth of 9.6%. The continuing growth in China’s economy and the rise in the disposable income of its citizens will inevitably lead to a higher demand for quality housing. During the year under review, the Chinese Govern- ment implemented a series of macro economic mea- sures to counter act the overheated property market. These macro economic measures have helped stabi- lized market conditions and in the long run are ex- pected to create a more balanced supply and demand situation and a healthier development of the prop- erty market. -

The Systematic Evolution of Beijing: a Human Ecology Perspective

Research Article Int J Environ Sci Nat Res Volume 23 Issue 4 - March 2020 Copyright © All rights are reserved by Lachang Lyu DOI: 10.19080/IJESNR.2020.23.556121 The Systematic Evolution of Beijing: A Human Ecology Perspective Lachang Lyu1* and Richard Greene2 1College of Resource, Environment and Tourism, Capital Normal University, China 2College of Geospatial Information Science and Technology, Capital Normal University, China Submission: Published: rd *Corresponding February author: 17, 2020; March 04, 2020 Lachang Lyu, College of Resource Environment and Tourism, Capital Normal University, No. 105 West 3 Ring Road North, Haidian District, Beijing, 10004, China Abstract Megacity sprawl is an international phenomenon and Chinese megacities have been especially exposed to rapid sprawl since reform and the opening-up policy in the year of 1978. As the political, cultural, and international communication center of China, Beijing has witnessed a morphological transition that demonstrates typical aspects of this megacity sprawl. Though the morphological changes have been investigated by a number of scholars, emerging changes and new high resolution multi temporal global urban land data allow for a more systematic investigation that results in an evolutionary model that uncovers the urban form dynamics of megacity sprawl. In this paper, we examine the Beijing morphological evolutionary process and the geographic direction of intra-urban sprawl with the use of a new global urban land database obvious periodic sequences ranging from compact to a more loosely-shaped form but also triangular in some cases and rectangular in other cases that utilized an extensive number of LANDSAT images for five-year periods from 1980-2015. -

Journal of Cleaner Production 206 (2019) 688E700

Journal of Cleaner Production 206 (2019) 688e700 Contents lists available at ScienceDirect Journal of Cleaner Production journal homepage: www.elsevier.com/locate/jclepro Emission pattern mining based on taxi trajectory data in Beijing * Tingting Li a, , Jianping Wu a, Anrong Dang b, Lyuchao Liao a, Ming Xu a a Department of Civil Engineering, Tsinghua University, Beijing, 100084, China b School of Architecture, Tsinghua University, 100084, China article info abstract Article history: Traffic-related air pollution has been one of the major environmental problems in China. It is urgent to Received 20 June 2017 explore the urban traffic emission patterns for the low-carbon urban planning and traffic management. Received in revised form With this purpose, a new urban traffic emission analysis model is proposed in this paper. The traffic 9 August 2018 analysis zones (TAZs) are treated as the analysis unit. Then the spatial and temporal dynamic emission Accepted 7 September 2018 patterns are studied based on taxi GPS data in Beijing. The whole urban area of Beijing is divided into 33 Available online 18 September 2018 TAZs depending on the feature of road networks. And the trip patterns of TAZs are extracted. The instantaneous emissions of CO , NOx, VOC and PM within and between TAZs are estimated. The re- Keywords: 2 Data mining lationships between emissions and road densities are studied. The results demonstrated that (1) the Traffic analysis zone highest taxi trips during the day occur at 10:00, 16:00 and 20:00. (2) The variations of the 4 pollutants Emission pattern within and between TAZs are similar. -

Evergrande Real Estate Group Limited 恒 大 地 產 集 團 有 限 公 司 (Incorporated in the Cayman Islands with Limited Liability) (Stock Code: 3333)

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. Evergrande Real Estate Group Limited 恒 大 地 產 集 團 有 限 公 司 (Incorporated in the Cayman Islands with limited liability) (Stock Code: 3333) DISCLOSEABLE TRANSACTION The Board announces that on 2 December 2015, Shengyu (BVI) Limited, a wholly-owned subsidiary of the Company, as the purchaser, entered into three agreements respectively with the Vendor, pursuant to which the Purchaser agreed to acquire the interests in the relevant shares in and loans to the target companies held by the Vendor. These target companies hold the interests in the Haikou Project, the Huiyang Project and two projects located in Wuhan. Since the Vendor is the seller in these three agreements, such agreements will be aggregated in accordance with Rule 14.22 of the Listing Rules. As the applicable percentage ratios for the Acquisition exceed 5% but are less than 25%, the Acquisition constitutes a discloseable transaction for the Company under Chapter 14 of the Listing Rules and is subject to the reporting and announcement requirements under Chapter 14 of the Listing Rules. 1. INTRODUCTION The Board announces that on 2 December 2015, Shengyu (BVI) Limited, a wholly-owned subsidiary of the Company, as the purchaser, entered into three agreements respectively with the Vendor, pursuant to which the Purchaser agreed to acquire the interests in the relevant shares in and loans to the target companies held by the Vendor. -

Uillage Uillage Uillage

UILLAGE UILLAGE UILLAGE RETHINKING URBAN VILLAGE IN BEIJING EXPLORING STRATEGIES FOR INFRASTRUCTURE AND PUBLIC SPACE, STRENGTHENING COMMUNITY LIFE WHAT IS URBAN VILLAGE IN CHINA? [URBAN VILLAGE] [INFRASTRUCTURE] [PUBLIC SPACE] [COMMUNITY LIFE] Master Thesis Jian Zhou Supervisors: Ana Betancour, Flavia Cozma, Jaime Montes, Master's programme in Sustainable Urban Planning and Design Kungliga Tekniska högskolan June 3rd, 2014 UILLAGE WHAT IS URBAN VILLAGE IN CHINA? ILLAGE U -Commonly seen on outskirts and the downtown of Chinese megacities -Surrounded by modern urban structure -A unique phenomenon during China’s urbanization -Inhabitants: the poor and transient, manual laborers -Space: super densified, infrastructure+space+social problems -Services for the city, -Cheap living cost for new comers UILLAGE FROM RURAL VILLAGE TO URBAN VILLAGE UILLAGE RURAL VILLAGES IN 40 YEARS AGO: URBAN VILLAGE: BROADENED INFRASTRUCTURE, FARMLAND, STREET SYSTEM, PUBLIC SPACE INVADED FRINGES, COMPRESSED PUBLIC SPACE Source for description of urban village’s formation process: Mapping of urban villages in China. Zhengdong Huang, Qingming Zhan. School of Urban Design, Wuhan University Source for description of urban village’s formation process: Mapping of urban villages in China. Zhengdong Huang, Qingming Zhan. School of Urban Design, Wuhan University ORIGINAL RESIDENTIAL HOUSING FARMLAND TRAFFIC ROADS ORIGINAL RESIDENTIAL HOUSING AFTERWARDS DENSIFIED HOUSING ROUTES: WALKING, SMALL VEHICLES MAIN PUBLIC SPACE NODES SKYSCRAPERS MODERN RESIDENTIAL BUILDING WITH 6-8