Cp-Proxy-2012.Pdf

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

THE ROYAL INSTITUTION for the ADVANCEMENT of LEARNING/Mcgill UNIVERSITY

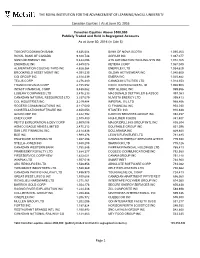

THE ROYAL INSTITUTION FOR THE ADVANCEMENT OF LEARNING/McGILL UNIVERSITY Canadian Equities │ As at June 30, 2016 Canadian Equities Above $500,000 Publicly Traded and Held in Segregated Accounts As at June 30, 2016 (in Cdn $) TORONTO DOMINION BANK 9,836,604 BANK OF NOVA SCOTIA 1,095,263 ROYAL BANK OF CANADA 9,328,748 AGRIUM INC 1,087,077 SUNCOR ENERGY INC 5,444,096 ATS AUTOMATION TOOLING SYS INC 1,072,165 ENBRIDGE INC 4,849,078 KEYERA CORP 1,067,040 ALIMENTATION COUCHE-TARD INC 4,628,364 ENERFLEX LTD 1,054,629 BROOKFIELD ASSET MGMT INC 4,391,535 GILDAN ACTIVEWEAR INC 1,040,600 CGI GROUP INC 4,310,339 EMERA INC 1,025,882 TELUS CORP 4,276,480 CANADIAN UTILITIES LTD 1,014,353 FRANCO-NEVADA CORP 4,155,552 EXCO TECHNOLOGIES LTD 1,008,903 INTACT FINANCIAL CORP 3,488,562 WSP GLOBAL INC 999,856 LOBLAW COMPANIES LTD 3,476,233 MACDONALD DETTWILER & ASSOC 997,083 CANADIAN NATURAL RESOURCES LTD 3,337,079 NUVISTA ENERGY LTD 995,413 CCL INDUSTRIES INC 3,219,484 IMPERIAL OIL LTD 968,856 ROGERS COMMUNICATIONS INC 3,117,080 CI FINANCIAL INC 954,030 CONSTELLATION SOFTWARE INC 2,650,053 STANTEC INC 910,638 GOLDCORP INC 2,622,792 CANYON SERVICES GROUP INC 892,457 ONEX CORP 2,575,400 HIGH LINER FOODS 841,407 PEYTO EXPLORATION & DEV CORP 2,509,098 MAJOR DRILLING GROUP INTL INC 838,304 AGNICO EAGLE MINES LIMITED 2,475,212 EQUITABLE GROUP INC 831,396 SUN LIFE FINANCIAL INC 2,414,836 DOLLARAMA INC 829,840 BCE INC 1,999,278 LEON'S FURNITURE LTD 781,495 ENGHOUSE SYSTEMS LTD 1,867,298 CANADIAN ENERGY SERVICES &TECH 779,690 STELLA-JONES INC 1,840,208 SHAWCOR LTD 775,126 -

Formerly Manulife Asset Management UCITS Series ICAV

Half Yearly Report Manulife Investment Management II ICAV Interim Report and Condensed Unaudited Financial Statements for the six months ended 30 September 2020 An open-ended umbrella Irish Collective Asset-Management Vehicle with segregated liability between its funds registered in Ireland on 15 April 2015 under the Irish Collective Asset-Management Vehicles Act 2015 the “ICAV Act” and authorised and regulated by the Central Bank of Ireland as an Undertaking for Collective Investment in Transferable Securities pursuant to the European Communities (Undertakings for Collective Investment in Transferable Securities Regulations 2011, as amended the “UCITS Regulations”) Manulife Investment Management II ICAV Table of contents 2 A Message to Shareholders 3 General Information 4 Manager’s Report Condensed Interim Financial Statements 11 Statement of Comprehensive Income 15 Statement of Financial Position 19 Statement of Changes in Net Assets Attributable to Holders of Redeemable Participating Shares 21 Statement of Cash Flows 24 Notes to the Condensed Interim Financial Statements 44 Schedule of Investments 112 Supplemental Information 1 A Message to Shareholders Dear shareholder, Despite heightened fears over the coronavirus (COVID-19), which sent markets tumbling just prior to the beginning of the reporting period, global financial markets delivered positive returns for the 6 months ended 30 September 2020. The governments of many nations worked to shore up their economies, equity markets began to rise, and credit spreads rebounded off their highs as liquidity concerns eased. Of course, it would be a mistake to consider this market turnaround a trustworthy signal of assured or swift economic recovery. While there has been economic growth in much of the developed world, the pace has slowed in many areas as interest rates remain low and consumer spending remains far below prepandemic levels. -

TC Energy 2021 Management Information Circular

Management information circular March 4, 2021 Notice of annual meeting of shareholders to be held May 7, 2021 24668 TC_ENGLISH Circular cover spread.pdf - p1 (March 6, 2021 00:22:29) DT Letter to shareholders ........................................... 1 Notice of 2021 annual meeting ................................ 2 About Management information circular ............................3 TC Energy Summary ....................................................................4 About the shareholder meeting ...............................6 Delivering the energy people need, every day. Safely. Delivery of meeting materials ........................................7 Responsibly. Collaboratively. With integrity. Attending and participating in the meeting .....................8 We are a vital part of everyday life — delivering the energy millions of people rely on to power their lives in a Voting ...................................................................... 10 sustainable way. Thanks to a safe, reliable network of natural gas and crude oil pipelines, along with power generation Business of the meeting .............................................. 14 and storage facilities, wherever life happens — we’re there. Guided by our core values of safety, responsibility, Governance ........................................................33 collaboration and integrity, our 7,500 people make a positive difference in the communities where we operate across About our governance practices ...................................33 Canada, the U.S. and Mexico. -

Domtar Annual Reviwe 2007

DOMTAR ANNUAL REVIEW 2 0 0 7 • VOL. 01 this is domtar Getting to know North America’s newest leader in fine papermaking being annual review number oneInterview with Raymond Royer P R E S I D E N T A N D C E O DOMTAR CORPORATION paper is part of everyday life Ask Cougar® a strategically positioned production system Domtar is proud of its papermakers. Find out where it all happens… SUSTainability: putting words into action • NEW PRODUCT DEVELOPMENT • ONE TEAM, ONE GOAL, 13,000 STRONG • AIR, WATER, FIRE AND EARTH Great ideas always command greater attention. That’s why you need Cougar®. Offering standout performance, Cougar remains the favorite for its power to amaze and impress. Cougar’s stellar brightness and balanced 98 GE white shade — in addition to its smooth, uniform print brightness surface and high opacity — deliver rich, vibrant colors and sharp images with startling results. With consistent performance, both on press and off, Cougar provides FSC uncompromising quality and excellent value. Containing certified 10% post-consumer fiber, Cougar is now FSC-certified and a premiere member of the Domtar EarthChoice® Smooth family. For guaranteed success and a performance that & Vellum commands attention, always remember to ask for Cougar. finishes Domtar is pleased to make an annual contribution of $275,000 to WWF from the sale of Cougar brand products. © 1986 Panda symbol WWF-World Wide Fund For Nature (also known as World Wildlife Fund) ® “WWF” is a WWF Registered Trademark cougar ® 2007 ANNUAL REVIEW Michel A. RATHIER Editor in Chief EDITOrial TeaM Marie CHAMBERLAND Richard DESCARRIES Bérangère PARRY Lyla RADMANOVICH CONTRIBUTORS Linda BÉLANGER Pascal BOSSÉ Guy BOUCHER Michael CROSS Michel DAGENAIS Tom HOWARD Patrice LÉGER-BOURGOUIN Jim LENHOFF 14 Rick MULLEN Chantal NEPVEU governing for success Domtar is Mélanie PAILLÉ committed to the highest standards of ethical behavior Gilles PHARAND and business conduct. -

DOMTAR CORPORATION (Exact Name of Registrant As Specified in Its Charter)

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 10-Q T QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended September 30, 2015 OR ¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from ________to_______ COMMISSION FILE NUMBER 001-33164 DOMTAR CORPORATION (Exact name of registrant as specified in its charter) DELAWARE 20-5901152 (I.R.S. Employer (State of Incorporation) Identification No.) 234 Kingsley Park Drive, Fort Mill, SC 29715 (Address of principal executive offices) (zip code) (803) 802-7500 (Registrant’s telephone number) Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. YES x NO ¨ Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation ST (232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). YES x NO ¨ Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. -

Climate Change 2020

Emera Inc. - Climate Change 2020 C0. Introduction C0.1 (C0.1) Give a general description and introduction to your organization. Emera Inc. is a geographically diverse energy and services company headquartered in Halifax, Nova Scotia, Canada with approximately $32 billion in assets and 2019 revenues of $6.1 billion. From our origins as a single electric utility in Nova Scotia, Emera has grown into an energy leader serving 2.5 million customers in Canada, the US, and the Caribbean. Emera’s strategy has been focused on safely delivering cleaner, affordable and reliable energy to customers for more than 15 years. Our company has investments throughout North America, and in four Caribbean countries. A description of the Emera affiliates that report to CDP is as follows: Tampa Electric (TEC) is a vertically integrated regulated electric utility servicing 780,000 customers in West Central Florida. Peoples Gas (PGS) is a natural gas utility serving 406,000 customers in Florida. New Mexico Gas Company (NMGC) is a natural gas utility serving 534,000 customers in New Mexico. Nova Scotia Power Inc. (NSPI) is a vertically integrated electric utility serving 523,000 customers in Nova Scotia. Emera Caribbean includes vertically integrated electric utilities serving 184,000 customers on the islands of Barbados, Grand Bahama, St. Lucia and Dominica. Emera Maine is a transmission and distribution electric utility serving 159,000 customers in northern and eastern Maine. The sale of Emera Maine to ENMAX Corporation closed in March 2020. Emera New Brunswick owns and operates the Brunswick Pipeline, a 145 km pipeline natural gas pipeline in New Brunswick and Emera Newfoundland and Labrador owns and operates the Maritime Link and manages investments in associated projects. -

PPSA Quarterly Review Page 2 of 44

PPSA First Quarter, 2012 Volume 1, Issue 18 Quarterly Review Pulp and Paper Safety Association (850) 584-3639 Website www.ppsa.org : Special Interest Articles: • Chairman’s Letter Safety o 2011 Safety Awards o Safety Recalls and Alerts Legal Corner Ergonomics • About Us Individual Highlights: 2012 Conference 3 Safety Awards 4 Legal Corner 10 Safety 15 Ergonomics 32 Our Sponsors 34 About our Organization 44 PPSA Quarterly Review Page 2 of 44 A Letter from Our Chairman The Board is very excited about the development of the 69th Annual Professional Development Conference. The program revolves around how people make the difference to our organizations. Attendees can look forward to some outstanding speakers, presentations, and of course the always valuable networking. Another exciting development that I will report on at the upcoming conference is the potential hire of a full-time Executive Director. The Executive Committee is meeting at the end of this month to further explore job requirements and costs associated with such a hiring. The existing board of volunteers (in particular John Sunderland) has done a very good job of getting the organization on the right track financially and operationally. However, in order to stay on track we may need to hire a full-time Executive Director. Stay tuned. Our relationship with TAPPI continues to bear fruit. We are currently partnering on safety leadership and contractor safety training. See the article on TAPPI-Safe in this edition. I also want to mention that I have reviewed the list of this year’s safety award winners. Every year I am impressed by how many of you post incredibly industry leading safety records. -

INFORMATION (C-07.Pdf)

CAPABILITIES BOILER CIRCULATION STUDIES Boiler Circulation (Chemical Recovery, Biomass, and RDF/MSW Boilers) Circulation of water through boiler tubes is necessary to prevent tube overheating and potential failure. The need to conduct a circulation study on a boiler is typically dictated because of any one, or combination of, the following reasons: • To establish the maximum steaming rate at which circulation remains adequate. • To determine pressure part modifications needed to support a significant increase in fuel burning rate. • To evaluate the effect of changing boiler operating conditions (such as type of fuel or operating pressure) on circulation. • To evaluate the effect of changing heating surfaces on circulation. • To uncover factors causing repeat pressure part failures and/or tube overheating. • To investigate the cause of excessive scale depositions inside tubing. A valuable technique used by JANSEN during its analyses of circulation conditions is the application of Ultrasonic Flow Monitoring (UFM). Selected References (see next page) C-07 2/17 Selected References Boiler Circulation Studies Alabama River Cellulose - Perdue Hill, AL KapStone Paper - Roanoke Rapids, NC Alberta-Pacific Forest Industries, Inc. - Boyle, AB Kimberly-Clark Corporation - Coosa Pines, AL APRIL Group - Rizhao, China (2 units) Kimberly-Clark Forest Products Inc. - Terrace Bay, ON AssiDomän Sepap - Stetí, Czech Republic Kimberly-Clark Nova Scotia Inc. - New Glasgow, NS Australian Paper - Morwell, Australia MacMillan Bloedel Limited - Port Alberni, BC AV Nackawic - Nackawic, NB Mead Corporation - Chillicothe, OH Bahia Specialty Cellulose S.A. - Camaçari, BA, Brazil Mead Corporation - Escanaba, MI (2 units) Blue Ridge Paper Company - Canton, NC Mead Corporation - Kingsport, TN Boise Cascade Corp. - DeRidder, LA MeadWestvaco - Phenix City, AL (2 units) Boise Cascade Corp. -

2020 Management Information Circular

2020 Management information circular Manulife Financial Corporation Annual Meeting May 7, 2020 Notice of annual meeting of shareholders Your participation is important. Please read this document and vote. Notice of annual meeting of common shareholders You’re invited to attend our 2020 annual meeting of common shareholders When Four items of business May 7, 2020 • Receiving the consolidated financial statements and 11 a.m. (Eastern time) auditors’ reports for the year ended December 31, 2019 • Electing directors Where • Appointing the auditors Manulife Head Office • Having a say on executive pay 200 Bloor Street East We’ll consider any other matters that are properly Toronto, Canada brought before the meeting, but we are not aware of any at this time. The annual meeting for The Manufacturers Life Insurance Company will be held at the same time and place. We are actively monitoring the coronavirus (COVID-19) situation and are sensitive to the public health and travel concerns our shareholders may have as well as the protocols public health authorities may recommend. We remind shareholders that a live webcast of the meeting will be available at manulife.com and this year, more than ever, we encourage you to vote your shares prior to the meeting. Please read the voting section starting on page 10 for information on how to vote. In the event it is not possible or advisable to hold our annual meeting in person, we will announce alternative arrangements for the meeting via press release as promptly as practicable, which may include holding the meeting solely by means of remote communication. -

Bank of America Global Agriculture & Materials Conference

March 4, 2021 Bank of America Global Agriculture & Materials Conference All financial information is in U.S. dollars, and all earnings per share results are diluted, unless otherwise noted Safe Harbor Forward-Looking Statements All statements in this presentation about our expectations and future performance, including the statements related to our “Strategic Initiatives,” are “forward-looking statements.” Actual results may differ materially from those suggested by these statements for a number of reasons, including the COVID-19 pandemic and the resulting decrease in paper sales and the challenges we face in maintaining manufacturing operations, changes in customer demand and pricing, changes in manufacturing costs, future acquisitions and divestitures, including facility closings, the failure to achieve our cost containment goals, costs of conversion in excess of our expectations, demand for linerboard, and the other reasons identified under “Risk Factors” in our Form 10-K for 2020 as filed with the SEC and as updated by subsequently filed Form 10-Qs. Except to the extent required by law, we expressly disclaim any obligation to update or revise these forward- looking statements to reflect new events or circumstances or otherwise. Risk Factors For a summary of the risk factors, please refer to Domtar’s Annual Report on Form 10-K for the year ended December 31, 2020 filed with the Securities and Exchange Commission and as updated by subsequently filed Form 10-Q’s. Non-GAAP Financial Measures This presentation refers to non-GAAP financial information. For a reconciliation to GAAP financial measures, please refer to the investors section of the company’s website at http://www.domtar.com (Refer to Earnings in the Investor Relations section of the website). -

RBC Principal Protected Guaranteed Return Enhanced Yield LEOS® Series 247

EQUITY LINKED NOTE | RBC GLOBAL INVESTMENT SOLUTIONS RBC Principal Protected Guaranteed Return Enhanced Yield LEOS® Series 247 7 year Term 100% Principal 0.40% - 6.00% Protection at Maturity Coupon in Years 1-7 This Note is a 7 year investment designed to provide annual income based on exposure to an equally Offering Closes weighted Canadian Equity Portfolio. Investors will receive a minimum coupon of 0.40%, to a maximum of 6.00% in years 1-7 based on the price performance of a portfolio of 10 Canadian companies. The May 21, 2021 principal amount is guaranteed by RBC at maturity. The maturity date is May 30, 2028. FundSERV INVESTMENT HIGHLIGHTS RBC4247 Income Potential: Minimum Coupon of 0.40%, to a maximum of 6.00% in Years 1-7, based on the price performance of the Shares in the Equity Portfolio where performance per Share is measured from inception to each annual coupon valuation date, subject to a maximum of 6.00% and a minimum of Issue Date -10%. Notes do not represent an interest in the securities of the companies that comprise the Equity Portfolio, and holders will have no right or entitlement to such securities including the dividends and May 26, 2021 other distributions paid on these securities. The indicative dividend yield on the Equity Portfolio as of April 30, 2021 was 4.96%, representing an aggregate dividend yield of approximately 40.34% annually compounded over the seven year term, on the assumption that the dividend yield remains constant. Principal Protection: Royal Bank of Canada guarantees the principal amount at maturity. -

Bank of Montreal Protected Deposit Notes Advantage Minimum Y.I.E.L.D

Bank of Montreal Protected Deposit Notes Advantage Minimum Y.I.E.L.D. Class TM, Series 1 > Key Features • 5 year term to maturity • Minimum annual interest payment of 0.70% • Annual interest payment ranging from 0.70% to 7.0% based on the price performance of a portfolio of ten (10) Canadian issuers* • 100% principal guaranteed by BMO as issuer if held to maturity *The amount of annual interest paid is unlikely to mirror the price performance of the securities in the Benchmark Portfolio since the return cannot exceed 7.0% of the Deposit Amount and could be zero provided no extraordinary event has occurred under the terms of the Information Statement. > Hypothetical Return Examples On an Interest Payment Date a Holder will be entitled to receive Interest on a Deposit Note equal to: (i) the maximum amount of Interest of 7.0% of the Deposit Amount, if the Closing Price of each Security has increased from the Closing Date to the applicable Valuation Date; (ii) 0.70% of the Deposit Amount, if the simple average of the effective returns is zero or negative; or (iii) a percentage of the Deposit Amount greater than 0.70% and less than 7.0%, if the simple average of the effective returns is greater than 0% and less than 6.3%. The following examples are included for illustration purposes only. The values of the Deposit Notes used to illustrate two different scenarios are hypothetical and are not estimates or forecasts of expected returns from the Closing Date to and including the Final Valuation Date.