Page 1 of 33 26 June 2008

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Erasmus Student W0RK Placement

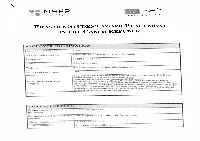

ERAsMus STuDENT W0RK PLAcEMENT IN THE CzEcH REPuBuc EMPLOYER INFORMATION Name of organization Pixmania s.r Address mcl. post cede Trnt 391/5. 60200 Brne, Czech Repuhiic Felephone 00420 543 123 100 mail [email protected] Wehsite \n uaa e; johs pixmania.corn Number cI emplevees 180 Dixons Reta plc s one of ELropes Ieadng electrLcal retaers, The Group trades through L200 stores and online stores, spanning 28 countnes and empIoyng 3650O people. Shert descrption of the Pixmania.com, as a part of Dixons Retail pc., is an European E-taer of company consurner e1ectronc goods. It app{ies innovative market strateges on an nterrational evei, leading te a pan-European presence n 26 countnes and 17 anguages. In order te support ts development in the flagshp markets and increase ts brard-awareness Pixrnanìa would ike to give an opportunty to studentsin vanousf!elds te join our tearn! Other CONTACT DETAILS (rntact persen for this ‘v arernka Modra placei ienl Departmer t and de’enata e i HR Support it Pi\mania [IR D partme ìt h ‘7 Diret tcleohene nun bLr (Ni42( 51 i i 593 E a Idrc \ ned’a i5 pi\ViI e om I)epartrnent I Funetion Transport aceount coordinator Description of activities The Transport Team Is responsible for ensure the quality of tra nsport services ordered by customers. The interna wN be responsibe for foflowing transport issues • Pick Ups (parcels on the way back to Pixmania frorn custorner) • !nvestigations hnquiry of darnaged, Iost parcels or delayed parceR) o Vahdation of Pick Ups with different carriers. -

The World's Most Active Consumer Electronics Professionals on Social

Europe's Most Active Consumer Electronics Professionals on Social - May 2021 Industry at a glance: Why should you care? So, where does your company rank? Position Company Name LinkedIn URL Location Employees on LinkedIn No. Employees Shared (Last 30 Days) % Shared (Last 30 Days) 1 EPOS https://www.linkedin.com/company/eposaudio/Denmark 438) 121) 27.63% 2 VanMoof https://www.linkedin.com/company/vanmoof/Netherlands 346) 80) 23.12% 3 ATAG Benelux https://www.linkedin.com/company/atagbenelux/Netherlands 269) 59) 21.93% 4 Eurofred https://www.linkedin.com/company/eurofred-group/Spain 206) 43) 20.87% 5 Zound Industries https://www.linkedin.com/company/zoundindustries/Sweden 245) 49) 20.00% 6 Cellularline https://www.linkedin.com/company/cellularline-group/Italy 227) 44) 19.38% 7 Jabra https://www.linkedin.com/company/jabra/Denmark 1,898) 351) 18.49% 8 Swappie https://www.linkedin.com/company/swappie/Finland 331) 57) 17.22% 9 Trust International https://www.linkedin.com/company/trustofficial/Netherlands 261) 41) 15.71% 10 LDLC https://www.linkedin.com/company/ldlc/France 393) 58) 14.76% 11 Devialet https://www.linkedin.com/company/devialet/France 326) 46) 14.11% 12 Netatmo https://www.linkedin.com/company/netatmo/France 251) 35) 13.94% 13 Skousen https://www.linkedin.com/company/skousen/Denmark 235) 30) 12.77% 14 WhiteAway https://www.linkedin.com/company/whiteaway-group/Denmark 252) 31) 12.30% 15 - COYOTE - https://www.linkedin.com/company/coyotesystem/France 340) 38) 11.18% 16 Bang & Olufsen https://www.linkedin.com/company/bangolufsen/Denmark -

European Technology Media & Telecommunications Monitor

European Technology Media & Telecommunications Monitor Market and Industry Update H1 2013 Piper Jaffray European TMT Team: Eric Sanschagrin Managing Director Head of European TMT [email protected] +44 (0) 207 796 8420 Jessica Harneyford Associate [email protected] +44 (0) 207 796 8416 Peter Shin Analyst [email protected] +44 (0) 207 796 8444 Julie Wright Executive Assistant [email protected] +44 (0) 207 796 8427 TECHNOLOGY, MEDIA & TELECOMMUNICATIONS MONITOR Market and Industry Update Selected Piper Jaffray H1 2013 TMT Transactions TMT Investment Banking Transactions Date: June 2013 $47,500,000 Client: IPtronics A/S Transaction: Mellanox Technologies, Ltd. signed a definitive agreement to acquire IPtronics A/S from Creandum AB, Sunstone Capital A/S and others for $47.5 million in cash. Pursuant to the Has Been Acquired By transaction, IPtronics’ current location in Roskilde, Denmark will serve as Mellanox’s first research and development centre in Europe and IPtronics A/S will operate as a wholly-owned indirect subsidiary of Mellanox Technologies, Ltd. Client Description: Mellanox Technologies Ltd. is a leading supplier of end-to-end InfiniBand and June 2013 Ethernet interconnect solutions and services for servers and storage. PJC Role: Piper Jaffray acted as exclusive financial advisor to IPtronics A/S. Date: May 2013 $46,000,000 Client: inContact, Inc. (NasdaqCM: SAAS) Transaction: inContact closed a $46.0 million follow-on offering of 6,396,389 shares of common stock, priced at $7.15 per share. Client Description: inContact, Inc. provides cloud contact center software solutions. PJC Role: Piper Jaffray acted as bookrunner for the offering. -

Operating Review International

Operating review 1 International 2 3 4 1. Unbeatable offers in Gentofte – El Giganten’s biggest store in Denmark. 2. Gigantti doubled its store base in Finland, growing from four to eight stores. 3. Thousands of customers queued to shop in the first Electro World store in Budapest, February 2002. 4. Shopping for fantastic offers at the Electro World opening. 22 Dixons Group plc Annual Report & Accounts 2001/02 4 The International Retail division achieved Elkjøp opened 15 new stores, including an operating profit of £15.2 million five El Gigantens in Sweden and four (£22.3 million) on sales increased by Gigantti stores in Finland, bringing its 14 per cent to £688 million (£602 million). total to 148 stores in five countries. We intend to open a further 11 new Nordic countries stores in this financial year. Elkjøp’s sales increased by 12 per cent to £596 million (£531 million). Although Central Europe like for like sales were 1 per cent lower, In February, the Elkjøp team launched this reflected a downturn in a number the Group’s first store in Hungary under of Nordic markets. Elkjøp continued to the Electro World brand. The 43,000 5 gain share in each of its markets. square feet store combines the best of the Group’s formats from around In July 2001, Elkjøp completed Europe. The store has quickly established the purchase of seven out of town a strong market presence.We intend SuperRadio stores in Denmark. to open a further Electro World store These stores have been rebranded in Budapest and our first in Prague this under Elkjøp’s El Giganten fascia and financial year. -

Chief Executive's Review Group Turnover for the 52 Weeks Ended 27

Chief Executive’s review Group turnover for the 52 weeks ended 27 April 2002 increased by 5 per cent to £4,888 million (2000/01 £4,643 million excluding Freeserve). Like for like sales were unchanged across the Group in challenging markets. Group profit before tax and exceptional The Group continued to grow market telecoms solutions provider for the items increased by 7 per cent to £297.2 share, showing particularly strong gains business to business market. million (2000/01 £277.8 million before in widescreen televisions, large domestic taxation, exceptional items and Freeserve). appliances, games, personal computers International and PC related products. The International Retail division achieved UK Retail an operating profit of £15.2 million UK Retail division operating profit before The product cycle is a major determinant (£22.3 million) on sales ahead 14 per cent exceptional items was £253.6 million of sales growth. New products have at £688 million (£602 million). (£244.8 million), an increase of 4 per cent. driven sales even during the recessions Total UK Retail sales were £4,122 million of the early 1980s and 1990s. Looking Our expansion into Continental (£3,979 million), a 4 per cent increase ahead, the product outlook appears Europe continued, with investments year on year and unchanged like for like. positive with new technologies coming in eight markets. The Group now has onto the market, from large flat screen retail operations in 11 countries. Although Currys and PC World made televisions to wireless home networks, As anticipated, start-up losses were strong contributions to the divisional and the potential for a recovery in the incurred in new businesses in France, performance, these were largely personal computer market. -

Discover Athens, Greece Top 5

Discover Athens, Greece Photo: Anastasios71/Shutterstock.com Of all Europe’s historical capitals, Athens is probably the one that has changed the most in recent years. But even though it has become a modern metropolis, it still retains a good deal of its old small town feel. Here antiquity meets the future, and the ancient monuments mix with a trendier Athens and it is precisely these great contrasts that make the city such a fascinating place to explore.The heart of its historical centre is the Plaka neighbourhood, with narrow streets mingling like a labyrinth where to discover ancient secrets. Anastasios71/Shutterstock.com Top 5 1. Roman Agora During the antiquity, the Agora played a major role as both a marketplace and … 2. National Archaeological Museum The National Archaeological Museum, in Exarchia, is home to 3. The Acropolis and its surround The Parthenon, the temple of Athena, is the major city attraction as well as... Anastasios71/Shutterstock.com 4. Benaki Museum of Greek Culture Benaki is a history museum with Greek art and objects from the 5. Mount Lycabettus Mount Lycabettus (in Greek: Lykavittos, Λυκαβηττός) lies right in the centre... Milan Gonda/Shutterstock.com Athens THE CITY DO & SEE Nick Pavlakis/Shutterstock.com Anastasios71/Shutterstock.com Athens’ heyday was around 400 years BC, that’s Dive in perhaps the most historically rich capital when most of the classical monuments were of Europe and discover its secrets. Athens' past built. During the Byzantine and Turkish eras, the and its landmarks are worldly famous, but the city decayed into just an insignicant little city ofiers much more than the postcards show: village, only to become the capital of it is a vivid city of culture and art, where the newly-liberated Greece in 1833. -

PR 04/09 7.00Am, 15 January 2009 DSG

PR 04/09 7.00am, 15 January 2009 DSG INTERNATIONAL PLC INTERIM MANAGEMENT STATEMENT DSG international plc, one of Europe’s leading specialist electrical retailers, is today updating the market on trading for the 12 weeks ended 10 January 2009. • In the 12 week period, total Group sales were down 1% in sterling and like for like sales were down 10%. • In the two week period to 10 January, Group like for likes were up 2%, with a better performance in UK computing and electricals and with Nordics flat. • Gross margins across the Group were down 0.8% year on year, primarily as a result of both the increased proportion of revenue in the sale period as well as a higher mix of televisions and laptops. • The Group remains focused on cash, cutting costs, managing margins and reducing stock. • Further cost reductions in the current year of £20 million in response to trading environment, bringing total cost savings for the year to £95 million. • Careful stock management has resulted in stock levels 16% lower than last year at constant exchange rates. • The Group is operating within its £400 million committed credit facility which is currently undrawn and available, although it is expected that some drawdown will occur in the final quarter, as anticipated. • Renewal and Transformation plan on track: • New format stores continue to perform strongly with sales 15% to 25% ahead of the rest of the chain; • 41 PC World, 11 Currys Superstores, 4 Currys.digital, 1 Currys Megastore and 1 trial combined PC World and Currys store all traded through Christmas Peak; • Currys Megastore sales and gross profit contribution exceeded expectations and should generate over £30 million of sales per year. -

DSG International Plc

28 November 07 - PR 160/07 Strictly embargoed For release at 07.00 hours DSG international plc INTERIM RESULTS FOR THE 24 WEEKS ENDED 13 OCTOBER 2007 DSG international plc, one of Europe’s largest specialist electrical retailers, today announces Interim results for the 24 weeks ended 13 October 2007: Financial highlights • Group sales up 8% to £3,377.6 million (2006/07(1): £3,123.5 million) • Group sales up 9% excluding PC City France(2) • Group like for like sales(3) up 5% • International sales now represent 42% of total Group sales • Underlying pre-tax profit(4) £52.4 million (2006/07: £70.3 million) • Profit after tax £37.3 million (2006/07: £29.8 million) • Underlying diluted earnings per share 2.0 pence (2006/07: 2.6 pence); Basic earnings per share 2.0 pence (2006/07: 1.9 pence) • Interim dividend per share 2.02 pence (2006/07: 2.02 pence) • 39.9 million shares repurchased for a total consideration of £61.2 million • On track to deliver over £30 million of cost savings in the full year, ahead of target • Continued focus on working capital maintaining zero average paid days stock(5) Page 1 of 32 Operational highlights • Group continues to capitalise on strong demand for digital products such as flat panel televisions, games consoles and laptops • Unique structure of five core logistics hubs now operational across Europe • The TechGuys sales doubled, responding to demand for support and service from customers • Successful launch of new large space mixed electrical format in Europe and introduction of mezzanines into Currys stores • Electro World brand launched in Greece and Turkey • Strong growth in internet sales, underpinning the Group’s multi-channel and pure play approach • Recycling and in-store take-back of used products launched in the UK with 12,000 tonnes collected so far Sir John Collins, Group Chairman commented: “We had an encouraging start to the year in terms of sales, and I am pleased with the performances of the UK Electricals businesses as well as our operations in the Nordics, Greece and Central Europe. -

AUTO RECONCILIATION SERVER • Cost Reduction

Note: This brochure is Customer designed to be Managing critical Dixons Carphone Warehouse Auto printed. You tasks at the entry should test print point is fundamental Region Reconciliation on regular paper to increase Europe to ensure proper productivity and positioning before Challenge – How it started printing on card ensure information stock. • Input of source 100% paper based. Papersoft professional services for Enterprise departments, quality at a lower enterprise shared services – SSC or large BPO providers that • Manage input branches all over the UK and IRL. cost. want to: You may need to • Monthly +1M/documents. • Organize unstructured data. uncheck Scale to • Human based reporting to commissions team and loss Fit Paper in the prevention. • Manage volume peaks. • Register accurate data into ERP´s. Print dialog (in the • Multiple document reconciliation checks such as bank statements, IDs, contract and others. • Meet regulatory target dates. Full Page Slides • External/Internal audit control. dropdown). To speed up implementation • Vendor relation satisfaction. “we took a staged approach. Benefits from initiative • Credibility/Professionalism. Papersoft consulted with us Check your printer • Full process automation. to create a roadmap of the Finance departments that aim to: instructions to • Process standardisation. print double-sided discrete stages and • Approve/Reject internal information. • Compliant and auditable customer info. pages. identified gaps where best • Avoid service cancellation/penalties. Workflow with alerts and action steps on frauds and practices would speed up • • Optimize cash flow. each phase. This approach errors for all branches. To change images allowed us to accelerate on this slide, business transformation and Benefits from Papersoft ecosystem select a picture greatly reduced the About Dixons Carphone Warehouse and delete it. -

Greece Athens University of Economics and Business Fourlis

CFA Institute Research Challenge hosted by CFA Society Greece Athens University of Economics and Business The CFA Institute Research Challenge is a global competition that tests the equity research and valuation, investment report writing, and presentation skills of university students. The following report was submitted by a team of university students as part of this annual educational initiative and should not be considered a professional report. Disclosures: Ownership and material conflicts of interest The author(s), or a member of their household, of this report does not hold a financial interest in the securities of this company. The author(s), or a member of their household, of this report does not know of the existence of any conflicts of interest that might bias the content or publication of this report. Receipt of compensation Compensation of the author(s) of this report is not based on investment banking revenue. Position as an officer or a director The author(s), or a member of their household, does not serve as an officer, director, or advisory board member of the subject company. Market making The author(s) does not act as a market maker in the subject company’s securities. Disclaimer The information set forth herein has been obtained or derived from sources generally available to the public and believed by the author(s) to be reliable, but the author(s) does not make any representation or warranty, express or implied, as to its accuracy or completeness. The information is not intended to be used as the basis of any investment decisions by any person or entity. -

Appointment of New Group CEO

22 January 2018 Embargoed until 7.00am Appointment of new Group CEO Dixons Carphone plc announces the appointment of Alex Baldock as Group Chief Executive from April 2018, to succeed Sebastian James who has informed the board of his decision to step down around the end of the financial year after six years in the role. Sebastian will be joining Walgreens Boots Alliance later this year. Alex Baldock is currently Group Chief Executive of Shop Direct plc, the UK’s second largest pure-play online retailer, a position which he has held since 2012. Ian Livingston, Chairman of Dixons Carphone plc, said: “Seb has made an outstanding contribution to both the creation and success of Dixons Carphone. It is a much stronger company today than when he became CEO of Dixons Retail in 2012 with revenue, profit and customer satisfaction all substantially higher. The Group is now the market leader in eight countries.” “On behalf of the Board and all our colleagues, I would like to thank Seb for all that he has done over the past six years as CEO of first Dixons Retail and now Dixons Carphone. We wish him every success in his new role.” “The Board and I are delighted to welcome Alex Baldock to the Group. He has an outstanding track record in leading large, complex consumer-facing businesses. He’s led Shop Direct through one of UK Retail’s fastest, most far-reaching and most successful digital transformations, delivering five consecutive years of record financial performance, with strongly rising sales and an almost tenfold increase in profits. -

Continued Strong Online Momentum Despite Covid

20 January 2021 Trading Update for 10 weeks ended 9 January 2021 Continued strong online momentum despite Covid impact • Electricals like-for-like revenue +11% o Highest growth in large screen TVs, smart tech, food preparation, health & beauty and all areas of computing & gaming • UK & Ireland Electricals like-for-like revenue +8% o Online growth +121% o Online market share +6%pts • International like-for-like revenue +14%: Nordics +19%, Greece (13)% o Nordic online sales +97%, Greece online sales +366% o Nordics: Double-digit growth and strong market share gains o Greece: Performance impacted by national lockdown • UK & Ireland Mobile total revenue down (40)% o Sales and cashflow in line with plan given UK standalone Carphone Warehouse store closures last April • Transformation progress: o Omnichannel: Group Electricals online sales +118%. ShopLive 24/7 live video shopping growing strongly o Credit: UK Electricals credit customers grew to 1.4m o Services: Nordic Customer Club grew to over 4.9m members and 50% of Black Friday week sales o Mobile: Restructuring on track, new mobile offer to launch this year Alex Baldock, Group Chief Executive “I’m so grateful to my colleagues. Thanks to their dedication and adaptability in such a testing time, we’ve kept safely providing vital technology to the public, keeping millions of people connected, healthy, productive and entertained. And so we’ve continued to trade strongly, both in the UK and Internationally, while ensuring colleague and customer safety is paramount. We’re winning online, where we’re the biggest and fastest-growing specialist technology retailer in all our markets.