Download This PDF File

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

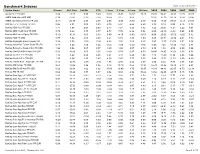

Benchmark Indexes Data As Of: 03/31/2011 Index Name Sharpe Std

Benchmark Indexes Data as of: 03/31/2011 Index Name Sharpe Std. Dev. 1st Qtr YTD 1 Year 3 Year 5 Year 10 Year 2010 2009 2008 2007 2006 Alerian MLP TR USD 0.89 23.25 5.99 5.99 33.02 20.03 16.57 17.25 35.85 76.41 -36.91 12.72 26.07 AMEX Gold Miners PR USD 0.39 47.82 -2.15 -2.15 35.65 8.12 9.68 - 33.94 37.30 -26.79 16.86 21.86 AMEX International Market PR USD -0.13 25.37 2.77 2.77 4.05 -5.95 -0.80 2.17 0.80 17.60 -39.51 16.18 21.51 BarCap 1-5 Yr Treasury TR USD 0.98 2.51 0.00 0.00 2.79 2.91 4.88 4.20 3.73 0.19 8.83 8.16 3.75 BarCap ABS Auto TR USD 1.17 5.68 0.63 0.63 2.47 7.21 6.23 5.12 3.25 26.07 -5.57 5.22 4.61 BarCap ABS Credit Card TR USD 0.79 9.42 0.77 0.77 4.73 7.76 6.86 5.84 6.55 29.89 -9.33 5.45 4.55 BarCap ABS Home Equity TR USD -0.19 16.91 0.00 0.00 0.00 -4.10 -5.80 -0.53 0.00 20.63 -36.00 -8.25 5.32 BarCap ABS TR USD 0.77 6.92 0.64 0.64 4.21 5.74 4.36 4.59 5.85 24.71 -12.72 2.21 4.70 BarCap Aggregate Bond Treasury TR 0.58 5.58 -0.16 -0.16 4.53 3.55 5.69 5.15 5.87 -3.57 13.74 9.01 3.08 BarCap Asian Pac Taiwan Dollar TR JPY 0.78 6.24 1.54 1.54 -2.45 -1.00 -2.50 -0.66 -2.26 7.45 -11.24 -7.52 2.81 BarCap Bellwether Swap 6 Mon TR USD 1.92 0.56 0.07 0.07 0.39 1.50 3.07 2.79 0.38 1.58 4.09 5.39 5.54 BarCap CMBS ERISA Eligible TR USD 0.53 18.46 2.05 2.05 12.62 8.79 6.87 6.53 20.40 28.45 -20.52 5.58 4.72 BarCap Credit 1-3 Yr TR USD 1.16 3.62 0.58 0.58 3.24 4.73 5.29 4.80 4.15 11.59 0.30 5.96 4.66 BarCap Credit 1-5 Yr TR USD 1.06 4.64 0.85 0.85 4.36 5.47 5.77 5.27 5.44 13.52 -1.13 6.09 4.69 BarCap Danish Krone Aggregate TR DKK 0.12 14.76 -

Press Release Paris – June 21St, 2021

Press Release Paris – June 21st, 2021 Europcar Mobility Group rejoins Euronext SBF 120 index Europcar Mobility Group, a major player in mobility markets, is pleased to announce that it has re-entered into the SBF 120 and CAC Mid 60 indices, in accordance with the decision taken by the Euronext Index Steering Committee. This re-entry, which took place after market close on Friday 18 June 2021, is effective from Monday 21 June 2021. The SBF 120 is one of the flagship indices of the Paris Stock Exchange. It includes the first 120 stocks listed on Euronext Paris in terms of liquidity and market capitalization. The CAC Mid 60 index includes 60 companies of national and European importance. It represents the 60 largest French equities beyond the CAC 40 and the CAC Next 20. It includes the 60 most liquid stocks listed in Paris among the 200 first French capitalizations. This total of 120 companies compose the SBF 120. Caroline Parot, CEO of Europcar Mobility Group, said: “Europcar Mobility Group welcomes the re-integration of the SBF 120 and CAC Mid 60. This follows the successful closing of the Group’s financial restructuring during Q1 2021, which allowed the Group to open a new chapter in its history. Europcar Mobility Group re-entry into the SBF 120 and CAC Mid 60 is an important step for our Group and recognizes the fact that we are clearly "back in the game”, in a good position to take full advantage of the progressive recovery of the Travel and Leisure market. In that perspective, our teams are fully mobilized for summer of 2021, in order to meet the demand and expectations of customers who are more than ever eager to travel”. -

Financial Market Data for R/Rmetrics

Financial Market Data for R/Rmetrics Diethelm Würtz Andrew Ellis Yohan Chalabi Rmetrics Association & Finance Online R/Rmetrics eBook Series R/Rmetrics eBooks is a series of electronic books and user guides aimed at students and practitioner who use R/Rmetrics to analyze financial markets. A Discussion of Time Series Objects for R in Finance (2009) Diethelm Würtz, Yohan Chalabi, Andrew Ellis R/Rmetrics Meielisalp 2009 Proceedings of the Meielisalp Workshop 2011 Editor Diethelm Würtz Basic R for Finance (2010), Diethelm Würtz, Yohan Chalabi, Longhow Lam, Andrew Ellis Chronological Objects with Rmetrics (2010), Diethelm Würtz, Yohan Chalabi, Andrew Ellis Portfolio Optimization with R/Rmetrics (2010), Diethelm Würtz, William Chen, Yohan Chalabi, Andrew Ellis Financial Market Data for R/Rmetrics (2010) Diethelm W?rtz, Andrew Ellis, Yohan Chalabi Indian Financial Market Data for R/Rmetrics (2010) Diethelm Würtz, Mahendra Mehta, Andrew Ellis, Yohan Chalabi Asian Option Pricing with R/Rmetrics (2010) Diethelm Würtz R/Rmetrics Singapore 2010 Proceedings of the Singapore Workshop 2010 Editors Diethelm Würtz, Mahendra Mehta, David Scott, Juri Hinz R/Rmetrics Meielisalp 2011 Proceedings of the Meielisalp Summer School and Workshop 2011 Editor Diethelm Würtz III tinn-R Editor (2010) José Cláudio Faria, Philippe Grosjean, Enio Galinkin Jelihovschi and Ri- cardo Pietrobon R/Rmetrics Meielisalp 2011 Proceedings of the Meielisalp Summer Scholl and Workshop 2011 Editor Diethelm Würtz R/Rmetrics Meielisalp 2012 Proceedings of the Meielisalp Summer Scholl and Workshop 2012 Editor Diethelm Würtz Topics in Empirical Finance with R and Rmetrics (2013), Patrick Hénaff FINANCIAL MARKET DATA FOR R/RMETRICS DIETHELM WÜRTZ ANDREW ELLIS YOHAN CHALABI RMETRICS ASSOCIATION &FINANCE ONLINE Series Editors: Prof. -

Neoen Joins the SBF 120Index

Paris, June 11, 2020 Neoen joins the SBF 120 index Neoen (ISIN: FR0011675362, Ticker: NEOEN), one of the world’s leading and fastest-growing independent producers of exclusively renewable energy, is announcing it is joining the SBF 120 index consisting of the top 120 stocks listed on the Euronext Paris market in term of both liquidity and market capitalization. As part of its quarterly review of the Euronext Paris indices, the Index Committee decided to include Neoen in both the SBF 120 and the CAC Mid 60 indices. This decision will take effect from June 22, 2020. Neoen’s inclusion in these indices is a testament to its good share price performance since its October 2018 IPO. Over the past 20 months, the Company’s market capitalization has more than doubled to almost €3 billion. This strong rise was accompanied by a steady increase in trading volumes. Since its IPO, Neoen has consistently delivered strong earnings growth and expansion in its project portfolio. Assets in operation or under construction have increased from 1.8 GW at June 30, 2018 to 3.1 GW at March 31, 2020, and the target is to have more than 5 GW by year-end 2021. This rapid and profitable growth has been founded on geographical and technological diversification of its asset base. Neoen is present in 14 countries on 4 continents and it develops and operates solar and wind energy generation and storage capacity. Xavier Barbaro, Neoen’s Chairman and Chief Executive Officer, commented: “We are very pleased to be joining this benchmark index, which marks a new important step for Neoen. -

Final Report Amending ITS on Main Indices and Recognised Exchanges

Final Report Amendment to Commission Implementing Regulation (EU) 2016/1646 11 December 2019 | ESMA70-156-1535 Table of Contents 1 Executive Summary ....................................................................................................... 4 2 Introduction .................................................................................................................... 5 3 Main indices ................................................................................................................... 6 3.1 General approach ................................................................................................... 6 3.2 Analysis ................................................................................................................... 7 3.3 Conclusions............................................................................................................. 8 4 Recognised exchanges .................................................................................................. 9 4.1 General approach ................................................................................................... 9 4.2 Conclusions............................................................................................................. 9 4.2.1 Treatment of third-country exchanges .............................................................. 9 4.2.2 Impact of Brexit ...............................................................................................10 5 Annexes ........................................................................................................................12 -

Execution Version GUARANTEED SENIOR SECURED NOTES

Execution Version GUARANTEED SENIOR SECURED NOTES PROGRAMME issued by GOLDMAN SACHS INTERNATIONAL in respect of which the payment and delivery obligations are guaranteed by THE GOLDMAN SACHS GROUP, INC. (the “PROGRAMME”) PRICING SUPPLEMENT DATED 21 DECEMBER 2020 SERIES 2020-20 SENIOR SECURED FIXED RATE NOTES (the “SERIES”) ISIN: XS2277589615 Common Code: 227758961 This document constitutes the Pricing Supplement of the above Series of Secured Notes (the “Secured Notes”) and must be read in conjunction with the Base Listing Particulars dated 25 September 2020, as supplemented and amended by Prospectus Supplement No. 1 dated 20 October 2020, Prospectus Supplement No. 2 dated 2 November 2020 and Prospectus Supplement No. 3 dated 12 November 2020 (as so amended the “Base Listing Particulars”), and in particular, the Base Terms and Conditions of the Secured Notes, as set out therein. Full information on the Issuer, The Goldman Sachs Group. Inc. (the “Guarantor”), and the terms and conditions of the Secured Notes, is only available on the basis of the combination of this Pricing Supplement and the Base Listing Particulars as so supplemented. The Base Listing Particulars has been published at www.ise.ie and is available for viewing during normal business hours at the registered office of the Issuer, and copies may be obtained from the specified office of the listing agent in Ireland. The Issuer accepts responsibility for the information contained in this Pricing Supplement. To the best of the knowledge and belief of the Issuer and the Guarantor the information contained in the Base Listing Particulars, as completed by this Pricing Supplement in relation to the Series of Secured Notes referred to above, is true and accurate in all material respects and, in the context of the issue of this Series, there are no other material facts the omission of which would make any statement in such information misleading. -

Execution Version

Execution Version GUARANTEED SENIOR SECURED NOTES PROGRAMME issued by GOLDMAN SACHS INTERNATIONAL in respect of which the payment and delivery obligations are guaranteed by THE GOLDMAN SACHS GROUP, INC. (the “PROGRAMME”) PRICING SUPPLEMENT DATED 23rd SEPTEMBER 2020 SERIES 2020-12 SENIOR SECURED EXTENDIBLE FIXED RATE NOTES (the “SERIES”) ISIN: XS2233188510 Common Code: 223318851 This document constitutes the Pricing Supplement of the above Series of Secured Notes (the “Secured Notes”) and must be read in conjunction with the Base Listing Particulars dated 25 September 2019, as supplemented from time to time (the “Base Prospectus”), and in particular, the Base Terms and Conditions of the Secured Notes, as set out therein. Full information on the Issuer, The Goldman Sachs Group. Inc. (the “Guarantor”), and the terms and conditions of the Secured Notes, is only available on the basis of the combination of this Pricing Supplement and the Base Listing Particulars as so supplemented. The Base Listing Particulars has been published at www.ise.ie and is available for viewing during normal business hours at the registered office of the Issuer, and copies may be obtained from the specified office of the listing agent in Ireland. The Issuer accepts responsibility for the information contained in this Pricing Supplement. To the best of the knowledge and belief of the Issuer and the Guarantor the information contained in the Base Listing Particulars, as completed by this Pricing Supplement in relation to the Series of Secured Notes referred to above, is true and accurate in all material respects and, in the context of the issue of this Series, there are no other material facts the omission of which would make any statement in such information misleading. -

Structures De Gouvernance Des Sociétés Cotées Radiographie

Structures de gouvernance des sociétés cotées Radiographie Observatoire Capital humain Centre de Gouvernement d'Entreprise Octobre 2015 Second line optional lorem ipsum B Subhead lorem ipsum, date quatueriure Mesurer pour comprendre, comprendre pour agir, agir pour progresser Sommaire Executive Summary 2 Préambule 4 1. Radiographie des conseils 7 Introduction 7 Typologie des conseils 8 Indépendance des administrateurs 12 Féminisation des conseils 14 Internationalisation des conseils 18 Distribution par âge et par ancienneté 20 Cumul des mandats 22 Mercato 2014-2015 25 Rémunérations des administrateurs 29 Evaluation des conseils 38 2. Les comités du Conseil 42 Introduction 43 Comités spécialisés 45 3. Assemblées générales 2015 52 Introduction 53 Nature des résolutions 54 Résultats des votes 56 Facteurs d'influence 66 Liste des sociétés 70 Structures de gouvernance des sociétés cotées - Radiographie 1 Executive Summary Des pratiques globalement en ligne avec les codes de gouvernance, mais des différences marquées selon l'indice de cotation Nous sommes très heureux de vous présenter la Nous étudierons les comités spécialisés, leur fréquence radiographie de la gouvernance des sociétés cotées et leur composition, ainsi que la distribution des rôles 2015, issue de l’analyse des pratiques de gouvernement des administrateurs en leur sein. d’entreprise de plus de 300 sociétés cotées au marché Le chapitre relatif aux assemblées générales 2015 Euronext de la Bourse de Paris. analysera près de 5 700 résolutions présentées lors Le gouvernement d’entreprise désigne les modes de 318 assemblées générales en rapprochant les taux de fonctionnement des organes d'administration et d’approbation, la nature des résolutions, la structure de surveillance d’une organisation et leurs relations actionnariale des sociétés et les recommandations de avec la direction et les actionnaires. -

Euronext Indices - Performance Report - November 2015

EURONEXT INDICES - PERFORMANCE REPORT - NOVEMBER 2015 Closing Levels Returns Index Name Nr. of Constit. ISIN Code Mnemo Location Index Type 30/11/2015 30/10/2015 31/12/2014 Ann. 3 Year Ann. 5 Year '15 YtD Nov-15 Blue-Chip Indices (Price) AEX 25 NL0000000107 AEX Amsterdam Blue Chip 469.52 462.12 424.47 11.74% 7.48% 10.61% 1.60% BEL 20 20 BE0389555039 BEL20 Brussels Blue Chip 3760.89 3600.20 3285.26 15.56% 8.46% 14.48% 4.46% CAC 40 40 FR0003500008 PX1 Paris Blue Chip 4957.60 4897.66 4272.75 11.70% 6.55% 16.03% 1.22% PSI 20 18 PTING0200002 PSI20 Lisbon Blue Chip 5350.36 5468.69 4798.99 0.59% -6.08% 11.49% -2.16% Blue-Chip Indices (Net Return) AEX NR 25 QS001121156 AEXNR Amsterdam Blue Chip 1253.92 1231.03 1103.04 14.64% 10.50% 13.68% 1.86% BEL 20 NR 20 BE0389558066 BEL2P Brussels Blue Chip 7287.22 6964.52 6207.32 18.87% 11.69% 17.40% 4.63% CAC 40 NR 40 QS0011131826 PX1NR Paris Blue Chip 9443.83 9325.58 7976.45 14.30% 9.36% 18.40% 1.27% PSI 20 NR 18 QS0011211180 PSINR Lisbon Blue Chip 9566.04 9777.61 8412.60 2.81% -3.45% 13.71% -2.16% Blue-Chip Indices (Gross Return) AEX GR 25 QS0011131990 AEXGR Amsterdam Blue Chip 1411.77 1386.00 1237.44 15.07% 11.01% 14.09% 1.86% BEL 20 GR 20 BE0389557050 BEL2I Brussels Blue Chip 9153.18 8743.12 7730.39 20.02% 12.82% 18.41% 4.69% CAC 40 GR 40 QS0011131834 PX1GR Paris Blue Chip 11760.34 11610.92 9849.44 15.42% 10.50% 19.40% 1.29% PSI 20 GR 18 PTING0210005 PSITR Lisbon Blue Chip 11117.58 11363.48 9713.40 3.56% -2.55% 14.46% -2.16% French Indices CAC Next 20 20 QS0010989109 CN20 Paris Size 10428.31 9990.90 -

Names, Acronyms, and Facts About Important Stock Exchanges Around the World Nyse

NAMES, ACRONYMS, AND FACTS ABOUT IMPORTANT STOCK EXCHANGES AROUND THE WORLD NYSE New York Stock Exchange HQ- New York, USA Important facts: At a market capitalisation of over US$25 trillion the NYSE represents nearly 40% of the total market value in the world and is the largest stock exchange in the world. Stacey Cunningham is appointment as NYSE president and she is the first lady to be appointed as the president in 226 year long history of NYSE. NASDAQ National Association of Securities Dealers Automated Quotations HQ- New York USA It has a combined market capitalisation of nearly US$12 trillion. Ranked 2nd in terms of Market Cap in the world. JPX/TSE/TYO/Nikkei Tokyo Stock Exchange – TSE Japan Exchange Group - JPX Country- Japan Ranked 3rd in terms of market cap i.e. US$6.2 trillion. Important facts: JPX is the Asia’s largest exchange in terms of market capital and monthly trading. SSE Shanghai Stock Exchange HQ – Shanghai, China. Ranked 4th in terms of market cap i.e. US$5 trillion. SZSE Shenzhen Stock Exchange. HQ – Shenzhen, China. It has a market cap of around US$3.5 trillion. Euronext Euronext is the largest stock exchange in Europe and fifth largest in the world. Originally created by the mergers of Amsterdam, Paris and Brussels stock exchanges. Market Cap: US$4.6 trillion Some of its more notable benchmark indices include: AEX/AMX/AScX Index Amsterdam Exchange index HQ- Amsterdam, Netherlands. BEL 20 BEL 20 is the benchmark stock market index of Euronext Brussels. Country – Belgium. CAC 40/CAC Small The CAC 40 (Cotation Assistée en Continu) is a benchmark French stock market index. -

Lyxor Mergers

Merger of Lyxor funds on 19 April 2018 List of funds identifiers Lyxor CAC 40 Daily (2x) Leveraged UCITS ETF Label Absorbed fund indentifier Absorbing fund identifier Acc Share ISIN Code FR0010592014 No change BBG Ticker - Euronext Paris LVC FP No change Lyxor CAC 40 Daily (-2x) Inverse UCITS ETF Label Absorbed fund indentifier Absorbing fund identifier Acc Share ISIN Code FR0010411884 No change BBG Ticker - Euronext Paris BX4 FP No change Lyxor CAC 40 Daily (-1x) Inverse UCITS ETF Label Absorbed fund indentifier Absorbing fund identifier Acc Share ISIN Code FR0010591362 No change BBG Ticker - Euronext Paris SHC FP No change Lyxor CAC MID 60 UCITS ETF Label Absorbed fund indentifier Absorbing fund identifier Dist Share ISIN Code FR0011041334 No change BBG Ticker - Euronext Paris CACM FP No change Merger of Lyxor funds on 19 April 2018 List of funds identifiers Lyxor IBEX 35 Doble Apalancado Diario UCITS ETF Label Absorbed fund indentifier Absorbing fund identifier Acc Share ISIN Code FR0011042753 No change BBG Ticker - Bolsa de Madrid IBEXA SM No change Lyxor IBEX 35 Inverso Diario UCITS ETF Label Absorbed fund indentifier Absorbing fund identifier Acc Share ISIN Code FR0010762492 No change BBG Ticker - Bolsa de Madrid INVEX SM No change Lyxor IBEX 35 Doble Inverso Diario UCITS ETF Label Absorbed fund indentifier Absorbing fund identifier Acc Share ISIN Code FR0011036268 No change BBG Ticker - Bolsa de Madrid IBEXA SM No change Merger of Lyxor funds on 19 April 2018 List of funds identifiers Lyxor Daily ShortDAX x2 UCITS ETF Label Absorbed -

Carmila Joins the Sbf 120 and Cac Mid 60

PRESS RELEASE Boulogne-Billancourt, 11 December 2020 CARMILA JOINS THE SBF 120 AND CAC MID 60 Carmila is pleased to announce that it has joined the SBF 120 – a flagship Paris stock exchange index listing the top 120 Euronext Paris stocks in terms of liquidity and market capitalisation – as well as the CAC Mid 60. Following the quarterly review of the Euronext Paris indices on 10 December 2020, the Expert Indices Committee (Conseil Scientifique des Indices) decided at its meeting held the same day to include Carmila among the issuers making up the SBF 120 and CAC Mid 60 indices. This decision will take effect on 18 December 2020, after trading. Marie Cheval, Chairman and Chief Executive Officer of Carmila, said: "Carmila's entry in the SBF 120 and CAC Mid 60 represents a milestone in the company's stock market journey and serves to recognise its steady trajectory and solid performance." INVESTOR AND ANALYST CONTACT PRESS CONTACT Florence Lonis – General Secretary Morgan Lavielle - Corporate Communications Director [email protected] [email protected] +33 6 82 80 15 64 +33 6 87 77 48 80 INVESTOR AGENDA 17 February 2021 (after trading): 2020 Annual Results 18 February 2021 (9:00 a.m. Paris time): Investor and Analyst Meeting 22 April 2021 (after trading): First-quarter 2021 Financial Information 28 July 2021 (after trading): 2021 Half-year Results 29 July 2021 (2:30 p.m. Paris time): Investor and Analyst Meeting Visit our website 1 at https://www.carmila.com/en/ PRESS RELEASE ABOUT CARMILA As the third largest listed owner of commercial property in continental Europe, Carmila was founded by Carrefour and large institutional investors in order to transform and enhance the value of shopping centres adjoining Carrefour hypermarkets in France, Spain and Italy.