Comparative Study of Customer's Satisfaction Towards Hdfc Bank And

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Application Form for Debt Schemes

Application Form for Debt Schemes HDFC INCOME FUND l HDFC SHORT TERM PLAN l HDFC LIQUID FUND $ HDFC HIGH INTEREST FUND l HDFC FLOATING RATE INCOME FUND HDFC CASH MANAGEMENT FUND l HDFC GILT FUND CDQ Continuing a tradition of trust. Offer of Units At NAV Based Prices Investors must read the Key Information Memorandum and the instructions before completing this Form. KEY PARTNER / AGENT INFORMATION FOR OFFICE USE ONLY Name and AMFI Reg. No. (ARN) Sub Agent’s Name and Code Date of Receipt Folio No. Branch Trans. No. ISC Name & Stamp South Indian Bank ARN-3845 1. EXISTING UNIT HOLDER INFORMATION (If you have existing folio, please fill in your folio number, complete details in section 2 and proceed to section 6. Refer instruction 2). Folio No. The details in our records under the folio number mentioned alongside will apply for this application. 2. PAN AND KYC COMPLIANCE STATUS DETAILS (MANDATORY) PAN # (refer instruction 13) KYC Compliance Status** (if yes, attach proof) First / Sole Applicant / Guardian * Yes No Second Applicant Yes No Third Applicant Yes No *If the first/sole applicant is a Minor, then please state the details of Guardian. # Please attach PAN proof. If PAN is already validated, please don’t attach any proof. ** Refer instruction 15 3. STATUS (of First/Sole Applicant) MODE OF HOLDING OCCUPATION (of First/Sole Applicant) [Please tick (4)] [Please tick (4)] [Please tick (4)] Resident Individual NRI Partnership Trust Single Service Student Professional HUF AOP Company FIIs Joint Housewife Business Retired Minor through guardian BOI Body Corporate Anyone or Survivor Agriculture Society / Club Others _____________________ (please specify) Others ________________ (please specify) 4. -

Official Site, Telegram, Facebook, Instagram, Instamojo

Page 1 Follow us: Official Site, Telegram, Facebook, Instagram, Instamojo All SUPER Current Affairs Product Worth Rs 1200 @ 399/- ( DEAL Of The Year ) Page 2 Follow us: Official Site, Telegram, Facebook, Instagram, Instamojo SUPER Current Affairs MCQ PDF 3rd August 2021 By Dream Big Institution: (SUPER Current Affairs) © Copyright 2021 Q.World Sanskrit Day 2021 was celebrated on ___________. A) 3 August C) 5 August B) 4 August D) 6 August Answer - A Sanskrit Day is celebrated every year on Shraavana Poornima, which is the full moon day in the month of Shraavana in the Hindu calendar. In 2020, Sanskrit Day was celebrated on August 3, while in 2019 it was celebrated on 15 August. Sanskrit language is believed to be originated in India around 3,500 years ago. Q.Nikol Pashinyan has been re-appointed as the Prime Minister of which country? A) Ukraine C) Turkey B) Armenia D) Lebanon Answer - B Nikol Pashinyan has been re-appointed as Armenia’s Prime Minister by President Armen Sarkissian. Pashinyan was first appointed as the prime minister in 2018. About Armenia: Capital: Yerevan Currency: Armenian dram President: Armen Sargsyan Page 3 Follow us: Official Site, Telegram, Facebook, Instagram, Instamojo Q.Min Aung Hlaing has taken charge as the Prime Minister of which country? A) Bangladesh C) Thailand B) Laos D) Myanmar Answer - D The Chief of the Myanmar military, Senior General Min Aung Hlaing has taken over as the interim prime minister of the country on August 01, 2021. About Myanmar Capital: Naypyitaw; Currency: Kyat. NEWLY Elected -

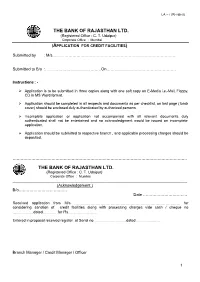

Credit Facility (LA-I Revised) Form

LA – I (REVISED) THE BANK OF RAJASTHAN LTD. (Registered Office : C. T. Udaipur) Corporate Office : Mumbai (APPLICATION FOR CREDIT FACILITIES) Submitted by : M/s………………………………………………………………………………… Submitted to B/o :……………………………………On……………………………………………. Instructions : - Ø Application is to be submitted in three copies along with one soft copy on E-Media i.e.-Mail, Floppy, CD in MS Word format. Ø Application should be completed in all respects and documents as per checklist, on last page ( back cover) should be enclosed duly authenticated by authorized persons. Ø Incomplete application or application not accompanied with all relevant documents duly authenticated shall not be entertained and no acknowledgment would be issued on incomplete application. Ø Application should be submitted to respective branch , and applicable processing charges should be deposited. …………………………………………………………………………………………………………………. THE BANK OF RAJASTHAN LTD. (Registered Office : C. T. Udaipur) Corporate Office : Mumbai _____________________________________________________________________________ (Acknowledgement ) B/o……………………………… Date …………………………… Received application from M/s …………………………………………………………………………. for considering sanction of credit facilities along with processing charges vide cash / cheque no ……..………dated…………for Rs…………………. Entered in proposal received register at Serial no ……………………..dated ………………. Branch Manager / Credit Manager / Officer 1 Please tick Check List of Enclosures to the application for credit facilities :- Ö (Yes / No) 1. Audited Financial Statements for last three Financial Years with Directors’ Report, Auditor’s Report, Schedules, and Notes to Accounts relating to Yes No applicant & group concerns. 2. CMA Report including Computation of Funded & Non Funded Limits, based on Last two years (actuals), current years estimates and projections of next year Yes No 3. Profile & Banking Arrangement of the Group Companies/Sister Concerns as per format Annexure-I Yes No 4. -

State Bank of India

State Bank of India State Bank of India Type Public Traded as NSE: SBIN BSE: 500112 LSE: SBID BSE SENSEX Constituent Industry Banking, financial services Founded 1 July 1955 Headquarters Mumbai, Maharashtra, India Area served Worldwide Key people Pratip Chaudhuri (Chairman) Products Credit cards, consumer banking, corporate banking,finance and insurance,investment banking, mortgage loans, private banking, wealth management Revenue US$ 36.950 billion (2011) Profit US$ 3.202 billion (2011) Total assets US$ 359.237 billion (2011 Total equity US$ 20.854 billion (2011) Owner(s) Government of India Employees 292,215 (2012)[1] Website www.sbi.co.in State Bank of India (SBI) is a multinational banking and financial services company based in India. It is a government-owned corporation with its headquarters in Mumbai, Maharashtra. As of December 2012, it had assets of US$501 billion and 15,003 branches, including 157 foreign offices, making it the largest banking and financial services company in India by assets.[2] The bank traces its ancestry to British India, through the Imperial Bank of India, to the founding in 1806 of the Bank of Calcutta, making it the oldest commercial bank in the Indian Subcontinent. Bank of Madras merged into the other two presidency banks—Bank of Calcutta and Bank of Bombay—to form the Imperial Bank of India, which in turn became the State Bank of India. Government of Indianationalised the Imperial Bank of India in 1955, with Reserve Bank of India taking a 60% stake, and renamed it the State Bank of India. In 2008, the government took over the stake held by the Reserve Bank of India. -

Impact of Bank Mergers on Efficiency of Banks in India

International Journal of Education, Modern Management, Applied Science & Social Science (IJEMMASSS) 180 ISSN : 2581-9925, Impact Factor: 5.143, Volume 02, No. 03, July - September, 2020, pp.180-184 IMPACT OF BANK MERGERS ON EFFICIENCY OF BANKS IN INDIA Parminderjeet Kaur Kitti ABSTRACT This paper utilizes the non-parametric frontier approach, Data Envelopment Analysis (DEA), to analyze the technical and scale efficiency of HDFC and SBI bank during the merger year, pre-and post- merger period. For this purpose secondary data was collected from the RBI database. It is found that HDFC and SBI banks exhibited a commendable efficiency level from 2005 to2018 and thereby improving governance in these banks. Our results suggest that the merger program was successful for both HDFC and SBI banks, which have benefited from the merger and acquisition via economies of scale and simultaneously improving governance in these banks. Keywords: Efficiency, Merger and Acquisitions, Governance, Data Envelopment Analysis. ________________ Introduction Merger and acquisition is a major tool for an expansion of business in different countries. The researchers all over the world are taking keen interest to work in this field (Goyal & Joshi.2011) Minimization of cost and good financial planning are needed for the expansion of business of banks. All these initiatives are possible with the help of mergers and acquisitions. The banking sector being largest growing sector and the soundness of the banking sector is the key principle for the development of the country’s economy. The banks adopt the merger and acquisitions to meet these changing scenarios in the banks. The paper aims to analyse the effects of mergers and acquisitions on the efficiency of the State Bank of India and HDFC banks. -

List of Unclaimed Dividend As on March 31, 2014 For

LIST OF UNCLAIMED DIVIDEND AS ON MARCH 31, 2014 FOR FINANCIAL YEAR 2006-07 DPID CO_FOLIO NAME LOCATION PIN BANK_ACC BANK_NM BEN_POS AMOUNT DIV_CAT MICR WARNO 35 KRISHNA SAHAI 600 450.00 3 42 17023 42 VINOD MALHOTRA 200 150.00 3 44 17024 81 NARENDRA GUPTA 208002 1000 750.00 3 62 17026 IN300239 11928248 RAYAMARAKKAR VEETTIL MOHAMMED ABDUL KADER 081010100345101 UTI BANK LTD 500 375.00 5 65 6337 IN303028 52416976 LAKSHMI SUNDAR CANADA M2H2K4 0 602601251547 I C I C I BANK 500 375.00 5 66 16691 IN303028 53312700 RAJIV KUMAR WADHWA 0 032601075085 I C I C I BANK 160 120.00 5 67 16773 IN303028 53152064 IPTHIKAR AHAMED KSA 11461 000401800418 I C I C I BANK 100 75.00 5 69 16765 IN302679 33533755 DIWAKAR KESHAV KAMATH CANADA-L5B4P5 111111 NRO020901075271 ICICI BANK LTD 104 78.00 5 73 15273 IN302902 41446558 KAMATH JAHANARA DIWAKAR CANADA-L5B4P5 111111 NRO020901075645 ICICI BANK LTD 104 78.00 5 74 15818 IN303028 50981646 STANLY JOHN 111111 004601076690 I C I C I BANK 1000 750.00 5 76 16549 IN300484 12487732 VASANT CHHEDA 111111 064010100122504 AXIS BANK LTD 10000 7500.00 5 78 8114 IN302902 41368936 MATSYA RAJ SINGH KUWAIT-913119 111111 628101076232 I C I C I BANK 100 75.00 5 79 15806 IN301549 16866066 SATISH GANGWANI 400832 0011060006675 HDFC BANK LTD TULSIANI 1300 975.00 5 80 12307 IN300888 14561256 SURBHI AGRAWAL MALAYSIA 504700 4034317 SYNDICATE BANK 2600 1950.00 5 81 9833 IN301549 18385836 PADMAJA UPPALAPATI SOUTH AFRICA 999999 0041060014403 HDFC BANK LTD ITC CENTRE 200 150.00 5 82 12420 IN303028 51253550 ISMAIL MOHAMED GHOUSE 999999 000401473103 -

S. No. Regional Office Party/Payee Name Individual

AGRICULTURE INSURANCE COMPANY OF INDIA LTD. STATEMENT OF STALE CHEQUES As on 30.09.2017 Unclaimed amount of Policyholders related to Stale Cheques more than Rs. 1000/- TYPE OF PAYMENT- REGIONAL INDIVIDUAL/ FINANCIAL AMOUNT (IN S. NO. PARTY/PAYEE NAME ADDRESS CLAIMS/ EXCESS SCHEME SEASON OFFICE INSTITUTION RS.) COLLECTION (a) (b) (c) (d) (e) (i) (j) (k) (l) (m) 1 AHMEDABAD BANK OF BARODA, GODHARA FINANCIAL INSTITUTION STATION ROAD ,GODHARA 2110.00 EXCESS COLLECTION NAIS KHARIF 2006 2 AHMEDABAD STATE BANK OF INDIA, NADIAD FINANCIAL INSTITUTION PIJ ROAD,NADIAD 1439.70 EXCESS COLLECTION NAIS KHARIF 2006 3 AHMEDABAD STATE BANK OF INDIA (SBS),JUNAGADH FINANCIAL INSTITUTION CIRCLE CHOWK,JUNAGADH 1056.00 EXCESS COLLECTION NAIS KHARIF 2007 4 AHMEDABAD UNION BANK OF INDIA, NADIAD FINANCIAL INSTITUTION TOWER,DIST.KHEDA,NADIAD 1095.50 EXCESS COLLECTION NAIS KHARIF 2007 5 AHMEDABAD BANK OF BARODA, MEHSANA FINANCIAL INSTITUTION STATION ROAD,MEHSANA 1273.80 EXCESS COLLECTION NAIS KHARIF 2008 PATNAGAR YOJANA 6 AHMEDABAD BANK OF INDIA, GANDHINAGAR FINANCIAL INSTITUTION 13641.60 EXCESS COLLECTION NAIS KHARIF 2008 BHAVAN,GHANDHINAGAR 7 AHMEDABAD ORIENTAL BANK OF COMMERCE, UNJHA FINANCIAL INSTITUTION DIST.MEHSANA,UNJA 16074.00 EXCESS COLLECTION NAIS KHARIF 2008 OTHERS 8 AHMEDABAD NAJABHAI DHARAMSIBHAI SAKARIYA INDIVIDUAL DHANDHALPUR, CHOTILA 1250.00 CLAIMS KHARIF 2009 PRODUCTS OTHERS 9 AHMEDABAD TIGABHAI MAVJIBHAI INDIVIDUAL PALIYALI, TALAJA, BHAVNAGAR 1525.00 CLAIMS KHARIF 2009 PRODUCTS OTHERS 10 AHMEDABAD REMATIBEN JEHARIYABHAI VASAVA INDIVIDUAL SAGBARA, -

Customer Attitude on Service Quality of Private Banks in Tiruchirappalli

26326 R.Karthi et al./ Elixir Marketing Mgmt. 73 (2014) 26326-26329 Available online at www.elixirpublishers.com (Elixir International Journal) Marketing Management Elixir Marketing Mgmt. 73 (2014) 26326-26329 Customer Attitude on Service Quality of Private Banks in Tiruchirappalli R.Karthi *, B.Asha Daisy and M.Ganga E.G.S.Pillay Engineering College Nagapattinam, Tamilnadu, India. ARTICLE INFO ABSTRACT Article history: Marketing in today’s world is so difficult for existing players and the new entrants due to Received: 10 June 2014; the fast growing, changes in the customer preference and tastes, rapid growth of Received in revised form: technology, penetration of foreign players in the local market, price sensitiveness of 25 July 2014; customers and quality consciousness of government for attracting, acquiring, retaining Accepted: 9 August 2014; customers in the business. To identify the attitude of the customer in the banking sector, a study has been made in the Tiruchirappalli region among private bank. Keywords © 2014 Elixir All rights reserved. Customer Attitude, Service Quality, Private Banks. Introduction Reserve bank of India (RBI) came in picture in 1935 and Retail banking Industry is growing rapidly in a fast and study became the centre of every other bank taking away all the phase to acquire and retain the customers. To face the global responsibilities and functions of Imperial bank. Between 1969 competition the private banks are taking innumerable steps to and 1980 there was rapid increase in the number of branches of defend their business in order to maximize their potential the private banks. In April 1980, they accounted for nearly 17.5 business. -

List of Indian Public Sector Banks :- (Click to Visit the Website of the Bank)

List of Banks in India - 2014 Directory of Public Sector / Private Sector / Foreign Banks List of Indian Public Sector Banks :- (Click to visit the website of the Bank) Nationalized Banks, State Bank Group Banks have been included here as PS Banks : Allahabad Bank Andhra Bank Bank of Baroda Bank of India Bank of Maharashtra Canara Bank Central Bank of India Corporation Bank Dena Bank IDBI Bank Limited Indian Bank Indian Overseas Bank IDBI Bank Industrial Development Bank of India Oriental Bank of Commerce Punjab & Sind Bank Punjab National Bank State Bank of Bikaner and Jaipur State Bank of Hyderabad State Bank of India State Bank of Mysore State Bank of Patiala State Bank of Travancore Syndicate Bank UCO Bank Union Bank of India United Bank Of India Vijaya Bank (a) The following two State Bank Group Banks have since been merged with SBI) State Bank of Indore (since merged with SBI) State Bank of Saurashtra (since merged with SBI) ( b) New Bank of India (a nationalised bank) was merged with Punjab National Bank in 1993 List of Private Sector Banks in India Ads by Google Axis Bank Catholic Syrian Bank Ltd. IndusInd Bank Limited ICICI Bank ING Vysya Bank Kotak Mahindra Bank Limited Karnataka Bank Karur Vysya Bank Limited. Tamilnad Mercantile Bank Ltd. The Dhanalakshmi Bank Limited. The Federal Bank Ltd. The HDFC Bank Ltd. The Jammu & Kashmir Bank Ltd. The Nainital Bank Ltd. The Lakshmi Vilas Bank Ltd Yes Bank copied from www,allbankingsolutions.com List of Private Sector Banks Since Merged with other banks The Nedungadi Bank (merged with -

Introduction Banking in India

Introduction Banking in India Banking in India originated in the last decades of the 18th century. The first banks were The General Bank of India which started in 1786, and the Bank of Hindustan, both of which are now defunct. The oldest bank in existence in India is the State Bank of India, which originated in the Bank of Calcutta in June 1806, which almost immediately became the Bank of Bengal. This was one of the three presidency banks, the other two being the Bank of Bombay and the Bank of Madras, all three of which were established under charters from the British East India Company. For many years the Presidency banks acted as quasi-central banks, as did their successors. The three banks merged in 1921 to form the Imperial Bank of India, which, upon India’s Independence became the State Bank of India. Origin of Banking in India Indian merchants in Calcutta established the Union Bank in 1839, but it failed in 1848 as a consequence of the economic crisis of 1848-49. The Allahabad Bank, established in 1865 and still functioning today, is the oldest Joint Stock bank in India. (Joint Stock Bank: A company that issues stock and requires shareholders to be held liable for the company’s debt) It was not the first though. That honor belongs to the Bank of Upper India, which was established in 1863, and which survived until 1913, when it failed, with some of its assets and liabilities being transferred to the Alliance Bank of Simla. When the American Civil War stopped the supply of cotton to Lancashire from the Confederate States, promoters opened banks to finance trading in Indian cotton. -

Is a 7 Digit Unique Number Issued by the Bank. What Are the Last Three

Mobile Money Identifier (MMID) is a 7 digit unique number issued by the bank. What are the last three digits represent? 1) to identify the account of the user 2) to identify the branch of the user 3) to identify the bank of the user 4) All of the above three 5) None of these Answer: to identify the account of the user What does the last character represent in PAN CARD? 1) type of holder 2) Surname of holder 3) Check digit 4) All of the above three 5) None of these Answer: Check digit What does I stands for, in PPI? 1) Instruments 2) Investment 3) Income 4) India 5) None of these Answer: Instruments Which of the below facility cannot be provided by Payment Banks? 1) ATM Card 2) Debit Card 3) Net banking 4) Mobile banking 5) Credit Card Answer: Credit Card Aapka Bank Aapke Dwar is a tagline of __________. 1) Airtel Payments Bank Limited 2) India Post Payments Bank Limited 3) Paytm Payments Bank Limited 4) Fino Payments Bank Limited 5) Vodafone M-Pesa Answer: India Post Payments Bank Limited Where is the headquarters of Paytm Payments Bank Limited? 1) Noida 2) New Delhi 3) Haryana 4) Lucknow 5) Varanasi Answer: Noida The headquarters of Equitas Small Finance Bank is _______________. 1) Guwahati 2) Thrissur 3) Coimbatore 4) Varanasi 5) Chennai Answer: Chennai Headquarters of Fino Payments Bank Limited is __________. 1) Kochi 2) New Delhi 3) Bangalore 4) Mangalore 5) Mumbai Answer: Mumbai Ho much % of FDI is allowed for Payment Banks in India? 1) 49% 2) 20% 3) 74% 4) 100% 5) 51% Answer: 74% Headquarters of FINCARE Small Finance Bank Limited is at? 1) Ahmedabad 2) Kochi 3) Mumbai 4) Bengaluru 5) Lucknow Answer: Bengaluru Loans to individuals up to ______ in metropolitan centres (with the population of ten lakh and above) under priority sector. -

A Study on Customer Satisfaction of Bharat Interface for Money (BHIM)

International Journal of Innovative Technology and Exploring Engineering (IJITEE) ISSN: 2278-3075, Volume-8 Issue-6, April 2019 A Study on Customer Satisfaction of Bharat Interface for Money (BHIM) Anjali R, Suresh A Abstract: After demonetization on November 8th, 2016, India saw an increased use of different internet payment systems for Mobile banking saw its growth during the period of 2009- money transfer through various devices. NPCI (National 2010 with improvement in mobile internet services across Payments Corporation India) launched Bharat interface for India. SMS based applications along with mobile Money (BHIM) an application run on UPI (Unified Payment application compatible with smartphones offered improved Interface) in December 2016 to cater the growing online payment banking services to the customers. Apart from the bank’s needs. The different modes of digital payments saw a drastic mobile applications other applications like BHIM, Paytm, change in usage in the last 2 years. Though technological Tez etc. offered provided enhanced features that lead to easy innovations brought in efficiency and security in transactions, access to banking services. In addition to this, The Reserve many are still unwilling to adopt and use it. Earlier studies Bank of India has given approval to 80 Banks to start mobile related to adoption, importance of internet banking and payment systems attributed it to some factors which are linked to security, banking services including applications. Bharat Interface for ease of use and satisfaction level of customers. The purpose of money (BHIM) was launched after demonetization by this study is to unfold some factors which have an influence on National Payments Corporation (NPCI) by Prime Minister the customer satisfaction of BHIM application.