Heavy Crude Oil: a Global Analysis and Outlook to 2035 2011

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Madagascar's Extractive Industries Poised for Big Leap Forward

Madagascar’s extractive industries poised for big leap forward Report produced by The Energy Exchange www.theenergyexchange.co.uk 2 Contents page 3 Foreword 4 Executive summary 5 Madagascar Country profile 6 The political and economic environment 7 Madagascar’s mining potential 8 Madagascar’s hydrocarbon potential 9 Exploration is everywhere 10 Strengths, weaknesses, opportunities and threats 11 Conclusion 12 About The Energy Exchange 13 From the people who brought you... www.theenergyexchange.co.uk 3 Foreword The last frontier of the last frontier Following presidential and parliamentary elections held in late 2013, the situation in Madagascar is returning to normal after five years of internal socio-political crisis following the coup. The government is now keen to exploit the abundant and diversified natural resources and use them to carry out major structural changes in the economy. We have created a report to enable you to understand the potential of the extractive industries in the last frontier of Africa. This report includes: • An analysis of the current economic and political environment in the country • An overview of the mineral and hydrocarbon potential • A SWOT analysis of Madagascar as an investment destination The Energy Exchange is committed to creating high quality, strategic and technical conferences across the globe. We also recognise your need for pioneering industry content throughout the year. Enjoy the report, and please do get in touch with any feedback or questions. Best regards, Hannah Wharrier Managing Director, The Energy Exchange Telephone: +44 (0)20 7384 8030 Email: [email protected] www.theenergyexchange.co.uk 4 Executive summary The inauguration of Madagascar’s President Hery Rajaonarimampianina International support for the country is growing and foreign direct investment on 25 January 2014, and his pledge to open up his country to foreign (FDI) inflow this year is put at $837.5 million. -

Madagascar: the New Eldorado for Mining and Oil Companies

Madagascar: The New Eldorado for Mining and Oil Companies Researched and written by: Association IRESA (Initiative pour la Recherche Economique et Sociale en Afrique Edited by: Juliette Renaud, Darek Urbaniak, Viviana Varin, Holly Rakotondralambo Published by Friends of the Earth France and Friends of the Earth Europe The full version of this report is available in French language at: www.amisdelaterre.org/rapportmadagascar This Report has been produced with the financial assistance of the European Union in the context of the Making Extractive Industry Work for Climate and Development project. The content of this report is the sole responsibility of Friends of the Earth Europe, Friends of the Earth Netherlands, Friends of the Earth France and CEE Bankwatch, and can under no circumstances be regarded as reflecting the position of the European Union. 2 INTRODUCTION Current production and consumption habits in the countries of the Global North are leading to over- consumption of resources such as oil, minerals, water and wood. This has resulted in low-cost access to raw materials becoming the priority for states and multinational corporations that wish to meet this growing demand. This frenetic race to gain access to raw materials is leading to an increase in the extractive industry’s projects, continually pushing the boundaries of the acceptable to new heights. These demands are being met at the expense of the environment and local communities, essentially in the countries of the Global South, which is where most of these resources are located. What is going on is nothing less than plundering and, for local communities, the extractive industries are often synonymous with destruction and contamination of their environment and livelihoods. -

Impacts and Mitigations of in Situ Bitumen Production from Alberta Oil Sands

Impacts and Mitigations of In Situ Bitumen Production from Alberta Oil Sands Neil Edmunds, P.Eng. V.P. Enhanced Oil Recovery Laricina Energy Ltd. Calgary, Alberta Submission to the XXIst World Energy Congress Montréal 2010 - 1 - Introduction: In Situ is the Future of Oil Sands The currently recognized recoverable resource in Alberta’s oil sands is 174 billion barrels, second largest in the world. Of this, about 150 billion bbls, or 85%, is too deep to mine and must be recovered by in situ methods, i.e. from drill holes. This estimate does not include any contributions from the Grosmont carbonate platform, or other reservoirs that are now at the early stages of development. Considering these additions, together with foreseeable technological advances, the ultimate resource potential is probably some 50% higher, perhaps 315 billion bbls. Commercial in situ bitumen recovery was made possible in the 1980's and '90s by the development in Alberta, of the Steam Assisted Gravity Drainage (SAGD) process. SAGD employs surface facilities very similar to steamflooding technology developed in California in the ’50’s and 60’s, but differs significantly in terms of the well count, geometry and reservoir flow. Conventional steamflooding employs vertical wells and is based on the idea of pushing the oil from one well to another. SAGD uses closely spaced pairs of horizontal wells, and effectively creates a melt cavity in the reservoir, from which mobilized bitumen can be collected at the bottom well. Figure 1. Schematic of a SAGD Well Pair (courtesy Cenovus) Economically and environmentally, SAGD is a major advance compared to California-style steam processes: it uses about 30% less steam (hence water and emissions) for the same oil recovery; it recovers more of the oil in place; and its surface impact is modest. -

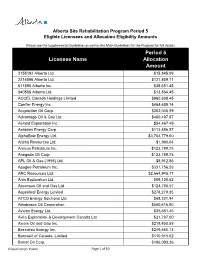

Alberta Site Rehabilitation Program Period 5 Eligible Licensees and Allocation Eligibility Amounts

Alberta Site Rehabilitation Program Period 5 Eligible Licensees and Allocation Eligibility Amounts Please see the Supplemental Guidelines as well as the Main Guidelines for the Program for full details Period 5 Licensee Name Allocation Amount 2155192 Alberta Ltd. $15,845.09 2214896 Alberta Ltd. $121,809.11 611890 Alberta Inc. $35,651.45 840586 Alberta Ltd. $13,864.45 ACCEL Canada Holdings Limited $960,608.45 Conifer Energy Inc. $464,459.14 Acquisition Oil Corp. $302,046.99 Advantage Oil & Gas Ltd. $460,497.87 Aeneid Exploration Inc. $54,467.49 Aeraden Energy Corp. $113,886.57 AlphaBow Energy Ltd. $3,704,779.60 Altima Resources Ltd. $1,980.64 Amicus Petroleum Inc. $123,789.75 Anegada Oil Corp. $123,789.75 APL Oil & Gas (1998) Ltd. $8,912.86 Apogee Petroleum Inc. $331,756.53 ARC Resources Ltd. $2,664,945.71 Artis Exploration Ltd. $89,128.62 Ascensun Oil and Gas Ltd. $124,780.07 Aspenleaf Energy Limited $278,279.35 ATCO Energy Solutions Ltd. $68,331.94 Athabasca Oil Corporation $550,616.80 Avalon Energy Ltd. $35,651.45 Avila Exploration & Development Canada Ltd $21,787.00 Axiom Oil and Gas Inc. $219,850.59 Baccalieu Energy Inc. $249,560.13 Barnwell of Canada, Limited $110,915.62 Barrel Oil Corp. $196,083.36 #Classification: Public Page 1 of 10 Alberta Site Rehabilitation Program Period 5 Eligible Licensees and Allocation Eligibility Amounts Please see the Supplemental Guidelines as well as the Main Guidelines for the Program for full details Period 5 Licensee Name Allocation Amount Battle River Energy Ltd. -

2010 Annual Report

2010 Annual Report MISSION Our mission is to facilitate innovation, collaborative research and technology development, demonstration and deployment for a responsible Canadian hydrocarbon energy industry. VISION Our vision is to help Canada become a global hydrocarbon energy technology leader. Contact Us For further information please contact: PTAC Petroleum Technology Alliance Canada Suite 400, Chevron Plaza, 500 Fifth Avenue SW, Calgary, Alberta, Canada T2P 3L5 MAIN: 403-218-7700 FAX: 403-920-0054 EMAIL: [email protected] WEB SITE: www.ptac.org PERSONNEL SOHEIL ASGARPOUR BRENDA BELLAND SUSIE DWYER LORIE FREI MARC GODIN President Manager, Knowledge Centre Innovation and Technology R&D Initiatives Assistant and Technical Advisor (403) 218-7701 (403) 218-7712 Development Web Site (403) 870-5402 [email protected] [email protected] Coordinator Administrator marc.godin@portfi re.com (403) 218-7708 (403) 218-7707 [email protected] [email protected] ARLENE MERLING TRUDY HIGH BOBBI SINGH LAURA SMITH TANNIS SUCH Director, Operations Administrative and Registration Accountant Controller Manager, Environmental (403) 218-7702 Coordinator (403) 218-7723 (403) 218-7701 Research [email protected] (403) 218-7711 [email protected] [email protected] Initiatives [email protected] (403) 218-7703 [email protected] PETROLEUM TECHNOLOGY ALLIANCE CANADA 2010 ANNUAL REPORT 3 Message from the Board A New Decade – A New Direction 2010 proved to be a turning point for PTAC as we redeined our role and PTAC Technology Areas set new strategies in motion. Over the past year PTAC has achieved goals in diverse areas of our organization: improving our inances, rebalancing our MANAGE ENVIRONMENTAL IMPACTS project portfolios to address a broad spectrum of needs, leveraging support • Emission Reduction / Eco-eficiency for ield implementations, and building a measurably more effective and • Energy Eficiency eficient organization. -

World Bank Document

Document of The WorldBank C: FOR OFFICIAL USE ONLY Public Disclosure Authorized /129&-MR C- ReportNo. P-3204-MAG REPORT AND RECOMMENDATION OF THE PRESIDENT OF THE Public Disclosure Authorized INTERNATIONALDEVELOPMENT ASSOCIATION TO THE EXECUTIVEDIRECTORS ON A PROPOSED CREDIT IN AN AMOUNT EQUIVALENT TO US$11.5 MILLION TO THE Public Disclosure Authorized DEMOCRATIC REPUBLIC OF MADAGASCAR FOR THE TSIMIROROHEAVY OIL EXPLORATIONPROJECT October 20, 1982 Public Disclosure Authorized This documenthas a restricteddistribution and may be used by recipientsonly in the performuaceof I their official duties. Its contentsmay not otherwise be disclosed without World Bank authorization. CURRENCY EQUIVALENTS December 1981 June 1982 Unit = Malagasy Franc (FMG) = Malagasy Franc (FMG) US$1.00 = FMG 278 = FMG 375 FMG 1,000 = US$3.59 - US$2.67 FMG 1,000,000 = US$3,590 = US$2,670 (The cost estimates are based on US$1 = FMG 375) WEIGHTS AND MEASURES GWh = Gigawatt hour kWh = kilowatt hour MW = Megawatt RD = Barrels per day GLOSSARY OF ABBREVIATIONS OMNIS - Office Militaire National pour les Industries Strategiques EIB - European Investment Bank GOVERNMENT OF MADAGASCAR FISCAL YEAR January 1 to December 31 FOR OFFICIALUSE ONLY MADAGASCAR TSIMIRORO HEAVY OIL EXPLORATION PROJECT CREDIT AND PROJECT SUMMARY Borrower: Democratic Republic of Madagascar Beneficiary: Office Militaire National pour les Industries Strategiques (OMNIS) t Amount: SDR 10.7 million (US$11.5 million equivalent) Terms: Standard Onlending Terms: The Government would make the proceeds of the credit available to OMNIS as a grant. Project Description: (i) Objective: The project would support the Government's efforts to evaluate the country's hydrocarbon potential with the objective of realizing domestic oil production in the future. -

Emerging Oil Sands Producers

RBC Dominion Securities Inc. Emerging Oil Sands Producers Mark Friesen (Analyst) (403) 299-2389 Initiating Coverage: The Oil Sands Manifesto [email protected] Sam Roach (Associate) Investment Summary & Thesis (403) 299-5045 We initiate coverage of six emerging oil sands focused companies. We are bullish with [email protected] respect to the oil sands sector and selectively within this peer group of new players. We see decades of growth in the oil sands sector, much of which is in the control of the emerging companies. Our target prices are based on Net Asset Value (NAV), which are based on a long-term flat oil price assumption of US$85.00/bbl WTI. The primary support for our December 13, 2010 valuations and our recommendations is our view of each management team’s ability to execute projects. This report is priced as of market close December 9, 2010 ET. We believe that emerging oil sands companies are an attractive investment opportunity in the near, medium and longer term, but investors must selectively choose the All values are in Canadian dollars companies with the best assets and greatest likelihood of project execution. unless otherwise noted. For Required Non-U.S. Analyst and Investment Highlights Conflicts Disclosures, please see • page 198. MEG Energy is our favourite stock, which we have rated as Outperform, Above Average Risk. We have also assigned an Outperform rating to Ivanhoe Energy (Speculative Risk). • We have rated Athabasca Oil Sands and Connacher Oil & Gas both as Sector Perform, (Above Average Risk). We have also assigned a Sector Perform rating to SilverBirch Energy (Speculative Risk). -

Emerging East Africa Energy Overview

‹ Countries Emerging East Africa Energy Last Updated: May 23, 2013 (Notes) full report Overview Emerging oil and gas developments in East Africa Although oil and natural gas exploration has been going on for decades in various East African countries, there has been limited success until recently. In the past there were doubts about the amount of recoverable resources in the region, along with regional and civil conflicts that presented challenges and risks to foreign companies. Consequently, exploration activities in East Africa have evolved at a much slower pace relative to other African regions. However, the pace of exploration activity has recently picked up after foreign oil and gas companies made a series of sizable discoveries in several East African countries. This new regional analysis covers emerging developments in the oil and gas sectors in five East African countries: Mozambique, Tanzania, Uganda, Kenya, and Madagascar. The larger area that EIA considers as East Africa (see Africa by region map) includes 21 countries. In this region, almost all of the oil production comes from Sudan and South Sudan, which are not covered in this report because they are mature oil producers. Among the countries with emerging oil and gas developments, Mozambique, Tanzania, Uganda, and Madagascar have shown the most progress toward commercial development of newly discovered resources in recent years. Uganda and Madagascar will most likely be the next new oil producers on the continent. Mozambique will probably be the first country in East Africa to develop the capability to export liquefied natural gas (LNG), possibly followed by Tanzania. Although progress toward commercial development of hydrocarbon resources in Kenya has been modest, the country plays a vital role in the region as an oil transit hub, particularly for oil products coming into the region. -

Notice of Applications Connacher Oil and Gas Limited Great Divide Expansion Project Athabasca Oil Sands Area

NOTICE OF APPLICATIONS CONNACHER OIL AND GAS LIMITED GREAT DIVIDE EXPANSION PROJECT ATHABASCA OIL SANDS AREA ENERGY RESOURCES CONSERVATION BOARD APPLICATION NO. 1650859 ALBERTA ENVIRONMENT ENVIRONMENTAL PROTECTION AND ENHANCEMENT ACT APPLICATION NO. 003-240008 WATER ACT FILE NO. 00271543 ENVIRONMENTAL IMPACT ASSESSMENT The Energy Resources Conservation Board (ERCB/Board) has received Application No. 1650859 and Alberta Environment (AENV) has received Environmental Protection and Enhancement Act (EPEA) Application No. 003-240008 and Water Act File No. 00271543 from Connacher Oil and Gas Limited (Connacher) for approval of the proposed Great Divide Expansion Project (the Project). This notice is to advise interested parties that the applications are available for viewing and that the ERCB, AENV, and other government departments are now undertaking a review of the applications and associated environmental impact assessment (EIA). Description of the Project Connacher has applied to construct, operate, and reclaim an in-situ oil sands project about 70 kilometres (km) south of the City of Fort McMurray in Townships 81, 82, and 83, Ranges 11 and 12, West of the 4th Meridian. Construction of the Project is proposed to begin in 2011, with increased production starting by 2012. The proposed Project would amalgamate Connacher’s existing Great Divide (EPEA Approval No. 223216-00-00) and Algar (EPEA Approval No. 240008-00-00) projects which were each designed to produce 1600 cubic metres per day (m3/day) (10 000 barrels per day [bbl/d]) of bitumen. The proposed Project would also increase Connacher’s bitumen production capacity to 7000 m3/day (44 000 bbl/d) at peak production using the in situ steam assisted gravity drainage (SADG) thermal recovery process. -

Alberta Oil Sands Quarterly Update Fall 2013

ALBERTA OIL SANDS INDUSTRY QUARTERLY UPDATE FALL 2013 Reporting on the period: June 18, 2013, to Sep. 17, 2013 2 ALBERTA OIL SANDS INDUSTRY QUARTERLY UPDATE Canada has the third-largest oil methods. Alberta will continue to rely reserves in the world, after Saudi to a greater extent on in situ production Arabia and Venezuela. Of Canada’s in the future, as 80 per cent of the 173 billion barrels of oil reserves, province’s proven bitumen reserves are 170 billion barrels are located in too deep underground to recover using All about Alberta, and about 168 billion barrels mining methods. are recoverable from bitumen. There are essentially two commercial This is a resource that has been methods of in situ (Latin for “in the oil sands developed for decades but is now place,” essentially meaning wells are gaining increased global attention Background of an used rather than trucks and shovels). as conventional supplies—so-called In cyclic steam stimulation (CSS), important global resource “easy” oil—continue to be depleted. high-pressure steam is injected into The figure of 168 billion barrels directional wells drilled from pads of bitumen represents what is for a period of time, then the steam considered economically recoverable is left to soak in the reservoir for a with today’s technology, but with period, melting the bitumen, and new technologies, this reserve then the same wells are switched estimate could be significantly into production mode, bringing the increased. In fact, total oil sands bitumen to the surface. reserves in place are estimated at 1.8 trillion barrels. -

Alberta Oil Sands Industry Quarterly Update

ALBERTA OIL SANDS INDUSTRY QUARTERLY UPDATE WINTER 2013 Reporting on the period: Sep. 18, 2013 to Dec. 05, 2013 2 ALBERTA OIL SANDS INDUSTRY QUARTERLY UPDATE Canada has the third-largest oil methods. Alberta will continue to rely All about reserves in the world, after Saudi to a greater extent on in situ production Arabia and Venezuela. Of Canada’s in the future, as 80 per cent of the 173 billion barrels of oil reserves, province’s proven bitumen reserves are the oil sands 170 billion barrels are located in too deep underground to recover using Background of an Alberta, and about 168 billion barrels mining methods. are recoverable from bitumen. There are essentially two commercial important global resource This is a resource that has been methods of in situ (Latin for “in developed for decades but is now place,” essentially meaning wells are gaining increased global attention used rather than trucks and shovels). as conventional supplies—so-called In cyclic steam stimulation (CSS), “easy” oil—continue to be depleted. high-pressure steam is injected into The figure of 168 billion barrels TABLE OF CONTENTS directional wells drilled from pads of bitumen represents what is for a period of time, then the steam considered economically recoverable is left to soak in the reservoir for a All about the oil sands with today’s technology, but with period, melting the bitumen, and 02 new technologies, this reserve then the same wells are switched estimate could be significantly into production mode, bringing the increased. In fact, total oil sands Mapping the oil sands bitumen to the surface. -

Madagascar Mining

www.global-insight.net MADAGASCAR GLOBAL INSIGHT MADAGASCAR The ambitious island nation is capitalizing on its precious natural resources and enviable strategic location The giant of the Indian Ocean takes major strides From rare minerals to cash crops, Madagascar is making the most of make it more affordable to the Malagasy. We are looking for its national treasures to offer international investors rich rewards investors and many have already come and reached out to us.” The giant of the Indian Ocean, With four large hydroelectric Madagascar’s ambitious national projects and two solar energy ini- development plan is gathering tiatives, officials have earmarked pace as government reforms significant investment in infra- Dudarev Mikhail-Shutterstock PHOTO: boost economic growth, improve structure that will be supported the investment climate and by dozens of rural electrification increase returns on its abundant projects. natural resources. Democratic elections in 2013 Energizing the economy created long-awaited political Spearheading this invest- stability that has been a catalyst ment drive and modernization for solid fiscal progress, regional program is the Ministry of integration and generated a Energy and Hydrocarbons, myriad of investment opportuni- Hery Rajaonarimampianina Olivier Mahafaly Solonandrasana where officials understand the ties throughout all sectors of the President Prime Minister importance of having foreign economy. partners — such as Panasonic Strategically located close able energy and transport — that investor in the biggest mining — to develop such important to the crossroads of three con- will help eradicate poverty. project in Madagascar and the projects. tinents and key international “Madagascar has a strate- wider region — the Ambatovy “Our energy sector has a legal shipping lanes, the world’s gic location right in between project for nickel and cobalt.