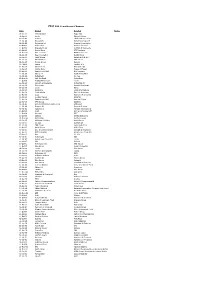

CBIS Global Funds Plc an Umbrella Fund with Segregated Liability Between Sub-Funds

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Engineering That Moves the World Highlights of the Year Delivering on Expectations

Annual Report and Accounts 2016 Engineering that moves the world Highlights of the year Delivering on expectations ◆ Another year of growth delivering earnings ◆ Sharpening the focus through the disposal of Stromag momentum. and a Group-wide fixed cost reduction programme. ◆ Strong performance from Fokker Technologies ◆ Continued investment in technology primarily focused (‘Fokker’) in first full year of ownership. on electrified drivetrains and additive manufacturing. STATUTORY BASIS MANAGEMENT BASIS1 Sales Sales £8,822m 2015: £7,231m £9,414m 201 5: £ 7,6 89m Earnings per share Earnings per share 14.1p 2015: 11.8p 31.0p 201 5: 27.8p Profit before tax Profit before tax £292m 2015: £245m £678m 2015: £603m Management sales Management trading profit £9,414m £773m2 Other Businesses £39m GKN Land Systems £18m GKN Land Systems GKN Powder Metallurgy £118m £704m GKN Aerospace £3,423m GKN Powder GKN Aerospace Metallurgy £339m £1,032m GKN Driveline £323m GKN Driveline £4,216m 1 See page 39 for details on measurement and reporting of performance on a management basis. 2 Including corporate costs and Other Businesses. Contents Strategic report Governance Financial statements 1 Overview 60 Board of Directors 111 Independent auditor’s report 12 Chairman’s statement 62 Chairman’s introduction to governance 118 Group financial statements 14 Our strategic framework 63 Corporate governance 167 Company financial statements 15 Our business model 72 Nominations Committee report 176 Group financial record 16 Key performance indicators 74 Audit & Risk Committee report 19 Chief Executive’s review 81 Directors’ remuneration report Other information 22 Financial review 107 Additional information 178 Shareholder information 24 Divisional reviews 110 Statement of Directors’ responsibilities 24 – GKN Aerospace review Pages 60 to 110 comprise the Directors’ report. -

Completed Acquisition of Two Vauxhall Dealerships from Riders' Garages Limited by Eden

Completed acquisition of two Vauxhall dealerships from Riders’ Garages Limited by Eden (GM) Limited ME/6474-14 The CMA’s decision on reference under section 22(1) on 24 October 2014. Full text of the decision published on 17 November 2014. Please note that [] indicates figures or text which have been deleted or replaced in ranges at the request of the parties for reasons of commercial confidentiality. Summary 1. Eden (GM) Limited (Eden) operates Vauxhall franchised car dealerships. Its two Devon dealerships, Exeter and Honiton, supply new and used Vauxhall cars to private customers as well as repair and maintenance services to Vauxhall cars. 2. Eden acquired two Vauxhall dealerships in Newton Abbot and Torbay (the Riders dealerships) from Riders Garages Limited (Riders) (the Merger). The Riders dealerships supply new and used Vauxhall cars to private customers and repair and maintenance services to Vauxhall cars. Eden and the Riders dealerships together are referred to in this decision as the Parties. 3. The Competition and Markets Authority (CMA) considers that the Parties are enterprises that as a result of the Merger have ceased to be distinct and that the share of supply test is met. The CMA therefore believes that it is or may be the case that a relevant merger situation has been created. 4. Eden and the Riders dealerships overlap in the supply of new and used Vauxhall cars and the supply of repair and maintenance services for Vauxhall cars in the Exeter, Newton Abbot and Torbay areas. 5. In relation to the supply of new and used Vauxhall cars, the CMA does not consider there to be competition concerns based on the constraints faced by the Parties locally from dealerships of other car marques including other sellers of used cars (both Vauxhall and others). -

Fidelity Special Values Plc 31 August 2021

ret.en.xx.20210831.GB00BWXC7Y93.pdf FIDELITY INVESTMENT TRUSTS MONTHLY FACTSHEET FIDELITY SPECIAL VALUES PLC 31 AUGUST 2021 Investment Objective Portfolio Manager Commentary To achieve long term capital growth primarily through investment in UK equities recorded a seventh straight monthly gain in August. equities (and their related securities) of UK companies which the Sentiment remained buoyant, propelled by M&A activity, alongside Investment Manager believes to be undervalued or where the expectations for continued earnings strength. potential has not been recognised by the market It is encouraging to see the underlying stock picking coming through despite the recent underperformance of value stocks. This is partly down to the Trust benefiting from a number of M&A bids, Investment Trust Facts the latest being Meggitt, but is also a reflection of improving corporate fundamentals. Launch date: 17.11.94 Portfolio manager: Alex Wright, Jonathan Winton UK equities remain significantly undervalued compared to global 01.09.12, 03.02.20 markets, and reasonably valued in absolute terms on 13x 2022 Appointed to trust: estimates. While the UK market has looked cheap over the past Years at Fidelity: 20, 16 five years, the key differentiator in 2021 is that fundamentals on the Total Net Assets (TNA): £ 954m ground look very good. UK stocks are well positioned not only to Ordinary shares in Issue: 313,028,920 benefit from a recovery from the COVID pandemic, but also from Share price: 308.50p the lifting of the Brexit uncertainty. 304.79p NAV: We remain comfortable with how the portfolio looks from a Premium 1.22% valuations, returns on capital and risk perspective, and continue to Gross Market Gearing: 14.6% see meaningful upside potential for our holdings. -

Top 50 Leasing Companies

ANALYSIS: TOP 50 LEASING COMPANIES The top 50 leasing companies and their on-risk size of fleet (the number of cars for which the lease firm carries the RV risk) Company Change 2012 2011 Boss Parent company Contact from ’11 ▼ 1. Lex Autolease ▲ 268,240 280,218 Rick Francis Lloyds 0800 389 3690 www.lexautolease.co.uk ▼ 2. Leaseplan ▲ 134,115 130,200 David Brennan Leaseplan Corporation 0844 493 5810 www.leaseplan.co.uk 3. Alphabet ▲ 3 109,236 50,396 Richard Schooling BMW AG 0870 505 0100 www.alphabet.co.uk 4. Arval ▼ 1 85,612 86,932 Bart Beckers BNP Paribas 01793 887000 www.arval.co.uk ▼ 5. ALD ▲ 80,331 63,561 Keith Allen Societe Generale 0870 001 1181 www.aldautomotive.co.uk 6. Volkswagen Group ▲ 1 59,936 49,437 Graham Wheeler Volkswagen Financial 0870 333 2229 Leasing Services www.volkswagengroupleasing.co.uk 7. Arnold Clark ▲ 4 49,483 42,019* Hugh Wallace Arnold Clark Automobiles 01413 322626 www.acvm.co.uk 8. GE Capital ▲ 2 43,685 43,495 John Jenkins GE (General Electric) 0870 444 9020 www.gecapital.co.uk/fleet 9. BT Fleet ▲ 5 32,150 33,083 David Bowen BT Group 0800 032 0012 www.btfleet.com 10. Hitachi Capital ▲ 3 28,889 34,065 Robert Wastell Hitachi Ltd 0844 463 2900 www.hitachicapitalvehiclesolutions.co.uk 11. Inchcape ▲ 4 24,249 22,455 Steve Archer Inchcape PLC 0870 191 4444 Fleet Solutions www.ifs.inchcape.co.uk 12. Citroen ▲ 4 23,448 22,392 Duncan Chumley Banque PSA Finance 0845 013 0761 Contract Motoring www.citroen-contract-motoring.co.uk 13. -

United Kingdom Small Company Portfolio-Institutional Class As of July 31, 2021 (Updated Monthly) Source: State Street Holdings Are Subject to Change

United Kingdom Small Company Portfolio-Institutional Class As of July 31, 2021 (Updated Monthly) Source: State Street Holdings are subject to change. The information below represents the portfolio's holdings (excluding cash and cash equivalents) as of the date indicated, and may not be representative of the current or future investments of the portfolio. The information below should not be relied upon by the reader as research or investment advice regarding any security. This listing of portfolio holdings is for informational purposes only and should not be deemed a recommendation to buy the securities. The holdings information below does not constitute an offer to sell or a solicitation of an offer to buy any security. The holdings information has not been audited. By viewing this listing of portfolio holdings, you are agreeing to not redistribute the information and to not misuse this information to the detriment of portfolio shareholders. Misuse of this information includes, but is not limited to, (i) purchasing or selling any securities listed in the portfolio holdings solely in reliance upon this information; (ii) trading against any of the portfolios or (iii) knowingly engaging in any trading practices that are damaging to Dimensional or one of the portfolios. Investors should consider the portfolio's investment objectives, risks, and charges and expenses, which are contained in the Prospectus. Investors should read it carefully before investing. This fund operates as a feeder fund in a master-feeder structure and the holdings listed below are the investment holdings of the corresponding master fund. Your use of this website signifies that you agree to follow and be bound by the terms and conditions of use in the Legal Notices. -

Annual Report and Accounts 2018 Inchcape Plc Annual

INCHCAPE PLC ANNUAL REPORT & ACCOUNTS 2018 ANNUAL REPORT AND ACCOUNTS 2018 STRATEGIC REPORT REVENUE 1 Chairman’s welcome 2 Chief Executive’s review £9.3BN 4 Our unique global position 2017: £9.0BN 6 Working with leading OEM partners 8 Our value chain 1 11 Overview of our industry DIVIDEND PER SHARE 12 Our strategy 15 Our investment proposition 26.8P 16 Capital Allocation Framework 18 Key Performance Indicators 2017: 26.8P 20 Operating and financial review 28 Corporate social responsibility CASH RETURNED TO SHAREHOLDERS 35 Risk management GOVERNANCE £115.2M 48 Board of Directors 2017: £152.9M 50 Chairman’s statement 51 Corporate Governance Report RETURN ON CAPITAL EMPLOYED1 68 Directors’ Report on Remuneration 88 Directors’ Report 28% FINANCIAL STATEMENTS 2017: 30% 94 Independent auditor’s report to the members of Inchcape plc 102 Consolidated income statement 1APM (alternative performance measures), 103 Consolidated statement of comprehensive income page 165 104 Consolidated statement of financial position 105 Consolidated statement of changes in equity 106 Consolidated statement of cash flows 107 Accounting policies 118 Notes to the financial statements 165 Alternative performance measures 166 Five year record 167 Company statement of financial position 168 Company statement of changes in equity 169 Company Accounting policies 171 Notes to the Company financial statements OTHER INFORMATION 184 Shareholder information Visit our website for additional information and interactive features inchcape.com Clarifying our Financial Metrics The following table shows the key profit measures that we use throughout this report to most accurately describe underlying operating performance and how they relate to statutory measures. Metric Results Use of Metric Gross Profit 1,301.3 Direct profit contribution from Value Drivers (e.g. -

Strassmann, Inc. Global Information Productivity® Rankings © Copyright 1997, All Rights Reserved

Strassmann, Inc. Global Information Productivity® Rankings © Copyright 1997, All Rights Reserved This document contains selected 1995 Information Productivity® rankings from industrial companies in Strassmann, Inc.’s database of 8,600 global firms. The 1996 ranking of industrial firms will appear in The Productivity of Information Management , The Information Economics Press, 1998. Definitions Rank: Information Productivity (IP) rankings of 510 industrial firms, with employment of over 15,000 and satisfying a number of financial criteria. Information Management Expenses: Sales, General, Administrative, Research and Development costs. Profits: Net Income after Income Taxes, before Preferred Dividends About Strassmann, Inc. Strassmann, Inc. offers Information Productivity Assessment services to firms wishing to benchmark their performance. Comparisons are made against look-alike firms as well as competitors. Ten year trend analysis in factors contributing to Information Productivity are included in each case. For further information and analytical services, send email to [email protected], or visit our web site, http://www.strassmann.com Available Services 1. Information Productivity ® Assessment Ranking a firm’s information management performance as compared with look- alike organizations. Includes: Ten year analysis of trends, ratio of information to finance costs, correlation with standard measures of financial performance and tabulation of over- or under-performance relative to industry peer group. Detects shifts from labor to capital-intensive information work. Application: Diagnostic method for justifying, planning and budgeting expenditures for information resources. 2. Knowledge Capital ® Assessment Ranking a firm’s performance in terms of is accumulation of knowledge assets as compared with-alike organizations. Includes: Ten year trend analyses, ratio of finance and knowledge capital, comparisons with market valuation (if available) and valuation of employees as assets and not as an expense. -

Annual Report 2018

Compass Group PLC Annual Report 2018 Annual Report 2018 STRATEGIC REPORT 2 2018 performance at a glance 4 Our business at a glance 6 Our market position 7 Our sectors 8 Chairman’s statement 10 Our business model and strategy 12 How we create value Sharpening our 14 Chief Executive’s review 18 Key performance indicators focus through: 20 Regional review 20 North America Performance, People 22 Europe 24 Rest of World and Purpose 26 People report 28 Business review 35 Risk management 36 Principal risks As the industry leader, we have an 38 Corporate responsibility important long term role to play in society. We drive our financial Performance by CORPORATE GOVERNANCE 44 Governance and Directors’ report delivering great food to our clients and 44 Chairman’s letter consumers combined with a rigorous focus 46 Introduction to Corporate Governance on execution. We are further enhancing our 49 Board of Directors People proposition and developing a clearer 52 Corporate Governance report 56 Audit Committee report social Purpose to improve the long term 64 Corporate Responsibility Committee report quality and sustainability of our 68 Nomination Committee report financial results. 71 Directors’ Remuneration report 94 Other statutory disclosures FINANCIAL STATEMENTS 101 Directors’ responsibilities 102 Independent auditor’s report 108 Consolidated financial statements 114 Group accounting policies 122 Notes to the consolidated financial statements 183 Parent Company financial statements 185 Parent Company accounting policies 187 Notes to the Parent Company financial statements SHAREHOLDER INFORMATION 190 Shareholder information 193 Notice of Annual General Meeting GLOSSARY 202 Glossary of terms Visit our website for related information www.compass-group.com Our Corporate Responsibility report will be available online in early 2019 Performance We drive our financial performance by providing our clients with great and healthy food, combined with a rigorous focus on operational execution 2018 has been another strong year with good organic revenue +5.5% growth of 5.5%. -

Achieving Excellence 2013 European Shareholder Value Awards

Achieving excellence 2013 European Shareholder Value Awards June 2013 On behalf of PwC and Automotive News Europe, we are pleased to announce the winners of the 2013 European Shareholder Value Awards in conjunction with the 16th Annual Automotive News Europe Congress. While the industry wrestles with a volatile global economy and the struggles in the euro zone, automotive companies are redefining the way they go to market. We would like to congratulate a handful of companies who have identified growth opportunities which have delivered returns to their shareholders. The PwC European Automotive Shareholder Value Index (SVI) has become accepted as the standard measure of relative shareholder value in the automotive industry. Much of the SVI’s success lies in its simplicity. It looks at the value of €100 invested in a stock over one- and three-year periods, and compares relative returns generated by different companies and industry segments. The result is an objective and reliable measure of shareholder value for stock market-listed automotive companies. The SVI takes into account rise and falls in a company’s share price, dividends, share buy backs and new share issues. Because it is based on the investment of €100, movements in exchange rates also impact the global index and specific company returns. The SVI represents the average return of each portfolio weighted according to the market capitalization of common constituents. The SVI recognizes the highest total shareholder return for European Vehicle Manufacturers, Parts Suppliers and Retailer over one-year and three-year periods ending 31 March 2013. The European Automotive Shareholder Value Awards are presented annually at the Automotive News Europe Congress. -

BEN Boook of Numbers 2012

The Ben Book of Numbers Many thanks for purchasing the BEN Book of Numbers 2012, the definitive guide to what's happening in the automotive sector. Whether you are an industry executive, analyst, sales and marketing professional, researcher or student the BEN Book of Numbers provides you with a wide range of data for a comprehensive overview of the challenging automotive sector. It would not have been possible to produce this publication without the support of financial services Consultancy and Systems provider, White Clarke Group, and the agreement of the providers of data who are acknowledged throughout the report. The majority of the cover price is donated to BEN. BEN exists to provide care, support and advice to those in the automotive industries who need its help in times of hardship or distress. BEN provides a wide range of different types of support depending on your or your loved ones’ situation. This could mean helping with the cost of specialist disabled equipment for a child, giving emotional support through an illness or funding a respite break for you and your partner. BEN will help in whatever way it can. BEN also has four residential centres around the country offering a range of services from nursing to end of life care. In addition, it owns and runs the UK’s first workplace day care centre based in Coventry. Each of the centres provides high quality care so BEN can continue to look after older people in our communities. It costs approximately £11 million each year for BEN to continue its vital work within our industries, and it’s only thanks to the generosity of its supporters it is able to do so. -

Annual Report & Accounts

Annual Report & Accounts 2007 Johnson Matthey Annual Report & Accounts 2007 .com om y e gd h t C1N 8EE t (0)20 7269 8400 7269 (0)20 E a Kin 4 n d o .m e d t n l: +4 ni o e 40-42 Hatton Garden Hatton 40-42 L U Fax: +44 (0)20 7269 8433 7269 +44 (0)20 Fax: www T Cautionary Statement The Operating and Financial Review and certain other sections of this Annual Report, including the Business Review, contain forward looking statements that are subject to risk factors associated with, amongst other things, the economic and business circumstances occurring from time to time in the countries and sectors in which the group operates. It is believed that the expectations reflected in these statements are reasonable but they may be affected by a wide range of variables which could cause actual results to differ materially from those currently anticipated. Front cover: A schematic drawing showing a diesel oxidation catalyst (DOC) and catalysed soot filter (CSF) assembly used to control emissions of carbon monoxide (CO), unburnt hydrocarbons (HC) and particulate matter (PM) from light duty diesel vehicles. In 2006/07 Johnson Matthey completed a new CSF manufacturing facility in Royston, UK and installed additional CSF capacity at its South African facility to meet the growing demand for CSFs in Europe. Image copyright Johnson Matthey Plc 2007 Contents 1 Financial Highlights 50 Consolidated Income Statement 2 Chairman’s Statement 51 Consolidated and Parent Company Balance Sheets 4 Chief Executive’s Statement 52 Consolidated and Parent Company Cash Flow -

FTSE 100 Constituent History Updated

FTSE 100 Constituent Changes Date Added Deleted Notes 19-Jan-84 CJ Rothschild Eagle Star 02-Apr-84 Lonrho Magnet Sthrns. 02-Jul-84 Reuters Edinburgh Inv. Trust 02-Jul-84 Woolworths Barrat Development 19-Jul-84 Enterprise Oil Bowater Corporation 01-Oct-84 Willis Faber Wimpey (George) 01-Oct-84 Granada Group Scottish & Newcastle 01-Oct-84 Dowty Group MFI Furniture 04-Dec-84 Brit. Telecom Matthey Johnson 02-Jan-85 Dee Corporation Dowty Group 02-Jan-85 Argyll Group Berisford (S.& W.) 02-Jan-85 MFI Furniture RMC Group 02-Jan-85 Dixons Group Dalgety 01-Feb-85 Jaguar Hambro Life 01-Apr-85 Guinness (A) Enterprise Oil 01-Apr-85 Smiths Inds. House of Fraser 01-Apr-85 Ranks Hovis McD. MFI Furniture 01-Jul-85 Abbey Life Ranks Hovis McD. 01-Jul-85 Debenhams I.C. Gas 06-Aug-85 Bnk. Scotland Debenhams 01-Oct-85 Habitat Mothercare Lonrho 02-Jan-86 Scottish & Newcastle Rothschild (J) 08-Jan-86 Storehouse Habitat Mothercare 08-Jan-86 Lonrho B.H.S. 01-Apr-86 Wellcome EXCO International 01-Apr-86 Coats Viyella Sun Life Assurance 01-Apr-86 Lucas Harrisons & Crosfield 01-Apr-86 Cookson Group Ultramar 21-Apr-86 Ranks Hovis McD. Imperial Group 22-Apr-86 RMC Group Distillers 01-Jul-86 British Printing & Comms. Corp Abbey Life 01-Jul-86 Burmah Oil Bank of Scotland 01-Jul-86 Saatchi & S. Ferranti International 01-Oct-86 Bunzl Brit. & Commonwealth 01-Oct-86 Amstrad BICC 01-Oct-86 Unigate Smiths Industries 09-Dec-86 British Gas Northern Foods 02-Jan-87 Hillsdown Holdings Argyll Group 02-Jan-87 I.C.