BEN Boook of Numbers 2012

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

LABOUR and TECHNOLOGY in the CAR INDUSTRY. Ford Strategies in Britain and Brazil

LABOUR AND TECHNOLOGY IN THE CAR INDUSTRY. Ford strategies in Britain and Brazil Elizabeth Bortolaia Silva Thesis submitted for the Degree of PhD, Imperial College of Science and Technology University of London May 1988 LABOUR AND TECHNOLOGY IN THE CAR INDUSTRY Ford strategies in Britain and Brazil ABSTRACT This thesis looks at aspects of recent changes in international competition in the car industry. It examines the implications of the changes for the relationship between technology and work and it considers how strategies of multinational corporations interact with different national contexts. It is based on a case-study of the Ford Motor Company in its two largest factories in Britain and Brazil, Dagenham and São Bernardo. Chapter 1 describes existing theoretical approaches to comparative studies of technology and work, criticizes technological and cultural determinist approaches and argues for a method that draws on a 'historical regulation' approach. Chapters 2, 3 and 4 describe the long-term background and recent shifts in the pattern of international competition in the motor industry. In particular they look at important shifts in the late 1970s and 1980s and at Ford's changes in management structure and product strategy designed to meet these challenges. Chapter 5 considers recent debates on international productivity comparisons and presents a fieldwork-based comparison of the production process at Dagenham and São Bernardo. The description shows the importance of issues other than technology in determining the flexibility and quality of production. In different national contexts, 2 different mixes of technology and labour can produce comparable results. Chapters 6, 7 and 8 look at the national and local contexts of industrial relations in the two countries to throw light on the different patterns of change observed in the factories. -

Esmee Hawkey Confirms Brand Ambassador Role for Porsche Centre South London

Esmee Hawkey confirms Brand Ambassador Role for Porsche Centre South London Racing superstar, Esmee Hawkey has taken on a new role. The 19-year-old from Chislehurst will be representing the new Porsche Centre in South London as a brand ambassador. The cooperation is initially signed for one year and involves a communications and brand awareness campaign. Esmee is already very familiar with the Porsche brand having raced a Cayman GT4 for the past two years. This year sees Esmee step up to the Porsche Carrera Cup GB championship racing the 911 GT3 Cup car. In addition to progressing through the Porsche motorsport ranks, Hawkey has achieved other successes with the Stuttgart-based manufacturer. In September 2017, Hawkey took victory in class C4 at the Brighton Speed Trials in an unmodified four- wheel drive 911 Turbo S. "Esmee is an exceptional talent. She combines top performance in her sports cars with elegance and precision. These are precisely the qualities that made Esmee the perfect choice to represent Porsche Centre South London” comments Chris Butler who is the Centre Principal at South London. Of the partnership Esmee says “It is an absolute honour for me to be chosen to represent such an amazing new Porsche Centre. The facilities at Porsche Centre South London are state of the art and amazing. As part of my role, I will also get the benefit of driving one of their Porsche road cars, as well as my race car!” ---------- END --------- Porsche in the UK There are currently 38 Porsche Centres in the GB and Ireland network, with additional Centres planned in Perth and Isle of Man and due to open in April 2018. -

May 2011.Csv

Supplier Name Supplier ID Payment Date Amount Spend Area Account Code Account Description Internal Reference Number 007 STRATFORD TAXIS LIMITED C20689 16/05/2011 1,213.00 ENVIRONMENT AND ECONOMY CF08 SEN UNDER 16 PT362418,1 007 STRATFORD TAXIS LIMITED C20689 16/05/2011 538.00 ENVIRONMENT AND ECONOMY CF09 SEN (FEFC) PT362136,1 2028 (SOUTHAM) SQUADRON AIR TRAINING CORPS U07899 12/05/2011 700.00 RESOURCES D730 GRANTS TO VOLUNTARY ORGANISATIONS CL189227,1 A F BLAKEMORE & SON LTD C22790 05/05/2011 8,936.84 RESOURCES DB40 FOOD WA234829,1 A F BLAKEMORE & SON LTD C22790 09/05/2011 736.45 RESOURCES DB40 FOOD WA235469,1 A F BLAKEMORE & SON LTD C22790 16/05/2011 759.97 RESOURCES BF12 CLEANING MATERIALS WA236545,2 A F BLAKEMORE & SON LTD C22790 16/05/2011 26,389.01 RESOURCES DB40 FOOD WA236545,1 A F BLAKEMORE & SON LTD C22790 23/05/2011 948.23 RESOURCES BF12 CLEANING MATERIALS WA237219,2 A F BLAKEMORE & SON LTD C22790 23/05/2011 25,874.97 RESOURCES DB40 FOOD WA237219,1 A F BLAKEMORE & SON LTD C22790 31/05/2011 1,113.03 RESOURCES BF12 CLEANING MATERIALS WA237925,2 A F BLAKEMORE & SON LTD C22790 31/05/2011 27,874.26 RESOURCES DB40 FOOD WA237925,1 A LINE TAXIS CI5096 12/05/2011 1,350.25 ENVIRONMENT AND ECONOMY CF01 SCHOOL TRANSPORT PAYMENTS PT362073,2 A LINE TAXIS CI5096 12/05/2011 1,925.00 ENVIRONMENT AND ECONOMY CF01 SCHOOL TRANSPORT PAYMENTS PT362073,1 A R CARTWRIGHT (CONSTRUCTION) LTD U02699 26/05/2011 53,670.65 CAPITAL B1 BUILDING WORKS WA237623,1 A TO B TAXIS C20792 16/05/2011 660.00 ENVIRONMENT AND ECONOMY CF08 SEN UNDER 16 PT362290,1 A TO B TAXIS -

FTSE Factsheet

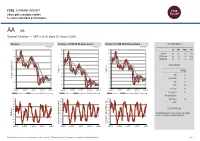

FTSE COMPANY REPORT Share price analysis relative to sector and index performance AA AA. General Retailers — GBP 0.25 at close 03 August 2020 Absolute Relative to FTSE UK All-Share Sector Relative to FTSE UK All-Share Index PERFORMANCE 03-Aug-2020 03-Aug-2020 03-Aug-2020 0.7 140 140 1D WTD MTD YTD 130 130 Absolute 4.6 4.6 4.6 -57.0 0.6 Rel.Sector 2.4 2.4 2.4 -48.8 120 120 Rel.Market 2.5 2.5 2.5 -46.1 110 110 0.5 100 100 VALUATION 90 0.4 90 80 Trailing Relative Price Relative Relative Price Relative 80 70 0.3 PE 1.6 70 Absolute Price (local currency) (local Price Absolute 60 EV/EBITDA 8.0 60 50 0.2 PB -ve 50 40 PCF 0.7 0.1 40 30 Div Yield 2.6 Aug-2019 Nov-2019 Feb-2020 May-2020 Aug-2020 Aug-2019 Nov-2019 Feb-2020 May-2020 Aug-2020 Aug-2019 Nov-2019 Feb-2020 May-2020 Aug-2020 Price/Sales 0.1 Absolute Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Net Debt/Equity - 100 90 90 Div Payout 4.6 90 80 80 ROE - 80 70 70 70 Index) Share Share Sector) Share - - 60 60 60 DESCRIPTION 50 50 50 40 40 The principal activity of the Company is providing 40 RSI RSI (Absolute) service of consumer roadside assistance. -

Jardine Motors Group

CASE STUDY JARDINE MOTORS GROUP Liquidline were awarded the Jardine Motors Group coffee and vending contract in 2014 due to the innovative bean to cup coffee machines. Previously, JMG were using a widely known, capsule-based coffee system but wanted a premium, fresh bean coffee solution to enhance the customer experience. Jardine Motors Group is a leading vehicle retailer of new and used cars from some of the world’s largest and most prestigious manufacturers. They represent more than 20 motor vehicle franchises in over 70 locations within the UK and trade under the name of Lancaster. Employing over 3,500 staff, their business services include new car sales, used car sales and aftersales. Jardine Motors Group is a leading franchised retail motor group in the UK, with an annual revenue of over £2 billion. Operating under the Lancaster brand, the Group represents Aston Martin, Audi, BMW, Ferrari, Harley-Davidson, Honda, Jaguar, Lamborghini, Land Rover, Lexus, Maserati, McLaren, Mercedes-Benz, Porsche, Toyota and Volkswagen brands through their dealership network of more than 70 sites located throughout the UK. CASE STUDY Jardine Motors Group also has motor retail operations in Hong Kong and China and is part of the Jardine Matheson Group, with headquarters in Hong Kong and whose other interests include Dairy Farm, Hong Kong Land, Astra International and the Mandarin Oriental Hotels Group. Ultimately, their mission is ‘to be the best motor retailer as judged by you’ and they expect their supplier partners to help them achieve this goal. Like many industries, the automotive industry has been significantly impacted by the internet. -

Engineering That Moves the World Highlights of the Year Delivering on Expectations

Annual Report and Accounts 2016 Engineering that moves the world Highlights of the year Delivering on expectations ◆ Another year of growth delivering earnings ◆ Sharpening the focus through the disposal of Stromag momentum. and a Group-wide fixed cost reduction programme. ◆ Strong performance from Fokker Technologies ◆ Continued investment in technology primarily focused (‘Fokker’) in first full year of ownership. on electrified drivetrains and additive manufacturing. STATUTORY BASIS MANAGEMENT BASIS1 Sales Sales £8,822m 2015: £7,231m £9,414m 201 5: £ 7,6 89m Earnings per share Earnings per share 14.1p 2015: 11.8p 31.0p 201 5: 27.8p Profit before tax Profit before tax £292m 2015: £245m £678m 2015: £603m Management sales Management trading profit £9,414m £773m2 Other Businesses £39m GKN Land Systems £18m GKN Land Systems GKN Powder Metallurgy £118m £704m GKN Aerospace £3,423m GKN Powder GKN Aerospace Metallurgy £339m £1,032m GKN Driveline £323m GKN Driveline £4,216m 1 See page 39 for details on measurement and reporting of performance on a management basis. 2 Including corporate costs and Other Businesses. Contents Strategic report Governance Financial statements 1 Overview 60 Board of Directors 111 Independent auditor’s report 12 Chairman’s statement 62 Chairman’s introduction to governance 118 Group financial statements 14 Our strategic framework 63 Corporate governance 167 Company financial statements 15 Our business model 72 Nominations Committee report 176 Group financial record 16 Key performance indicators 74 Audit & Risk Committee report 19 Chief Executive’s review 81 Directors’ remuneration report Other information 22 Financial review 107 Additional information 178 Shareholder information 24 Divisional reviews 110 Statement of Directors’ responsibilities 24 – GKN Aerospace review Pages 60 to 110 comprise the Directors’ report. -

Lex Autolease Limited Annual Report

Lex Autolease Limited Report and Accounts 2020 Member of Lloyds Banking Group Strategic report For the year ended 31 December 2020 The directors present their Strategic report of Lex Autolease Limited (the "Company") for the year ended 31 December 2020. Business overview The principal activities of the Company are vehicle contract hire and the provision of motor vehicles under credit sale, contract purchase and finance lease agreements. The directors consider the level of new business written in the year to be satisfactory under the circumstances where the COVID-19 pandemic caused considerable disruption to the delivery and collection of vehicles and to the use made of vehicles supplied to customers during the national lockdowns. The Company has supported customers experiencing financial difficulty through this period of economic uncertainty offering tailored payment holidays for customers in financial difficulty. In response to the worsening economic climate caused by the COVID-19 pandemic, the credit impairment provision increased by £9,432,000 from £10,864,000 as at 31 December 2019 to £20,296,000 as at 31 December 2020, in anticipation of a fall in used car prices. In 2020, the Company as part of Lloyds Banking Group ("the Group"), signed a 5 year agreement, effective from January 2021, to continue the strategic relationship with Jaguar Land Rover, which for the Company secures the supply of up to 6,000 vehicles annually under the Jaguar Land Rover branded contract hire product. Additionally the Company’s investment programme continued to transform and digitise the customer journey, creating a more efficient experience for customers and facilitating cost savings for the Company. -

THE DECEMBER SALE Collectors’ Motor Cars, Motorcycles and Automobilia Thursday 10 December 2015 RAF Museum, London

THE DECEMBER SALE Collectors’ Motor Cars, Motorcycles and Automobilia Thursday 10 December 2015 RAF Museum, London THE DECEMBER SALE Collectors' Motor Cars, Motorcycles and Automobilia Thursday 10 December 2015 RAF Museum, London VIEWING Please note that bids should be ENQUIRIES CUSTOMER SERVICES submitted no later than 16.00 Wednesday 9 December Motor Cars Monday to Friday 08:30 - 18:00 on Wednesday 9 December. 10.00 - 17.00 +44 (0) 20 7468 5801 +44 (0) 20 7447 7447 Thereafter bids should be sent Thursday 10 December +44 (0) 20 7468 5802 fax directly to the Bonhams office at from 9.00 [email protected] Please see page 2 for bidder the sale venue. information including after-sale +44 (0) 8700 270 089 fax or SALE TIMES Motorcycles collection and shipment [email protected] Automobilia 11.00 +44 (0) 20 8963 2817 Motorcycles 13.00 [email protected] Please see back of catalogue We regret that we are unable to Motor Cars 14.00 for important notice to bidders accept telephone bids for lots with Automobilia a low estimate below £500. +44 (0) 8700 273 618 SALE NUMBER Absentee bids will be accepted. ILLUSTRATIONS +44 (0) 8700 273 625 fax 22705 New bidders must also provide Front cover: [email protected] proof of identity when submitting Lot 351 CATALOGUE bids. Failure to do so may result Back cover: in your bids not being processed. ENQUIRIES ON VIEW Lots 303, 304, 305, 306 £30.00 + p&p AND SALE DAYS (admits two) +44 (0) 8700 270 090 Live online bidding is IMPORTANT INFORMATION available for this sale +44 (0) 8700 270 089 fax BIDS The United States Government Please email [email protected] has banned the import of ivory +44 (0) 20 7447 7447 with “Live bidding” in the subject into the USA. -

Completed Acquisition of Two Vauxhall Dealerships from Riders' Garages Limited by Eden

Completed acquisition of two Vauxhall dealerships from Riders’ Garages Limited by Eden (GM) Limited ME/6474-14 The CMA’s decision on reference under section 22(1) on 24 October 2014. Full text of the decision published on 17 November 2014. Please note that [] indicates figures or text which have been deleted or replaced in ranges at the request of the parties for reasons of commercial confidentiality. Summary 1. Eden (GM) Limited (Eden) operates Vauxhall franchised car dealerships. Its two Devon dealerships, Exeter and Honiton, supply new and used Vauxhall cars to private customers as well as repair and maintenance services to Vauxhall cars. 2. Eden acquired two Vauxhall dealerships in Newton Abbot and Torbay (the Riders dealerships) from Riders Garages Limited (Riders) (the Merger). The Riders dealerships supply new and used Vauxhall cars to private customers and repair and maintenance services to Vauxhall cars. Eden and the Riders dealerships together are referred to in this decision as the Parties. 3. The Competition and Markets Authority (CMA) considers that the Parties are enterprises that as a result of the Merger have ceased to be distinct and that the share of supply test is met. The CMA therefore believes that it is or may be the case that a relevant merger situation has been created. 4. Eden and the Riders dealerships overlap in the supply of new and used Vauxhall cars and the supply of repair and maintenance services for Vauxhall cars in the Exeter, Newton Abbot and Torbay areas. 5. In relation to the supply of new and used Vauxhall cars, the CMA does not consider there to be competition concerns based on the constraints faced by the Parties locally from dealerships of other car marques including other sellers of used cars (both Vauxhall and others). -

2002 Ford Motor Company Annual Report

2228.FordAnnualCovers 4/26/03 2:31 PM Page 1 Ford Motor Company Ford 2002 ANNUAL REPORT STARTING OUR SECOND CENTURY STARTING “I will build a motorcar for the great multitude.” Henry Ford 2002 Annual Report STARTING OUR SECOND CENTURY www.ford.com Ford Motor Company G One American Road G Dearborn, Michigan 48126 2228.FordAnnualCovers 4/26/03 2:31 PM Page 2 Information for Shareholders n the 20th century, no company had a greater impact on the lives of everyday people than Shareholder Services I Ford. Ford Motor Company put the world on wheels with such great products as the Model T, Ford Shareholder Services Group Telephone: and brought freedom and prosperity to millions with innovations that included the moving EquiServe Trust Company, N.A. Within the U.S. and Canada: (800) 279-1237 P.O. Box 43087 Outside the U.S. and Canada: (781) 575-2692 assembly line and the “$5 day.” In this, our centennial year, we honor our past, but embrace Providence, Rhode Island 02940-3087 E-mail: [email protected] EquiServe Trust Company N.A. offers the DirectSERVICE™ Investment and Stock Purchase Program. This shareholder- paid program provides a low-cost alternative to traditional retail brokerage methods of purchasing, holding and selling Ford Common Stock. Company Information The URL to our online Investor Center is www.shareholder.ford.com. Alternatively, individual investors may contact: Ford Motor Company Telephone: Shareholder Relations Within the U.S. and Canada: (800) 555-5259 One American Road Outside the U.S. and Canada: (313) 845-8540 Dearborn, Michigan 48126-2798 Facsimile: (313) 845-6073 E-mail: [email protected] Security analysts and institutional investors may contact: Ford Motor Company Telephone: (313) 323-8221 or (313) 390-4563 Investor Relations Facsimile: (313) 845-6073 One American Road Dearborn, Michigan 48126-2798 E-mail: [email protected] To view the Ford Motor Company Fund and the Ford Corporate Citizenship annual reports, go to www.ford.com. -

Auto 04 Temp.Qxd

FORD AUTOTEAM THE MAGAZINE FOR ALL FORD DEALER STAFF ISSUE 3/2016 EDITORIAL Changing Times It’s all change for the management team at the Henry Ford Academy. Stuart Harris has moved on to a new position within Ford of Europe and, as I move into his role, I hope to continue with his goal of driving up training standards. Also joining the team is new Academy Principle, Kevin Perks, who brings with him a lifetime of automotive industry experience. Dan Savoury, the new Vice Principal, joined the Academy earlier this year and also has a wealth of industry and training experience that will help us continue to improve our training which, in turn, benefits your business. I hope to use the experience gained in my previous sales and marketing roles within Ford to help our training continue to grow in scope and quality. It is a really exciting time to be a part of the Ford family; with new vehicles joining the range and new technology transforming the industry more widely. Good training is vital to our success and we continue to strive to achieve the highest standards and keep you up to date with this rapidly changing industry, from the technical training for the All-new Ford Mustang detailed on page 4, to ensuring our Commercial Vehicle Sales staff can give their customers the best advice with courses such as Commercial Vehicle Type Approval and Legislation on page 30. The success of our training programmes is demonstrated in this issue, with Chelsea Riddle from TrustFord in Bradford a great example of what the Ford Masters Apprenticeship scheme offers to young people, or the success that Mike Gates from Dinnages Ford in Burgess Hill has achieved with a university scholarship through the Henry Ford Academy. -

Don't Leave Your Cars Sitting in the Dark. Put Them in The

AM100 Top 100 table FOR MORE DETAILS SEE PAGE 26 Headline sponsors Rank (2012) Name T/O 2013 (£,000) T/O 2012 (£,000) Outlets 2013 Outlets 2012 Total cars Total LCV Rank (2012) Name T/O 2013 (£,000) T/O 2012 (£,000) Outlets 2013 Outlets 2012 Total cars Total LCV Rank (2012) Name T/O 2013 (£,000) T/O 2012 (£,000) Outlets 2013 Outlets 2012 Total cars Total LCV Rank (2012) Name T/O 2013 (£,000) T/O 2012 (£,000) Outlets 2013 Outlets 2012 Total cars Total LCV 1 (1) Pendragon Plc 3,635,100 3,465,800 238 222 246,100 n/a 26 (26) Eastern Western Motor Group 346,000 325,000 27 27 n/a n/a 51 (61) Motorline 199,769 166,290 21 20 11,965 n/a 76 (75) Brindley Garages 135,000 140,000 18 17 n/a n/a 2 (2) Sytner Group 3,001,000 2,500,000 141 138 105,224 n/a 27 (31) Harwoods 340,898 276,814 16 15 8,021 n/a 52 (58) Johnsons Cars 194,200 171,000 23 22 13,409 n/a 77 (80) Macrae & Dick 134,802 127,709 11 10 n/a n/a 3 (3) Arnold Clark Automobiles 2,604,080 2,253,071 197 154 202,377 n/a 28 (23) Park’s Motor Group 340,000 340,000 37 29 n/a n/a 53 (59) Caffyns Plc 191,760 170,192 14 18 n/a n/a 78 (87) Jacksons Bournemouth 134,000 117,791 10 8 4,296 n/a 4 (5) Lookers Plc 2,163,100 1,898,500 118 109 n/a n/a 29 (22) Pentagon Motor Holdings 339,990 377,753 29 25 25,128 4,861 54 (50) Donnelly Bros Garages (Dungannon) 189,000 185,000 30 32 11,033 2,257 79 (95) Heritage Automotive 130,618 101,146 12 12 n/a n/a 5 (4) Inchcape Retail 2,096,400 2,023,200 113 116 n/a n/a 30 (44) Peter Vardy 312,941 206,982 10 9 13,229 389 55 (52) CEM Day 186,205 181,000 11 11 8,202 3,096 80