Vanguard Emerging Markets Stock Index Fund Annual Report October

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Dalian Refrigeration Co., Ltd. 2011 Annual Report

Dalian Refrigeration Co., Ltd. 2011 Annual Report Dalian Refrigeration Co., Ltd. 2011 Annual Report CONTENTS §1 Important Notes⋯⋯⋯⋯⋯ ⋯⋯⋯⋯⋯ ⋯⋯⋯⋯⋯ ⋯⋯⋯⋯⋯ ⋯⋯⋯⋯⋯ ⋯⋯ 2 §2 Company Profile⋯⋯⋯⋯ ⋯⋯⋯ ⋯⋯ ⋯⋯⋯ ⋯⋯ ⋯⋯⋯ ⋯⋯ ⋯⋯⋯ ⋯⋯ ⋯ 2 §3 Summary of Accounting Data and Business Data⋯⋯ ⋯ ⋯⋯⋯ ⋯⋯ ⋯⋯⋯ ⋯⋯ ⋯ 4 §4 Changes in Share Capital and Particulars about Shareholders⋯⋯⋯ ⋯⋯⋯ ⋯⋯ 6 §5 Directors, Supervisors, Senior Staff Members and Employees of the Company⋯⋯ 9 §6 The Administrative System of the Company⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯ 13 §7 The Internal Control of the Company⋯ ⋯⋯⋯⋯⋯ ⋯⋯⋯⋯⋯ ⋯⋯⋯⋯⋯ ⋯⋯⋯ 15 §8 Brief Introduction to the Shareholders General Meeting⋯ ⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯ 16 §9 Report of the Board of Directors⋯⋯⋯⋯ ⋯⋯⋯⋯⋯ ⋯⋯⋯⋯⋯ ⋯⋯⋯⋯⋯ ⋯ 17 §10 Report of the Supervisory Board⋯⋯⋯⋯ ⋯⋯⋯⋯ ⋯ ⋯⋯⋯⋯ ⋯ ⋯⋯⋯⋯ ⋯ ⋯ 29 §11 Significant Events⋯⋯⋯⋯⋯ ⋯⋯⋯⋯⋯ ⋯⋯⋯⋯⋯ ⋯⋯⋯⋯⋯ ⋯⋯⋯⋯⋯ ⋯ 31 §12 Financial Report⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯ 37 §13 Contents of Reference Documents⋯ ⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯ 95 1 Dalian Refrigeration Co., Ltd. 2011 Annual Report §1 Important Notes 1.1 The directors and the Board of Directors, the supervisors and the Supervisory Board, and Senior staff members of Dalian Refrigeration Co., Ltd. (hereinafter referred to as the Company) hereby confirm that there are not any important omissions, fictitious statements or serious misleading carried in this report, and shall take all responsibilities, individual and/or joint, for the reality, accuracy and completeness of the whole contents. 1.2 The financial report has been audited by ZON ZUN Certified Public Accounts Office Ltd. who has presented unqualified opinion audit report. 1.3 Chairman of the Board of Directors of the Company Mr. Zhang He, Financial Majordomo and the head of Accounting Department Ms. Xu Junrao hereby confirm that the financial report of the annual report is true and complete. 1.4 This report is written respectively in Chinese and in English. -

Q3 2019 Holding Lijst

Aandelen Obligaties 360 Security Technology Inc 3SBio Inc 3i Group PLC Abbott Laboratories 3M Co AbbVie Inc 3SBio Inc Acadia Healthcare Co Inc 51job Inc adidas AG 58.com Inc ADLER Real Estate AG AAC Technologies Holdings Inc ADO Properties SA ABB Ltd Aermont Capital LLP Abbott Laboratories AES Corp/VA AbbVie Inc African Development Bank ABIOMED Inc Aggregate Holdings SA Aboitiz Equity Ventures Inc Air France-KLM Absa Group Ltd Air Transport Services Group I Accell Group NV Akamai Technologies Inc Accenture PLC Aker BP ASA Accor SA Albertsons Investor Holdings L Acer Inc Alcoa Corp ACS Actividades de Construccio Alfa SAB de CV Activision Blizzard Inc Alibaba Group Holding Ltd Acuity Brands Inc Allergan PLC Adecco Group AG Alliander NV adidas AG Allianz SE Adobe Inc Ally Financial Inc Advance Auto Parts Inc Almirall SA Advanced Info Service PCL Altice USA Inc Advanced Micro Devices Inc Amazon.com Inc Advantech Co Ltd America Movil SAB de CV Aegon NV American International Group I AES Corp/VA Amgen Inc Affiliated Managers Group Inc ams AG Agilent Technologies Inc ANA Holdings Inc AIA Group Ltd Anglian Water Group Ltd Aier Eye Hospital Group Co Ltd Anglo American PLC Air LiQuide SA Anheuser-Busch InBev SA/NV Air Products & Chemicals Inc Antero Resources Corp AirAsia Group Bhd APA Group Airbus SE APERAM SA Aisino Corp Aphria Inc Akamai Technologies Inc Apollo Global Management Inc Aker BP ASA Apple Inc Akzo Nobel NV Aptiv PLC Alcon Inc Arab Republic of Egypt Alexandria Real Estate Equitie Arconic Inc Alfa Laval AB ARD Holdings SA Alfa SAB de -

Retirement Strategy Fund 2060 Description Plan 3S DCP & JRA

Retirement Strategy Fund 2060 June 30, 2020 Note: Numbers may not always add up due to rounding. % Invested For Each Plan Description Plan 3s DCP & JRA ACTIVIA PROPERTIES INC REIT 0.0137% 0.0137% AEON REIT INVESTMENT CORP REIT 0.0195% 0.0195% ALEXANDER + BALDWIN INC REIT 0.0118% 0.0118% ALEXANDRIA REAL ESTATE EQUIT REIT USD.01 0.0585% 0.0585% ALLIANCEBERNSTEIN GOVT STIF SSC FUND 64BA AGIS 587 0.0329% 0.0329% ALLIED PROPERTIES REAL ESTAT REIT 0.0219% 0.0219% AMERICAN CAMPUS COMMUNITIES REIT USD.01 0.0277% 0.0277% AMERICAN HOMES 4 RENT A REIT USD.01 0.0396% 0.0396% AMERICOLD REALTY TRUST REIT USD.01 0.0427% 0.0427% ARMADA HOFFLER PROPERTIES IN REIT USD.01 0.0124% 0.0124% AROUNDTOWN SA COMMON STOCK EUR.01 0.0248% 0.0248% ASSURA PLC REIT GBP.1 0.0319% 0.0319% AUSTRALIAN DOLLAR 0.0061% 0.0061% AZRIELI GROUP LTD COMMON STOCK ILS.1 0.0101% 0.0101% BLUEROCK RESIDENTIAL GROWTH REIT USD.01 0.0102% 0.0102% BOSTON PROPERTIES INC REIT USD.01 0.0580% 0.0580% BRAZILIAN REAL 0.0000% 0.0000% BRIXMOR PROPERTY GROUP INC REIT USD.01 0.0418% 0.0418% CA IMMOBILIEN ANLAGEN AG COMMON STOCK 0.0191% 0.0191% CAMDEN PROPERTY TRUST REIT USD.01 0.0394% 0.0394% CANADIAN DOLLAR 0.0005% 0.0005% CAPITALAND COMMERCIAL TRUST REIT 0.0228% 0.0228% CIFI HOLDINGS GROUP CO LTD COMMON STOCK HKD.1 0.0105% 0.0105% CITY DEVELOPMENTS LTD COMMON STOCK 0.0129% 0.0129% CK ASSET HOLDINGS LTD COMMON STOCK HKD1.0 0.0378% 0.0378% COMFORIA RESIDENTIAL REIT IN REIT 0.0328% 0.0328% COUSINS PROPERTIES INC REIT USD1.0 0.0403% 0.0403% CUBESMART REIT USD.01 0.0359% 0.0359% DAIWA OFFICE INVESTMENT -

In the United States District Court for the Eastern District of Texas Marshall Division Fundamental Innovation Systems Internati

Case 2:20-cv-00117 Document 1 Filed 04/23/20 Page 1 of 24 PageID #: 1 IN THE UNITED STATES DISTRICT COURT FOR THE EASTERN DISTRICT OF TEXAS MARSHALL DIVISION FUNDAMENTAL INNOVATION SYSTEMS INTERNATIONAL LLC, Plaintiff, Civil Action No. 2:20-cv-00117 vs. COOLPAD GROUP LIMITED, COOLPAD JURY TRIAL DEMANDED TECHNOLOGIES, INC., and YULONG COMPUTER TELECOMMUNICATION SCIENTIFIC (SHENZHEN) CO. LTD., Defendants. COMPLAINT FOR PATENT INFRINGEMENT AND JURY DEMAND Plaintiff Fundamental Innovation Systems International LLC (“Plaintiff” or “Fundamental”), by and through its undersigned counsel, brings this action against Defendants Coolpad Group Limited, Coolpad Technologies, Inc., and Yulong Computer Telecommunication Scientific (Shenzhen) Co. Ltd. (collectively “Defendants” or “Coolpad”) to prevent Defendants’ continued infringement of Plaintiff’s patents without authorization and to recover damages resulting from such infringement. PARTIES 1. Plaintiff is a Delaware limited liability company with a place of business located at 2990 Long Prairie Road, Suite B, Flower Mound, Texas 75022. 2. Plaintiff is the owner by assignment of all right, title, and interest in U.S. Patent Nos. 7,239,111 (the “’111 Patent”), 8,624,550 (the “’550 Patent”), 7,834,586 (the “’586 Patent”), 8,232,766 (the “’766 Patent”), and 7,986,127 (the “’127 Patent”) (collectively, the “Patents-in- Suit”). 06904-00001/12059581.3 Case 2:20-cv-00117 Document 1 Filed 04/23/20 Page 2 of 24 PageID #: 2 3. On information and belief, Defendant Coolpad Group Limited is a company duly organized and existing under the laws of the Cayman Islands, with a place of business located at Coolpad Information Harbor, No. -

China Construction Machinery

10 Feb 2020 CMB International Securities | Equity Research | Sector Update China Construction Machinery Scenario analysis on the resumption of factory production OUTPERFORM (Maintain) Factories in China, except Hubei, are scheduled to resume operation today. We China Capital Goods evaluate the companies under our coverage from several dimensions, including location of factories, capacity utilization, downstream demand and cash flow Wayne Fung, CFA management. Our base case scenario suggests that the overall earnings impact (852) 3900 0826 for the full year should be limited, as the sales volume in 1Q (the traditional peak [email protected] season) will potentially be shifted to 2Q or 3Q (low seasons) when the construction activities pick up when the epidemic is under control. We believe potential share price volatility in the near term will serve as opportunities to accumulate quality names such as SANY Heavy (600031 CH, BUY, TP: RMB19.0), Jiangsu Hengli (601100 CH, BUY, TP: RMB54.0) and Weichai Power (2338 HK, BUY, TP: HK$17.9 / 000338 CH, BUY, TP: RMB15.9). Utilization rate to gradually increase. For the companies under our coverage, no production base is located in Hubei province (figure 1). Some companies such as Weichai, SANY Heavy and Zoomlion have already resumed production since last week while others will restart today. That said, we do expect most of them will only ramp up its production gradually due to the potential labour shortage in the near term. Companies are trying their best to ramp up production to fulfil the existing orders, based on our check. Related Reports Expect mild delay on downstream demand. -

Global Industrials

28 May 2013 Americas/United States Equity Research Electrical Equipment / Capital Goods i-Spy Global Industrials Weekly Research Analysts COMMENT Julian Mitchell 212 325 6668 [email protected] More signs of Japanese manufacturing Charles Clarke 212 538 7095 renaissance; rising competition in industrial [email protected] Jonathan Shaffer automation, but bottoming demand 212 325 1259 [email protected] ■ Further signs of Japanese manufacturing renaissance: In an earlier i-Spy, we noted that Nissan had delayed the migration of certain car model production out of Japan; now Kawasaki has announced it will bring back production of mid- sized motorbikes from Thailand to Japan due to the falling Yen. Many of KHI's motorbikes manufactured in Thailand are sold in the US; production will move This Week (5/27/2013 - 6/2/2013) gradually to Japan beginning this autumn. Macro Events ■ China to develop large aero engines within a decade: The MITI's industry 5/28 US May Dallas Fed Mfg. Activity plan last week targets 5% local market share for the domestic commercial 5/28 US May Richmond Fed aerospace industry by 2020 (C919 orders have already reached almost 400 5/30 Euro-Zone Business Climate aircraft), and an assembly line for medium-power aero engines by 2015, with 5/31 US May Chicago PMI larger engines to be produced within 10 years. 6/1 China PMI Mfg ■ Industrial automation competition increasing; PLC role under threat: Company Events Meetings at EPG and at ETN confirmed several themes we noted following our 5/27-30 Siemens AG Roadshow - Beijing trip to Hannover's Automation Fair in April. -

Federal Register/Vol. 79, No. 124/Friday, June 27, 2014/Notices

36462 Federal Register / Vol. 79, No. 124 / Friday, June 27, 2014 / Notices area, information may be obtained from: Administration employees in the States For all other records, information may Office of Work Force Management, of Connecticut, Delaware, Maine, be obtained from: Office of Human National Oceanic and Atmospheric Massachusetts, New Hampshire, New Resources Management, Human Administration, 1305 East-West Jersey, New York, North Carolina, Ohio, Resources Operations Center, U.S. Highway, SSMC#4, Room 12434, Silver Pennsylvania, Rhode Island, South Department of Commerce, Office of the Spring, Maryland 20910, (301) 713– Carolina, Vermont, Virginia, West Secretary, Room 7412 HCHB, 1401 6302. Virginia, Puerto Rico, and the Virgin Constitution Avenue NW., Washington, For records of Office of the Secretary, Islands; for employees in the Bureau of DC, 20230, (202) 482–3301. Bureau of Economic Analysis, Bureau of Industry and Security, Economic Industry and Security, Economic Development Administration, Minority RECORD ACCESS PROCEDURES: Development Agency, Minority Business Development Agency, and Requests from individuals should be Business Development Agency, National International Trade Administration in addressed to: Same address of the Telecommunications and Information the States of Alabama, Delaware, desired location as stated in the Administration employees in the Florida, Georgia, Maryland, New Jersey, Notification section above. Washington, DC, metropolitan area, New York, North Carolina, CONTESTING RECORDS PROCEDURES: information may be obtained from: Pennsylvania, South Carolina, The Department’s rules for access, for Office of Human Resource Management, Tennessee, Virginia, West Virginia, contesting contents, and appealing Human Resource Operations Center, Puerto Rico, and the Virgin Islands: initial determinations by the individuals Office of the Secretary, Room 7412, Human Resources Manager, Eastern concerned appear in 15 CFR part 4b. -

A Relatively Cautious View for 2019, Reiterate "Accumulate"

股 票 研 [Table_Title] Company Report: China Merchants Port (00144 HK) Spencer Fan 范明 究 (86755) 2397 6686 Equity Research 公司报告: 招商局港口 (00144 HK) [email protected] 10 May 2019 A[Table_S Relativelyummary ]Cautious View for 2019, Reiterate "Accumulate" 对2019年维持相对谨慎,重申“收集” The Company's management guided low single-digit growth in 2019. On [Table_Rank] the other hand, the management predicts that the Company's main driving Rating: Accumulate Maintained force in 2019 will come from the overseas segment, and it expects overseas 公 container volume to record medium-to-high single-digit YoY growth in 2019. 评级: 收集 (维持) 司 Domestic port container loading and unloading operation fee might not be 报 greatly adjusted in 2019, while handling fees of some overseas ports might increase. Overall, we expect CMP's port business to generate low single-digit [Table_Price] 告 6-18m TP 目标价: HK$16.80 YoY revenue growth in 2019. Revised from 原目标价: HK$17.00 Company Report Qianhai land ready to release value; the disposal of land interests is Share price 股价: HK$15.120 expected to bring about HK$3.58 billion in after-tax income. We believe that China Merchants Port will benefit indirectly from the long-term development of Shenzhen’s Qianhai Shekou Free Trade Zone. It is Stock performance understood that Qianhai Land will still be developed in accordance with the 股价表现 mature development model of the "Port-Zone-City" of China Merchants [Table_QuotePic] Group. % of return 10.0 Reiterate "Accumulate" rating and adjust TP to HK$16.80. CMP’s port 5.0 resources are still balanced, and we still favor CMP's overseas development 0.0 capability. -

GC Influencers Have Been Chosen Following Research Among Private Practice Lawyers and Other In-House Counsel

v GC Influencers CHINA 2019 Friday, 11th January 2019 JW Marriott Hotel, Hong Kong Programme Engaging content, networking and celebration with leading General Counsel and top ranked lawyers globally. GC Influencers For more informationCHINA visit 2019 chambers.com A5-Advert-Forums.idml 1 22/10/2018 12:17 Welcome SARAH KOGAN Editor Chambers Asia-Pacific Meet the most influential General Counsel in China today. Chambers has provided insight into the legal profession for over 30 years. During this time, in-house lawyers and third-party experts have shared their views on the value and importance placed on the role of the General Counsel. No longer just the ethical and legal heart of a business, these professionals now sit as influential participants at board level. Effective managers, industry pioneers, diversity and CSR champions: these Influencers show the way. Research Methodology: Our GC Influencers have been chosen following research among private practice lawyers and other in-house counsel. We identified the key areas in which GCs have displayed substantial influence: Engaging content, • Effective management and development of an in-house team • Navigation of substantial business projects such as M&A or strategic networking and business change. • Development of litigation strategy and understanding the pressures faced celebration with leading within industry General Counsel and top • Bringing diversity & inclusion and CSR to the forefront of industry. ranked lawyers globally. • Ability to influence and respond to regulatory change Our aim is to celebrate excellence within the legal profession. This dynamic hall of fame encourages collaboration among the in-house legal community. Our GC Influencers have created best practice pathways endorsed by both private practice and other in-house lawyers. -

Shenzhen Chiwan Petroleum Supply Base Co., Ltd

ANNUAL REPORT FOR YEAR 2015 SHENZHEN CHIWAN PETROLEUM SUPPLY BASE CO., LTD. ANNUAL REPORT FOR YEAR 2015 April 2016 1 ANNUAL REPORT FOR YEAR 2015 PART Ⅰ Important Notice The Board of Directors, the Board of Supervisors, directors, supervisors and senior management guarantee that there are no omissions, misstatement or misleading information in this report. They are responsible, individually and jointly, for the authenticity, accuracy and integrity of the information herein. Mr. Tian Junyan, Chairman of the Board, Ms. Yu Zhongxia, Deputy General Manager &Financial Controller, and Ms. Sun Yuhui, Financial Manager, guarantee the authenticity and integrity of the financial result in this report. Except the following directors, other directors attend the Board Meeting. Absent Director Post of the Absent Director Reason Authorized Person Mr. Mingzhi Mei Director Business Arrangement Wang Shiyun Mr. Kent Yang Director Business Arrangement Shu Qian This annual report contains prospective descriptions, which does not constitute substantial commitment to investors. Investors are requested to be aware of the risks attached to their investment decisions. Impossible risk has been well-described in this report. Please find details of risks and countermeasures of future development described in Section IX, Part IV. Securities Times, Hong Kong Commercial Daily and www.cninfo.com.cn are the media designated for disclosing our information. All the Company’s information is subject to the information disclosed in the aforesaid media as designated. The Company will not distribute cash dividends or bonus shares, neither capitalizing of common reserves for the report period. This report is prepared both in Chinese and English languages, when ambiguity occurs in the two versions, the Chinese version shall prevail. -

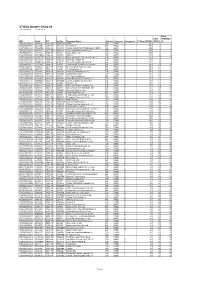

STOXX Greater China 80 Last Updated: 01.08.2017

STOXX Greater China 80 Last Updated: 01.08.2017 Rank Rank (PREVIOU ISIN Sedol RIC Int.Key Company Name Country Currency Component FF Mcap (BEUR) (FINAL) S) TW0002330008 6889106 2330.TW TW001Q TSMC TW TWD Y 113.9 1 1 HK0000069689 B4TX8S1 1299.HK HK1013 AIA GROUP HK HKD Y 80.6 2 2 CNE1000002H1 B0LMTQ3 0939.HK CN0010 CHINA CONSTRUCTION BANK CORP H CN HKD Y 60.5 3 3 TW0002317005 6438564 2317.TW TW002R Hon Hai Precision Industry Co TW TWD Y 51.5 4 4 HK0941009539 6073556 0941.HK 607355 China Mobile Ltd. CN HKD Y 50.8 5 5 CNE1000003G1 B1G1QD8 1398.HK CN0021 ICBC H CN HKD Y 41.3 6 6 CNE1000003X6 B01FLR7 2318.HK CN0076 PING AN INSUR GP CO. OF CN 'H' CN HKD Y 32.0 7 9 CNE1000001Z5 B154564 3988.HK CN0032 BANK OF CHINA 'H' CN HKD Y 31.8 8 7 KYG217651051 BW9P816 0001.HK 619027 CK HUTCHISON HOLDINGS HK HKD Y 31.1 9 8 HK0388045442 6267359 0388.HK 626735 Hong Kong Exchanges & Clearing HK HKD Y 28.0 10 10 HK0016000132 6859927 0016.HK 685992 Sun Hung Kai Properties Ltd. HK HKD Y 20.6 11 12 HK0002007356 6097017 0002.HK 619091 CLP Holdings Ltd. HK HKD Y 20.0 12 11 CNE1000002L3 6718976 2628.HK CN0043 China Life Insurance Co 'H' CN HKD Y 20.0 13 13 TW0003008009 6451668 3008.TW TW05PJ LARGAN Precision TW TWD Y 19.7 14 15 KYG2103F1019 BWX52N2 1113.HK HK50CI CK Property Holdings HK HKD Y 18.3 15 14 CNE1000002Q2 6291819 0386.HK CN0098 China Petroleum & Chemical 'H' CN HKD Y 16.4 16 16 HK0823032773 B0PB4M7 0823.HK B0PB4M Link Real Estate Investment Tr HK HKD Y 15.4 17 19 HK0883013259 B00G0S5 0883.HK 617994 CNOOC Ltd. -

SINDICATO DOS DESPACHANTES ADUANEIROS DE SANTOS E REGIÃO Declarado De Utilidade Pública – Lei 4.119/77 CNPJ-58.251.224/0001-56

SINDICATO DOS DESPACHANTES ADUANEIROS DE SANTOS E REGIÃO Declarado de Utilidade Pública – Lei 4.119/77 CNPJ-58.251.224/0001-56 Santos, 15 de julho de 2019. Taxa Siscomex DIA DÓLAR EURO LIBRA ESTERLINA PESO- ARG 15 3,7452 4,2156 4,7021 0,08979 PORTARIA Nº 494, DE 12 DE JULHO DE 2019 Aplicar direito antidumping definitivo, por um prazo de até 5 (cinco) anos, às importações brasileiras de aço GNO originárias da Alemanha, e alterar os direitos antidumping aplicados sobre as importações do mesmo produto e origens. O SECRETÁRIO ESPECIAL DE COMÉRCIO EXTERIOR E ASSUNTOS INTERNACIONAIS DO MINISTÉRIO DA ECONOMIA, no uso das atribuições que lhe confere o art. 82, inciso V do Anexo I do Decreto nº 9.745, de 8 de abril de 2019, e considerando o que consta dos autos do Processo SECEX 52272.001504/2018-88, conduzido em conformidade com o disposto no Decreto no 8.058, de 26 de julho de 2013, e dos autos do Processo SEI 19972.100359/2019-35, conduzido de acordo com os procedimentos previstos na Resolução CAMEX nº 29, de 7 de abril de 2017, resolve: Art. 1° Encerrar a investigação com aplicação de direito antidumping definitivo, por um prazo de até 5 (cinco) anos, às importações brasileiras de laminados planos de aço ao silício, denominados magnéticos, de grãos não orientados (aço GNO), comumente classificados nos itens 7225.19.00 e 7226.19.00 da Nomenclatura Comum do Mercosul - NCM, originárias da Alemanha, conforme recomendação constante do Anexo I. Art. 2º O disposto no art. 1onão se aplica aos seguintes produtos: a) laminados planos de aço ao silício semiprocessados; b) laminados planos de aço ao silício de grãos orientados; c) bobinas de liga de metal amorfo; d) laminados planos de aço manganês; e) cabos de soldagem; f) núcleos magnéticos de ferrite; e g) laminados planos de aço ao silício com espessura inferior a 0,35mm.