Pakistan Equity Market Strategy 2021 14Th January 2021

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

MAPLE LEAF CEMENT FACTORY LIMITED Table of Contents

MAPLE LEAF CEMENT FACTORY LIMITED Table of Contents Mission Statement 2 Corporate Strategy 3 Statement of Ethics and Business Practices 5 Company Profile 7 Company Information 9 Notice of Annual General Meeting 10 Directors’ Report to the Shareholders 11 Six Years Summary 16 Pattern of Shareholding 17 Statement of Compliance with the Code of Corporate Governance 22 Review Report to the Members on Statement of Compliance with Best Practices of Code of Corporate Governance 24 Auditors’ Report to the Members 25 Balance Sheet 26 Profit and Loss Account 28 Statement of other Comprehensive Income 29 Cash Flow Statement 30 Statement of Changes in Equity 31 Notes to the Accounts 32 Proxy Form ANNUAL REPORT 2010 Mission Statement “The Maple Leaf Cement Factory Limited stated mission is to achieve and then remain as the most progressive and profitable company in Pakistan in terms of industry standards and stakeholders interests. The company shall achieve its mission through a continuous process of having sourced and implemented the best leading edge technology, industry best practice, human resource and by conducting its business professionally and efficiently with responsibility to all its stakeholders and community.” 02 ANNUAL REPORT 2010 Corporate Strategy We at Maple Leaf Cement Factory Limited manufacture and market different types of consistently high quality cement, according to the demanding requirements of the construction industry. Our strategy is to be competitive in the market through quality and efficient operations. As a responsible member of the community, we are committed to serve the interest of all our stakeholders and contribute towards the prosperity of the country. -

Investor Kit Wednesday, 14 February 2018

BRP - 009 Investor Kit Wednesday, 14 February 2018 Top New s PSX Data Portfolio Buy Sell Net A long-running case filed by pensioners from MCB Bank, KSE30 KSE100 KSE ALL FIPI USDmn Habib Bank, United Bank and Allied Bank--the country's Close (Curr.) 21,791 43,690 31,567 13-Feb-18 4.9 (11.9) (6.99) largest scheduled banks-- finally saw their case conclude Close (Prev.) 21,688 43,515 31,480 MTD 58.3 (86.2) (27.9) in the Supreme Court on Tuesday. https://w w w .daw n.com/new s/1389249/bank-pensioners- Chg 103 175 88 CYTD 389.9 (332.1) 57.8 get-meagre-relief-from-apex-court % Chg 0.5% 0.4% 0.3% Foreign Ind. 0.0 (0.0) 0.03 CYTD 7.8% 8.0% 6.0% Foreign Corp. 1.9 (9.1) (7.3) A government's proposal to eliminate subsidy on urea is FYTD -10.1% -6.2% -2.9% Overseas Pak 3.0 (2.7) 0.24 likely to offset the benefit of a three percent reduction in Volume (mn) 62 204 LIPI USDmn sales tax on the key agriculture input, industry officials Value Trade (PKRmn) 4,560 7,565 Individuals 58.25 (54.52) 3.73 said on Tuesday. https://w w w .thenew s.com.pk/print/280642-urea-subsidy- Market Cap (USDbn) 69.7 82.9 Companies 3.59 (2.14) 1.45 elimination-likely-to-offset-tax-incentive Vol Leaders Banks/DFIs 1.57 (3.08) (1.50) Scrip Price Chg Vol NBFC 0.0 (0.1) (0.12) A major basmati rice exporting entity, Matco Foods Ltd, TRG 38.8 (0.4) 11.5 Mutual Fund 6.4 (4.5) 1.84 started trading on the Pakistan Stock Exchange (PSX) on PAEL 57.8 0.4 4.1 Other Org. -

Maple Leaf Cement Factory Limited Annual Report 2001

Maple Leaf Cement Factory Limited Annual Report 2001 Contents Company Information Notice of Meeting Directors' Report Five Years Summary Auditors' Report Balance Sheet Profit and Loss Account Cash Flow Statement Statement of Equity Notes To The Accounts Pattern of Shareholding COMPANY INFORMATION Board of Directors Auditors Mr. Tariq Sayeed Saigol Ford, Rhodes, Robson, Morrow Chairman/Chief Executive Chartered Accountants Mr. Aamir Fayyaz Sheikh Legal Advisors Mr. Sayeed Tariq Saigol 1. Cornelius Lane and Mufti Mr. Waleed Tariq Saigol Advocates & Solicitors, Mr. Zamiruddin Azar Lahore. Rana Muhammad Hanif 2. Mr. Nomaan Akram Raja Mr. Muhammad Riyaz Husain Bokhari Barrister-At-Law (Representing FLS & IFU, Denmark) Raja Mohammad Akram & Co. Mr. Mahmood Ahmed Advocates and Legal Consultants, (Representing Crescent Investment Bank Ltd.) Lahore. Company Secretary Registered Office Mr. Mohammad Sharif 42-Lawrence Road, Lahore. Phone: (042) 6278904-5 Bankers of the Company Fax: (042) 6363184 Muslim Commercial Bank Limited E-mail: [email protected] The Bank of Punjab Allied Bank of Pakistan Limited Factory Soneri Bank Limited Iskanderabad Distt. Mianwali. Habib Bank Limited Phones: (0459) 392237-8 PICIC Commercial Bank Limited United Bank Limited National Bank of Pakistan NOTICE OF THE ANNUAL GENERAL MEETING Notice is hereby given that the 41st Annual General Meeting of the members of Maple Leaf Cement Factory Limited will be held at its Registered Office, 42-Lawrence Road, Lahore on Wednesday, 26th December, 2001 at 10:30 A.M. to transact the following business: 1) To confirm the minutes of last General Meeting. 2) To receive and adopt Audited Accounts of the Company for the year ended June 30, 2001 together with Auditors' and Directors' Reports thereon. -

1966 1969 1970 1972 1974 1978 1979 1981 1982 1985 1986 1987 1990 1993 1993-94 1995 Summary of Piling Works Completed Ivcc

IVCC ENGINEERING (PVT) LTD. Email: [email protected], [email protected] SUMMARY OF PILING WORKS COMPLETED Master Serial Project Particulars Piling Clients No. Footage 1966 47 HYDERABAD-KOTRI, TRAMISSION LINE. 5,901 Dir Gen. Barrages WAPDA & BICC Ltd. Lahore. 49-50 CHINIOT AND MALAKWAL, SUI GAS PIPELINE. 2,008 Motherwell Bridge Contracting Co. Ltd. Karachi. 1969 66 GUDDU, THERMAL POWER STATION. 1,200 The Chief Engineer (Construction) WAPDA, Lahore. 1970 77 MIRPUR (AZAD KASHMIR), ROPEWAY. 911 R.E. AK Logging & Saw Mills Ltd., Mirpur (AK). 80 LAHORE- RIVER RAVI , 220 KV T/L CROSSING. 1,344 WAPDA & Imperial Electric Co. Ltd. Lahore. 1972 88 GUJRANWALA, SUI GAS PIPELINE. 211 Sui Northern Gas Pipelines Ltd., Lahore. 91 TAUNSA, 132 KV TRANSMISSION LINE. 560 Chief Engineer, GSC, WAPDA, Lahore. 1974 108 BHIMBER NULLAH, 220 K.V. T / LINE. 1,296 WAPDA & Societa Anonima Elect. (SAE), Italy. 109 PALKHU NULLAH, 220 KV T / LINE. 300 Chief Engineer, GSC, WAPDA, Lahore. 1978 142 WAH CANTT, SPECIAL FOUNDATIONS. 1,560 Chief Engineer (Works) POF Wah Cantt. 1979 162 CHENAB RIVER CROSSING. 5,748 WAPDA & Greaves Cotton Lahore. 1981 183 RIVER JHELUM, 132 KV TRANSMISSION LINE. 2,000 Project Director GSC,WAPDA Lahore. 1982 196 KHAIRPUR, GRAIN SILOS. 140,000 National Logistic Cell (NLC) GHQ, Rawalpindi. 1985 231 PIPRI, PAKISTAN STEEL. 1,000 Pakistan Steel,MacDonald Layton&Co.Ltd.,Karachi. 233 LAHORE - PIA SALES OFFICE. 9,700 PIA/NCL. 234 TARBELA-FAISALABAD 500 KV T/LINE. 7,383 WAPDA/ICC Lahore. 1986 249 KANDKOT - GUDDU, GAS PIPELINE. 600 WAPDA & Petrocon (Pvt) Ltd., Lahore. 1987 266 LAHORE, 132 KV TRANMISSION LINE. -

Shariah Compliance Screening Report

Al-Hilal Shariah Advisors JUNE 2017 Shariah Compliance Screening Report Al-Hilal Shariah Advisors (Pvt.) Limited. INSIDE Key Highlights ................................ .......................................................................................................... 4 Shariah Compliant Companies ................................ ............................................................................... 8 Shariah Non - Compliant Companies .................................................................................................... 10 Suspended & Delisted Companies…………………………………………………………………………………………………...12 Approved list of Sukuk………………………………………………………………………………………………….....................13 Approved Islamic Banks & Windows for Placements……………….……………………………………………………….14 Approved list of charitable orginizations ............................................................................................. 15 Screening Guidelines for Equity Securities ........................................................................................... 16 Purification Guidelines .......................................................................................................................... 16 P a g e | 2 Al-Hilal Shariah Advisors (Pvt.) Limited. P a g e | 3 Al-Hilal Shariah Advisors (Pvt.) Limited. 14 July, 2017 KEY HIGHLIGHTS We have conducted Shariah compliance screening of 554 selected companies listed on the Pakistan Stock Exchange as per their latest financial statements (June’17), on the basis of the Shariah compliance -

Morgan Stanley Investment Funds 31 December 2016

INVESTMENT MANAGEMENT Société d’Investissement Morgan Stanley à Capital Variable incorporated under Investment Funds the laws of Luxembourg Annual Report December 31, 2016 R.C.S. Luxembourg: B-29. 192 Morgan Stanley Investment Funds 31 December 2016 Table of contents 1 Shareholders’ information 146 Global Bond Fund 2 Board of Directors’ Report 155 Global Buy and Hold 2020 Bond Fund 157 Global Convertible Bond Fund SCHEDULE OF INVESTMENTS 162 Global Credit Fund Equity Funds 170 Global Fixed Income Opportunities Fund 6 Asia Opportunity Fund 182 Global High Yield Bond Fund 8 Asian Equity Fund 189 Global Mortgage Securities Fund 11 Asia-Pacifi c Equity Fund 197 Global Premier Credit Fund 14 Asian Property Fund 201 Short Maturity Euro Bond Fund 16 Breakout Nations Fund 207 US Dollar Corporate Bond Fund 19 Emerging Europe, Middle East and Africa Equity Fund 213 US Dollar High Yield Bond Fund 21 Emerging Leaders Equity Fund 219 US Dollar Short Duration Bond Fund 24 Emerging Markets Equity Fund 224 US Dollar Short Duration High Yield Bond Fund 28 European Champions Fund Liquidity Funds 30 European Equity Alpha Fund 229 US Dollar Liquidity Fund 32 European Property Fund Asset Allocation Funds 35 Eurozone Equity Alpha Fund 230 Diversifi ed Alpha Plus Fund 37 Frontier Emerging Markets Equity Fund 237 Diversifi ed Alpha Plus Low Volatility Fund 40 Global Active Factor Equity Fund 243 Global Balanced Defensive Fund 42 Global Advantage Fund 250 Global Balanced Fund 44 Global Brands Fund 259 Global Balanced Income Fund 46 Global Brands Equity Income Fund -

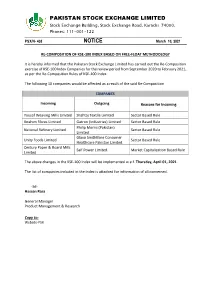

Recomposition of KSE-100 Index

PAKISTAN STOCK EXCHANGE LIMITED Stock Exchange Building, Stock Exchange Road, Karachi-74000, Phones: 111-001-122 PSX/N- 438 NOTICE March 10, 2021 RE-COMPOSITION OF KSE-100 INDEX BASED ON FREE-FLOAT METHODOLOGY It is hereby informed that the Pakistan Stock Exchange Limited has carried out the Re-Composition exercise of KSE-100 Index Companies for the review period from September 2020 to February 2021, as per the Re-Composition Rules of KSE-100 Index. The following 10 companies would be affected as a result of the said Re-Composition. COMPANIES Incoming Outgoing Reasons for Incoming Yousaf Weaving Mills Limited Shahtaj Textile Limited Sector Based Rule Ibrahim Fibres Limited Gatron (Industries) Limited Sector Based Rule Philip Morris (Pakistan) National Refinery Limited Sector Based Rule Limited. Glaxo SmithKline Consumer Unity Foods Limited Sector Based Rule Healthcare Pakistan Limited. Century Paper & Board Mills Saif Power Limited. Market Capitalization Based Rule Limited The above changes in the KSE-100 Index will be implemented w.e.f. Thursday, April 01, 2021. The list of companies included in the Index is attached for information of all concerned. -Sd- Hassan Raza General Manager Product Management & Research Copy to: Website-PSX PAKISTAN STOCK EXCHANGE LIMITED Stock Exchange Building, Stock Exchange Road, Karachi-74000, Phones: 111-001-122 REVISED / RECOMPOSED LIST OF KSE-100 INDEX COMPANIES TO BE IMPLEMENTED W.E.F. April 01, 2021 CLOSE – END MUTUAL FUNDS CEMENT TRANSPORT 01. HBL Growth Fund – A * 36. Cherat Cement Company Ltd 70. Pakistan International Bulk Term. Ltd. * 37. D. G. Khan Cement Co. Ltd MODARABA 38. Fauji Cement Company Ltd. -

National Clearing Company of Pakistan Limited 8Th Floor, Karachi Stock Exchange Building, Stock Exchange Road, Karachi NCCPL/SLB/MARCH-12/16 March 30, 2012

National Clearing Company of Pakistan Limited 8th Floor, Karachi Stock Exchange Building, Stock Exchange Road, Karachi NCCPL/SLB/MARCH-12/16 March 30, 2012 List of Securities Lending and Borrowing (SLB) Eligible Securities Based on the Revised Criteria Dear Clearing Members, We are pleased to inform you that the existing eligibility criteria for the selection of Securities Lending and Borrowing (“SLB”) Eligible Securities have been revised. Accordingly, we are enclosing herewith the revised list of SLB Eligible Securities based on the following revised criteria: A. SLB Eligible Securities - Category A for Short-Selling: 1. Security has been traded at least 80% of the trading days during the review period of last 6 months. 2. Average Impact Cost of the security will not be greater than 2% as calculated based on daily Impact Costs of the review period of last 6 months. 3. Average Daily Traded Volume of security during review period of last six months in the Ready Market selected based on above criteria will not be less than 0.5% of its Free Float or 100,000 shares, whichever is lower. 4. The security is in book entry form. 5. The issuer of security is not placed on the defaulter's counter of the Exchange B. SLB Eligible Securities - Category B for any other: 1. The Listed security is in book entry form. 2. The issuer of security is not placed on the defaulter's counter of the Exchange. List of SLB Eligible Securities for both Categories A & B is attached herewith as Annexure A & B respectively.. Please note that the revised list of SLB Eligible Securities will be effective from Monday April 02, 2012. -

4. Appendices

International Investment Position of Pakistan 2018 4. Appendices 33 State Bank of Pakistan Notification STATE BANK OF PAKISTAN (CENTRAL DIRECTORATE) KARACHI the 1st June, 1971 No.DS.FI./6-71 – Whereas the International Monetary Fund requires the Central Government to furnish certain information and it is essential for the purpose of complying with the request of the International Monetary Fund to require the persons herein mentioned to furnish the information hereby required, the State Bank of Pakistan, in exercise of the powers conferred by sub-section (1) of Section 4 of International Monetary Fund and Bank Act. 1950 (XL-III of 1950), read with the Government of Pakistan, Ministry of Finance Notification No.3(3)IMF/56 dated 4th October, 1956 (vide Gazette of Pakistan dated October 12, 1956), is pleased to direct all persons listed below to furnish all such information as on 31st December of the year under survey specified in the relevant schedules as applicable to the persons mentioned below. The return in the appropriate schedules, duly completed in accordance with the explanation set out below and the instructions appended to the Schedules, shall be made to the Director Statistics, State Bank of Pakistan, Karachi. Serial Number Description Schedule Col.1 Col.2 Col.3 1. Every firm or company registered or incorporated outside Pakistan but operating in Pakistan I 2. Every company (Public or Private Ltd.) incorporated in Pakistan (Under the companies Act VII of 1913) in which any non-resident have any interest of any nature whatsoever, direct or indirect, in respect of its shares, debentures or other obligations, etc. -

Winners List of Best Corporate & Sustainability

WINNERS LIST OF BEST CORPORATE & SUSTAINABILITY REPORT AWARDS 2017 Cherat Packaging Limited declared Overall Top Winner and following companies received the ‘BCSR Awards 2017’ held on 7th August 2018 under respective sectors: POSITION SECTOR / COMPANY POSITION SECTOR / COMPANY BANKS TEXTILE 1st MCB Bank Limited 1st Kohinoor Textile Mills Limited 2nd Allied Bank Limited 2nd Gadoon Textile Mills Limited 3rd Meezan Bank Limited 3rd Sadaqat Limited 4th Bank Alfalah Limited 4th Gul Ahmed Textile Mills Limited FUEL & ENERGY NBFIs 1st Attock Petroleum Limited 1st Jubilee General Insurance Company Limited 2nd Mari Petroleum Company Limited 2nd First Habib Modaraba 3rd Pakistan State Oil Company Limited 3rd EFU Life Assurance Limited 4th Oil and Gas Development Company Limited 4th TPL Insurance Limited 5th Hub Power company Limited 5th EFU General Insurance Limited SUGAR & CEMENT OTHERS 1st Cherat Cement Company Limited 1st Cherat Packaging Limited 2nd Maple Leaf Cement Factory Limited 2nd Pakistan Tobacco Company Limited 3rd Lucky Cement Limited 3rd Synthetic Product Enterprises Limited 4th Thatta Cement Limited 4th Tri Pack Films Limited 5th Shakarganj Limited 5th Cyan Limited CHEMICAL & PHARMACEUTICALS NON-PROFIT ORGANIZATION 1st Fauji Fertilizers Company Limited 1st The Citizens Foundation 2nd Engro Polymers and Chemicals Limited 3rd ICI Pakistan Limited 4th Lotte Chemicals Pakistan Limited 5th Abbot Laboratories (Pakistan) Limited BEST SUSTAINABILITY REPORTS 1st ICI Pakistan Limited ENGINEERING & AUTOS 2nd Attock Refinery Limited 1st Mughal Iron & Steel Industries Limited 3rd Fauji Fertilizer Company Limited 2nd Pak Electron Limited 4th Sadaqat Limited 3rd Al-Ghazi Tractors Limited 5th Crescent Steel and Allied Products Limited 4th Atlas Honda Limited 5th Atlas Battery Limited . -

Annual Report 2020 Building Sustainable Future

ANNUAL REPORT 2020 BUILDING SUSTAINABLE FUTURE We believe in a sustainable development where needs of current are met without compromising the abilities of future generations to meet their own needs. We are striving to achieve economic development with a socially responsible and environment friendly attitude. We are committed to develop more and more renewable energy sources for clean-energy and water re-cycling facilities to stay green and eco-friendly for building a sustainable future. IN THIS REPORT 05 ORGANISATIONAL OVERVIEW AND EXTERNAL ENVIRONMENT 27 STRATEGY AND RESOURCE ALLOCATION 32 RISKS AND OPPORTUNI- TIES The Company continues to ensure that its current competitive position is maintained as well as supporting the ongoing improvement process in our endeavor to maintain world’s best manufacturing practice. Operations of the Company are subject to different environmental and labour laws. The Company is fully complying with all applicable environmental, labour, corporate and other relevant legal laws. 02 KOHINOOR TEXTILE MILLS LIMITED 112 OUTLOOK 116 PERFORMANCE 38 AND POSITION CORPORATE BRIEFING 138 FINANCIAL 93 STATEMENTS STAKEHOLDERS RELATIONSHIP 203 AND CONSOLIDATED ENGAGEMENT FINANCIAL STATEMENTS 107 CORPORATE SUSTAINABILITY ANNUAL REPORT 2020 03 2020 YEAR AT A GLANCE 04 KOHINOOR TEXTILE MILLS LIMITED ORGANISATIONAL OVERVIEW AND EXTERNAL ENVIRONMENT Company Profile & Principal Business Activities 06 Our Vision & Mission 12 Our Values 15 Code of Business Conduct and Ethical Principles 16 Culture 17 Corporate Strategy 17 Group Structure 18 Organization Chart 19 Position in Value Chain 21 Factors Effecting External Environment 22 ANNUAL REPORT 2020 05 COMPANY PROFILE & PRINCIPAL BUSINESS ACTIVITIES KOHINOOR TEXTILE MILLS LIMITED (“THE COMPANY”) COMMENCED TEXTILE OPERATIONS IN 1953 AS A PRIVATE LIMITED COMPANY AND BECAME A PUBLIC LIMITED COMPANY IN 1968. -

Sr.No. Name of Facility Address of Facility Balochistan District Kalat 1 Mondelez International B-182, H

Industrial Radiation Facilities with License Valid upto 30-06-2020 Sr.No. Name of Facility Address of Facility Balochistan District Kalat 1 Mondelez International B-182, H. I. T. E, Hub, Kalat District Lasbela Mauza Chaichai, 44 Km, Main R. C. D. Highway, Hub, Tehsil Gadani, Distt. DG Khan Cement Co. 1 Lasbela District Quetta 1 Ubaid Trading Company C/O Pakistan Flour Mills, N-25, Western By-Pass, Quetta District Naseerabad 1 Uch-II Power (Pvt.) Ltd. Dera Murad Jamali, Distt. Naseerabad, Balochistan Captital District Islamabad 1 Dowell Schlumberger Western S. A. Plot No. 267-268, Industrial Area, I-9/2, Islamabad 2 Eastern Testing Services (Pvt.) Ltd. Plot No. 127-128, Street No. 8, I-10/3, Islamabad 3 Haidri Beverages (Pvt.) Ltd. CDA Industrial Triangle Kahuta Road, Islamabad 4 Halliburton Worldwide Limited Plot No. 18/20, Sector I-9/2, Industrial Area, Service Road West, Islamabad 5 National Centre for NDT (NCNDT) Plot No. 234, Street No. 7, Sector I-9/2, Industrial Area, Islamabad 6 Oil and Gas Development Company Limited (OGDCL.) Street No. 10, Sector I-9/2, Near Masjid Kibriya, Islamabad 7 Schlumberger Seaco Inc. Plot No. 267-269, Industrial Area I-9/2, Islamabad 8 Weatherford Oil Tool M. E. Ltd. Plot No. 208, 209 & 210, Sector I-10/3, Islamabad K.P.K District Haripur 1 Bestway Cement Ltd. Suraj Gali Road, Haripur 2 Bestway Cement Ltd. Farooqia 12 Km, Taxila-Haripur Road, Haripur 3 Dewan Cement Ltd. (Old Saddi Cement Ltd.) Village Kamilpur, Haripur 4 Horizon Paper & Board Mills (Pvt.) Ltd.