Durham Research Online

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Boisdale of Bishopsgate Whisky Bible

BOISDALE Boisdale of Bishopsgate Whisky Bible 1 All spirits are sold in measures of 25ml or multiples thereof. All prices listed are for a large measure of 50ml. Should you require a 25ml measure, please ask. All whiskies are subject to availability. 1. Springbank 10yr 19. Old Pulteney 17yr 37. Ardbeg Corryvreckan 55. Glenfiddich 21yr 2. Highland Park 12yr 20. Glendronach 12yr 38. Ardbeg 10yr 56. Glenfiddich 18yr 3. Bowmore 12yr 21. Whyte & Mackay 30yr 39. Lagavulin 16yr 57. Glenfiddich 15yr Solera 4. Oban 14yr 22. Royal Lochnagar 12yr 40. Laphroaig Quarter Cask 58. Glenfarclas 10yr 5. Balvenie 21yr PortWood 23. Talisker 10yr 41. Laphroaig 10yr 59. Macallan 18yr 6. Glenmorangie Signet 24. Springbank 15yr 42. Ardbeg Uigeadail 60. Highland Park 18yr 7. Suntory Yamazaki DR 25. Ailsa Bay 43. Tomintoul 16yr 61. Glenfarclas 25yr 8. Cragganmore 12yr 26. Caol Ila 12yr 44. Glenesk 1984 62. Macallan 10yr Sherry Oak 9. Brora 30yr 27. Port Charlotte 2008 45. Glenmorangie 25yr QC 63. Glendronach 12yr 10. Clynelish 14yr 28. Balvenie 15yr 46. Strathmill 12yr 64. Balvenie 12yr DoubleWood 11. Isle of Jura 10yr 29. Glenmorangie 18yr 47. Glenlivet 21yr 65. Aberlour 18yr 12. Tobermory 10yr 30. Macallan 12yr Sherry Cask 48. Macallan 12yr Fine Oak 66. Auchentoshan 3 Wood 13. Glenfiddich 26yr Excellence 31. Bruichladdie Classic Laddie 49. Glenfiddich 12yr 67. Dalmore King Alexander III 14. Dalwhinnie 15yr 32. Chivas Regal 18yr 50. Monkey Shoulder 68. Auchentoshan 12yr 15. Glenmorangie Original 33. Chivas Regal 25yr 51. Glenlivet 25yr 69. Benrinnes 23yr 2 16. Bunnahabhain 12yr 34. Dalmore Cigar Malt 52. Glenlivet 12yr 70. -

2019 Scotch Whisky

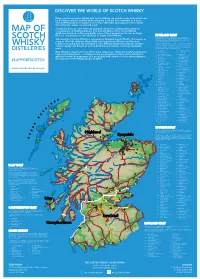

©2019 scotch whisky association DISCOVER THE WORLD OF SCOTCH WHISKY Many countries produce whisky, but Scotch Whisky can only be made in Scotland and by definition must be distilled and matured in Scotland for a minimum of 3 years. Scotch Whisky has been made for more than 500 years and uses just a few natural raw materials - water, cereals and yeast. Scotland is home to over 130 malt and grain distilleries, making it the greatest MAP OF concentration of whisky producers in the world. Many of the Scotch Whisky distilleries featured on this map bottle some of their production for sale as Single Malt (i.e. the product of one distillery) or Single Grain Whisky. HIGHLAND MALT The Highland region is geographically the largest Scotch Whisky SCOTCH producing region. The rugged landscape, changeable climate and, in The majority of Scotch Whisky is consumed as Blended Scotch Whisky. This means as some cases, coastal locations are reflected in the character of its many as 60 of the different Single Malt and Single Grain Whiskies are blended whiskies, which embrace wide variations. As a group, Highland whiskies are rounded, robust and dry in character together, ensuring that the individual Scotch Whiskies harmonise with one another with a hint of smokiness/peatiness. Those near the sea carry a salty WHISKY and the quality and flavour of each individual blend remains consistent down the tang; in the far north the whiskies are notably heathery and slightly spicy in character; while in the more sheltered east and middle of the DISTILLERIES years. region, the whiskies have a more fruity character. -

Silicon Cities Silicon Cities Supporting the Development of Tech Clusters Outside London and the South East of England

Policy Exchange Policy Silicon Cities Cities Silicon Supporting the development of tech clusters outside London and the South East of England Eddie Copeland and Cameron Scott Silicon Cities Supporting the development of tech clusters outside London and the South East of England Eddie Copeland and Cameron Scott Policy Exchange is the UK’s leading think tank. We are an educational charity whose mission is to develop and promote new policy ideas that will deliver better public services, a stronger society and a more dynamic economy. Registered charity no: 1096300. Policy Exchange is committed to an evidence-based approach to policy development. We work in partnership with academics and other experts and commission major studies involving thorough empirical research of alternative policy outcomes. We believe that the policy experience of other countries offers important lessons for government in the UK. We also believe that government has much to learn from business and the voluntary sector. Trustees Daniel Finkelstein (Chairman of the Board), David Meller (Deputy Chair), Theodore Agnew, Richard Briance, Simon Brocklebank-Fowler, Robin Edwards, Richard Ehrman, Virginia Fraser, David Frum, Edward Heathcoat Amory, Krishna Rao, George Robinson, Robert Rosenkranz, Charles Stewart-Smith and Simon Wolfson. About the Authors Eddie Copeland – Head of Unit @EddieACopeland Eddie joined Policy Exchange as Head of the Technology Policy Unit in October 2013. Previously he has worked as Parliamentary Researcher to Sir Alan Haselhurst, MP; Congressional intern to Congressman Tom Petri and the Office of the Parliamentarians; Project Manager of global IT infrastructure projects at Accenture and Shell; Development Director of The Perse School, Cambridge; and founder of web startup, Orier Digital. -

Boisdale of Canary Wharf Whisky Bible

BOISDALE Boisdale of Canary Wharf Whisky Bible 1 All spirits are sold in measures of 25ml or multiples thereof. All prices listed are for a large measure of 50ml. Should you require a 25ml measure, please ask. All whiskies are subject to availability. 1. Springbank 10yr 19. Old Pulteney 12yr 37. Ardbeg Corryvreckan 55. Longmorn 16yr 2. Highland Park 12yr 20. Aberfeldy 12yr 38. Smokehead 56. Glenrothes Select Reserve 3. Bowmore 12yr 21. Blair Athol 12yr 39. Lagavulin 16yr 57. Glenfiddich 15yr Solera 4. Oban 14yr 22. Royal Lochnagar 12yr 40. Laphroaig Quarter Cask 58. Glenfarclas 10yr 5. Cragganmore 12yr 23. Talisker 10yr 41. Laphroaig 10yr 59. Ben Nevis 12yr 6. Fettercairn (Old) 10yr 24. Laphroaig 15yr 42. Octomore 7.1 60. Highland Park 18yr 7. Benromach 10yr 25. Benriach Curiositas 10yr 43. Tomintoul 16yr 61. Glenfarclas 40yr 105 8. Ardmore Traditional 26. Caol Ila 12yr 44. Glengoyne 10yr 62. Macallan 10yr Sherry Oak 9. Connemara Peated 27. Port Charlotte 2008 45. Cardhu 12yr 63. Glendronach 12yr 10. St. George’s Chapter 9 28. Loch Lomond 12yr 46. An Cnoc 16yr 64. Balvenie 12yr DoubleWood 11. Isle of Jura 10yr 29. Speyburn 10yr 47. Glenkinchie 12yr 65. Aberlour 10yr 12. Glen Garioch 21yr 30. Balblair 1997 48. Macallan 12yr Fine Oak 66. Glengoyne 12yr 13. Tobermory 10yr 31. Bruichladdie Classic 49. Glenfiddich 12yr 67. Penderyn Madeira 14. Dalwhinnie 15yr Laddie 50. Bushmills 10yr 68. Glen Moray 12yr 15. Glenmorangie Original 32. Tullibardine 223 51. Tomatin 12yr 69. Glen Grant 10yr 16. Bunnahabhain 12yr 33. Tomatin 18yr 52. Glenlivet 12yr 70. -

GRI-Rapport 2016:2 Bank Management

Gothenburg Research Institute GRI-rapport 2016:2 Bank Management Banks and their world view contexts Sten Jönsson © Gothenburg Research Institute All rights reserved. No part of this report may be repro- duced without the written permission from the publisher. Gothenburg Research Institute School of Business, Economics and Law at University of Gothenburg P.O. Box 600 SE-405 30 Göteborg Tel: +46 (0)31 - 786 54 13 Fax: +46 (0)31 - 786 56 19 E-post: [email protected] ISSN 1400-4801 Layout: Henric Karlsson Banks and their world view contexts By Sten Jönsson Gothenburg Research Institute (GRI) School of Business, Economics and Law University of Gothenburg Contents Introduction 8 1. Preliminaries 13 1.1. Theoretical orientation 13 1.2. What is a bank anyway? 15 1.3. The changing nature of arbitrage 16 1.4. A quick tour of the world views that set the stage for banking 18 2. Greed, arbitrage, and decency in action 22 2.1. Greed – the original sin! 22 2.2. An overview of wealth and the afterlife during the first centuries AD 24 3. Scholasticism – guiding individuals to proper use of their free will 26 4. The most prominent banks – watched by the scholastics 32 4.1. Medici 32 4.2. Fugger 37 5. Mercantilism – the origins of political economy and, consequently, of economic policy 42 5.1. The glory and decline of merchant banks 45 6. Neoliberalim started with the Austrian School 59 6.1. Modernism and crumbling empires 59 6.2. The context in which the Austrian school developed 61 6.3. -

Jak Rozwijać Klaster

Jak rozwija ć klaster - praktyczny przewodnik Jak rozwija ć klaster - praktyczny przewodnik DTI nap ędza nasze ambicje -„bogactwo dla wszystkich” poprzez prace na rzecz stworzenia lepszego środowiska sukcesu biznesowego w Wielkiej Brytanii. Pomagamy ludziom i przedsi ębiorstwom w osi ągni ęciu wi ększej produktywno ści poprzez promowanie przedsiębiorstw, innowacyjno ści oraz kreatywno ści. Wspieramy brytyjski biznes w kraju i zagranic ą. Silnie inwestujemy w światowej klasy nauk ę oraz technologie. Chronimy prawa ludzi pracuj ących oraz konsumentów. Opowiadamy si ę za uczciwymi i otwartymi rynkami w Wielkiej Brytanii, Europie i na całym świecie. 2 Jak rozwija ć klaster - praktyczny przewodnik dti Jak rozwija ć klaster - Praktyczny Przewodnik Raport przygotowany dla Departamentu Handlu i Przemysłu oraz angielskich Regionalnych Agencji Rozwoju (RDAs) przez firm ę Ecotec Research & Consulting 3 Jak rozwija ć klaster - praktyczny przewodnik SPIS TRE ŚCI SPIS TRE ŚCI Przedmowa 5 1. Wprowadzen 7 ie CZ ĘŚĆ A Strategia klastra 2. Rozwój strategii opartych na klastrach 12 3. Mierzenie (ocena) rozwoju klastrów 19 CZ ĘŚĆ B: ‘Co działa”?: Polityka działania w celu wspierania klastrów 4. Krytyczne czynniki sukcesu 25 5. Czynniki wspieraj ące oraz polityki sukcesu 43 6. Instrumenty komplementarne oraz uwarunkowania polityki sukcesu 54 ZAL ĄCZNIKI A: Przypisy 58 B: Bibliografia 61 C: Słowniczek 69 D: Konsultanci 77 E: Poradnik oceny rozwoju klastra 79 4 Jak rozwij ać klaster - pra ktyc zny przewo dnik Lord Sainsbury PRZEDMOWA W zglobalizowanym i technologicznie zaawansowanym świecie, przedsi ębiorstwa coraz cz ęś ciej ł ącz ą si ę w celu wygenerowania wi ększej konkurencyjno ści. To zjawisko – klastrowanie (clustering) – jest widoczne na całym świecie. -

Boisdale of Mayfair Whisky Bible

BOISDALE Boisdale of Mayfair Whisky Bible 1 All spirits are sold in measures of 25ml or multiples thereof. All prices listed are for a large measure of 50ml. Should you require a 25ml measure, please ask. All whiskies are subject to availability. 1. Springbank 10yr 19. Old Pulteney 17yr 37. Ardbeg Corryvreckan 55. Glenfiddich 21yr 2. Highland Park 12yr 20. Glendronach 12yr 38. Ardbeg 10yr 56. Glenfiddich 18yr 3. Bowmore 12yr 21. Whyte & Mackay 40yr 39. Lagavulin 16yr 57. Glenfiddich 15yr Solera 4. Oban 14yr 22. Royal Lochnagar S. Res. 40. Laphroaig Quarter Cask 58. Glenfarclas 10yr 5. Balvenie 21yr PortWood 23. Talisker 10yr 41. Laphroaig 10yr 59. Macallan 18yr 6. Glenmorangie Signet 24. Springbank 15yr 42. Ardbeg Uigeadail 60. Highland Park 18yr 7. Suntory Yamazaki 18yr 25. Ailsa Bay 43. Tomintoul 16yr 61. Glenfarclas 25yr 8. Cragganmore 12yr 26. Caol Ila 12yr 44. Glenesk 1984 62. Macallan 10yr Sherry Oak 9. Brora 25yr 2008 27. Port Charlotte 2008 45. Glenmorangie 25yr QC 63. Glendronach 12yr 10. Clynelish 14yr 28. Balvenie 15yr 46. Strathmill 12yr 64. Balvenie 12yr DoubleWood 11. Isle of Jura 10yr 29. Glenmorangie 18yr 47. Glenlivet 21yr 65. Aberlour 18yr 12. Tobermory 15yr 30. Macallan 12yr Sherry 48. Macallan 12yr Fine Oak 66. Auchentoshan 3 Wood 13. Glenfiddich 26yr Excellence Cask 49. Glenfiddich 12yr 67. Dalmore King Alexander III 14. Dalwhinnie 15yr 31. Bruichladdie Classic Laddie 50. Monkey Shoulder 68. Auchentoshan 12yr 15. Glenmorangie Original 32. Chivas Regal 18yr 51. Glenlivet 25yr 69. Benrinnes 23yr 2 16. Bunnahabhain 12yr 33. Chivas Regal 25yr 52. Glenlivet 12yr 70. -

ECON the Corridor Strategies in the Megacity Development

Wenjing L, Zhongyin S, Li XU The Spatial Strategies of Knowledge Corridors in Megacity Development Case Study Paper The Spatial Strategies of Knowledge Corridors in Megacity Development: Case Study of the Optical Valley Knowledge Corridor, China Wenjing LUO, Wuhan Planning & Design Institute; China Zhongying SONG, Wuhan Planning & Design Institute; China LI XU, Wuhan Planning & Design Institute; China Abstract As a comprehensive spatial concept, corridors especially mega-corridors and knowledge corridors have played irreplaceable roles in developing megacities. This paper uses the case of the Optical Valley Knowledge Corridor in China as an example to illustrate how to make spatial strategies of knowledge corridors in the dimensions of innovation networks, knowledge economies, environments and urban amenities, transportation systems and urban governance towards making a liveable, sustainable and efficient megacity in the backgrounds of knowledge-based urban development. Keywords Corridors, Knowledge-based urban development, Knowledge economies, Megacities 1. Introduction Originated from the linear city model more than a century ago, the term “corridor” is not only an urban model fully tailored to the transport technology but also a comprehensive spatial concept in dimensions of infrastructures, economics, urbanizations and ecology. It is in the 1990s that the modern version of the corridor concept namely mega-corridor has been brought up in the Europe 1992 project, which aimed at the physical integration of European Territory. Especially with the addition of a prefix “mega”, mega-corridors have been assumed to play key roles not only in physical but economic integrations together with the cross-border and transnational infrastructures. In a similar way, cities especially megacities are also growing out of their borders towards regional collaboration, which has given a new role for corridors in the aspects of achieving spatial, economic and social integrations to enhance regional competitiveness. -

Auction Lot List

Lot No Lot Tittle Size Low High NV Orphan Barrel 26 Year Old Single Malt 1 x 750ml 250 380 1 Scotch Whisky, Forager's Keep (2019), Bottled by Orphan Barrel Whiskey Company NV Orphan Barrel 26 Year Old Single Malt Scotch Whisky, Forager's Keep (2019), Bottled by Orphan Barrel Whiskey Company Lot Details 48% NV Booker's Straight Bourbon Whiskey, 30th 1 x 750ml 300 450 2 Anniversary (2018), James B. Beam Distilling Co. (owc) NV Booker's Straight Bourbon Whiskey, 30th Anniversary (2018), James B. Beam Distilling Co. 62.90% Lot Details NV Buffalo Trace Straight Bourbon Whiskey, 3 x 375ml 380 550 3 Single Oak Project, Barrel #22, Buffalo Trace Distillery (375ml) (3 oc) NV Buffalo Trace Straight Bourbon Whiskey, Single Oak Project, Barrel #22, Buffalo Trace Distillery (375ml) Lot Details 45%; two base neck, one top shoulder; one capsule nicked NV Eagle Rare 17 Year Old Straight Bourbon 1 x 750ml 850 1300 4 Whiskey (2018 bottling), Buffalo Trace Distillery NV Eagle Rare 17 Year Old Straight Bourbon Whiskey (2018 bottling), Buffalo Trace Distillery 50.5% Lot Details NV Elijah Craig 23 Year Old Straight Bourbon 1 x 750ml 250 380 5 Whiskey, Barrel #102 (2018), Elijah Craig Distillery (Heaven Hill) NV Elijah Craig 23 Year Old Straight Bourbon Whiskey, Barrel #102 (2018), Elijah Craig Distillery (Heaven Hill) Lot Details 45% NV Elijah Craig 18 Year Old Single Barrel 1 x 750ml 180 280 6 Straight Bourbon Whiskey (2018), Elijah Craig Distillery (Heaven Hill) NV Elijah Craig 18 Year Old Single Barrel Straight Bourbon Whiskey (2018), Elijah Craig Distillery -

Innovation and Regional Competitiveness

The Spatial Dimensions of Knowledge Flows: Implications for Innovation Policy Philip McCann University of Groningen Special Adviser to the EU Commissioner for Regional Policy Johannes Hahn Features of Knowledge • Knowledge is: - sticky with respect to institutions, organisations and location - sticky with respect to geography and location – clustering • Issue of boundaries or barriers to knowledge or innovation • Issue of systems of knowledge or innovation Features of Innovation • Features of Innovation: (i) newness (ii) improvement (iii) reduction of uncertainty by creation of a monopoly position • Types of Innovation (OECD Oslo Manual): (i) product innovation (ii) process innovation (iii) radical innovation – new products to market Systems of Innovation • Sectoral innovation systems (SIS) Technological systems of innovation (TIC) National systems of innovation (NIS) Regional systems of innovation (RIS) • Which specific innovation system is dominant depends on the context: the prevailing industrial, organizational and geographical structure Systems of Innovation • Innovation via large firms with large R&D budgets • Innovation via groups of SMEs • Innovations via networks of firms and organisations • Innovation via publicly funded universities and research institutes • Systems mixtures of each Agglomeration and Clustering • Sources of externalities - Knowledge spillovers (learning) - Non-traded specialist inputs (sharing) - Specialist skilled labour pool (matching) Outcomes of externalities - Localisation economies - Urnanisation economies -

Islay Whisky Adventure Itinerary

scotland.nordicvisitor.com ISLAY WHISKY ADVENTURE ITINERARY DAY 1 DAY 1: ARRIVAL TO EDINBURGH When you arrive in Scotland, make your way into Edinburgh city centre where your hotel will be located. Many travellers opt to take public transport, but for a more direct and comfortable journey, we will be happy to organise a private airport transfer for you. For those arriving early in the day, we recommend spending the afternoon walking around the city, strolling along the Royal Mile and exploring the Old and New Towns, a UNESCO World Heritage Site. There are also plenty of museums and landmarks to visit within the city centre, including the majestic Edinburgh Castle. You could also take in the largest private collection of whisky in the world at the Scotch Whisky Experience or taste some unique drams at the Scotch Malt Whisky Society. Spend the night at Nira Caledonia or similar. Attractions: Edinburgh, Edinburgh Castle, Edinburgh New Town, Edinburgh Old Town, Scotch Malt Whisky Society, Scotch Whisky Experience, The Royal Mile & St Giles Cathedral DAY 2 DAY 2: TRAVEL THROUGH DRAMATIC SCENERY TO ISLAY Today your driver-guide will pick you up from your accommodation to start our trip toward the west coast. We will pass through Stirlingshire and the Loch Lomond and Trossachs National Park, to reach the charming seaside town of Oban. Here we will have have our first whisky experience at the Oban Distillery. There will be time afterwards to enjoy some lunch and explore the town. We‘ll then drive south past sea lochs and inlets to the historic valley of Kilmartin Glen. -

Global City Theory in Question: the Case of London and the Logics of Capital

GLOBAL CITY THEORY IN QUESTION: THE CASE OF LONDON AND THE LOGICS OF CAPITAL Dissertation Presented in Partial Fulfillment of the Requirements for the Degree Doctor of Philosophy in the Graduate School of The Ohio State University By Delphine Ancien, M.A. * * * * * The Ohio State University 2008 Dissertation Committee: Approved by Professor Kevin R. Cox, Adviser Professor Nancy Ettlinger ________________________ Professor Edward J. Malecki Adviser Geography Graduate Program Professor Darla K. Munroe Copyright by Delphine Ancien 2008 ABSTRACT Since the 1980s the greater London area has been home to an increasingly large proportion of the British population, economic activities and profits; its population growth has been quite phenomenal. Many observers over the past few years have been warning that this growth threatens to be self-inhibiting. This has to do with London’s escalating housing costs. Housing shortages in turn tend to create labor shortages in low- skilled low-paying jobs as much as for middle-and-higher-income positions. This problem is quite common in large economically-booming cities, and even more so in what have been identified as ‘world’ or ‘global cities’, such New York City, Tokyo, and London. These cities are characterized, in particular, by their concentration of command and control functions of the world economy, and especially global financial functions. These have become a crucial aspect of capitalism in an era of increased globalization and financialization of capital. However, although the world city and global city literatures appear as a very important departure point for analyzing London’s housing crisis and, crucially from the standpoint of this dissertation, the ways different agents and coalitions of actors have been approaching this issue, I argue that it is necessary to go beyond the rather standard world/global city accounts that have ensued.