Cambridge Family Enterprise Group

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Maranello World Spiel Maranello Mit Das Magazin Fürferraristi Gelungenes Facelift Portofino M

AUSGABE 4-2020 # 119 WORLD MARANELLO WORLD DAS MAGAZIN FÜR FERRARISTI MARANELLO MARANELLO MIT GROSSEM WEIHNACHTS GEWINN SPIEL Deutschland € 9,80 · Österreich € 11,50 · Schweiz CHF 15,70 · Luxemburg/Belgien € 11,80 · Italien 12,80 Deutschland € 9,80 · Österreich 11,50 Schweiz CHF 15,70 Luxemburg/Belgien FERRARI ROMA PORTOFINO M FORMEL 1 EVENTS 2020 ERSTE FAHREINDRÜCKE GELUNGENES FACELIFT 1000 GRANDS PRIX HISTORIC RACING MaranelloWorld4-20EberleinZW.indd 1 12.10.20 12:41 EDITORIAL Liebe Ferraristi, mit einem lachenden und einem weinenden Auge wird Sebastian Vettel am Ende der Saison die Scuderia Ferrari verlassen und ein neues Kapitel in seiner Motorsport-Biografie aufschlagen. 2015 war er zu Ferrari gekommen, als vierfacher Weltmeister im Red Bull Racing Team. Die Fußstapfen, in die er trat, waren dennoch riesig, denn Michael Schumacher hatte immerhin fünf Weltmeis- tertitel für die Roten geholt, Doch die Epoche Schumi lag zehn Jah- re zurück, und außerdem galten seit Einführung der 1,6-Liter-Tur- bomotoren mit zusätzlichem Elektroantrieb völlig andere Regeln. Ferrari war bei der technischen Entwicklung ganz vorne dabei und genoss einen klaren Favoritenstatus. Mit seinem ersten Sieg im zweiten Rennen für die Scuderia schürte Sebastian Vettel große Hoffnungen, doch mehr als zwei Vize-Weltmeistertitel hinter Le- wis Hamilton im überragenden Mercedes (2017 und 2018) waren für den Heppenheimer in den sechs Jahren nicht drin. In der vor- letzten Saison verschlechterte sich die Bilanz der Scuderia zuse- hends, und doch kam die Meldung von seinem Rücktritt Mitte Mai 2020 einigermaßen überraschend. Sebastian verhält sich wie ein englischer Gentleman, der mit steifer Oberlippe die letzten Grands Prix der Corona-Saison 2020 mit Anstand über die Bühne bringt und sich trotz offensichtlicher Defizite von Team und Arbeitsge- rät mit Kritik vornehm zurückhält. -

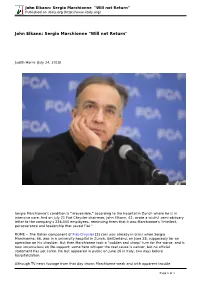

John Elkann: Sergio Marchionne "Will Not Return" Published on Iitaly.Org (

John Elkann: Sergio Marchionne "Will not Return" Published on iItaly.org (http://www.iitaly.org) John Elkann: Sergio Marchionne "Will not Return" Judith Harris (July 24, 2018) Sergio Marchionne's condition is "irreversible," according to the hospital in Zurich where he is in intensive care. And on July 21 Fiat Chrysler chairman, John Elkann, 42, wrote a wistful semi-obituary letter to the company's 236,000 employees, reminding them that it was Marchionne's "intellect, perseverance and leadership that saved Fiat." ROME -- The Italian component of Fiat-Chrysler [2] cars was already in crisis when Sergio Marchionne, 66, was in a university hospital in Zurich, Switzerland, on June 28, supposedly for an operation on his shoulder. But then Marchionne took a "sudden and sharp" turn for the worse, and is now unconscious on life-support; some here whisper the real cause is cancer, but no official statement has yet come. He last appeared in public on June 26 in Italy, two days before hospitalization. Although TV news footage from that day shows Marchionne weak and with apparent trouble Page 1 of 3 John Elkann: Sergio Marchionne "Will not Return" Published on iItaly.org (http://www.iitaly.org) breathing, some Italian press accounts say that the situation "precipitated almost without warning" while others spoke of an "unspecified aggressively infectious disease" only recently diagnosed. Whatever the cause, no improvement will come, for his condition is "irreversible," according to the hospital; and on July 21 Fiat Chrysler chairman, John Elkann, 42, wrote a wistful semi-obituary letter to the company's 236,000 employees, reminding them that it was Marchionne's "intellect, perseverance and leadership that saved Fiat." Marchionne, born in Italy but raised in Canada, took over the then failing 119-year-old Fiat company [3] in 2004. -

96 Pagine Interne Layout 1 16/05/11 12:59 Pagina 3 96 Pagine Interne Layout 1 16/05/11 12:59 Pagina 4

96 pagine interne_Layout 1 16/05/11 12:59 Pagina 3 96 pagine interne_Layout 1 16/05/11 12:59 Pagina 4 ASSOCIAZIONE NAZIONALE INDUSTRIE CINEMATOGRAFICHE AUDIOVISIVE E MULTIMEDIALI - LA PRODUZIONE ITALIANA 2010 LA PRODUZIONE ITALIANA 2010 THE ITALIAN PRODUCTION Edito da ANICA I film compresi nel catalogo sono Associazione Nazionale Industrie lungometraggi di produzione italiana forniti Cinematografiche Audiovisive e Multimediali di visto censura nell’anno 2010 In collaborazione con il cast e crediti non contrattuali Ministero per i Beni e le Attività Culturali Direzione Generale per il Cinema ANICA Viale Regina Margherita, 286 A cura dell’Ufficio Stampa ANICA 00198 Roma (Italia) Tel. +39 06 4425961 Coordinatore Editoriale Fax +39 06 4404128 Paolo Di Reda email: [email protected] Elaborazioni Informatiche Elenco Inserzionisti Gennaro Bruni Alberto Grimaldi Productions p. XVII con la collaborazione di Cinetecnica 73 Romina Coppolecchia Eurolab 74 Kodak 75 Redazione e reperimento dati Medusa 76 Claudia Bonomo Panalight XXI Antonio Dell’Erario Sound Art V Technicolor II-III Progetto Grafico e impaginazione Una vita per il cinema 72 Selegrafica‘80 s.r.l. Stampa Selegrafica‘80 s.r.l. - Guidonia (Rm) www.selegrafica.it [email protected] Concessionaria esclusiva della pubblicità Fotolito e impianti Via Tor dè Schiavi, 355 - 00171 Roma Composit s.r.l. - Guidonia (Roma) Tel. 06 89015166 - fax. 06 89015167 [email protected] [email protected] - www.apsadvertising.it Le schede complete della produzione italiana 2010 sono consultabili al sito www.anica.it IV 96 pagine interne_Layout 1 16/05/11 12:59 Pagina 5 ità 7 g.it 96 pagine interne_Layout 1 16/05/11 12:59 Pagina 6 ASSOCIAZIONE NAZIONALE INDUSTRIE CINEMATOGRAFICHE AUDIOVISIVE E MULTIMEDIALI - LA PRODUZIONE ITALIANA 2010 ELENCO REGISTI LIST OF DIRECTORS A D I Adriatico, Andrea pag. -

Copyrighted Material

Part I THE POWER OF A FAMILY COPYRIGHTED MATERIAL cc01.indd01.indd 1111 005/11/115/11/11 22:01:01 PPMM cc01.indd01.indd 1122 005/11/115/11/11 22:01:01 PPMM Chapter 1 The Scattered Pieces short time before he died, Gianni Agnelli had asked his younger brother Umberto, who had come to visit him every A day at Gianni’s mansion on a hill overlooking Turin, to do something very diffi cult. Umberto said he needed to think about it. Now, at the end of January 2003, Umberto had come to give Gianni an answer. Gianni was confi ned to a wheelchair, spending his fi nal days at home. He had once found solace looking out of the window onto his wife Marella’s fl ower gardens below, especially his favorites, the yellow ones. But now it was winter. Gianni looked out at the city of Turin, which was visible across the river through the bare trees. Street after street stretched out toward the horizon in the crisp January air, lined up like an army of troops marching to meet the Alps beyond. It was a clear day, and he could see Fiat’s white Lingotto headquarters, as well as the vast bulk of Fiat’s Mirafi ori car factory on the far side of the city. The factories had been built by their grandfather, Giovanni Agnelli. 13 cc01.indd01.indd 1133 005/11/115/11/11 22:01:01 PPMM 14 the power of a family Gianni wouldn’t admit to his family that he was dying, but they all knew. -

Stellantis N.V. (Name of Issuer)

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 SCHEDULE 13D Under the Securities Exchange Act of 1934 (Amendment No. 1) Stellantis N.V. (Name of Issuer) Common Shares, nominal value of €0.01 each (Title of Class of Securities) N82405106 (CUSIP Number) Thierry Mabille de Poncheville Deputy Chief Executive Officer Établissements Peugeot Frères S.A. 66, avenue Charles de Gaulle 92200 Neuilly-sur-Seine, France +33 6 07 48 38 77 (Name, Address and Telephone Number of Person Authorized to Receive Notices and Communications) Copy to: Adam O. Emmerich John L. Robinson Wachtell, Lipton, Rosen & Katz 51 West 52nd Street New York, New York 10019 (212) 403-1000 April 14, 2021 (Date of Event which Requires Filing of this Statement) If the filing person has previously filed a statement on Schedule 13G to report the acquisition that is the subject of this Schedule 13D, and is filing this schedule because of Rule 13d-1(e), 13d-1(f) or 13d-1(g), check the following box. ☐ Note: Schedules filed in paper format shall include a signed original and five copies of the schedule, including all exhibits. See Rule 13d-7 for other parties to whom copies are sent. * The remainder of this cover page shall be filled out for a reporting person’s initial filing on this form with respect to the subject class of securities, and for any subsequent amendment containing information which would alter disclosures provided in a prior cover page. The information required on the remainder of this cover page shall not be deemed to be “filed” for the purpose of Section 18 of the Securities Exchange Act of 1934, as amended (the “Act”) or otherwise subject to the liabilities of that section of the Act but shall be subject to all other provisions of the Act (however, see the Notes). -

The History of Corporate Ownership in Italy

This PDF is a selection from a published volume from the National Bureau of Economic Research Volume Title: A History of Corporate Governance around the World: Family Business Groups to Professional Managers Volume Author/Editor: Randall K. Morck, editor Volume Publisher: University of Chicago Press Volume ISBN: 0-226-53680-7 Volume URL: http://www.nber.org/books/morc05-1 Conference Date: June 21-22, 2003 Publication Date: November 2005 Title: The History of Corporate Ownership in Italy Author: Alexander Aganin, Paolo Volpin URL: http://www.nber.org/chapters/c10273 6 The History of Corporate Ownership in Italy Alexander Aganin and Paolo Volpin 6.1 Introduction Recent contributions show that the Italian corporate governance regime exhibits low legal protection for investors and poor legal enforcement (La Porta et al. 1998), underdeveloped equity markets (La Porta et al. 1997), pyramidal groups, and very high ownership concentration (Barca 1994). Arguably, due to these institutional characteristics, private benefits of con- trol are high (Zingales 1994), and minority shareholders are often expro- priated (Bragantini 1996). How did this corporate governance system emerge over time? In this paper we use a unique data set with information on the control of all companies traded on the Milan Stock Exchange (MSE) in the twentieth century to study the evolution of the stock market, the dynamics of the ownership structure of traded firms, the birth of pyramidal groups, and the growth and decline of ownership by families. We find that all our indicators (stock market development, ownership concentration, separation of ownership and control, and the power of fam- ilies) followed a nonmonotonic pattern. -

Gianni Agnelli and Ferrari. the Elegance of the Legend”, Centenary Exhibition at the Mef Modena

“GIANNI AGNELLI AND FERRARI. THE ELEGANCE OF THE LEGEND”, CENTENARY EXHIBITION AT THE MEF MODENA. ONLINE OPENING ON 12 MARCH, LIVE VIRTUAL TOURS UNTIL 1 APRIL. Maranello, 11 March 2021 – The new exhibition at the Museo Enzo Ferrari in Modena brings together the one-off cars built by Ferrari for Gianni Agnelli and meticulously customised in close collaboration with him. This unique collection is a testament to the symbiotic relationship that developed between two of the most charismatic and authoritative figures of the 20th century and endured for over 50 years. “Gianni Agnelli and Ferrari. The Elegance of the Legend” is an homage by the Maranello marque to one of its greatest touchstones, first and foremost as a loyal client and later as close confidant and partner, on the 100th anniversary of the latter’s birth tomorrow. The official online opening of the exhibition takes place on March 12 on the Ferrari Museums’ social media channels and website. As we wait for new government regulations to allow us to reopen the MEF’s exhibition halls to the public, we will be organising two free virtual live tours of around 30 minutes each day until April 1. These can be booked starting tomorrow at the Museums’ website (Ferrari.com/it-IT/museums). A Prancing Horse enthusiast from a young age, Gianni Agnelli was consistently courteous and respectful in his proposals for highly customised special versions of certain models. For his part, Enzo Ferrari was aware that the influence, aesthetic tastes and personality of a client who was both very close to the factory and familiar with working on exclusive projects, might lead to successful and farsighted choices. -

FOLLIA a GENOVA DI ANDREA MONTI Nel Vergognoso Spettacolo Di Genova C’È GenoaSiena Ostaggio Degli Qualcosa Di Medievale E Di Osceno Che Non Dimenticheremo Facilmente

REDAZIONE DI MILANO VIA SOLFERINO 28 - TEL. 0262821 - REDAZIONE DI ROMA PIAZZA VENEZIA 5 - TEL. 06688281 www.gazzetta.it lunedì 23 aprile 2012 1,20 € POSTE ITALIANE SPED. IN A.P. - D.L. 353/2003 CONV. L. 46/2004 ART. 1, C1, DCB MILANO Annoanno 116 Numeronumero 96 ITALIA LA VERGOGNA MARASSI IN MANO AI TIFOSI GENOANI DOPO IL QUARTO GOL DEL SIENA l©Editoriale DURI CONTRO LA GOGNA FOLLIA A GENOVA DI ANDREA MONTI Nel vergognoso spettacolo di Genova c’è GenoaSiena ostaggio degli qualcosa di medievale e di osceno che non dimenticheremo facilmente. Che non dob ultrà per 44’. Rossoblù biamo dimenticare. Certo, ieri non c’è scap costretti a togliersi la maglia. pato il morto ma la gogna imposta dagli ultrà ai giocatori è un inedito raggelante, Perdono 41. Salta Malesani, unbrividoancestralechevienedirettamen arriva De Canio te dai secoli bui. Gli stessi a cui appartengo no, per architettura e atmosfera, molti dei DA RONCH, GALDI, GRIMALDI ALLE PAGINE 14151617 nostri stadi. 3 Da sin. Preziosi, Rossi con le maglie, Sculli parla con gli ultrà L’ARTICOLO A PAGINA 24 LA VOLATA A 5 GIORNATE DALLA FINE IL PAREGGIO DEL BOLOGNA (11) A SAN SIRO FA AUMENTARE IL DISTACCO JUVE D'ITALIA Bianconeri a valanga con la Roma, +3 sul Milan: scudetto ipotecato Due gol di Vidal nei primi 8‘ chiudono il match SENZA GOL PARI NERAZZURRO A FIRENZE a Torino. Poi la Roma resta in dieci per l’espulsione 3 Arturo Vidal, 24 anni, in tuffo sui di Stekelenburg sul rigore concesso ai bianconeri: compagni per la festa a Pirlo nascosto finisce 40. -

Nber Working Paper Series Corporate Control Around

NBER WORKING PAPER SERIES CORPORATE CONTROL AROUND THE WORLD Gur Aminadav Elias Papaioannou Working Paper 23010 http://www.nber.org/papers/w23010 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts Avenue Cambridge, MA 02138 December 2016 We thank Julian Franks, Rafael La Porta, Florencio Lopez-de-Silanes, and Andrei Shleifer for useful suggestions and comments. All errors are our sole responsibility. The views expressed herein are those of the authors and do not necessarily reflect the views of the National Bureau of Economic Research. NBER working papers are circulated for discussion and comment purposes. They have not been peer-reviewed or been subject to the review by the NBER Board of Directors that accompanies official NBER publications. © 2016 by Gur Aminadav and Elias Papaioannou. All rights reserved. Short sections of text, not to exceed two paragraphs, may be quoted without explicit permission provided that full credit, including © notice, is given to the source. Corporate Control around the World Gur Aminadav and Elias Papaioannou NBER Working Paper No. 23010 December 2016 JEL No. F30,G3,G34,G38,K11,K12,K31 ABSTRACT We provide an autopsy of the patterns of corporate control and ownership concentration in a dataset covering more than 40,000 listed firms from 127 countries over 2004 2012. Employing a plethora of original and secondary sources, big data techniques, and applying the Shapley-Shubik algorithm to quantify shareholder’s voting power we trace ultimate controlling shareholders from the complex, pyramidal, and often obscure corporate structures. First, we show that there are large differences in the type of corporate control (widely held firms with and without significant equity blocks, firms controlled by families, governments, and other public-private firms) across and within continents. -

Annual Report of Proxy Voting Record Date Of

ANNUAL REPORT OF PROXY VOTING RECORD DATE OF REPORTING PERIOD: JULY 1, 2018 - JUNE 30, 2019 FUND: THE VANGUARD GLOBAL ENHANCED EQUITY FUND --------------------------------------------------------------------------------------------------------------------------------------------------------------------------------- ISSUER: 3i Group Plc TICKER: III CUSIP: G88473148 MEETING DATE: 6/27/2019 FOR/AGAINST PROPOSAL: PROPOSED BY VOTED? VOTE CAST MGMT PROPOSAL #1: ACCEPT FINANCIAL STATEMENTS AND ISSUER YES FOR FOR STATUTORY REPORTS PROPOSAL #2: APPROVE REMUNERATION REPORT ISSUER YES FOR FOR PROPOSAL #3: APPROVE FINAL DIVIDEND ISSUER YES FOR FOR PROPOSAL #4: RE-ELECT JONATHAN ASQUITH AS DIRECTOR ISSUER YES FOR FOR PROPOSAL #5: RE-ELECT CAROLINE BANSZKY AS DIRECTOR ISSUER YES FOR FOR PROPOSAL #6: RE-ELECT SIMON BORROWS AS DIRECTOR ISSUER YES FOR FOR PROPOSAL #7: RE-ELECT STEPHEN DAINTITH AS DIRECTOR ISSUER YES FOR FOR PROPOSAL #8: RE-ELECT PETER GROSCH AS DIRECTOR ISSUER YES FOR FOR PROPOSAL #9: RE-ELECT DAVID HUTCHISON AS DIRECTOR ISSUER YES FOR FOR PROPOSAL #10: ELECT COLINE MCCONVILLE AS DIRECTOR ISSUER YES FOR FOR PROPOSAL #11: RE-ELECT SIMON THOMPSON AS DIRECTOR ISSUER YES FOR FOR PROPOSAL #12: RE-ELECT JULIA WILSON AS DIRECTOR ISSUER YES FOR FOR PROPOSAL #13: REAPPOINT ERNST & YOUNG LLP AS AUDITORS ISSUER YES FOR FOR PROPOSAL #14: AUTHORISE BOARD ACTING THROUGH THE ISSUER YES FOR FOR AUDIT AND COMPLIANCE COMMITTEE TO FIX REMUNERATION OF AUDITORS PROPOSAL #15: AUTHORISE EU POLITICAL DONATIONS AND ISSUER YES FOR FOR EXPENDITURE PROPOSAL #16: -

Governance in Brief

Governance in Brief December 3, 2020 Edited by: Martin Wennerström FCA – PSA merger details revealed Fiat Chrysler Automobiles N.V. (“FCA”) and Peugeot S.A. (“PSA”) unveiled the prospectus for their cross-border merger into Stellantis, a Dutch company to be listed in Paris, Milan and New York. PSA – the acquirer “for accounting purposes” – will hold six of the 11 seats on Stellantis’ board headed by FCA Chairman John Elkann, with PSA CEO Carlos Tavares to serve as the firm’s CEO. Following the merger, the holding company of Italy’s Agnelli family is expected to be Stellantis’ largest shareholder with a 14.4% stake, followed by the Peugeot family with a 7.2% stake, the French State with 6.2% and China’s Dongfeng with 5.6%. The initial term of office for Stellantis’ chairman, CEO, senior independent director and vice-chairman will be five years, four in the case of the other directors, with all board members to serve two-year terms thereafter. In addition to a 30% voting cap, Stellantis will implement a controversial loyalty voting structure whereby shareholders holding Stellantis stock for three years can receive one special voting share for each share held. Notably, a September 2020 Amsterdam court ruling called into question the acceptability of loyalty voting rights in a Dutch company. FCA and PSA shareholders will vote on the merger on January 4, 2021. SEC | PSA | FCA | Reuters | Rechtspraak Sasol faces shareholder Australia’s IOOF Holdings holds FRC report highlights poor code stormy meeting explanations backlash Petrochemicals group Sasol faced a Wealth manager IOOF Holdings Ltd saw The UK watchdog Financial Reporting rare rebuke at its 2020 AGM, which saw significant opposition at its 2020 AGM, as Council (“FRC”) released a report a majority of votes (57%) cast against 27% of votes cast opposed the concluding that companies continue to the remuneration report and 28% cast remuneration report, while 26% and 18% treat the revised UK Corporate Governance against the remuneration policy. -

Reviews of Books and Audiobooks in Italian

Reviews of books and audiobooks in Italian Susanna Agnelli (1922-2009), Vestivamo alla marinara, 231pp. (1975). Susanna Agnelli's paternal grandfather founded the Fiat company in 1899. She was thus a member of one of the richest families in Italy. Vestivamo alla marina is an autobiography beginning in childhood and ending with Agnelli's marriage in 1945. The title \We dressed like sailors" refers to the sailor-suits her parents made all the children wear, and gives little hint of what the book is really about. It begins with the sailor-suits and her upbringing under the stern eye of British nanny \Miss Parker", but before long Italy has joined the Axis and the young \Suni", as Susanna was known, is volunteering as a nurse on ships bringing injured soldiers from Africa back to Italy. As a war memoir it is fascinating, including for example an account of the utter confusion and chaos created by the Armistice of September 8, 1943 (Suni was in Rome at the time). Judging by her own account, Suni was a very courageous young woman, but it is only fair to point out that her war experience was highly atypical because of her access to wealth and power. In the middle of the war, she takes a ski vacation in Switzerland. When she and her brother Gianni need a car in Firenze, hoping to get to Perugia where they can hide out in one of their grandfather's numerous houses and await the allied advance, as Agnellis they have only to go to the local Fiat headquarters and they're set.