An International Review of Experiences from On-Demand Public Transport Services

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Parramatta-Liverpool-Bankstown Area Bus Services (Region 13)

Parramatta-Liverpool-Bankstown Area Bus Services (Region 13) FAIRFIELD INSET University of Western Sydney PARRAMATTA INSET FAIRFIELD INSET MAP Parramatta Parramatta Campus PARRAMATTA INSET MAP Hassall St r D Camellia S SEE SEE t m S t h a Camellia r S c t PARRAMATTA PARRHAMarrisA PTaTrkA e r S T d s Station u t h h e u H Station r e C o R f r l C sl INSET INSET e s Rosehill Gardens o y A u D e r r Racecourse t St A m Parramatta R ld llenSt a Parramatta d t e J nS irfi Rosehill Station M92 Ala Fa Church St t Rosehill Interchange t S 904 erS Harris Station t penc P 906 S S a s rr i a Ar r m r 905 ldSt a d Park gyle a fie tta o M Shoppingtown St 909 ir 92 Parramatta H 906 t Fa Rd o n t e G S C sc am St t pb es S4 e t G ell k i r r LIVERPOOL INSET Cr Bold St eatW St Pa P Granville e e t Silverwater stern Th S Stockland M Station Hw s y Station Granville e C e m Mall Neil h Hume H v P wy o a u e St r r V r ia r r W a c e in T illi l m am h d e S M St D a 906 Lachlan St P t erry r tta S y lan t ds R a Rd e South St d W 907 ilw u e Harris a Merrylands n st 907 R Granville e Clyde er 909 Merrylands v n Park t TAFE M Campbell Station A M91 St S Station 909 w 910 e y Station n Granville h (M T 4 Liverpool Park Clyde ) t tt S SS Lou Marshalling oulbur is St Elizabeth G Yards R Liverpool a Olympic Park St w Bigge BiggeBigge Hospital 906 S2 so d Station t d Normanby Rd M90 South R S n 900 R S n t e t Pde l o 901 S l i i t 901 Mona a y TAFE v St Homebush TAFE NSW of Westernllege Sydney t d t S w 902 Mo o Mo ore Liverpool 908 d Concord West ore t St -

Roselands to Bankstown Servicing Lakemba & Greenacre

946 Roselands to Bankstown servicing Lakemba & Greenacre How to use this timetable Fares This timetable provides a snap shot of service information in 24-hour To travel on public transport in Sydney and surrounding regions, an time (e.g. 5am = 05:00, 5pm = 17:00). Information contained in Opal card is the cheapest and easiest ticket option. this timetable is subject to change without notice. Please note that An Opal card is a smartcard you keep and reuse. You put credit onto timetables do not include minor stops, additional trips for special the card then tap on and tap off to pay your fares throughout Sydney, events, short term changes, holiday timetable changes, real-time the Blue Mountains, Central Coast, Hunter and Illawarra, along with information or any disruption alerts. Intercity Trains in the Southern Highlands and South Coast. For the most up-to-date times, use the Trip Planner or Departures on Fares are based on: transportnsw.info • the type of Opal card you use Real-time trip planning • the distance you travel from tap on to tap off You can plan your trip with real-time information using the Trip • the mode of transport you choose Planner or Departures on transportnsw.info or by downloading travel • any Opal benefits such as discounts and capped fares that apply. apps on your smartphone or tablet. Find out about Opal fares and benefits at transportnsw.info/opal The Trip Planner, Departures and travel apps offer various features: • favourite your regular trips Which Opal card is right for you? • see where your service is on the route Adult – For customers 16 years and over who are not entitled to any concessions. -

Annual Report

Annual Report 2019 – 2020 We acknowledge the Traditional Owners and Custodians of country throughout Australia and their continuing connection to the land, water and community. We pay our Respect to Aboriginal and Torres Strait Island Cultures and Elders past, present and emerging. Cover: Sydney, New South Wales This page: Palm Island, Queensland At SeaLink we are dedicated to connecting people, linking communities, sharing experiences, and creating brilliant memories. SeaLink Travel Group 2 Key Results 22 Five Year Financial Highlights 3 Directors’ Report 23 Our Global Operations 4 Financial Report 28 Our Australian Operations 6 Auditor’s Report 75 Community and Sustainability 8 Auditor’s Independence Declaration 81 Chair Report 10 Remuneration Report 82 Review of Operations 12 ASX Additional Information 92 Revenue History 20 Corporate Governance 94 Adelaide, South Australia SEALINK TRAVEL GROUP SeaLink provides innovative SeaLink Travel Group is Australia’s and London underway, an electric bus largest land and marine tourism and trial currently operating in NSW, on and efficient transport public transport service provider with demand services in Sydney, and is part established international operations. of the world’s first hydrogen consortium, the H2OzBus Project. As well as solutions that link people and It is one of Australia’s most experienced operating an eco-tourism resort on and diverse multi-modal transport communities with places and the world heritage listed, Fraser Island businesses, boasting performance-driven and eco experiences -

Drouin and Warragul Bus Services

2017 - September Volume 72 Number 9 $10.00 RRP Incl. GST transit australia australia’s urban passenger transportta journal ISSN 0818 5204 Features Announcements on trams Infrastructure Australia corrridor protection The Battle of Brisbane Revised bus services in Drouin and Warragul St Kilda Road tram replacement Plus Regulars 2017 - September Volume 72 Number 9 contents transit Features australia Announcements on trams ____________________ 261 australia’s urban passenger transportta journal Infrastructure Australia corridor protection _______ 263 Managing Editor: Tony Bailey Publisher: Transit Australia Digital The Battle of Brisbane _________________________ 267 PO Box 192, BOTANY NSW 1455 Revised bus services in Drouin and Warragul ____ 269 Australia Ph: (02) 9341 8700 St Kilda Road tram replacement _______________ 271 E-mail: [email protected] Website: www.transitaustralia.com.au Transit Newsfile Editorial Advisors: Hugh Ballment, Agnes Boskovitz, International ______________________________273 V M Isaacs, Stuart Keenan, L J Pascoe, National __________________________________273 Jeremy Wainwright, R K Willson Advertising: Tony Bailey Ph: (02) 9341 8700 New South Wales ___________________________273 E-mail: [email protected] Northern Territory __________________________ 277 Website Co-ordinator: John Clifton Layout: The Little Website Company Pty Ltd Queensland _______________________________ 279 www.tlwsc.com.au South Australia ____________________________ 279 Subscriptions: Tasmania ________________________________ 280 Print Subscription 2017: Victoria __________________________________ 280 Australia Overseas Airmail, AUD Western Australia _________________________ 284 (incl. GST) Asia/Pacific Zone # Rest of the World Western Pacific ______________________________ 284 Personal $120.00 $190.00 $220.00 New Zealand _____________________________ 284 Corporate $180.00 $220.00 $250.00 South East Asia ___________________________ 285 # Asia/Pacific Zone incl. NZ, PNG, Fiji, Malaysia, India, Japan, China. -

Urban Guidance: Detailed Coverage for Supported Transit Systems

Urban Guidance: Detailed coverage for supported transit systems Andorra .................................................................................................................................................. 3 Argentina ............................................................................................................................................... 4 Australia ................................................................................................................................................. 5 Austria .................................................................................................................................................... 7 Belgium .................................................................................................................................................. 8 Brazil ...................................................................................................................................................... 9 Canada ................................................................................................................................................ 10 Chile ..................................................................................................................................................... 11 Colombia .............................................................................................................................................. 12 Croatia ................................................................................................................................................. -

'We Specialise in Franchising'

interview adam leishman One of 380 buses that Tower Transit Singapore will begin operating later his year ‘We specialise in franchising’ Adam Leishman talks about Tower Transit’s ambitions in Singapore, London and the rest of the UK 2016 will see the 30th If these powers are implemented it will be company as a “franchise specialist”. anniversary of bus a huge change for Britain’s bus sector. Despite The company is a spin-off from Transit deregulation - but will there their opposition to franchising, it seems Systems, a company which won its first tender be a 40th anniversary? For unlikely that the ‘big five’ groups that dominate for bus operation in Perth, Western Australia, the past three decades, the industry will disappear (they’re happy to in 1995. Today the company operates a fleet Robert Jack private operators have operate within the franchised environments of around 1,000 buses in Australia, with Managing Editor played the dominant role of London’s bus market, the railways and contracts across the country. Tower Transit in planning and providing local bus services elsewhere), but could this revolution open up is a separate business, although it does share in England (outside London), Scotland and the market to new entrants? some of the same shareholders as Transit Wales, with local authorities and passenger London-based Tower Transit is one of the Systems. Leishman is one of four Tower transport executives limited to procuring companies that is waiting for this opportunity Transit shareholders, along with chairman Neil ‘non-commercial’ services on the periphery. to emerge. And the group’s Australian chief Smith, who is a co-founder of Transit Systems. -

Annual Report 2018 222 Bus Routes Operated Total

ANNUAL REPORT 2018 CLOSE TO 428 MILLION RAIL PASSENGER TRIPS 222 BUS ROUTES OPERATED TOTAL FLEET OF 192 TRAINS OUR VISION Moving People in a Safe, Reliable and Affordable Way OUR MISSION To achieve excellence for our customers, employees, shareholders and community. To this end, we are committed to delivering safe and reliable services at affordable prices, being an employer of choice, creating significant shareholder value and becoming a socially responsible corporate role model. CORE BELIEFS TO acHIEVE OUR VISION AND MISSION, WE are GUIDED BY THE following BELIEFS: We will: • Be driven by our customers’ needs • Strive for excellence in everything we do • Act with integrity at all times • Treat people with fairness and respect • Maintain safety as a top priority • Collaborate with our partners for a win-win outcome • Give our shareholders a reasonable return Annual Report 2018 01 CONTENTS 02 Chairman’s Statement 60 Financial Statements 06 Group Financial Highlights 61 Directors’ Statement 08 Corporate Information 65 Independent Auditor’s Report 09 Board of Directors 68 Statements of Financial Position 14 Key Management 70 Group Income Statement 18 Operations Review 71 Group Comprehensive Income Statement 24 Sustainability Report 72 Statements of Changes in Equity 30 Corporate Governance 74 Group Cash Flow Statement 50 Directors’ Particulars 75 Notes to the Financial Statements 56 Risk Management 110 Share Price Movement Chart 59 Financial Calendar 111 Shareholding Statistics 112 Notice of Annual General Meeting 116 Additional Information on Directors Seeking Re-Election Proxy Form 02 SBS Transit Ltd IntroDUCTION bus services, of which 12 used to be CHAIRMAN’S under another operator. -

No. 215, July 2010 ISBN 1038-3697 RRP $2.95 Published by the Australian Association of Timetable Collectors

No. 215, July 2010 ISBN 1038-3697 RRP $2.95 Published by the Australian Association of Timetable Collectors www.aattc.org.au JACK McLEAN 1921 – 2010 FOUNDER, AATTC About Table Talk Table Talk is published monthly by the Australian Association of Timetable Collectors Inc. (Registration No. A0043673H) as a journal of record covering recent timetable news items. The AATTC also publishes the Times covering timetable history and analysis. Contributions are very welcome and should be sent to the appropriate Editor. Editor, Rail and Tram, Air, Ferry: Victor Isaacs, 43 Lowanna St Braddon ACT 2612, [email protected] Please note the altered email address . Editor, Bus : Geoff Mann, 19 Rix St Glen Iris Vic 3146, [email protected] Production and Mailout : Geoff and Judy Lambert. Proofreader: Geoff Hassall. Original material appearing in Table Talk may be reproduced in other publications but acknowledgement is required. Membership of the AATTC includes monthly copies of the Times , Table Talk , the Distribution List of timetables, and the twice-yearly Auction catalogue. The membership fee is $55 (Adult) and $33 (Junior) pa. Membership enquiries should be directed to the Membership Officer, P O Box 1253, North Lakes Qld 4509, (07) 3260 5329. JACK McLEAN Our front cover photo shows Jack at a birthday celebration of his model railway, the Wingrove Harbour Railway. Many people gathered every Friday evening to operate the WHR according to authentic safeworking and timetabling principles. And for the good conversation about timetables and other matters. A tribute by Roderick Smith: Jack was active in many railway groups over many decades; he was well known by railway managers from low to top ranks. -

ASX Announcement

ASXMedia Announcement SEALINK TRAVEL GROUP LIMITED Level 3, 26 Flinders Street Adelaide, South Australia 5000 Tel (08) 8202 8688 16 January 2020 www.sealinktravelgroup.com.au SEALINK COMPLETES ACQUISITION OF TRANSIT SYSTEMS GROUP SeaLink’s acquisition of Transit Systems Group was completed today Strategically compelling acquisition creating a leading Australian multi-modal transport provider, with established international operations in Singapore and United Kingdom Transit Systems Group is a highly scalable operating platform, with a strong track record of contract wins and renewals, and an experienced management team operating typically long- term, low-risk, CPI indexed government service contracts Current Transit Systems Group CEO, Clint Feuerherdt, has replaced Jeff Ellison as SeaLink Group CEO SeaLink Travel Group Limited (ASX:SLK) (“SeaLink”) today announced it has completed the acquisition of 100% of Transit Systems Pty Ltd, Tower Transit Group Ltd and their broader group of entities (including trusts) (together the “Transit Systems Group”), Australia’s largest private operator of metropolitan public bus services and an established international bus operator in London and Singapore (the ‘Acquisition’). The SeaLink Board is also pleased to announce that Clint Feuerherdt, the current Group CEO of Transit Systems Group, has replaced Jeff Ellison as SeaLink Group CEO, effective from today. Jeff has agreed to provide support to Clint to ensure a smooth transition of leadership by remaining as an executive director of SeaLink for a short period of time, following which he will remain on the SeaLink Board of Directors as a non-executive director to continue sharing his extensive tourism and transport experience and knowledge. In addition, Neil Smith, one of the founding shareholders and current Chairman of Transit Systems Group, has joined the SeaLink Board of Directors as a non-executive director from today. -

For Personal Use Only

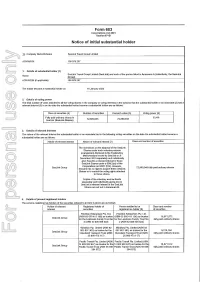

Form 603 Corporations Act 2001 Section 671 B Notice of initial substantial holder To Company Mame/Scheme SeaLink Trave! Group Limited ACN/ARSM 109078257 1. Details of substantial holder (1) SeaLink TraveE Group Limited (SeaLink) and each of the parties iisted in Annexure A (co!lective1y, the SeaLink Name Group) ACN/ARSN(ifappiicable) 109 078 257 The holder became a substantial holder on 16 January 2020 2. Details of voting power The total number of votes attached to al! the voting shares in the company or voting interests in the scheme that the substantial holder or an associate (2) had a relevant interest (3) in on the date the substantial holder became a substantial holder are as follows: Class of securities (4) Number of securities Person's votes (5) Voting power (6) Fuiiy paid ordinary shares in 33.4% SeaLink (SeaLink Shares) 72,569,945 72.869.945 3. Details of relevant interests substantiai holder are as follows: Holder of relevant interest Nature of relevant interest (7) Ciass and number of securities The restrictions on the disposal of the SeaLink Shares under each voluntary escrow arrangement disclosed in the Explanatory Memorandum issued by SeaUnk on 8 November 2019 ssparately and individuaSly give SeaLink a relevant interest in those Seai-ink Shares under s 608(1)(c) of the Corporations Act 2001 (Ctti). However, SeaLink Group 72,869,945 fully paid ordinary shares SeaLink has no right to acquire these SeaLink Shares or to control the voting rights attached to those shares. Copies of the voluntary escrow deeds separately and individually giving rise to SeaLink's relevant interest in the SeaLink Shares are set out in Annexure B. -

Understanding Ridership Drivers for Bus Rapid Transit Systems in Australia Graham Currie

Institute of Transport Studies, Monash University World Transit Research World Transit Research 1-1-2010 Understanding ridership drivers for bus rapid transit systems in Australia Graham Currie Alexa Delbosc Follow this and additional works at: http://www.worldtransitresearch.info/research Recommended Citation Currie, G., & Delbosc, A. (2010). Understanding ridership drivers for bus rapid transit systems in Australia. Paper delivered at the 33rd Australasian Transport Research Forum Conference held in Canberra, on 29 September - 1 October, 2010. This Conference Paper is brought to you for free and open access by World Transit Research. It has been accepted for inclusion in World Transit Research by an authorized administrator of World Transit Research. For more information, please contact [email protected]. Understanding ridership drivers for bus rapid transit systems in Australia Graham Currie1* and Alexa Delbosc2 *Corresponding Author 1*Graham Currie, Professor, Chair of Public Transport, Institute of Transport Studies, Department of Civil Engineering, Building 60, Monash University, Clayton, Victoria 3800, AUSTRALIA. Phone: + 61 3 9905 5574, Fax: +61 3 9905 4944, Email: [email protected] 3Alexa Delbosc, Research Fellow, Institute of Transport Studies, Department of Civil Engineering, Building 60, Monash University, Clayton, Victoria 3800, AUSTRALIA. Phone: + 61 3 9905 5568, Fax: +61 3 9905 4944, Email: [email protected] Abstract Bus Rapid Transit (BRT) systems are an increasingly popular public transport option in Australia and internationally. They provide rail-like quality for bus services for a fraction of the cost of fixed rail. Many claims of high and increasing ridership have resulted from BRT system development; however it is unclear exactly which aspects of BRT system design drive this. -

Transport Industry

Case study: Transport Industry Karen Armstrong’s Safety Strategies has been training transport personnel for over 15 years, with outstanding results in assault prevention and improved customer service. Our clients Safety Strategies has provided training to over 7,000 NSW State Transit personnel and 2,000 private bus industry drivers since 1996. State Transit Authority of NSW . Dion’s Bus Service . Transit Australia Group . Blue Mountains Bus Company . Sydney Ferries . Shoal Bus Company . Country Link . Hopkinsons . Busways . Jones Brothers . Hillsbus (formerly Westbus) . Berrima Buslines . Veolia . Redbus . Forest Coachlines . Coastal Liner . Shorelink . Port Stephens Coaches . Punchbowl Bus Company . Deane’s Transit Group Refresher programs have been custom designed to address the specific needs of employees working in high risk environments and duties. Risk profile Bus drivers deal with a wide range of people in their front line role of providing transport. Their safety can be compromised by: . Aggressive passengers . Late running . Drug / alcohol affected . Conflict over fares passengers . Unpredictable attack . Mentally unstable passengers . Working late at night . Isolated / high risk areas . Enforcing rules . School students’ disruptive . Robbery behaviour . Road rage . Attack with a weapon . Objects thrown at bus Safety Strategies’ training gives bus drivers the skills to prevent, avoid and defuse these situations, and as a last resort, teaches the use of physical protection skills within a legal and professional framework. m 0408 615 559 e [email protected] w karenarmstrong.com.au Case study: Transport Industry Our solution 1. Effective, hands-on workshops In Safety Strategies’ workshops, participants learn: . communication skills to provide high levels of customer service Cost savings .