State of Oregon Department of Consumer & Business Services

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Government Affairs Committee Meeting September 10Th & 11Th

Government Affairs Committee Meeting September 10th & 11th, 2013 Washington, D.C. AGENDA Tuesday Sept. 10 Location: Hall of States Building Room 231, 444 North Capitol St. NW, Washington, DC 11:00 a.m. – 11:30 a.m. Gather / Welcome 11:30 a.m. – 12:30 p.m. Lunch with Political Speaker 12:30 p.m. – 1:45 p.m. Employment / Labor Update (NLRB, Persuader, DOMA) Kara Maciel, Epstein Becker Green Healthcare Update (Employer Delay, Reporting Requirements) Adam Solander, Epstein Becker Green 1:45 p.m. – 2:00 p.m. Break 2:00 p.m. – 2:40 p.m. Patent Trolls Matthew Tanielian, Franklin Square Group 2:40 p.m. – 3:00 p.m. Issue Roundup (Interchange, SNAP, Menu Labeling, Etc.) 3:00 p.m. – 3:45 p.m. GMO Briefing Louis Finkel, EVP Grocery Manufactures Association (GMA) 3:45 p.m. – 4:30 p.m. Committee Policy Discussion on GMOs 5:00 p.m. – 6:30 p.m. NGA Capitol Hill Reception Featuring 2nd Annual Congressional Best Bagger Contest Location: Rayburn House Office Building B-318 45 Independence Ave SW, Washington, DC Wednesday Sept. 11 7:30a.m. – 7:50 a.m. Breakfast Location: NGA’s Offices 1005 North Glebe Road Arlington, VA (near Holiday Inn Hotel Ballston) 7:50 a.m. – 8:45 a.m. Capitol Hill Meetings Preparation / Briefing Primary Hill Meeting Topic: Healthcare 9:45 a.m. – 11:30 a.m. Capitol Hill Lobbying Meetings (NGA is coordinating meetings and teams) (approximately) Government Affairs Committee Roster Mr. Darrell Bourne Mr. Michael Erlandson Ragland Bros. Retail Co. SUPERVALU INC. -

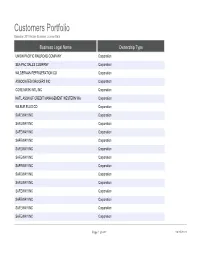

Customers Portfolio Based on 2010 Active Business License Data

Customers Portfolio Based on 2010 Active Business License Data Business Legal Name Ownership Type UNION PACIFIC RAILROAD COMPANY Corporation SEA PAC SALES COMPANY Corporation WILDERMAN REFRIGERATION CO Corporation ASSOCIATED GROCERS INC Corporation CORE MARK INTL INC Corporation NATL ASSN OF CREDIT MANAGEMENT WESTERN WA Corporation WILBUR ELLIS CO Corporation SAFEWAY INC Corporation SAFEWAY INC Corporation SAFEWAY INC Corporation SAFEWAY INC Corporation SAFEWAY INC Corporation SAFEWAY INC Corporation SAFEWAY INC Corporation SAFEWAY INC Corporation SAFEWAY INC Corporation SAFEWAY INC Corporation SAFEWAY INC Corporation SAFEWAY INC Corporation SAFEWAY INC Corporation Page 1 of 482 09/25/2021 Customers Portfolio Based on 2010 Active Business License Data Trade Name City, State, Zip UNION PACIFIC RAILROAD COMPANY SEATTLE, WA 98108 SEA-PAC SALES COMPANY KENT, WA 98032 WILDERMAN REFRIGERATION CO SEATTLE, WA 98109 ASSOCIATED GROCERS INC SEATTLE, WA 98118 CORE-MARK INTL INC LAKEWOOD, WA 98499 NACM WESTERN WASHINGTON & ALASKA SEATTLE, WA 98121 WILBUR-ELLIS CO AUBURN, WA 98001 SAFEWAY INC BELLEVUE, WA 98005 SAFEWAY INC #1477 SEATTLE, WA 98107 SAFEWAY STORE #1062 SEATTLE, WA 98116 SAFEWAY STORE #1143 SEATTLE, WA 98117 SAFEWAY STORE #1508 SEATTLE, WA 98118 SAFEWAY STORE #1550 SEATTLE, WA 98115 SAFEWAY STORE #1551 SEATTLE, WA 98112 SAFEWAY STORE #1586 SEATTLE, WA 98125 SAFEWAY STORE #1845 SEATTLE, WA 98103 SAFEWAY STORE #1885 SEATTLE, WA 98119 SAFEWAY STORE #1965 SEATTLE, WA 98118 SAFEWAY STORE #1993 SEATTLE, WA 98112 SAFEWAY STORE #219 SEATTLE, WA -

CRC Tech Memo #1706C-1 Prologis Emerald Gateway Tukwila

TECHNICAL MEMO 1706C-1 DATE: July 24, 2017 TO: Ken Sun Prologis FROM: Margaret Berger, Principal Investigator RE: Cultural Resources Assessment for the Prologis Emerald Gateway Project, King County, Washington Log No.: 2017-06-04611 The attached short report form constitutes our final report for the above referenced project. Background research and field investigations did not identify any recorded or as yet unrecorded precontact cultural resources within the project. CRC completed historic property inventory forms for four structures that would be demolished. These buildings may be considered locally significant but they do not appear to meet historic register eligibility criteria. CRC recommends archaeological monitoring during ground disturbing activity should proposed project actions intersect native Holocene sediments. Please contact our office should you have any questions about our findings and/or recommendations. 1416 NW 46TH STREET, STE 105 PMB 346 SEATTLE, WA 98107 PHONE 206 855-9020 - [email protected] CULTURAL RESOURCES REPORT COVER SHEET Author: Margaret Berger Title of Report: Cultural Resources Assessment for the Prologis Emerald Gateway Project, King County, Washington Date of Report: July 24, 2017 County(ies): King Section: 3 & 4 Township: 23 N Range: 4 E Quad: Seattle South, WA Acres: 62 PDF of report submitted (REQUIRED) Yes Historic Property Inventory Forms to be Approved Online? Yes No Archaeological Site(s)/Isolate(s) Found or Amended? Yes No TCP(s) found? Yes No Replace a draft? Yes No Satisfy a DAHP Archaeological Excavation Permit requirement? Yes # No Were Human Remains Found? Yes DAHP Case # No DAHP Archaeological Site #: • Submission of PDFs is required. • Please be sure that any PDF submitted to DAHP has its cover sheet, figures, graphics, appendices, attachments, correspondence, etc., compiled into one single PDF file. -

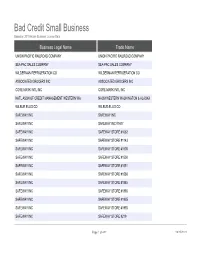

Bad Credit Small Business Based on 2010 Active Business License Data

Bad Credit Small Business Based on 2010 Active Business License Data Business Legal Name Trade Name UNION PACIFIC RAILROAD COMPANY UNION PACIFIC RAILROAD COMPANY SEA PAC SALES COMPANY SEA-PAC SALES COMPANY WILDERMAN REFRIGERATION CO WILDERMAN REFRIGERATION CO ASSOCIATED GROCERS INC ASSOCIATED GROCERS INC CORE MARK INTL INC CORE-MARK INTL INC NATL ASSN OF CREDIT MANAGEMENT WESTERN WA NACM WESTERN WASHINGTON & ALASKA WILBUR ELLIS CO WILBUR-ELLIS CO SAFEWAY INC SAFEWAY INC SAFEWAY INC SAFEWAY INC #1477 SAFEWAY INC SAFEWAY STORE #1062 SAFEWAY INC SAFEWAY STORE #1143 SAFEWAY INC SAFEWAY STORE #1508 SAFEWAY INC SAFEWAY STORE #1550 SAFEWAY INC SAFEWAY STORE #1551 SAFEWAY INC SAFEWAY STORE #1586 SAFEWAY INC SAFEWAY STORE #1845 SAFEWAY INC SAFEWAY STORE #1885 SAFEWAY INC SAFEWAY STORE #1965 SAFEWAY INC SAFEWAY STORE #1993 SAFEWAY INC SAFEWAY STORE #219 Page 1 of 482 09/25/2021 Bad Credit Small Business Based on 2010 Active Business License Data City, State, Zip SEATTLE, WA 98108 KENT, WA 98032 SEATTLE, WA 98109 SEATTLE, WA 98118 LAKEWOOD, WA 98499 SEATTLE, WA 98121 AUBURN, WA 98001 BELLEVUE, WA 98005 SEATTLE, WA 98107 SEATTLE, WA 98116 SEATTLE, WA 98117 SEATTLE, WA 98118 SEATTLE, WA 98115 SEATTLE, WA 98112 SEATTLE, WA 98125 SEATTLE, WA 98103 SEATTLE, WA 98119 SEATTLE, WA 98118 SEATTLE, WA 98112 SEATTLE, WA 98118 Page 2 of 482 09/25/2021 Bad Credit Small Business Based on 2010 Active Business License Data SAFEWAY INC SAFEWAY STORE #3091 SAFEWAY INC SAFEWAY STORE #368 SAFEWAY INC SAFEWAY STORE #373 SAFEWAY INC SAFEWAY STORE #423 SAFEWAY INC SAFEWAY -

National Register of Historic Places Registration Form (National Register Bulletin 16A)

FEB 2 6 2000 NPS Form 10-900 (Oct. 1990) RECEIVED 2280 United States Department of the Interior National Park Service MAR 1 2 2008 National Register of Historic Places NA HtGISIfcH OF HISTORIC PLA 3ES Registration Form NATIONAL PARK SFRVIHF This form is for use in nominating or requesting determinations for individual properties and districts. See instructions in How to Complete the National Register of Historic Places Registration Form (National Register Bulletin 16A). Complete each item by marking "x" in the appropriate box or by entering the information requested. If an item does not apply to the property being documented, enter "N/A" for "not applicable." For functions, architectural classification, materials and areas of significance, enter only categories and subcategories from the instructions. Place additional entries and narrative items on continuation sheets (NPS Form 10-900a). Use a typewriter, word processor, or computer, to complete all items. 1. Name of Property historic name Grocers Wholesale Company Building other names/site number Sears and Roebuck Farm Store 2. Location street & number 22 West Ninth Street N/A1 not for publication city or town __ Des Moines ___ [N/A1 vicinity state Iowa code IA county Polk code 153 zip code 3. State/Federal Agency Certification As the designated authority under the National Historic Preservation Act, as amended, I hereby certify that this [X] nomination LJ request for determination of eligibility meets the documentation standards for registering properties in the National Register of Historic Places and meets the procedural and professional requirements set forth in 36 CFR Part 60. In my opinion, the property [X] meets LJ does not meet the National Register criteria. -

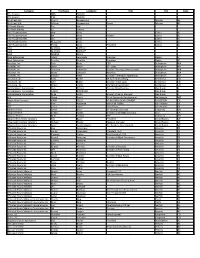

2013 List of Registrants

Company FirstName LastName Title City State 4T's Grocery ANN TAYLOR 4T's Grocery TIM TAYLOR 5th Street IGA Sherry Huenemann Minden NE 5th Street IGA William Huenemann Owner Minden NE 99 Ranch Market Tee Jaw 99 Ranch Market Ty Truong A & R Supermarkets Ann Davis Calera AL A & R Supermarkets Bill Davis Partner Calera AL A & R Supermarkets Jan Davis Calera AL A & R Supermarkets Margarita Davis Calera AL A & R Supermarkets Phillip Davis President Calera AL AAIA MICHAEL BARRATT AAIA MICHAEL BARRATT AAIA ARLENE DAVIS Abco Enterprises Adam Sepulveda Manager Ogden VT Abco Enterprises Suzette Sharifan President Ogden VT Accelitec, Inc. Tom Bartz CEO Bellingham WA Accelitec, Inc. Steve Byron VP - Sales Bellingham WA Accelitec, Inc. Christine Schneider Director -Business Development Bellingham WA Accelitec, Inc. Marty Schroder Accelitec Bellingham WA Accelitec, Inc. Edward West Director - Merchant Operations Bellingham WA AccuCode, Inc. Todd Baillie VP Sales & Marketing Centennial CO AccuCode, Inc. John Butler Director of AO: Apps Centennial CO AccuCode, Inc. Robyn Crotty Marketing Coordinator Centennial CO Ace Hardware Corporation Curt DeHart Director New Business Oak Brook IL Ace Hardware Corporation CARLO MORANDO Oak Brook IL Ace Hardware Corporation Mike Smith Grocery Channel Manager Oak Brook IL ACS Chuck Daniel Dir of Corporate Development Nottingham MD Action Retail Services JOHN GILLIS VP BUSINESS DEVELOPMENT FULLERTON CA ADT Teal Hausman Jack of all Trades San Antonio TX ADT Cesar Lopez Sales/Buyer San Antonio TX Advance Pierre David Minx VP Strategic Sourcing Cincinnati OH Advance Pierre Shawn Sparks Director of Strategic Sourcing Enid OK Advance Pierre Mike Zelkind SVP Cincinnati OH Advanced Inventory Solutions Tim Bayer President Grand Rapids MI Advanced Inventory Solutions Richard Heetai Regional Manager Grand Rapids MI Advanced Inventory Solutions Steve Southerington Dir. -

RETAIL VIEW: Unified Grocer Acquisition Creates Significant Growth

- Advertisement - RETAIL VIEW: Unified Grocer acquisition creates significant growth September 24, 2007 With the shareholders of Seattle-based grocery wholesaler Associated Grocers Inc. approving the sale of the company to Unified Western Grocers in Los Angeles, Unified has now moved into being one of the top-five retailer wholesalers in the country. And the close to 3,000 retailers it serves, in aggregate, create buying power that could be among the top 10 retail operations in the country. Unified Grocers, as it is now called while it goes through the process of effecting a legal name change, serves more than 2,500 stores, primarily in California and Oregon. Associated Grocers served close to 400 stores primarily in Washington but also in other Northwest states and Alaska. Unified spokesperson Tom Schaffner said that once the deal closes, which is expected by the end of September, Unified will be a $4 billion company. Its independent and small chain members, who typically buy 50-70 percent of their products in house, own the company, he said. Like the supermarket industry itself, wholesale grocery distributors built their industry largely on center-store items. But mirroring supermarkets, growth has been in the perimeter of the store, hence Unified has made a concerted effort in perishables over the past several years. "Our company put a new emphasis on all the perishable departments, including produce, four years ago," Mr. Schaffner said. "We added product line and expanded our offerings. Since then, we have doubled the size of our company [in terms of sales]. We have added a few stores in that period but mostly it has been due to the growth in perishables." In the past year, Unified Grocers opened a new produce warehouse in Southern California. -

Organization Last Name First Name Title City 210 Analytics, LLC Roerink Anne-Marie Principal Lakeland 3.14 Communications LLC Py

Organization Last Name First Name Title City 210 Analytics, LLC Roerink Anne-Marie Principal Lakeland 3.14 Communications LLC Pye Cassandra CEO A & R Supermarkets Davis Philip Owner Calera A & R Supermarkets Davis Jan Spouse Calera A.T. Kearney Ltd. Farmer Dan Principal Toronto Acapulco Tropical Huelga Romel CEO/FOUNDER Bradenton Acapulco Tropical Leyva Quintana Joey Spouse Bradenton Acapulco Tropical Leyva Quintana Ana Bradenton ACUITY, A Mutual Insurance Co. Borkenhagen Sarah CL Marketing Analyst Sheboygan ACUITY, A Mutual Insurance Co. Maliborski Steve CL Marketing Analyst Sheboygan Affiliated Foods Midwest Cooperative,Myers Inc. Tim Sr. V.P. Sales & Retail OperationsNorfolk Affiliated Foods Midwest Cooperative,Cunningham Inc. Doug Government Affairs Norfolk Affiliated Foods Midwest Cooperative,Tisch Inc. Jon Norfolk Affiliated Foods, Inc. Cooper Roy District Supervisor Amarillo Affiliated Foods, Inc. Garcia Michelle Director Dulce Affiliated Foods, Inc. Hamilton Randie Store Owner Amarillo Affiliated Foods, Inc. Hamilton Mary Spouse Amarillo Affiliated Foods, Inc. Kaden Jim Director of Operations Amarillo Affiliated Foods, Inc. Vigil Grant Spouse Dulce Affiliated Foods, Inc. Arceneaux Randy President & CEO Amarillo Affiliated Foods, Inc. Arceneaux Lisa Spouse Amarillo Affiliated Foods, Inc. Clawson Melody Spouse Amarillo Affiliated Foods, Inc. Clawson Val Private Brands Amarillo Affiliated Foods, Inc. Fontenot Tammy Spouse Amarillo Affiliated Foods, Inc. Fontenot Russell Director of Meat Amarillo Affiliated Foods, Inc. Halencak Tammy Spouse Amarillo Affiliated Foods, Inc. Halencak Andy Programming ManagerAmarillo Affiliated Foods, Inc. Herrera Dina Spouse Amarillo Affiliated Foods, Inc. Herrera Miguel Director of Produce Amarillo Affiliated Foods, Inc. McKelvey Anne Spouse Amarillo Affiliated Foods, Inc. McKelvey Dave Director of Marketing Amarillo Affiliated Foods, Inc. Robinson Misti Spouse Amarillo Affiliated Foods, Inc. -

746418 128.Pdf

19-11608-mew Doc 128 Filed 06/24/19 Entered 06/24/19 17:50:56 Main Document Pg 1 of 514 19-11608-mew Doc 128 Filed 06/24/19 Entered 06/24/19 17:50:56 Main Document Pg 2 of 514 EXHIBIT A 19-11608-mew Doc 128 Filed 06/24/19 Entered 06/24/19 17:50:56 Main Document Hollander Sleep Products, LLC, et al. - Service List to e-mail Recipients Pg 3 of 514 Served 6/19/2019 BLANK ROME, LLP BLANK ROME, LLP BLANK ROME, LLP BRYAN J. HALL JOSE BIBILONI JOSH LUCIAN [email protected] [email protected] [email protected] BUCHALTER, A PROFESSIONAL CORPORATION COHEN, WEISS & SIMON LLP COHEN, WEISS & SIMON LLP SHAWN M. CHRISTIANSON MARIE B. HAHN RICHARD M. SELTZER [email protected] [email protected] [email protected] GOLDBERG KOHN LTD GOLDBERG KOHN LTD KING & SPADING LLP KIM PRISCA RANDALL KLEIN AUSTIN JOWERS [email protected] [email protected] [email protected] KING & SPADING LLP KRAMER LEVIN NAFTALIS & FRANKEL, LLP KRAMER LEVIN NAFTALIS & FRANKEL, LLP STEPHEN M. BLANK ADAM C. ROGOFF JENNIFER SHARRET [email protected] [email protected] [email protected] KRAMER LEVIN NAFTALIS & FRANKEL, LLP KRAMER LEVIN NAFTALIS & FRANKEL, LLP LINEBARGER GOGGAN BLAIR & SAMPSON, LLP KENNETH ECKSTEIN NATHANIEL ALLARD ELIZABETH WELLER [email protected] [email protected] [email protected] NELSON MULLINS RILEY & SCARBOROUGH, LLP OFFICE OF THE ATTORNEY GENERAL OFFICE OF THE ATTORNEY GENERAL ALAN F. KAUFMAN [email protected] [email protected] [email protected] OFFICE OF THE ATTORNEY GENERAL OFFICE OF THE UNITED STATES TRUSTEE ORRICK, HERRINGTON & SUTCLIFFE LLP [email protected] SHANNON SCOTT LAURA METZGER [email protected] [email protected] ORRICK, HERRINGTON & SUTCLIFFE LLP PACHULSKI STANG ZIEHL & JONES PACHULSKI STANG ZIEHL & JONES PETER J.