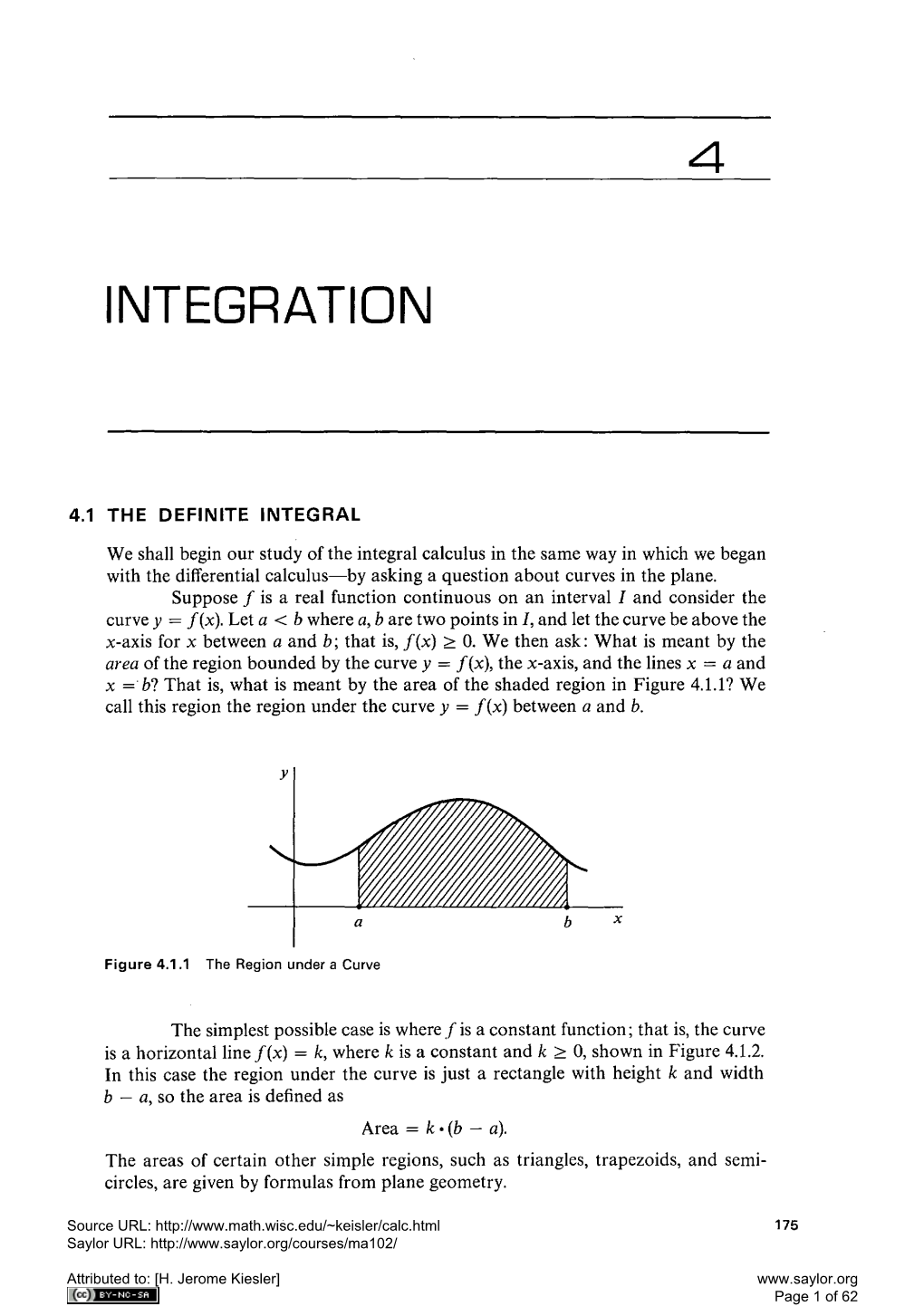

The Definite Integral

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Differential Calculus and by Era Integral Calculus, Which Are Related by in Early Cultures in Classical Antiquity the Fundamental Theorem of Calculus

History of calculus - Wikipedia, the free encyclopedia 1/1/10 5:02 PM History of calculus From Wikipedia, the free encyclopedia History of science This is a sub-article to Calculus and History of mathematics. History of Calculus is part of the history of mathematics focused on limits, functions, derivatives, integrals, and infinite series. The subject, known Background historically as infinitesimal calculus, Theories/sociology constitutes a major part of modern Historiography mathematics education. It has two major Pseudoscience branches, differential calculus and By era integral calculus, which are related by In early cultures in Classical Antiquity the fundamental theorem of calculus. In the Middle Ages Calculus is the study of change, in the In the Renaissance same way that geometry is the study of Scientific Revolution shape and algebra is the study of By topic operations and their application to Natural sciences solving equations. A course in calculus Astronomy is a gateway to other, more advanced Biology courses in mathematics devoted to the Botany study of functions and limits, broadly Chemistry Ecology called mathematical analysis. Calculus Geography has widespread applications in science, Geology economics, and engineering and can Paleontology solve many problems for which algebra Physics alone is insufficient. Mathematics Algebra Calculus Combinatorics Contents Geometry Logic Statistics 1 Development of calculus Trigonometry 1.1 Integral calculus Social sciences 1.2 Differential calculus Anthropology 1.3 Mathematical analysis -

Notes on Calculus II Integral Calculus Miguel A. Lerma

Notes on Calculus II Integral Calculus Miguel A. Lerma November 22, 2002 Contents Introduction 5 Chapter 1. Integrals 6 1.1. Areas and Distances. The Definite Integral 6 1.2. The Evaluation Theorem 11 1.3. The Fundamental Theorem of Calculus 14 1.4. The Substitution Rule 16 1.5. Integration by Parts 21 1.6. Trigonometric Integrals and Trigonometric Substitutions 26 1.7. Partial Fractions 32 1.8. Integration using Tables and CAS 39 1.9. Numerical Integration 41 1.10. Improper Integrals 46 Chapter 2. Applications of Integration 50 2.1. More about Areas 50 2.2. Volumes 52 2.3. Arc Length, Parametric Curves 57 2.4. Average Value of a Function (Mean Value Theorem) 61 2.5. Applications to Physics and Engineering 63 2.6. Probability 69 Chapter 3. Differential Equations 74 3.1. Differential Equations and Separable Equations 74 3.2. Directional Fields and Euler’s Method 78 3.3. Exponential Growth and Decay 80 Chapter 4. Infinite Sequences and Series 83 4.1. Sequences 83 4.2. Series 88 4.3. The Integral and Comparison Tests 92 4.4. Other Convergence Tests 96 4.5. Power Series 98 4.6. Representation of Functions as Power Series 100 4.7. Taylor and MacLaurin Series 103 3 CONTENTS 4 4.8. Applications of Taylor Polynomials 109 Appendix A. Hyperbolic Functions 113 A.1. Hyperbolic Functions 113 Appendix B. Various Formulas 118 B.1. Summation Formulas 118 Appendix C. Table of Integrals 119 Introduction These notes are intended to be a summary of the main ideas in course MATH 214-2: Integral Calculus. -

Analyzing Applied Calculus Student Understanding of Definite Integrals in Real-Life Applications

Graduate Theses, Dissertations, and Problem Reports 2021 ANALYZING APPLIED CALCULUS STUDENT UNDERSTANDING OF DEFINITE INTEGRALS IN REAL-LIFE APPLICATIONS CODY HOOD [email protected] Follow this and additional works at: https://researchrepository.wvu.edu/etd Part of the Mathematics Commons, and the Science and Mathematics Education Commons Recommended Citation HOOD, CODY, "ANALYZING APPLIED CALCULUS STUDENT UNDERSTANDING OF DEFINITE INTEGRALS IN REAL-LIFE APPLICATIONS" (2021). Graduate Theses, Dissertations, and Problem Reports. 8260. https://researchrepository.wvu.edu/etd/8260 This Dissertation is protected by copyright and/or related rights. It has been brought to you by the The Research Repository @ WVU with permission from the rights-holder(s). You are free to use this Dissertation in any way that is permitted by the copyright and related rights legislation that applies to your use. For other uses you must obtain permission from the rights-holder(s) directly, unless additional rights are indicated by a Creative Commons license in the record and/ or on the work itself. This Dissertation has been accepted for inclusion in WVU Graduate Theses, Dissertations, and Problem Reports collection by an authorized administrator of The Research Repository @ WVU. For more information, please contact [email protected]. Graduate Theses, Dissertations, and Problem Reports 2021 ANALYZING APPLIED CALCULUS STUDENT UNDERSTANDING OF DEFINITE INTEGRALS IN REAL-LIFE APPLICATIONS CODY HOOD Follow this and additional works at: https://researchrepository.wvu.edu/etd Part of the Mathematics Commons, and the Science and Mathematics Education Commons ANALYZING APPLIED CALCULUS STUDENT UNDERSTANDING OF DEFINITE INTEGRALS IN REAL-LIFE APPLICATIONS Cody Hood Dissertation submitted to the Eberly College of Arts and Sciences at West Virginia University in partial fulfillment of the requirements for the degree of Doctor of Philosophy in Mathematics Vicki Sealey, Ph.D., Chair Harvey Diamond, Ph.D. -

Connes on the Role of Hyperreals in Mathematics

Found Sci DOI 10.1007/s10699-012-9316-5 Tools, Objects, and Chimeras: Connes on the Role of Hyperreals in Mathematics Vladimir Kanovei · Mikhail G. Katz · Thomas Mormann © Springer Science+Business Media Dordrecht 2012 Abstract We examine some of Connes’ criticisms of Robinson’s infinitesimals starting in 1995. Connes sought to exploit the Solovay model S as ammunition against non-standard analysis, but the model tends to boomerang, undercutting Connes’ own earlier work in func- tional analysis. Connes described the hyperreals as both a “virtual theory” and a “chimera”, yet acknowledged that his argument relies on the transfer principle. We analyze Connes’ “dart-throwing” thought experiment, but reach an opposite conclusion. In S, all definable sets of reals are Lebesgue measurable, suggesting that Connes views a theory as being “vir- tual” if it is not definable in a suitable model of ZFC. If so, Connes’ claim that a theory of the hyperreals is “virtual” is refuted by the existence of a definable model of the hyperreal field due to Kanovei and Shelah. Free ultrafilters aren’t definable, yet Connes exploited such ultrafilters both in his own earlier work on the classification of factors in the 1970s and 80s, and in Noncommutative Geometry, raising the question whether the latter may not be vulnera- ble to Connes’ criticism of virtuality. We analyze the philosophical underpinnings of Connes’ argument based on Gödel’s incompleteness theorem, and detect an apparent circularity in Connes’ logic. We document the reliance on non-constructive foundational material, and specifically on the Dixmier trace − (featured on the front cover of Connes’ magnum opus) V. -

Epistemic Criteria for Designing Limit Tasks on a Real Variable Function

ISSN 1980-4415 DOI: http://dx.doi.org/10.1590/1980-4415v35n69a09 Epistemic Criteria for Designing Limit Tasks on a Real Variable Function Criterios Epistémicos para el Diseño de Tareas sobre Límite de una función en una variable Real Daniela Araya Bastias* ORCID iD 0000-0002-3395-3348 Luis R. Pino-Fan** ORCID iD 0000-0003-4060-7408 Iván G. Medrano*** ORCID iD 0000-0003-4910-1235 Walter F. Castro**** ORCID iD 0000-0002-7890-681X Abstract This article aims at presenting the results of a historical-epistemological study conducted to identify criteria for designing tasks that promote the understanding of the limit notion on a real variable function. As a theoretical framework, we used the Onto-Semiotic Approach (OSA) to mathematical knowledge and instruction, to identify the regulatory elements of mathematical practices developed throughout history, and that gave way to the emergence, evolution, and formalization of limit. As a result, we present a proposal of criteria that summarizes fundamental epistemic aspects, which could be considered when designing tasks that allow the promotion of each of the six meanings identified for the limit notion. The criteria presented allow us to highlight not only the mathematical complexity underlying the study of limit on a real variable function but also the richness of meanings that could be developed to help understand this notion. Keywords: Limit. Task design. Onto-Semiotic Approach. Resumen El objetivo de este artículo es presentar los resultados de un estudio de tipo histórico-epistemológico, que se llevó a cabo para identificar criterios a considerar en el diseño de tareas para promover la comprensión de la noción de * Magíster en Matemática por la Universidad de Santiago de Chile (USACH). -

List of Mathematical Symbols by Subject from Wikipedia, the Free Encyclopedia

List of mathematical symbols by subject From Wikipedia, the free encyclopedia This list of mathematical symbols by subject shows a selection of the most common symbols that are used in modern mathematical notation within formulas, grouped by mathematical topic. As it is virtually impossible to list all the symbols ever used in mathematics, only those symbols which occur often in mathematics or mathematics education are included. Many of the characters are standardized, for example in DIN 1302 General mathematical symbols or DIN EN ISO 80000-2 Quantities and units – Part 2: Mathematical signs for science and technology. The following list is largely limited to non-alphanumeric characters. It is divided by areas of mathematics and grouped within sub-regions. Some symbols have a different meaning depending on the context and appear accordingly several times in the list. Further information on the symbols and their meaning can be found in the respective linked articles. Contents 1 Guide 2 Set theory 2.1 Definition symbols 2.2 Set construction 2.3 Set operations 2.4 Set relations 2.5 Number sets 2.6 Cardinality 3 Arithmetic 3.1 Arithmetic operators 3.2 Equality signs 3.3 Comparison 3.4 Divisibility 3.5 Intervals 3.6 Elementary functions 3.7 Complex numbers 3.8 Mathematical constants 4 Calculus 4.1 Sequences and series 4.2 Functions 4.3 Limits 4.4 Asymptotic behaviour 4.5 Differential calculus 4.6 Integral calculus 4.7 Vector calculus 4.8 Topology 4.9 Functional analysis 5 Linear algebra and geometry 5.1 Elementary geometry 5.2 Vectors and matrices 5.3 Vector calculus 5.4 Matrix calculus 5.5 Vector spaces 6 Algebra 6.1 Relations 6.2 Group theory 6.3 Field theory 6.4 Ring theory 7 Combinatorics 8 Stochastics 8.1 Probability theory 8.2 Statistics 9 Logic 9.1 Operators 9.2 Quantifiers 9.3 Deduction symbols 10 See also 11 References 12 External links Guide The following information is provided for each mathematical symbol: Symbol: The symbol as it is represented by LaTeX. -

Pascal and Leibniz: Sines, Circles, and Transmutations

Pascal and Leibniz: Sines, Circles, and Transmutations The title of the last section promised some discussion of sine curves. In Roberval's construction a sine curve was drawn and used to find the area of the cycloidal arch (see Figure 2.13b), but Roberval called this curve the "companion of the cycloid." He did not see this curve as a graph of a sine or cosine, and neither did any of his contemporaries. They did discuss sines and cosines, however, and it is important to understand the conceptual point of view that was then standard. Before I present my last example of curve drawing from Leibniz, I must also return to some of the issues raised in section 2.3. Leibniz's use of the characteristic triangle (Figure 2.3b) was directly inspired by the work of Pascal concerning sines. Trigonometric functions were not defined using ratios, or the unit circle, until the textbooks of Euler were published in 1748 (Euler, 1988). Both Ptolemy and Arabic astronomers made detailed tables of the lengths of chords subtended by circular arcs (Katz, 1993). That is, given two points, A and B, on a circle, to find the length of the line segment AB. Such tables were usually made for a circle of a given (large) radius, and then scaled for use in other settings. It was also found useful by Arabic astronomers to have tables of half chords, and such tables became known in Latin as tables of "sines." 1 Since the perpendicular bisector of any chord passes through the center of the circle, half chords on the unit circle are the same as our sines, but I want to stress that trigonometric quantities were seen as lengths. -

Understanding Student Reasoning About Differentials and Integrals – Symbolic Forms and Metaphors

UNDERSTANDING INTRODUCTORY STUDENTS‘ APPLICATION OF INTEGRALS IN PHYSICS FROM MULTIPLE PERSPECTIVES by DEHUI HU B.S., University of Science and Technology of China, 2009 AN ABSTRACT OF A DISSERTATION Submitted in partial fulfillment of the requirements for the degree DOCTOR OF PHILOSOPHY Department of Physics College of Arts and Sciences KANSAS STATE UNIVERSITY Manhattan, Kansas 2013 Abstract Calculus is used across many physics topics from introductory to upper-division level college courses. The concepts of differentiation and integration are important tools for solving real world problems. Using calculus or any mathematical tool in physics is much more complex than the straightforward application of the equations and algorithms that students often encounter in math classes. Research in physics education has reported students‘ lack of ability to transfer their calculus knowledge to physics problem solving. In the past, studies often focused on what students fail to do with less focus on their underlying cognition. However, when solving physics problems requiring the use of integration, their reasoning about mathematics and physics concepts has not yet been carefully and systematically studied. Hence the main purpose of this qualitative study is to investigate student thinking in-depth and provide deeper insights into student reasoning in physics problem solving from multiple perspectives. I propose a conceptual framework by integrating aspects of several theoretical constructs from the literature to help us understand our observations -

Derivative Conceptions Over Riemann Sum-Based Conceptions in Students’ Explanations of Definite Integrals

International Journal of Mathematical Education in Science and Technology ISSN: 0020-739X (Print) 1464-5211 (Online) Journal homepage: http://www.tandfonline.com/loi/tmes20 The prevalence of area-under-a-curve and anti- derivative conceptions over Riemann sum-based conceptions in students’ explanations of definite integrals Steven R. Jones To cite this article: Steven R. Jones (2015) The prevalence of area-under-a-curve and anti- derivative conceptions over Riemann sum-based conceptions in students’ explanations of definite integrals, International Journal of Mathematical Education in Science and Technology, 46:5, 721-736, DOI: 10.1080/0020739X.2014.1001454 To link to this article: https://doi.org/10.1080/0020739X.2014.1001454 Published online: 29 Jan 2015. Submit your article to this journal Article views: 193 View related articles View Crossmark data Citing articles: 6 View citing articles Full Terms & Conditions of access and use can be found at http://www.tandfonline.com/action/journalInformation?journalCode=tmes20 International Journal of Mathematical Education in Science and Technology, 2015 Vol. 46, No. 5, 721–736, http://dx.doi.org/10.1080/0020739X.2014.1001454 The prevalence of area-under-a-curve and anti-derivative conceptions over Riemann sum-based conceptions in students’ explanations of definite integrals Steven R. Jones∗ Department of Mathematics Education, Brigham Young University, Provo, UT, USA (Received 29 May 2014) This study aims to broadly examine how commonly various conceptualizations of the definite integral are drawn on by students as they attempt to explain the meaning of integral expressions. Previous studies have shown that certain conceptualizations, such as the area under a curve or the values of an anti-derivative, may be less productive in making sense of contextualized integrals. -

What Does/Did the Integral Sign Represent?

What does/did the Integral Sign represent? Some comments on the origin of the usual integral sign notation b f(x) dx Za might be useful in understanding the ways in which integrals arise in questions of inde- pendent interest. We begin with the limit formula as stated on text page 125 of Guichard (this is page 137 in the pdf file): n−1 b b − a f(x) dx = lim f(ti) dt ; where ∆t = Z n!1 a Xi=0 n If we view the Riemann sums on the right as approximations to the area under the curve y = f(x) for a ≤ x ≤ b, then the sum is actually the sum of the areas of n rectangles of width ∆t, and the crucial fact is that these converge to a limiting value (the \actual area") as n ! 1. The integral symbol is a version of the essentially obsolete letter which is now written as s, and it was first employed to convey the idea that the integral isR a continuous sum of the quantities f(x) dx, which can be viewed as the areas of rectangles whose vertical sides have length f(x) and whose horizontal sides have a so-called infinitesimally thin width which is denoted by dx. Note on infinitesimals. The idea of working with infinitesimally small quanti- ties turns out to be very useful in working with problems in the sciences and engineering, both as a tool for finding solutions and also for explaining them. However, ever since the invention of calculus mathematicians and others have recognized that justifying the use of such objects in a simple, logically rigorous fashion is at best challenging and at worst not feasible. -

Ti3 O 3 T Project Number: BMV-1007 4C

Vernescu, B. (MA) 46 BMV-1007 6o /31- TYPE: IQP 9 1 DATE: 12/97 ti3 o 3 T Project Number: BMV-1007 4C, The History of the Calculus and the Development of Computer Algebra Systems An Interactive Qualifying Project Report submitted to the Faculty of the Worcester Polytechnic Institute in partial fulfillment of the requirements for the Degree of Bachelor of Science By Daniel Ginsburg Brian Groose Josh Taylor Date: December 1997 Approved: Professor Bogdan M. Vernescu, A isor On the web @ http://www.math.wpi.edu/IQP/BVCalcHist/ Abstract A technical examination of the Calculus from two directions: how the past has led to present methodologies and how present methodology has automated the methods from the past. Presented is a discussion of the mathematics and people responsible for inventing the Calculus and an introduction to the inner workings of Computer Algebra Systems. 0. INTRODUCTION 1 1. HISTORY OF THE INTEGRAL FROM THE 17 TH CENTURY 3 1.1 INTRODUCTION 3 1.2 CAVALIERI'S METHOD OF INDIVISBLES 3 1.3 WALLIS' LAW FOR INTEGRATION OF POLYNOMIALS 7 1.4 FERMAT'S APPROACH TO INTEGRATION 9 2. HISTORY OF THE DIFFERENTIAL FROM THE 17TH CENTURY 14 2.1 INTRODUCTION 14 2.2 ROBERVAL'S METHOD OF TANGENT LINES USING INSTANTANEOUS MOTION 14 2.3 FERMAT'S MAXIMA AND TANGENT 16 2.4 NEWTON AND LEIBNIZ 19 2.5 THE ELLUSIVE INVERSES - THE INTEGRAL AND DIFFERENTIAL 20 3. SELECTED PROBLEMS FROM THE HISTORY OF THE INFINITE SERIES 24 3.1 INTRODUCTION 24 3.2 JAMES GREGORY'S INFINITE SERIES FOR ARCTAN 24 3.3 LEIBNIZ'S EARLY INFINITE SERIES 25 3.4 LEIBNIZ AND THE INFINITE SERIES FOR TRIGONOMETRIC FUNCTIONS 26 3.5 EULER'S SUM OF THE RECIPROCALS OF THE SQUARES OF THE NATURAL NUMBERS 30 4. -

Real Analysis (4Th Edition)

Preface The first three editions of H.L.Royden's Real Analysis have contributed to the education of generations of mathematical analysis students. This fourth edition of Real Analysis preserves the goal and general structure of its venerable predecessors-to present the measure theory, integration theory, and functional analysis that a modem analyst needs to know. The book is divided the three parts: Part I treats Lebesgue measure and Lebesgue integration for functions of a single real variable; Part II treats abstract spaces-topological spaces, metric spaces, Banach spaces, and Hilbert spaces; Part III treats integration over general measure spaces, together with the enrichments possessed by the general theory in the presence of topological, algebraic, or dynamical structure. The material in Parts II and III does not formally depend on Part I. However, a careful treatment of Part I provides the student with the opportunity to encounter new concepts in a familiar setting, which provides a foundation and motivation for the more abstract concepts developed in the second and third parts. Moreover, the Banach spaces created in Part I, the LP spaces, are one of the most important classes of Banach spaces. The principal reason for establishing the completeness of the LP spaces and the characterization of their dual spaces is to be able to apply the standard tools of functional analysis in the study of functionals and operators on these spaces. The creation of these tools is the goal of Part II. NEW TO THE EDITION This edition contains 50% more exercises than the previous edition Fundamental results, including Egoroff s Theorem and Urysohn's Lemma are now proven in the text.