Music Markets and Mythologies

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Uila Supported Apps

Uila Supported Applications and Protocols updated Oct 2020 Application/Protocol Name Full Description 01net.com 01net website, a French high-tech news site. 050 plus is a Japanese embedded smartphone application dedicated to 050 plus audio-conferencing. 0zz0.com 0zz0 is an online solution to store, send and share files 10050.net China Railcom group web portal. This protocol plug-in classifies the http traffic to the host 10086.cn. It also 10086.cn classifies the ssl traffic to the Common Name 10086.cn. 104.com Web site dedicated to job research. 1111.com.tw Website dedicated to job research in Taiwan. 114la.com Chinese web portal operated by YLMF Computer Technology Co. Chinese cloud storing system of the 115 website. It is operated by YLMF 115.com Computer Technology Co. 118114.cn Chinese booking and reservation portal. 11st.co.kr Korean shopping website 11st. It is operated by SK Planet Co. 1337x.org Bittorrent tracker search engine 139mail 139mail is a chinese webmail powered by China Mobile. 15min.lt Lithuanian news portal Chinese web portal 163. It is operated by NetEase, a company which 163.com pioneered the development of Internet in China. 17173.com Website distributing Chinese games. 17u.com Chinese online travel booking website. 20 minutes is a free, daily newspaper available in France, Spain and 20minutes Switzerland. This plugin classifies websites. 24h.com.vn Vietnamese news portal 24ora.com Aruban news portal 24sata.hr Croatian news portal 24SevenOffice 24SevenOffice is a web-based Enterprise resource planning (ERP) systems. 24ur.com Slovenian news portal 2ch.net Japanese adult videos web site 2Shared 2shared is an online space for sharing and storage. -

AP1 Companies Affiliates

AP1 COMPANIES & AFFILIATES 100% RECORDS BIG MUSIC CONNOISSEUR 130701 LTD INTERNATIONAL COLLECTIONS 3 BEAT LABEL BLAIRHILL MEDIA LTD (FIRST NIGHT RECORDS) MANAGEMENT LTD BLIX STREET RECORDS COOKING VINYL LTD A&G PRODUCTIONS LTD (TOON COOL RECORDS) LTD BLUEPRINT RECORDING CR2 RECORDS ABSOLUTE MARKETING CORP CREATION RECORDS INTERNATIONAL LTD BOROUGH MUSIC LTD CREOLE RECORDS ABSOLUTE MARKETING BRAVOUR LTD CUMBANCHA LTD & DISTRIBUTION LTD BREAKBEAT KAOS CURB RECORDS LTD ACE RECORDS LTD BROWNSWOOD D RECORDS LTD (BEAT GOES PUBLIC, BIG RECORDINGS DE ANGELIS RECORDS BEAT, BLUE HORIZON, BUZZIN FLY RECORDS LTD BLUESVILLE, BOPLICITY, CARLTON VIDEO DEAGOSTINI CHISWICK, CONTEMPARY, DEATH IN VEGAS FANTASY, GALAXY, CEEDEE MAIL T/A GLOBESTYLE, JAZZLAND, ANGEL AIR RECS DECLAN COLGAN KENT, MILESTONE, NEW JAZZ, CENTURY MEDIA MUSIC ORIGINAL BLUES, BLUES (PONEGYRIC, DGM) CLASSICS, PABLO, PRESTIGE, CHAMPION RECORDS DEEPER SUBSTANCE (CHEEKY MUSIC, BADBOY, RIVERSIDE, SOUTHBOUND, RECORDS LTD SPECIALTY, STAX) MADHOUSE ) ADA GLOBAL LTD CHANDOS RECORDS DEFECTED RECORDS LTD ADVENTURE RECORDS LTD (2 FOR 1 BEAR ESSENTIALS, (ITH, FLUENTIAL) AIM LTD T/A INDEPENDENTS BRASS, CHACONNE, DELPHIAN RECORDS LTD DAY RECORDINGS COLLECT, FLYBACK, DELTA LEISURE GROPU PLC AIR MUSIC AND MEDIA HISTORIC, SACD) DEMON MUSIC GROUP AIR RECORDINGS LTD CHANNEL FOUR LTD ALBERT PRODUCTIONS TELEVISON (IMP RECORDS) ALL AROUND THE CHAPTER ONE DEUX-ELLES WORLD PRODUCTIONS RECORDS LTD DHARMA RECORDS LTD LTD CHEMIKAL- DISTINCTIVE RECORDS AMG LTD UNDERGROUND LTD (BETTER THE DEVIL) RECORDS DISKY COMMUNICATIONS -

Abuse of Dominantposition and Switching Costs

UNIVERSITY OF LONDON REFUSAL TO LICENSE: ABUSE OF DOMINANT POSITION AND SWITCHING COSTS NET LE SUBMITTED TO THE LAW DEPARTMENT OF THE LONDON SCHOOL OF ECONOMICS AND POLITICAL SCIENCE FOR THE DEGREE OF DOCTOR OF PHILOSOPHY LONDON, MAY 2004 U /« 3 L \ * f LONDIU) \ WtfV. / UMI Number: U615726 All rights reserved INFORMATION TO ALL USERS The quality of this reproduction is dependent upon the quality of the copy submitted. In the unlikely event that the author did not send a complete manuscript and there are missing pages, these will be noted. Also, if material had to be removed, a note will indicate the deletion. Dissertation Publishing UMI U615726 Published by ProQuest LLC 2014. Copyright in the Dissertation held by the Author. Microform Edition © ProQuest LLC. All rights reserved. This work is protected against unauthorized copying under Title 17, United States Code. ProQuest LLC 789 East Eisenhower Parkway P.O. Box 1346 Ann Arbor, Ml 48106-1346 Th e s e s F 353£ . Library British Library of Political and Economic Science IJW 5S 5 II ACKNOWLEDGEMENT Foremost, I wish to express my deep gratitude to my supervisors, Professor William T. Murphy and Mr. Andrew Murray for their continual support throughout this thesis. Their comments have helped to essentially improve the accuracy of my research. Further, I wish to thank Mr. Giorgio Monti for reviewing my drafts, sharing with me books, giving me invaluable feedback and assistance. Others from LSE whom I would like to thank include Doctors Carsten Sorensen and Ole Hanseth (Department of Information System), Professors Max Steuer, Dany Quah and Michele Picione (Department of Economics) for reading my drafts, generously sharing with me their knowledge, improving my understanding and moreover providing me with excellent research inspiration. -

Heavy? You Must Be Crazy

YOUR FREE WEEKDAY AFTERNOON SOURCE FOR NEWS, SPORTS AND ENTERTAINMENT 03 27 2008 Heavy? You must be crazy Sporting a belly at 40 seriously increases your chances of getting Alzheimer’s later. p.10 Look whom John McCain brought to Utah. p.4 Huge bills freak out Questar customers. p.4 All-you-can-eat seats for sports fan. p.14 SOMETHING TO BUZZ ABOUT Bartender, Another Hemotoxin Please Murder Suspect Not a Flight Risk A Texas rattlesnake rancher found Popplewell said his intent is not A morbidly obese Texas woman Mayra Lizbeth Rosales, who a new way to make money: Stick a to sell an alcoholic beverage but a who authorities originally thought weighs at least 800 pounds and is rattler inside a bottle of vodka and healing tonic. He said he uses the might have crushed her 2-year-old bedridden, was photographed and market the concoction as an “an- cheapest vodka he can find as a nephew to death was arraigned in fingerprinted at her La Joya home cient Asian elixir.” But Bayou Bob preservative for the snakes. The her bedroom Wednesday on a cap- before being released on a per- Popplewell has no liquor license and end result is a super sweet mixed ital murder charge, accused of strik- sonal recognizance bond, Hidalgo faces charges. drink he compared to cough syrup. ing him in the head. County Sheriff Lupe Trevino said. 27mar08 TheWeather Tonight Partly cloudy. 29° theprimer Sunset: 7:47 p.m. Friday 50° Mostly cloudy; 50 INTERNET percent chance of late rain and snow An Educational, Saturday and Fruitful, Site 45° Mostly cloudy; 40 A colorful, new interactive Web site, percent chance of rain designed to educate children ages 2 and snow. -

Audiences, Gender and Community in Fan Vidding Katharina M

University of Wollongong Research Online University of Wollongong Thesis Collection University of Wollongong Thesis Collections 2011 "Veni, Vidi, Vids!" audiences, gender and community in Fan Vidding Katharina M. Freund University of Wollongong, [email protected] Recommended Citation Freund, Katharina M., "Veni, Vidi, Vids!" audiences, gender and community in Fan Vidding, Doctor of Philosophy thesis, School of Social Sciences, Media and Communications, Faculty of Arts, University of Wollongong, 2011. http://ro.uow.edu.au/theses/3447 Research Online is the open access institutional repository for the University of Wollongong. For further information contact the UOW Library: [email protected] “Veni, Vidi, Vids!”: Audiences, Gender and Community in Fan Vidding A thesis submitted in fulfilment of the requirements for the award of the degree Doctor of Philosophy From University of Wollongong by Katharina Freund (BA Hons) School of Social Sciences, Media and Communications 2011 CERTIFICATION I, Katharina Freund, declare that this thesis, submitted in fulfilment of the requirements for the award of Doctor of Philosophy, in the Arts Faculty, University of Wollongong, is wholly my own work unless otherwise referenced or acknowledged. The document has not been submitted for qualifications at any other academic institution. Katharina Freund 30 September, 2011 i ABSTRACT This thesis documents and analyses the contemporary community of (mostly) female fan video editors, known as vidders, through a triangulated, ethnographic study. It provides historical and contextual background for the development of the vidding community, and explores the role of agency among this specialised audience community. Utilising semiotic theory, it offers a theoretical language for understanding the structure and function of remix videos. -

Summit Guide Guide Du Sommet Guía De La Cumbre Contents/Sommaire/Sumario

New Frontiers for Creators in the Marketplace 9-10 June 2009 – Ronald Reagan Center – Washington DC, USA www.copyrightsummit.com Summit Guide Guide du Sommet Guía de la Cumbre Contents/Sommaire/Sumario Page Welcome 1 Conference Programme 3 What’s happening around the Summit? 11 Additional Summit Information 12 Page Bienvenue 14 Programme des conférences 15 Autres événements autour du sommet ? 24 Informations supplémentaires du sommet 25 Página Bienvenidos 27 Programa de las Conferencias 28 ¿Lo que pasa alrededor del conferencia? 38 Información sobre el conferencia 39 Page Sponsor & Advisory Committee Profiles 41 Partner Organization Profiles 44 Media Partner Profiles 49 Speaker Biographies 53 9-10 June 2009 – Ronald Reagan Center – Washington DC, USA New Frontiers for Creators in the Marketplace Welcome Welcome to the World Copyright Summit! Two years on from our hugely successful inaugural event in Brussels it gives me great pleasure to welcome you all to the 2009 World Copyright Summit in Washington, DC. This year’s slogan for the Summit – “New Frontiers for Creators in the Marketplace” – illustrates perfectly what we aim to achieve here: remind to the world that creators’ contributions are fundamental for cultural, economic and social development but also that creators – and those who represent them – face several daunting challenges in this new digital economy. It is imperative that we bring to the forefront of political debate the creative industries’ future and where we, creators, fit into this new landscape. For this reason we have gathered, under the CISAC umbrella, all the stakeholders involved one way or another in the creation, production and dissemination of creative works. -

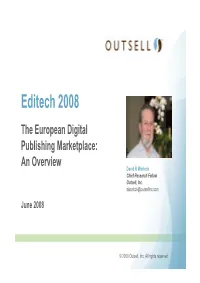

01 Worlock Editech 2008

Editech 2008 The European Digital Publishing Marketplace: An Overview David R Worlock Chief Research Fellow Outsell, Inc. [email protected] June 2008 © 2008 Outsell, Inc. All rights reserved. Slower Growth Ahead © 2008 Outsell, Inc. All rights reserved. 2 Search Surges Ahead of Information Industry 26.1% 25.1% 25.2% 24.8% 21.6% 22.5% 18.3% 9.0% 5.0% 4.3% 3.1% 3.1% 3.2% 3.4% 2004 2005 2006 2007 (P) 2008 (P) 2009 (P) 2010 (P) Search, Aggregation & Syndication Info Industry w/o SAS Source: Outsell’s Publishers & Information Providers Database © 2008 Outsell, Inc. All rights reserved. 3 Information Industry $380 Billion in 2007 9% 7% B2B Trade Publishing & Company Information 10% Credit & Financial Information 11% Education & Training HR Information Legal, Tax & Regulatory 5% 10% Market Research, Reports & Services IT & Telecom Research, 1% Reports & Services News Providers & Publishers 4% Scientific, Technical & Medical Information Search, Aggregation & 8% Syndication 1% Yellow Pages & Telephone 34% Directories Source: Outsell’s Publishers & Information Providers Database © 2008 Outsell, Inc. All rights reserved. 4 Search to Soar, While News Nosedives 2007-2010 Est. Industry Growth 5.5% Search, Aggregation & 22.7% Syndication HR Information 15.4% 9.5% IT & Telecom Research, Reports & Services 8.4% Credit & Financial Information 8.1% Market Research, Reports & Services 6.7% Scientific, Technical & Medical 6.7% Information Legal, Tax & Regulatory 5.8% B2B Trade Publishing & 5.7% Company Information Education & Training 5.2% -2.9% Yellow Pages & Directories Source: Outsell's Publishers & Information Providers Database News Providers & Publishers © 2008 Outsell, Inc. All rights reserved. 5 Global Growth in Asia and EMEA © 2008 Outsell, Inc. -

The Ghikas House on Hydra: from Artists’ Haven to Enchanted Ruins

The Ghikas House on Hydra: From Artists’ Haven to Enchanted Ruins HELLE VALBORG GOLDMAN Norwegian Polar Institute We sat on the terrace under the starry sky and talked about poetry, we drank wine, we swam, we rode donkeys, we played chess—it was like life in a novel. (Ghikas, quoted in Arapoglou 56) Introduction The Greek island of Hydra has become known for the colony of expatriate painters and writers that became established there in the 1950s and 60s (Genoni and Dalziell 2018; Goldman 2018). Two ‘literary houses,’ the homes of several of the island’s most well-known foreign residents during that era—the Australian couple, writers George Johnston and Charmian Clift, and Canadian singer-songwriter Leonard Cohen—have become places of pilgrimage for aficionados of Australian literature and popular music. Visitors wend through the maze of car- less, stone-paved lanes, asking for directions along the way, in order to stand outside the objects of their quests. Standing in the small public courtyard in front of the Johnstons’ house, or the tight laneway fronting the Cohen house, there is not much to see—the houses are quiet, the doors closed, the stone and white-washed walls surrounding the properties, which are typical of Hydra, are high. This doesn’t keep people from coming. They can picture in their minds’ eyes what is on the other side of the walls, having seen photographs of the writers at work and leisure inside the houses, and having read the books and listened to the songs that were written while the Johnstons and Cohen were in residence. -

Internet Peer-To-Peer File Sharing Policy Effective Date 8T20t2010

Title: Internet Peer-to-Peer File Sharing Policy Policy Number 2010-002 TopicalArea: Security Document Type Program Policy Pages: 3 Effective Date 8t20t2010 POC for Changes Director, Office of Computing and Information Services (OCIS) Synopsis Establishes a Dalton State College-wide policy regarding copyright infringement. Overview The popularity of Internet peer-to-peer file sharing is often the source of network resource allocation problems and copyright infringement. Purpose This policy will define Internet peer-to-peer file sharing and state the policy of Dalton State College (DSC) on this issue. Scope The scope of this policy includes all DSC computing resources. Policy Internet peer-to-peer file sharing applications are frequently used to distribute copyrighted materials such as music, motion pictures, and computer software. Such exchanges are illegal and are not permifted on Dalton State Gollege computers or network. See the standards outlined in the Appropriate Use Policy. DSG Procedures and Sanctions Failure to comply with the appropriate use of these resources threatens the atmosphere for the sharing of information, the free exchange of ideas, and the secure environment for creating and maintaining information property, and subjects one to discipline. Any user of any DSC system found using lT resources for unethical and/or inappropriate practices has violated this policy and is subject to disciplinary proceedings including suspension of DSC privileges, expulsion from school, termination of employment and/or legal action as may be appropriate. Although all users of DSC's lT resources have an expectation of privacy, their right to privacy may be superseded by DSC's requirement to protect the integrity of its lT resources, the rights of all users and the property of DSC and the State. -

Audio + Video 6/8/10 Audio & Video Releases *Click on the Artist Names to Be Taken Directly to the Sell Sheet

New Releases WEA.CoM iSSUE 11 JUNE 8 + JUNE 15 , 2010 LABELS / PARTNERS Atlantic Records Asylum Bad Boy Records Bigger Picture Curb Records Elektra Fueled By Ramen Nonesuch Rhino Records Roadrunner Records Time Life Top Sail Warner Bros. Records Warner Music Latina Word audio + video 6/8/10 Audio & Video Releases *Click on the Artist Names to be taken directly to the Sell Sheet. Click on the Artist Name in the Order Due Date Sell Sheet to be taken back to the Recap Page Street Date CD- WB 522739 AGAINST ME! White Crosses $13.99 6/8/10 N/A CD- White Crosses (Limited WB 524438 AGAINST ME! Edition) $13.99 6/8/10 5/19/10 White Crosses (Vinyl WB A-522739 AGAINST ME! w/Download Card) $18.98 6/8/10 5/19/10 CD- CUR 78977 BRICE, LEE Love Like Crazy $18.98 6/8/10 5/19/10 DV- WRN 523924 CUMMINS, DAN Crazy With A Capital F (DVD) $16.95 6/8/10 5/12/10 WB A-46269 FAILURE Fantastic Planet (2LP) $24.98 6/8/10 5/19/10 Selections From The Original Broadway Cast Recording CD- 'American Idiot' Featuring REP 524521 GREEN DAY Green Day $18.98 6/8/10 5/19/10 CD- RRR 177972 HAIL THE VILLAIN Population: Declining $13.99 6/8/10 5/19/10 CD- REP 519905 IYAZ Replay $9.94 6/8/10 5/19/10 CD- FBY 524007 MCCOY, TRAVIE Lazarus $13.99 6/8/10 5/19/10 CD- FBY 524670 MCCOY, TRAVIE Lazarus (Amended) $13.99 6/8/10 5/19/10 CD- ATL 522495 PLIES Goon Affiliated $18.98 6/8/10 5/19/10 CD- ATL 522497 PLIES Goon Affiliated (Amended) $18.98 6/8/10 5/19/10 The Twilight Saga: Eclipse CD- Original Motion Picture ATL 523836 VARIOUS ARTISTS Soundtrack $18.98 6/8/10 5/19/10 The Twilight Saga: -

Singer Kendra Shank Pays Tribute to Spirited Music of Abbey Lincoln

Photo by John Abbott Photo by John Kendra Shank will bring the music of Abbey Lincoln to Lincoln June 5. Singer Kendra Shank pays tribute ○○○○○○○○○○○○○○○○○○○○○ to spirited music of Abbey Lincoln ○○○○○○○○○○○○ By Tom Ineck ○○○○○○○○○○○○○○○○○○○○○ April 2007 Vol. 12, Number 2 With her new release, “A Spirit File Photo Free: Abbey Lincoln Songbook,” singer Kendra Shank has taken on a daunting task—interpreting the music of one of the most idiosyn- cratic jazz singer-songwriters in his- ○○○○○○○○○○○○○○○○○○○○○○○○○○○○○○○○○○○○ tory. In this issue of Jazz.... She and her longtime ensemble will bring the music of Lincoln to Prez Sez.........................................................2 Lincoln, Neb., June 5 in the open- Abbey Lincoln John Pizzarelli review........................6 ing concert of this year’s Jazz in Giacomo Gates/NJO review..................7 June series. this record were created there, on In a recent interview, Shank the gigs at that club. We would just Chick Corea/Gary Burton review...........8 talked about the recording and the try stuff and see what worked well Maria Schneider Orchestra review.....9 years it took to bring to fruition. and what didn’t work well,” she Mac McCune/NJO review......................10 Unlike many jazz musicians liv- said, pretty much describing the cre- Tomfoolery: Generous jazz calendar......11 ing in New York City, Shank has a ative process inherent in jazz mu- regular gig where she and the band sic. Harry “The Hipster” Gibson..................12 can work up new material and hone To Shank’s knowledge, no one Jazz on Disc reviews...........................14 their music to a fine edge. One Fri- else has ever attempted a full-length Discorama reviews..............................18 day a month, they appear at the 55 tribute to Lincoln’s very personal Letters to the Editor...............................19 Bar, Shank’s home away from music, although some of her tunes home for five years. -

Public Song List 06.01.18.Xlsx

Title Creator 1 Instrument Setup Department Cover Date Issue # ... River unto Sea Acoustic Classic Jun‐17 294 101 South Peter Finger D A E G A D Off the Record Mar‐00 87 1952 Vincent Black Lightning Richard Thompson C G D G B E, Capo III Feature Nov/Dec 1993 21 '39 Brian May Acoustic Classic May‐15 269 500 Miles Traditional For Beginners Mar/Apr 1992 11 9th Variaon from "20 Variaons and Fugue onManuel Ponce Lesson Feature Nov‐10 215 A Blacksmith Courted Me Traditional C G C F C D Private Lesson May‐04 137 A Day at the Races Preston Reed D A D G B E Feature Jul/Aug 1992 13 A Grandmother's Wish Keola Beamer F Bb C F A D Private Lesson Sep‐01 105 A Hard Rain's A‐Gonna Fall Bob Dylan D A D G B E, Capo II Feature Dec‐00 96 A Night in Frontenac Beppe Gambetta D A D G A D Off the Record Jun‐04 138 A Tribute to Peador O'Donnell Donal Lunny D A D F# A D Feature Sep‐98 69 About a Girl Kurt Cobain Contemporary Classic Nov‐09 203 AC Good Times Acoustic Classic Aug‐15 272 Addison's Walk (excerpts) Phil Keaggy Standard Feature May/Jun 1992 12 After the Rain Chuck Prophet D A D G B E Song Craft Sep‐03 129 After You've Gone Henry Creamer Standard The Basics Sep‐05 153 Ain't Life a Brook Ferron Standard, Capo VII Song Craft Jul/Aug 1993 19 Ain't No Sunshine Bill Withers Acoustic Classic Mar‐11 219 Aires Choqueros Paco de Lucia Standard, Capo II Feature Apr‐98 64 Al Di Meola's Equipment Picks Al Di Meola Feature Sep‐01 105 Alegrias Paco Peña Standard Feature Sep/Oct 1991 8 Alhyia Bilawal (Dawn) Traditional D A D G B E Solo Jul/Aug 1991 7 Alice's Restaurant