2020 Instructions for Form 1040-NR

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Tax Strategies for Selling Your Company by David Boatwright and Agnes Gesiko Latham & Watkins LLP

Tax Strategies For Selling Your Company By David Boatwright and Agnes Gesiko Latham & Watkins LLP The tax consequences of an asset sale by an entity can be very different than the consequences of a sale of the outstanding equity interests in the entity, and the use of buyer equity interests as acquisition currency may produce very different tax consequences than the use of cash or other property. This article explores certain of those differences and sets forth related strategies for maximizing the seller’s after-tax cash flow from a sale transaction. Taxes on the Sale of a Business The tax law presumes that gain or loss results upon the sale or exchange of property. This gain or loss must be reported on a tax return, unless a specific exception set forth in the Internal Revenue Code (the “Code”) or the Treasury Department’s income tax regulations provide otherwise. When a transaction is taxable under applicable principles of income tax law, the seller’s taxable gain is determined by the following formula: the “amount realized” over the “adjusted tax basis” of the assets sold equals “taxable gain.” If the adjusted tax basis exceeds the amount realized, the seller has a “tax loss.” The amount realized is the amount paid by the buyer, including any debt assumed by the buyer. The adjusted tax basis of each asset sold is generally the amount originally paid for the asset, plus amounts expended to improve the asset (which were not deducted when paid), less depreciation or amortization deductions (if any) previously allowable with respect to the asset. -

Manual for the Negotiation of Bilateral Tax Treaties

United Nations United Nations Manual for the Negotiation of Bilateral Tax Treaties Treaties Tax the Negotiation of Bilateral for Manual Manual for the Negotiation of Bilateral Tax Treaties between Developed and Developing Countries between Developed and Developing Countries United Nations Manual for the Negotiation of Bilateral Tax Treaties between Developed and Developing Countries asdf United Nations New York, 2016 Copyright © June 2016 For further information, please contact: United Nations United Nations All rights reserved Department of Economic and Social Affairs Financing for Development Office United Nations Secretariat Two UN Plaza, Room DC2-2170 New York, N.Y. 10017, USA Tel: (1-212) 963-7633 • Fax: (1-212) 963-0443 E-mail: [email protected] Preface Domestic resource mobilization, including tax revenues, is central to achieving sustainable development. Taxes represent a stable source of finance that, complemented by other sources, is critical to financing the 2030 Agenda for Sustainable Development, including the Sustainable Development Goals (SDGs). Taxation is essential to providing public goods and services, increasing equity and helping manage macroeco- nomic stability. SDG 17 on the means of implementation and global partnership for sustainable development calls on the international community to strengthen domestic resource mobilization, including through international support to developing countries, to improve domestic capacity for tax and other revenue collection. Mobilizing domestic public revenue for investment in sus- tainable development has featured prominently on the financing for development agenda since the 1990s. The Addis Ababa Action Agenda (AAAA) of the Third International Conference on Financing for Development (Addis Ababa, 13 – 16 July 2015) provides a new global framework for financing sustainable development by aligning all financial flows and policies with economic, social and environmental priorities. -

Identifying Section 1231, 1245 and 1250 Gains, 0% Bracket and Form 4797

FOR LIVE PROGRAM ONLY Fundamentals of Capital Gains: Identifying Section 1231, 1245 and 1250 Gains, 0% Bracket and Form 4797 TUESDAY, JANUARY 21, 2020, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is approved for 2 CPE credit hours. To earn credit you must: • Participate in the program on your own computer connection (no sharing) – if you need to register additional people, please call customer service at 1-800-926-7926 ext. 1 (or 404-881-1141 ext. 1). Strafford accepts American Express, Visa, MasterCard, Discover. • Listen on-line via your computer speakers. • Respond to five prompts during the program plus a single verification code. • To earn full credit, you must remain connected for the entire program. WHO TO CONTACT DURING THE LIVE PROGRAM For Additional Registrations: -Call Strafford Customer Service 1-800-926-7926 x1 (or 404-881-1141 x1) For Assistance During the Live Program: -On the web, use the chat box at the bottom left of the screen If you get disconnected during the program, you can simply log in using your original instructions and PIN. Tips for Optimal Quality FOR LIVE PROGRAM ONLY Sound Quality When listening via your computer speakers, please note that the quality of your sound will vary depending on the speed and quality of your internet connection. If the sound quality is not satisfactory, please e-mail [email protected] immediately so we can address the problem. Fundamentals of Capital Gains: Identifying Section 1231, 1245 and 1250 Gains, 0% Bracket and Form 4797 January 21, 2020 -

Taxation of Individuals 2020

Taxation of individuals Luxembourg 2020 kpmg.lu Tax year The tax year corresponds to the calendar year. Tax rates Progressive tax rates ranging from 0% to 45.78% apply to taxable income not exceeding €200,004 (€400,008 for couples taxed jointly). The excess is subject to 45.78%. The calculation of Luxembourg income taxes depends on the taxable income and the individual’s family status, i.e. the tax class. Tax classes - residents Without With Aged at least children dependent 65 years children on 1 January 2020 Single 1 1a 1a Married / Partners * 1 1/1a 1 Married/Partners - joint 2 2 2 taxation ** Separated / Divorced*** 2 / 1 2 / 1a 2 / 1a Widow(er)*** 2 / 1a 2 / 1a 2 / 1a * Joint application before 31 March of the following year for separate tax filing ** Married taxpayers file jointly: mandatory joint taxation Taxpayers who have entered into a registered partnership agreement and who shared a common residence during the whole tax year can elect to be taxed jointly *** Residents who separated (legal separation), divorced or were widowed during a specific tax year are granted tax class 2 for the next 3 tax years 2 Taxation of individuals – Luxembourg 2020 3 Tax classes - non-residents Without With Aged at least children dependent 65 years children on 1 January 2020 Single 1 1a 1a Married * / Partners 1 1 1 Married/Partners filing 2 2 2 jointly** Separated / Divorced*** 2 / 1 2 / 1a 2 / 1a Widow(er)*** 2 / 1a 2 / 1a 2 / 1a * Tax class 1a maintained for partners with dependent children or aged at least 65 years ** Specific requests before -

Dividends and Capital Gains Information Page 1 of 2

Dividends and Capital Gains Information Page 1 of 2 Some of the dividends you receive and all net long term capital gains you recognize may qualify for a federal income tax rate As noted above, for purposes of determining qualified dividend lower than your federal ordinary marginal rate. income, the concept of ex-dividend date is crucial. The ex- dividend date of a fund is the first date on which a person Qualified Dividends buying a fund share will not receive any dividends previously declared by the fund. A list of fund ex-dividend dates for each Qualified dividends received by you may qualify for a 20%, 15% State Farm Mutual Funds® dividend paid with respect to 2020, or 0% tax rate depending on your adjusted gross income (or and the corresponding percentage of each dividend that may AGI) and filing status. For single filing status, the qualified qualify as qualified dividend income, is provided below for your dividend tax rate is 0% if AGI is $40,000 or less, 15% if AGI is reference. more than $40,000 and equal to or less than $441,450, and 20% if AGI is more than $441,450. For married filing jointly Example: status, the qualified dividend tax rate is 0% if AGI is $80,000 or You bought 10,000 shares of ABC Mutual Fund common stock less, 15% if AGI is more than $80,000 and equal to or less than on June 8, 2020. ABC Mutual Fund paid a dividend of 10 cents $496,600, and 20% if AGI is more than $496,600. -

Beijing Subway Map

Beijing Subway Map Ming Tombs North Changping Line Changping Xishankou 十三陵景区 昌平西山口 Changping Beishaowa 昌平 北邵洼 Changping Dongguan 昌平东关 Nanshao南邵 Daoxianghulu Yongfeng Shahe University Park Line 5 稻香湖路 永丰 沙河高教园 Bei'anhe Tiantongyuan North Nanfaxin Shimen Shunyi Line 16 北安河 Tundian Shahe沙河 天通苑北 南法信 石门 顺义 Wenyanglu Yongfeng South Fengbo 温阳路 屯佃 俸伯 Line 15 永丰南 Gonghuacheng Line 8 巩华城 Houshayu后沙峪 Xibeiwang西北旺 Yuzhilu Pingxifu Tiantongyuan 育知路 平西府 天通苑 Zhuxinzhuang Hualikan花梨坎 马连洼 朱辛庄 Malianwa Huilongguan Dongdajie Tiantongyuan South Life Science Park 回龙观东大街 China International Exhibition Center Huilongguan 天通苑南 Nongda'nanlu农大南路 生命科学园 Longze Line 13 Line 14 国展 龙泽 回龙观 Lishuiqiao Sunhe Huoying霍营 立水桥 Shan’gezhuang Terminal 2 Terminal 3 Xi’erqi西二旗 善各庄 孙河 T2航站楼 T3航站楼 Anheqiao North Line 4 Yuxin育新 Lishuiqiao South 安河桥北 Qinghe 立水桥南 Maquanying Beigongmen Yuanmingyuan Park Beiyuan Xiyuan 清河 Xixiaokou西小口 Beiyuanlu North 马泉营 北宫门 西苑 圆明园 South Gate of 北苑 Laiguangying来广营 Zhiwuyuan Shangdi Yongtaizhuang永泰庄 Forest Park 北苑路北 Cuigezhuang 植物园 上地 Lincuiqiao林萃桥 森林公园南门 Datunlu East Xiangshan East Gate of Peking University Qinghuadongluxikou Wangjing West Donghuqu东湖渠 崔各庄 香山 北京大学东门 清华东路西口 Anlilu安立路 大屯路东 Chapeng 望京西 Wan’an 茶棚 Western Suburban Line 万安 Zhongguancun Wudaokou Liudaokou Beishatan Olympic Green Guanzhuang Wangjing Wangjing East 中关村 五道口 六道口 北沙滩 奥林匹克公园 关庄 望京 望京东 Yiheyuanximen Line 15 Huixinxijie Beikou Olympic Sports Center 惠新西街北口 Futong阜通 颐和园西门 Haidian Huangzhuang Zhichunlu 奥体中心 Huixinxijie Nankou Shaoyaoju 海淀黄庄 知春路 惠新西街南口 芍药居 Beitucheng Wangjing South望京南 北土城 -

Doing Business in Russia

Doing Business in Russia Your Roadmap to Successful Investments Tax and Legal kpmg.ru 2 Doing Business in Russia Moscow © 2019 KPMG. All rights reserved. Doing Business in Russia 3 Foreword Dear Reader, This brochure has been prepared to provide you with an economic overview of Russia and to introduce the tax and legal issues that are important when planning to do business in Russia. In particular, we provide here a discussion of the benefits of investing in the special economic zones, as well as review current trends in the wider economy concerning innovation and modernisation. Russian tax and civil legislation is constantly developing, meaning that sometimes there is no clear answer to what might be considered a simple question. In such circumstances, court cases and rulings are important sources for interpreting legislation. The exchange rate used in this report is the average official exchange rate of the Russian Central Bank in February 2019, which was USD 1: RUB 65,8105. Please note that this brochure is not intended to provide tax or legal advice for any specific person or situation. Readers are strongly advised to seek professional assistance from advisors with experience of doing business in Russia before undertaking any business ventures themselves. About KPMG KPMG is one of the world’s biggest advisory, audit, and tax and legal firms. We are a global network of professional firms employing more than 207,000 outstanding professionals who work together to deliver value in 153 countries worldwide. KPMG has been working for 28 years in Russia and has more than 5,500 professionals working at 23 offices spread across 9 CIS countries. -

Osprey Nest Queen Size Page 2 LC Cutting Correction

Template Layout Sheets Organizing, Bags, Foundation Papers, and Template Layout Sheets Sort the Template Layout Sheets as shown in the graphics below. Unit A, Temp 1 Unit A, Temp 1 Layout UNIT A TEMPLATE LAYOUT SHEET CUT 3" STRIP BACKGROUND FABRIC E E E ID ID ID S S S Please read through your original instructions before beginning W W W E E E Sheet. Place (2) each in Bag S S S TEMP TEMP TEMP S S S E E A-1 A-1 A-1 E W W W S S S I I I D D D E E E C TEMP C TEMP TEMP U U T T A-1 A-1 T A-1 #6, #7, #8, and #9 L L I the queen expansion set. The instructions included herein only I C C C N N U U U T T T T E E L L L I I I N N N E E replace applicable information in the pattern. E Unit A, Temp 2, UNIT A TEMPLATE LAYOUT SHEET Unit A, Temp 2 Layout CUT 3" STRIP BACKGROUND FABRIC S S S E E E The Queen Foundation Set includes the following Foundation Papers: W W W S S S ID ID ID E TEMP E TEMP E TEMP Sheet. Place (2) each in Bag A-2 A-2 A-2 E E E D D D I I TEMP I TEMP TEMP S S S A-2 A-2 A-2 W W W C E C E E S S S U C C U C U U U T T T T T T L L L L IN IN L IN I I N #6, #7, #8, and #9 E E N E E NP 202 (Log Cabin Full Blocks) ~ 10 Pages E NP 220 (Log Cabin Half Block with Unit A Geese) ~ 2 Pages NP 203 (Log Cabin Half Block with Unit B Geese) ~ 1 Page Unit B, Temp 1, ABRIC F BACKGROUND Unit B, Temp 1 Layout E E T SHEE YOUT LA TE TEMPLA A T UNI E D I D I D I S S STRIP 3" T CU S W W E W TP 101 (Template Layout Sheets for Log Cabins and Geese) ~ 2 Pages E S S E S TEMP TEMP TEMP S S S E E E 1 A- 1 A- 1 A- W W W S S S I I I D D D E E E C C Sheet. -

Analyzing Physics Students' Ethical Reasoning During a Unit On

ANALYZING PHYSICS STUDENTS’ ETHICAL REASONING DURING A UNIT ON THE DEVELOPMENT OF THE ATOMIC BOMB: A CALL FOR MACRO-ETHICAL DISCUSSIONS IN THE PHYSICS CLASSROOM by Egla K. Ochoa-Madrid, B.S A thesis submitted to the Graduate Council of Texas State University in partial fulfillment of the requirements for the degree of Master of Science with a Major in Physics August 2020 Committee Members: Alice Olmstead, Chair Eleanor Close Hunter Close Ayush Gupta COPYRIGHT by Egla K. Ochoa-Madrid 2020 FAIR USE AND AUTHOR’S PERMISSION STATEMENT Fair Use This work is protected by the Copyright Laws of the United States (Public Law 94-553, section 107). Consistent with fair use as defined in the Copyright Laws, brief quotations from this material are allowed with proper acknowledgement. Use of this material for financial gain without the author’s express written permission is not allowed. Duplication Permission As the copyright holder of this work I, Egla K. Ochoa-Madrid, authorize duplication of this work, in whole or in part, for educational or scholarly purposes only. DEDICATION I dedicate this page to my beautiful mother. Todo lo que hago, lo hago en su honor. ACKNOWLEDGEMENTS I’d like to acknowledge my advisor Dr. Alice Olmstead and my research partner Dr. Brianne Gutmann. I’d like to acknowledge the rest of my committee Dr. Ayush Gupta, Dr. Eleanor Close, & Dr. Hunter Close for offering their expertise and guidance v TABLE OF CONTENTS Page ACKNOWLEDGEMENT .............................................................................................. -

Idioms-And-Expressions.Pdf

Idioms and Expressions by David Holmes A method for learning and remembering idioms and expressions I wrote this model as a teaching device during the time I was working in Bangkok, Thai- land, as a legal editor and language consultant, with one of the Big Four Legal and Tax companies, KPMG (during my afternoon job) after teaching at the university. When I had no legal documents to edit and no individual advising to do (which was quite frequently) I would sit at my desk, (like some old character out of a Charles Dickens’ novel) and prepare language materials to be used for helping professionals who had learned English as a second language—for even up to fifteen years in school—but who were still unable to follow a movie in English, understand the World News on TV, or converse in a colloquial style, because they’d never had a chance to hear and learn com- mon, everyday expressions such as, “It’s a done deal!” or “Drop whatever you’re doing.” Because misunderstandings of such idioms and expressions frequently caused miscom- munication between our management teams and foreign clients, I was asked to try to as- sist. I am happy to be able to share the materials that follow, such as they are, in the hope that they may be of some use and benefit to others. The simple teaching device I used was three-fold: 1. Make a note of an idiom/expression 2. Define and explain it in understandable words (including synonyms.) 3. Give at least three sample sentences to illustrate how the expression is used in context. -

Humane Society Return

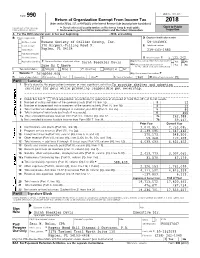

OMB No. 1545-0047 Form 990 Return of Organization Exempt From Income Tax 2018 Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private foundations) Open to Public Department of the Treasury G Do not enter social security numbers on this form as it may be made public. Internal Revenue Service G Go to www.irs.gov/Form990 for instructions and the latest information. Inspection A For the 2018 calendar year, or tax year beginning , 2018, and ending , B Check if applicable: C D Employer identification number Address change Humane Society of Collier County, Inc. 59-1033966 Name change 370 Airport-Pulling Road N. E Telephone number Initial return Naples, FL 34104 239-643-1880 Final return/terminated Amended return G Gross receipts $ 5,122,242. Is this a group return for subordinates? Application pending F Name and address of principal officer: Sarah Baeckler Davis H(a) Yes X No H(b) Are all subordinates included? Yes No Same As C Above If "No," attach a list. (see instructions) I Tax-exempt status: X 501(c)(3) 501(c) ()H (insert no.) 4947(a)(1) or 527 J Website: G hsnaples.org H(c) Group exemption number G K Form of organization: X Corporation Trust Association OtherG L Year of formation: 1960 M State of legal domicile: FL Part I Summary 1 Briefly describe the organization's mission or most significant activities:To provide shelter and adoption services for pets while promoting responsible pet ownership. 2 Check this box G if the organization discontinued its operations or disposed of more than 25% of its net assets. -

Analysis and Evaluation of the Beijing Metro Project Financing Reforms

Advances in Social Science, Education and Humanities Research, volume 291 International Conference on Management, Economics, Education, Arts and Humanities (MEEAH 2018) Analysis and Evaluation of the Beijing Metro Project Financing Reforms Haibin Zhao1,a, Bingjie Ren2,b, Ting Wang3,c 1Ministry of Transport Research Institute, Chaoyang, Beijing, China,100029; 2Beijing Urban Construction Design & Development Group Co., Limited, Xicheng, Beijing, China,100037; 3School of Civil Engineering, Beijing Jiaotong University, Haidian, Beijing, China, 100044. [email protected], [email protected], [email protected] Keywords: metro; financing; marketisation; reform Abstract. The construction and operation of a metro system are costly, and the sustainable development of a metro system is difficult using government funding alone, particularly for developing countries. The main source for metro system financing in China is, currently, government budget and bank debt. Many cities have begun to seek new ways to attract funds from finance markets, which is increasing the need for the evaluation of metro financing. This study uses Beijing as a case study that utilises various financing modes with impressive results. As participants of the financing reform, the authors collected all the relative government documents and interviewed stakeholders to accomplish this work. This article reviews the development of financing modes for the Beijing Metro system during the last four decades and analyses the role of the government in the reformed financing system within the Chinese social political environment. The study addresses the advantages and challenges of the reforms in this context. To further analyses the technical processes of typical financing modes, the public-private partnership mode of Line 4, the BT mode of Olympic Branch Line, the insurance claim mode of Line 10 and the failure of the market oriented financing for Capital Airport Line are analysed and evaluated in detail.