Value Chain Analysis of Allo (Girardinia Diversifolia)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Agricultural Transformation Around Koshi Hill Region: a Rural Development Perspective

95 NJ: NUTA Agricultural Transformation around Koshi Hill Region: A Rural Development Perspective Tirtha Raj Timalsina Lecturer, Dhankuta Multiple Campus, Dhankuta Eastern Nepal Email for correspondence:[email protected] Abstract Agriculture is considered to be the basic segment and the backbone of developing economy. In the same way it is a prime and domonent sector of Nepalese rural livelihood. By considering this fact, the true value of rural development lies on the rapid transformation of existing agricultural sector. The aim of this study is to analyze the role of agricultural transformation for rural development of Koshi Hill Region (KHR) of eastern Nepal. Both the primary as well as secondary data and information have been used to obtain the required findings. The study reveals the fact that agriculture is inevitable for rural people and its transformation is essential for the development of rural areas and the nation as a whole. Including primarily to the road network, the development of infrastructure can play the detrimental role to change the backward and rural scenario of this country. Key words: Agricultural transformation, rural development, Koshi-Hill, essential, backbone, access. Conceptualization Agriculture is an important segment of traditional (feudal) economy, the transformation from feudalism to capitalism necessarily implies a transformation of agriculture (Lekhi, 2005). Thereby, agriculture is the prime occupation and also the backbone of most of the developing economies. The countries that are in the low profile of international comparision, no doubt they are moving on stagnat and backward agriculture with under or misutilized physical as well as human resources. The country which are backward and underdeveloped are not always facing the scarcity of resources but the techniques or to know how to manage the scarcely available means and reslurces is accepted as the principal understanding of development science. -

Commercialization of Mandarin Orange in Solukhumbu District, Nepal

K.N. Pant et al. (2019) Int. J. Soc. Sc. Manage. Vol. 6, Issue-4: 97-104 DOI: 10.3126/ijssm.v6i4.26223 Research Article Commercialization of Mandarin Orange in Solukhumbu District, Nepal: Input, Production, Storage and Marketing Problem Assessment Kamal Nayan Pant1*, Dikshit Poudel1, Dipendra Kumar Bamma1, Shovit Khanal1, Madhav Dhital1 Agriculture and Forestry University, Nepal Abstract With the aim to assess major constraints and opportunities in commercialization along with the study of control measures and apposite services provided by stakeholders, the survey among 75 households from 5 different clusters in major citrus producing Dudhkoshi and Thulung Dudhkoshi regions during 2018 was conducted. The result from the pilot study portrays that – despite the long-term farming experiences in citrus, mandarins were unproductive in their orchards. Lack of technical knowledge, input supply, road and market access regarding commercial citrus farming has been major limiting aspect for orchard management and production. Likewise, condition of mechanical tools and record keeping was found poor from direct observation. 49.33% did not have storage facility for the fruit; problem on post-harvest and marketing was followed by poor transportation facility. The market for mandarin was the local market for 34 respondents where the price per kg was NRs. 77.94 which was significantly higher than the farmgate price (NRs. 49.02) at 5% level of significance. The fruit has invincible quality and taste. The development of collection centers, frequent monitoring and trainings for progressive farmers and input supplies management from government and private sectors are suggested, which can promote the productivity of citrus; thus, farming of mandarin can enhance livelihood and can be sustainable venture for the study area. -

Assessment of Health Seeking Behavior Regarding Complementary and Alternative Medicine in Solukhumbu District, Nepal

Original Article Nepal Med Coll J 2021; 23 (1): 23-30 Assessment of Health Seeking Behavior Regarding Complementary and Alternative Medicine in Solukhumbu District, Nepal Kafle PP, Pant PP, Dhakal N Department of Community Medicine, Nepal Medical College Teaching Hospital, Attarkhel, Gokarneshwor-8, Kathmandu, Nepal ABSTRACT The objective of the study was to assess the health seeking behavior of the people regarding complementary and alternative medicine (CAM) in remote area Dhudhakaushika, Gaunpalika of Solukumbu District during April – August 2017. The sample size was 300 (129 male and 171 female). Semi-structured question was design and Focus Group Discussion (FGD) was conducted. The results indicated that about three fourths of the respondents visited a modern medical institution 224 (74.7%), a little under one-half 129 (43.0%) visited Dhami-Jhakri and 85 (28.3%) contacted the Jharphuke who chanted a Mantra over a sick adult or child. Around 33 (11.0%) contacted the female community health volunteer (FCHV), 20 (6.7%) used domestic medicine or ethno- medicine, 13 (4.3%) visited a pharmacy and 9(3.0%) visited a private allopathic clinic when they felt discomfort. Respondents ascribed the cause of the disease to supernatural causes or evil spirits (53.3%), to germs (48.7%), curse of God (83.0%) to sins committed in the past (10.3%), and other causes (5.7%). The respondents usually consulted at firstDhami-Jhakri (43.0%) and Jharphuke (28.3%) when they fell sick. People utilized CAM in order to relieve undesired pain, uneasiness in the body and restore the health condition. The types of alternative medicine utilized by the respondents were Ayurveda 162 (54.0%), jadi-booti 248 (82.7%), homeopathy 94 (31.3%), relaxation 33 (11.0%), and meditation 68 (22.7%) healing touch 55 (18.3%), therapeutic massage 109 (36.3%), acupuncture 126 (42.0%), acupressure 44 (14.7%) Yoga 28 (3.3%) and 10 (3.3%) did not know any practice other than Dhamijhakri. -

ZSL National Red List of Nepal's Birds Volume 5

The Status of Nepal's Birds: The National Red List Series Volume 5 Published by: The Zoological Society of London, Regent’s Park, London, NW1 4RY, UK Copyright: ©Zoological Society of London and Contributors 2016. All Rights reserved. The use and reproduction of any part of this publication is welcomed for non-commercial purposes only, provided that the source is acknowledged. ISBN: 978-0-900881-75-6 Citation: Inskipp C., Baral H. S., Phuyal S., Bhatt T. R., Khatiwada M., Inskipp, T, Khatiwada A., Gurung S., Singh P. B., Murray L., Poudyal L. and Amin R. (2016) The status of Nepal's Birds: The national red list series. Zoological Society of London, UK. Keywords: Nepal, biodiversity, threatened species, conservation, birds, Red List. Front Cover Back Cover Otus bakkamoena Aceros nipalensis A pair of Collared Scops Owls; owls are A pair of Rufous-necked Hornbills; species highly threatened especially by persecution Hodgson first described for science Raj Man Singh / Brian Hodgson and sadly now extinct in Nepal. Raj Man Singh / Brian Hodgson The designation of geographical entities in this book, and the presentation of the material, do not imply the expression of any opinion whatsoever on the part of participating organizations concerning the legal status of any country, territory, or area, or of its authorities, or concerning the delimitation of its frontiers or boundaries. The views expressed in this publication do not necessarily reflect those of any participating organizations. Notes on front and back cover design: The watercolours reproduced on the covers and within this book are taken from the notebooks of Brian Houghton Hodgson (1800-1894). -

35173-013: Third Small Towns Water Supply and Sanitation Sector Project

Initial Environmental Examination Project Number: 35173-013 Loan Numbers: 3157 and 8304, Grant Number:0405 July 2020 Nepal: Third Small Towns Water Supply and Sanitation Sector Project - Enhancement Towns Project Prepared by the Government of Nepal for the Asian Development Bank This initial environmental examination is a document of the borrower. The views expressed herein do not necessarily represent those of ADB's Board of Directors, Management, or staff, and may be preliminary in nature. Your attention is directed to the “terms of use” section of this website. In preparing any country program or strategy, financing any project, or by making any designation of or reference to a particular territory or geographic area in this document, the Asian Development Bank does not intend to make any judgments as to the legal or other status of any territory or area. Updated Initial Environmental Examination July 2020 NEP: Third Small Towns Water Supply and Sanitation Sector Project – Phidim, Khandbari, Duhabi, Belbari, Birtamod DasarathChanda, Mahendranagar, Adarshnagar-Bhasi, Tikapur, Sittalpati, Bijuwar and Waling Enhancement Town Projects Prepared by Small Towns Water Supply and Sanitation Sector Project, Department of Water Supply and Sewerage Management, Ministry of Water Supply, Government of Nepal for the Asian Development Bank. Updated Initial Environmental Examination (IEE) of 12 Enhancement Small Town Projects Government of Nepal Ministry of Water Supply Asian Development Bank Updated Initial Environmental Examination (IEE) Of Phidim, Khandbari, Duhabi, Belbari, Birtamod, DasarathChanda, Mahendranagar, Adarshnagar-Bhasi, Tikapur, Sittalpati, Bijuwar, and Waling Enhancement Town Projects Submitted in July 2020 PROJECT MANAGEMENT OFFICE (PMO) Third Small Town Water Supply and Sanitation Sector Project Department of Water Supply and Sewerage Management Ministry of Water Supply Updated Initial Environmental Examination (IEE) of 12 Enhancement Small Town Projects Table of Contents ABBREVIATIONS EXECUTIVE SUMMARY 1. -

Damage from the April-May 2015 Gorkha Earthquake Sequence in the Solukhumbu District (Everest Region), Nepal David R

Damage from the april-may 2015 gorkha earthquake sequence in the Solukhumbu district (Everest region), Nepal David R. Lageson, Monique Fort, Roshan Raj Bhattarai, Mary Hubbard To cite this version: David R. Lageson, Monique Fort, Roshan Raj Bhattarai, Mary Hubbard. Damage from the april-may 2015 gorkha earthquake sequence in the Solukhumbu district (Everest region), Nepal. GSA Annual Meeting, Sep 2016, Denver, United States. hal-01373311 HAL Id: hal-01373311 https://hal.archives-ouvertes.fr/hal-01373311 Submitted on 28 Sep 2016 HAL is a multi-disciplinary open access L’archive ouverte pluridisciplinaire HAL, est archive for the deposit and dissemination of sci- destinée au dépôt et à la diffusion de documents entific research documents, whether they are pub- scientifiques de niveau recherche, publiés ou non, lished or not. The documents may come from émanant des établissements d’enseignement et de teaching and research institutions in France or recherche français ou étrangers, des laboratoires abroad, or from public or private research centers. publics ou privés. DAMAGE FROM THE APRIL-MAY 2015 GORKHA EARTHQUAKE SEQUENCE IN THE SOLUKHUMBU DISTRICT (EVEREST REGION), NEPAL LAGESON, David R.1, FORT, Monique2, BHATTARAI, Roshan Raj3 and HUBBARD, Mary1, (1)Department of Earth Sciences, Montana State University, 226 Traphagen Hall, Bozeman, MT 59717, (2)Department of Geography, Université Paris Diderot, 75205 Paris Cedex 13, Paris, France, (3)Department of Geology, Tribhuvan University, Tri-Chandra Campus, Kathmandu, Nepal, [email protected] ABSTRACT: Rapid assessments of landslides Valley profile convexity: Earthquake-triggered mass movements (past & recent): Traditional and new construction methods: Spectrum of structural damage: (including other mass movements of rock, snow and ice) as well as human impacts were conducted by many organizations immediately following the 25 April 2015 M7.8 Gorkha earthquake and its aftershock sequence. -

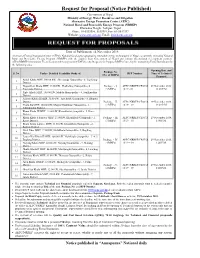

Request for Proposal (Notice Published)

Request for Proposal (Notice Published) Government of Nepal Ministry of Energy, Water Resources and Irrigation Alternative Energy Promotion Centre (AEPC) National Rural and Renewable Energy Program (NRREP) Khumaltar Height, Lalitpur, Nepal Phone: 01-5539390, 5539391, Fax: 01-5542397 Website: www.aepc.gov.np, Email: [email protected] Date of Publication: 14 November 2018 Alternative Energy Promotion Centre (AEPC): National focal agency promoting renewable energy technologies in Nepal, is currently executing National Rural and Renewable Energy Program (NRREP) with the support from Government of Nepal and various international development partners. AEPC/NRREP/Community Electrification Sub-Component (CESC) hereby Requests for Proposal (RFP) from eligible Consulting Firms/Institutions for the following tasks: Opening Date and Package No. S. No. Tasks - Detailed Feasibility Study of: RFP Number Time of Technical (No. of MHPs) Proposal Aamji Khola MHP, 100.00 kW, Shreejanga Gaunpalika - 8, Taplejung 1 District Nagpokhari Khola MHP, 15.00 kW, Phaktalung Gaunpalika - 6, Package - I, AEPC/NRREP/CESC/20 29 November 2018, 2 Taplejung District (3 MHPs) 18/19 - 01 12.20 P.M. Piple Khola MHP, 100.00 kW, Makalu Municipality - 4, Sankhusabha 3 District Aakuwa Khola II MHP, 32.00 kW, Amchowk Gaunpalika - 8, Bhojpur 4 District Package - II, AEPC/NRREP/CESC/20 29 November 2018, Cholu Ku MHP, 100.00 kW, Mapya Dhudhkosi Gaunpalika - 1, (2 MHPs) 18/19 – 02 12:40 P.M. 5 Solukhumbu District Khani Khola III MHP, 11.00 kW, Khanikhola Gaunpalika - 5, Kavre 6 District Khani Khola Falametar MHP, 23.00 kW, Khanikhola Gaunpalika - 2, Package - III, AEPC/NRREP/CESC/20 29 November 2018, 7 Kavre District (3 MHPs) 18/19 – 03 1:00 P.M. -

Sankhuwasabha

DTMP Sankhuwasabha 2012 FOREWORD It is my great pleasure to introduce this District Transport Master Plan (DTMP) of Sankhuwasabha district especially for district road core network (DRCN). I believe that this document will be helpful in backstopping to Rural Transport Inffrastructure Sector Wide Approach (RTI SWAp) through sustainable planning, resouurces mobilization, implementation and monitoring of the rural road sub-sector development. The document is anticipated to generate substantial employment opportunities for rural people through increased and reliable accessibility in on farm and off-farm livelihood diversification, and commercialization and industrialization of agriculture and other economic sectors, as well as harmonization of social centres. In this context, rural road sector will play a fundamental role to strengthen and promote overall economic growth of this district through established and improved year round transport services reiinforcing intra and inter-district linkages . Therefore, it is most crucial in executing rural road networks in a planned way as per the District Transport Master Plan (DTMP) by considering the framewwork of available resources in DDC comprising both inteernal and external sources. Viewing these aspects, DDC Sankhuwasabha has prepared the DTMP by focusing mostt of the available resources into upgrading and maintenance of the existing road networks. This document is also bbeen assumed to be helpful in lobbing and fascinating the donor agencies through central government towards generating needy resources through basket fund approach. Furthermore, this document not solely will be supportive in avoiding pervasive duplication approach in resources allocation under the rural road network development sector but also will be helpful in supporting overall development management of the district. -

Table of Province 01, Preliminary Results, Nepal Economic Census 2018

Number of Number of Persons Engaged District and Local Unit establishments Total Male Female Taplejung District 4,653 13,225 7,337 5,888 10101PHAKTANLUNG RURAL MUNICIPALITY 539 1,178 672 506 10102MIKWAKHOLA RURAL MUNICIPALITY 269 639 419 220 10103MERINGDEN RURAL MUNICIPALITY 397 1,125 623 502 10104MAIWAKHOLA RURAL MUNICIPALITY 310 990 564 426 10105AATHARAI TRIBENI RURAL MUNICIPALITY 433 1,770 837 933 10106PHUNGLING MUNICIPALITY 1,606 4,832 3,033 1,799 10107PATHIBHARA RURAL MUNICIPALITY 398 1,067 475 592 10108SIRIJANGA RURAL MUNICIPALITY 452 1,064 378 686 10109SIDINGBA RURAL MUNICIPALITY 249 560 336 224 Sankhuwasabha District 6,037 18,913 9,996 8,917 10201BHOTKHOLA RURAL MUNICIPALITY 294 989 541 448 10202MAKALU RURAL MUNICIPALITY 437 1,317 666 651 10203SILICHONG RURAL MUNICIPALITY 401 1,255 567 688 10204CHICHILA RURAL MUNICIPALITY 199 586 292 294 10205SABHAPOKHARI RURAL MUNICIPALITY 220 751 417 334 10206KHANDABARI MUNICIPALITY 1,913 6,024 3,281 2,743 10207PANCHAKHAPAN MUNICIPALITY 590 1,732 970 762 10208CHAINAPUR MUNICIPALITY 1,034 3,204 1,742 1,462 10209MADI MUNICIPALITY 421 1,354 596 758 10210DHARMADEVI MUNICIPALITY 528 1,701 924 777 Solukhumbu District 3,506 10,073 5,175 4,898 10301 KHUMBU PASANGLHAMU RURAL MUNICIPALITY 702 1,906 904 1,002 10302MAHAKULUNG RURAL MUNICIPALITY 369 985 464 521 10303SOTANG RURAL MUNICIPALITY 265 787 421 366 10304DHUDHAKOSHI RURAL MUNICIPALITY 263 802 416 386 10305 THULUNG DHUDHA KOSHI RURAL MUNICIPALITY 456 1,286 652 634 10306NECHA SALYAN RURAL MUNICIPALITY 353 1,054 509 545 10307SOLU DHUDHAKUNDA MUNICIPALITY -

OCHA Nepal Situation Overview

F OCHA Nepal Situation Overview Issue No. 19, covering the period 09 November -31 December 2007 Kathmandu, 31 December 2007 Highlights: • Consultations between the Seven Party Alliance (SPA) breaks political deadlock • Terai based Legislators pull out of government, Parliament • Political re-alignment in Terai underway • Security concerns in the Terai persist with new reports of extortion, threats and abductions • CPN-Maoist steps up extortion drive countrywide • The second phase of registration of CPN-Maoist combatants completed • Resignations by VDC Secretaries continue to affect the ‘reach of state’ • Humanitarian and Development actors continue to face access challenges • Displacements reported in Eastern Nepal • IASC 2008 Appeal completed CONTEXT Constituent Assembly. Consensus also started to emerge on the issue of electoral system to be used during the CA election. Politics and Major Developments On 19 November, the winter session of Interim parliament met Consultations were finalized on 23 December when the Seven but adjourned to 29 November to give time for more Party Alliance signed a 23-point agreement. The agreement negotiations and consensus on constitutional and political provided for the declaration of a republic subject to issues. implementation by the first meeting of the Constituent Assembly, a mixed electoral system with 60% of the members Citing failure of the government to address issues affecting of the CA to be elected through proportional system and 40% their community, four members of parliament from the through first-past-the-post system, and an increase in number Madhesi Community, including a cabinet minister affiliated of seats in the Constituent Assembly (CA) from the current 497 with different political parties resigned from their positions. -

Initial Environmental Examination: Nepal, Chainpur-Khandbari Road

Environmental Assessment Report Initial Environmental Examination for Chainpur-Khandbari Road Project Number: 44143 August 2010 NEP: Subregional Transport Enhancement Project Prepared by Department of Roads, Ministry of Physical Planning and Works for the Asian Development Bank (ADB). The initial environmental examination is a document of the borrower. The views expressed herein do not necessarily represent those of ADB’s Board of Directors, Management, or staff, and may be preliminary in nature. Table of Contents I. NAME AND ADDRESS OF THE INSTITUTION PREPARING THE REPORT............... 1 A. NAME OF THE PROPOSAL .............................................................................................. 1 B. NAME AND ADDRESS OF THE PROPONENT ..................................................................... 1 II. EXECUTIVE SUMMARY................................................................................................. 2 C. OBJECTIVE OF THE PROPOSAL ...................................................................................... 2 D. RELEVANCE OF THE PROPOSAL ..................................................................................... 2 E. ANTICIPATED IMPACTS BY THE PROPOSED SUBPROJECT ................................................ 2 III. DESCRIPTION OF THE PROJECT AND SUBPROJECT.............................................. 4 A. THE PROJECT ............................................................................................................... 4 B. RATIONALE .................................................................................................................. -

Phaplu Airport

PHAPLU AIRPORT Brief Description Phaplu Airport is situated at Solu Dudhkund Municipality of Solukhumbu District, Province No. 1. The airport is in close proximity to District Headquarter, Salleri. This airport is the gateway to Khumbu Trekking Route. General Information Name PHAPLU Location Indicator VNPL IATA Code PPL Aerodrome Reference Code 1B Aerodrome Reference Point 273053 N/0863510 E Province/District 1(One)/Solukhumbu Distance and Direction from City 1 Km North West Elevation 2468 m. /8097 ft. Contact Off: 977-38520153 Tower: 977-38520153 Fax: 977-38520153 AFS: VNPLYDYX E-mail: [email protected] Operation Hours 16th Feb to 15th Nov 0600LT-1215LT 16th Nov to 15th Feb 0630LT-1215LT Status In Operation Year of Start of Operation October, 1976 Serviceability All Weather Land Approx. 84288.04 m2 Re-fueling Facility Not Available Service AFIS Type of Traffic Permitted Visual Flight Rules (VFR) Type of Aircraft D228, DHC6, L410, Y12 Schedule Operating Airlines Tara Air, Sita Air, Nepal Airlines, Summit Air Schedule Connectivity Kathmandu, Lukla RFF Not Available Infrastructure Condition Airside Runway Type of Surface Bituminous Paved (Asphalt Concrete) Runway Dimension 680 m x 20 m Runway Designation 02/20 Parking Capacity Three D228 Types Size of Apron 1600 sq.m. Apron Type Asphalt Concrete Passenger Facilities Hotels Yes (city area) Restaurants Yes Transportations Jeep, Tractor, Van Internet Facility Wi-Fi Cable TV Yes Airport Facilities Console One Man Position Tower Console with Associated Equipment and Accessories Communication,