Puget Sound Office Market

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

North Bend, Washington

NORTH BEND, WASHINGTON PROPERTY OVERVIEW NORTH BEND PREMIUM OUTLETS ® NORTH BEND, WA MAJOR METROPOLITAN AREAS SELECT TENANTS Seattle: 31 miles west Bass Factory Outlet, Carter’s Outlet, Coach Factory Store, Cutter & Buck, Eddie Bauer Outlet, Jockey, Levi's, LOFT Outlet, Nike Factory RETAIL Store, OshKosh Outlet, Under Armour, VF Outlet, Volcom, Zumiez GLA (sq. ft.) 224,000; 50 stores TOURISM/TRAFFIC OPENING DATES The center is located in a region with economic diversity and stability. Microsoft and other high-tech industries are the economic drivers of Opened 1990 one of the fastest growing regions in the United States. Within a 60- Expanded 1995 mile radius of the center the population count is 4.1 million, with 50% earning $50,000 or more. PARKING RATIO The city of North Bend draws outdoor enthusiasts from around the country to take advantage of the many recreational activities such as 5.6:1 camping, hiking and bicycling. North Bend is also home to Nintendo North Bend, the main North RADIUS POPULATION American production facility and distribution center for the video game console manufacturer Nintendo. 15 miles: 197,094 30 miles: 2,329,218 45 miles: 4,077,720 60 miles: xxxxxxxxxx LOCATION/DIRECTIONS 461 South Fork Avenue SW, North Bend, WA 98045 AVERAGE HH INCOME East or West on I-90: Take Exit 31, North Bend Premium Outlets is 30 miles: $15,369 located at the exit interchange, on the north side of the highway. Information as of 5/1/21. Source: SPG Research; trade area demographic information per STI: PopStats (2020). OTHER RETAIL SHOPPING -

Off the Grid and Back to the Land Local Families Have Something to Teach Us About Self-Sufficiency

’cause parenting is a trip! Off the grid and back to the land Local families have something to teach us about self-sufficiency unplugged on the peninsula Camping, hiking, biking and more 27 A BREWING A GUY GOES WHEN GRANDMA GET TO KNOW JUNE 2016 BATHROOM BATTLE TO DAD SCHOOL HAS DEMENTIA DYLAN TOMINE Families mobilize to support Can teen daughters How to preserve bonds and How one dad fished and transgender youths 13 be a piece of cake? 41 help the kids understand 38 foraged to find closeness46 Recover ______________________________________Strength. Eating disorders become the number one priority. When you su er from an eating disorder, it takes over your life. You can become isolated and emotionally detached, losing interest in friends, and activities you used to enjoy. If you think you or someone you love may have an eating disorder, get help at Eating Recovery Center of Washington. And take back your life. #RecoverLife Locations: Bellevue, WA Programs: Residential, Partial Hospitalization and Intensive Outpatient levels of care Focus: Eating disorders as well as co-occuring and related conditions including: EatingRecoveryCenterWA.com BELLEVUE, WA Anxiety disorders, Trauma, Substance Abuse, Exercise Compulsion, Diabetes, Medical/Psychiatric (425) 608-9828 Complications Populations: Adults and adolescents, male and female inside JUNE 2016 27 46 18 WILL AUSTIN WILL AUSTIN FACEBOOK / KAYAK BRINNON Feature Ages + Stages Regulars 18 OFF THE GRID AND 38 4–10 Don’t let dementia 6 DEAR READER BACK TO THE LAND close the door How to Counter hate with love Local families have something preserve the bond between 11 PARENT FUEL to teach us about self-sufficiency kids and grandparents Family news, snack-sized 41 10–14 What I learned Parenting at dad school: Don’t worry 4 PARENTMAP.COM about hormones and periods — Father’s Day DIY, Dr. -

Bainbridge Police Officers Volunteer to Support Special Olympics

CITY OF BAINBRIDGE ISLAND FOR IMMEDIATE RELEASE MEDIA CONTACTS October 22, 2014 Matthew Hamner, Chief of Police Bainbridge Island Police Department [email protected] Bainbridge Police Officers Volunteer to Support Special Olympics Bainbridge Island, Wash., (October, 2014) – This Saturday, October 25, officers from the Bainbridge Island Police Department will take “serving the community” to a different level by volunteering to be celebrity waiters at the Red Robin in Silverdale to raise funds to support the Special Olympics. The “Tip- A-Cop” event will take place from 11:00 am to 8:00 pm. Law enforcement officers and department personnel from various local agencies will volunteer their time to collect tips to support the Special Olympics in Washington. “Tip-A-Cop” is an official Law Enforcement Torch Run Campaign fundraising event that takes place nationwide. The goal of the 2014 Red Robin “Tip-A-Cop” event is to raise more than $125,000 in Washington state. “The Bainbridge Island Police Department is proud to be part of this event to support the Special Olympics,” stated Chief Matthew Hamner. “By participating in sports, physical fitness and healthcare education programs, Special Olympics Washington athletes increase self-confidence and social skills, improve physical and motor skills, and have better success in leading more productive and independent lives. It is events like “Tip-A-Cop” that helps Special Olympics of Washington provide these programs at no cost to the athletes or their families.” Other Red Robin locations participating in this year’s Tip-a-Cop include Auburn, Bellevue Square, Bellingham, Bothell, Burlington, Covington, Des Moines, Everett, Factoria Mall, Federal Way, Issaquah, Kennewick, Kent, Lakewood, Lynnwood, Marysville, Monroe, Northgate, Olympia, Pier 55, Puyallup, Redmond Overlake, Redmond Town Center, Renton, Silverdale, Spokane Valley Mall, Spokane (downtown), Spokane (Newport Hwy.), Tacoma, Tukwila, Vancouver Mall, Vancouver (Mill Plain), Wenatchee, Woodinville, and Yakima. -

Effective 5/4/08 Macy's West SMALL TICKET DEPARTMENTS Store/DC List As of May 4, 2008

Macy's West SMALL TICKET DEPARTMENTS Store/DC List as of May 4, 2008 Current Current New New DC Division Store Division Store DC Alpha Effective Name Number Name Number Name Code Mall Name / Store Name Address City State Zip Date Macy's Northwest 0001 MCW 0301 Tukwila TU SEATTLE (DOWNTOWN) Third and Pine Seattle WA 98181 5/4/2008 Macy's Northwest 0002 MCW 0302 Tukwila TU NORTHGATE (WA) 401 NE Northgate Way Space 602 Seattle WA 98125 5/4/2008 Macy's Northwest 0003 MCW 0303 Tukwila TU TACOMA 4502 South Steele #700 Tacoma WA 98409 5/4/2008 Macy's Northwest 0004 MCW 0304 Tukwila TU WENATCHEE VALLEY 445 Valley Mall Pkwy E. Wenatchee WA 98802 5/4/2008 Macy's Northwest 0005 MCW 0305 Tukwila TU BELLIS FAIR (BELLINGHAM) 50 Bellis Fair Pkwy Bellingham WA 98226 5/4/2008 Macy's Northwest 0006 MCW 0306 Tukwila TU SPOKANE (DOWNTOWN) Main and Wall St Spokane WA 99201 5/4/2008 Macy's Northwest 0008 MCW 0308 Tukwila TU SOUTH CENTER (WA) 500 Southcenter Mall Tukwila WA 98188 5/4/2008 Macy's Northwest 0009 MCW 0309 Tukwila TU THREE RIVERS 331 Three Rivers Dr Kelso WA 98626 5/4/2008 Macy's Northwest 0010 MCW 0310 Tukwila TU WALLA WALLA (DOWNTOWN) 54 East Main St Walla Walla WA 99362 5/4/2008 Macy's Northwest 0011 MCW 0311 Tukwila TU COLUMBIA CENTER (WA) 1321 N.Columbia Center BLVD. Suite 400 Kennewick WA 99336 5/4/2008 Macy's Northwest 0012 MCW 0312 Tukwila TU NORTHTOWN (WA) N. -

Siff 2014 Festival Guide Starbucks Locations

SIFF 2014 FESTIVAL GUIDE STARBUCKS LOCATIONS Store Name Address City State Zip Ellingson Road- Auburn 4025 A STREET SE BLDG A AUBURN WA 98001 Auburn Fred Meyer 801 AUBURN WAY NORTH AUBURN WA 98002 Auburn Way South & M Street 1436 AUBURN WAY SOUTH AUBURN WA 98002 Auburn Way & 15th- Auburn 1420 HARVEY RD. NE AUBURN WA 98002 Sea Tac Mall 2002 SOUTH SEA-TAC MALL FEDERAL WAY WA 98003 320th St Drive-Thru 2032 SOUTH 320TH STREET FEDERAL WAY WA 98003 Federal Way Crossing 1401 SOUTH 348TH ST M101 FEDERAL WAY WA 98003 Bellevue 10214 NE 8TH BELLEVUE WA 98004 Downtown - Bellevue 606 NE 106TH BELLEVUE WA 98004 City Center Bellevue 500-108TH AVE. NE #1A1 BELLEVUE WA 98004 Main Street & Bellevue Way 42 BELLEVUE WAY NE BELLEVUE WA 98004 3 Bellevue Center 601 108TH AVENUE NE BELLEVUE WA 98004 Civic Office Building 225 108TH AVENUE NE BELLEVUE WA 98004 Bellevue Childrens Hospital 1500 116TH AVENUE BELLEVUE WA 98004 Bellevue Square II 226 BELLEVUE SQUARE BELLEVUE WA 98004 The Lodge 545 BELLEVUE SQUARE BELLEVUE WA 98004 Overlake Medical Pavilion 1231 116th AVENUE NE , SUITE 25 BELLEVUE WA 98004 120th Ave & NE 8th 661 120TH AVE NE BELLEVUE WA 98005 Evergreen Village 1645 140TH AVENUE NE BELLEVUE WA 98005 Factoria Village I 3560C 128TH AVE SE BELLEVUE WA 98006 Lakemont Village 4851 LAKEMONT #4 BELLEVUE WA 98006 Factoria Village II 3720 FACTORIA BOULEVARD SE BELLEVUE WA 98006 Eastgate-Bellevue 3181 156TH AVE SE BELLEVUE WA 98007 Kelsey Creek 15015 MAIN STREET BELLEVUE WA 98007 Crossroads 15600 N.E. 8TH #25 BELLEVUE WA 98008 Crossroads Drive - Thru 15600 N.E. -

REDMOND TOWN CENTER 7525 166Th Avenue NE | Redmond, WA 98052

REDMOND TOWN CENTER 7525 166th Avenue NE | Redmond, WA 98052 7325 166TH AVENUE NE, SUITE F-260 STEVE HANSEN STEVEN E. OLSEN JACOB MORGAN ALEX VLASKI REDMOND, WA 98052 [email protected] [email protected] [email protected] [email protected] 425.455.0500 | www.jshproperties.com Redmond, Washington offers all of the natural beauty and eclectic activity you seek in the Pacific Northwest. From serene and meandering bike paths to competitive cycling events; from lively outdoor concerts to diverse family activities; from an upscale outdoor shopping center to local boutique stores, Redmond is an unforgettable experience. You can also experience nearby wineries, dining for every taste, and luxury accommodations in Redmond’s world-class hotels. Redmond based companies are global technology leaders that are changing the world in which we live including software, aerospace, interactive media and electronics. From Microsoft, Nintendo, Oculus and Aerojet Rocketdyne to Physio-Control and Alstom Grid, these firms are developing the next technologies to advance the global economy from cloud computing, virtual reality, and smart grid to manned missions to Mars. These firms have proved the region can recruit and retain the technologically skilled talent pool for those companies interested in making Redmond home. Fun and exciting events take place all year long in Redmond. Regional and neighborhood parks, outdoor movies and concerts, sports tournaments, theater performances, annual festivals, a Saturday Farmers’ Market, and local arts highlight the long list of Redmond activities and events. Redmond is centrally located between Seattle/Bellevue and the Sammamish River Valley. Provided by experienceredmond.com and oneredmond.com N THE INFORMATION CONTAINED HEREIN HAS BEEN GIVEN TO US BY SOURCES WE DEEM RELIABLE, WE HAVE NO REASON TO DOUBT ITS ACCURACY, BUT WE DO NOT GUARANTEE IT. -

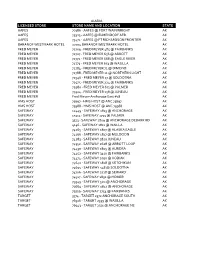

Licensed Store Store Name and Location State

ALASKA LICENSED STORE STORE NAME AND LOCATION STATE AAFES 70386 - AAFES @ FORT WAINWRIGHT AK AAFES 75323 - AAFES @ ELMENDORF AFB AK AAFES 75471 - AAFES @ FT RICHARDSON FRONTIER AK BARANOF WESTMARK HOTEL 22704 BARANOF WESTMARK HOTEL AK FRED MEYER 72709 - FRED MEYER 485 @ FAIRBANKS AK FRED MEYER 72727 - FRED MEYER 656 @ ABBOTT AK FRED MEYER 72772 - FRED MEYER 668 @ EAGLE RIVER AK FRED MEYER 72773 - FRED MEYER 653 @ WASILLA AK FRED MEYER 72784 - FRED MEYER 71 @ DIMOND AK FRED MEYER 72788 - FRED MEYER 11 @ NORTHERN LIGHT AK FRED MEYER 72946 - FRED MEYER 17 @ SOLDOTNA AK FRED MEYER 72975 - FRED MEYER 224 @ FAIRBANKS AK FRED MEYER 72980 - FRED MEYER 671 @ PALMER AK FRED MEYER 79324 - FRED MEYER 158 @ JUNEAU AK FRED MEYER Fred Meyer-Anchorage East #18 AK HMS HOST 75697 - HMS HOST @ ANC 75697 AK HMS HOST 75988 - HMS HOST @ ANC 75988 AK SAFEWAY 12449 - SAFEWAY 1813 @ ANCHORAGE AK SAFEWAY 15313 - SAFEWAY 1739 @ PALMER AK SAFEWAY 3513 - SAFEWAY 1809 @ ANCHORAGE DEBARR RD AK SAFEWAY 4146 - SAFEWAY 1811 @ WAILLA AK SAFEWAY 74265 - SAFEWAY 1807 @ ALASKA EAGLE AK SAFEWAY 74266 - SAFEWAY 1817 @ MULDOON AK SAFEWAY 74283 - SAFEWAY 1820 JUNEAU AK SAFEWAY 74352 - SAFEWAY 2628 @ ABBOTT LOOP AK SAFEWAY 74430 - SAFEWAY 1805 @ AURORA AK SAFEWAY 74452 - SAFEWAY 3410 @ FAIRBANKS AK SAFEWAY 74474 - SAFEWAY 1090 @ KODIAK AK SAFEWAY 74640 - SAFEWAY 1818 @ KETCHIKAN AK SAFEWAY 74695 - SAFEWAY 548 @ SOLDOTNA AK SAFEWAY 74706 - SAFEWAY 2728 @ SEWARD AK SAFEWAY 74917 - SAFEWAY 1832 @ HOMER AK SAFEWAY 79549 - SAFEWAY 520 @ ANCHORAGE AK SAFEWAY 79664 - SAFEWAY 1812 @ ANCHORAGE -

Major Retail, Specialty Area 250

Commercial Revalue 2019 Assessment roll MAJOR RETAIL AREA 250 King County, Department of Assessments Seattle, Washington John Wilson, Assessor Department of Assessments King County Administration Bldg. John Wilson 500 Fourth Avenue, ADM-AS-0708 Seattle, WA 98104-2384 Assessor (206)263-2300 FAX(206)296-0595 Email: [email protected] http://www.kingcounty.gov/assessor/ Dear Property Owners, Our field appraisers work hard throughout the year to visit properties in neighborhoods across King County. As a result, new commercial and residential valuation notices are mailed as values are completed. We value your property at its “true and fair value” reflecting its highest and best use as prescribed by state law (RCW 84.40.030; WAC 458-07-030). We continue to work hard to implement your feedback and ensure we provide accurate and timely information to you. We have made significant improvements to our website and online tools to make interacting with us easier. The following report summarizes the results of the assessments for your area along with a map. Additionally, I have provided a brief tutorial of our property assessment process. It is meant to provide you with background information about the process we use and our basis for the assessments in your area. Fairness, accuracy and transparency set the foundation for effective and accountable government. I am pleased to continue to incorporate your input as we make ongoing improvements to serve you. Our goal is to ensure every single taxpayer is treated fairly and equitably. Our office is here to serve you. Please don’t hesitate to contact us if you ever have any questions, comments or concerns about the property assessment process and how it relates to your property. -

Organizations with Certificates of Insurance

CERTIFICATES of INSURANCE 08.02.21 - 08.01.22 THIS IS A CURRENT LIST OF ORGANZIATIONS THAT HAVE RECEIVED GIRL SCOUTS OF WESTERN WASHINGTON COI. 4 CORNERS SELF STORAGE 24215 SE 271st Place Maple Valley WA 98038 Aberdeen School District 216 N. G St. Aberdeen WA 98520 Agnus Dei Lutheran Church Attn: Cindy 10511 Peacock HIll Ave NW Gig Harbor WA 98332 Aldersgate United Methodist Church Attn: Wendi Brick 14230 SE Newport Way Bellevue WA 98006 Alki UCC Attn: Larisa Wanserski 6115 SW Hinds Seattle WA 98116 American Girl Store Attn: Anthony Walser 3000 184th St SW Lynnwood WA 98037 Anacortes Lutheran Church Attn: Rachel Devine 2100 O Avenue Anacortes WA 98221 Anacortes School District 2200 M Ave Anacortes Anacortes WA 98221 Annie Wright Schools Attn: Erin Gann 827 N. Tacoma Ave Tacoma WA 98403 Archdiocese of Seattle St. John the Evangelist 106 N 79th St Seattle WA 98103 Archdiocese of Seattle-St Michael's School St. Michael Parish & School 1208 11th Avenue Olympia WA 98501 Arena Sports, Inc Attn: Whitney Simmons 9040 Willows Rd NE # 102 Redmond WA 98115 Arlington Boys & Girls Club 18513 59th Ave. NE Arlington WA 98223 Arlington School District Attn: Katherine Ray 315 North French Avenue Arlington WA 98223 Assumption St. Bridgett School 6220 32nd Ave., NE Seattle WA 98155 AUBURN PARKS & RECREATION 910 Ninth Street SE Auburn WA 98002 Auburn School District 915 - 4th Street, NE Auburn WA 98002 74169- Avis Budget Group, Inc. and its Subsidiaries 4500 S. 129th East Ave., Suite 100 PO Box 690360 Tulsa OK 0360 Bainbridge Island Parks & Recreation Attn: Mike Mejia 7666 NE High School Road Bainbridge Island WA 98110 Bainbridge Island School District 8489 Madison Ave. -

ALDERWOOD Lynnwood, Washington North Seattle TABLE of CONTENTS

ALDERWOOD Lynnwood, Washington North Seattle TABLE OF CONTENTS 03 PROPERTY OVERVIEW 04 MARKET DEMOGRAPICS 06 TRADE AREA DEMOGRAPHICS 08 OUR SHOPPER FEATURED RETAILERS & 09 DINING OPTIONS 10 ARE A GROW TH 11 SITE PLANS & RENDERINGS 19 ABOUT & CONTACT 3 PROPERTY OVERVIEW ALDERWOOD North Seattle’s Destination of Choice Alderwood is a unique shopping center in the northern suburbs of Seattle. This accessible, super-regional destination is situated at the intersection of highways I-5 and I-405—the two most heavily traveled freeways in the state. Alderwood is ideally located in the fastest- growing part of the Seattle trade area, with primary drivers being close proximity to the popular Northshore School District and the new light rail station opening in 2024. At Alderwood, affluent suburban shoppers enjoy a strong merchandise mix of more than 160 retail, entertainment, and dining options that span over 1.3 million square feet. Large interior and exterior fireplaces welcome visitors to The Terraces, a garden-like environment complete with restaurants and a 16-screen, state-of-the-art AMC Theatres. 4 MARKET DEMOGRAPHICS ALDERWOOD A premier West “Seattle remains a frontier Coast market metropolis, a place where people can experiment with their lives, Seattle is the largest city in the Pacific Northwest and is one of the fastest-growing major cities in the country due to job growth in key industry sectors such as information technology, clean energy, manufacturing, food and beverage, healthcare, and maritime. and change and grow and make DEMOGRAPHIC -

In the United States Bankruptcy Court for the District of Delaware

Case 20-13078-BLS Doc 7 Filed 12/31/20 Page 1 of 67 IN THE UNITED STATES BANKRUPTCY COURT FOR THE DISTRICT OF DELAWARE ------------------------------------------------------------ x In re: : Chapter 11 : FRANCESCA’S HOLDINGS CORPORATION, : Case No. 20-13076 (BLS) 1 et al., : Debtors. : Jointly Administered ------------------------------------------------------------ x STATEMENT OF FINANCIAL AFFAIRS FOR FRANCESCA'S COLLECTIONS, INC. (CASE NO. 20-13078) ____________________________________________ 1 The Debtors in these cases, along with the last four digits of each Debtor’s federal tax identification number, are Francesca’s Holdings Corporation (4704), Francesca’s LLC (2500), Francesca’s Collections, Inc. (4665), and Francesca’s Services Corporation (5988). The address of the Debtors’ corporate headquarters is 8760 Clay Road, Houston, Texas 77080. Case 20-13078-BLS Doc 7 Filed 12/31/20 Page 2 of 67 IN THE UNITED STATES BANKRUPTCY COURT FOR THE DISTRICT OF DELAWARE ------------------------------------------------------------ x : In re: : Chapter 11 : Case No. 20-13076 (BLS) FRANCESCA’S HOLDINGS CORPORATION, : et al.,1 : Jointly Administered : Debtors. : ------------------------------------------------------------ x GLOBAL NOTES, METHODOLOGY, AND SPECIFIC DISCLOSURES REGARDING THE DEBTORS’ SCHEDULES OF ASSETS AND LIABILITIES AND STATEMENTS OF FINANCIAL AFFAIRS Introduction Francesca’s Holdings Corporation and its affiliated debtors and debtors in possession (collectively, the “Debtors”), with the assistance of their advisors, have filed their respective Schedules of Assets and Liabilities (collectively, the “Schedules”) and Statements of Financial Affairs (collectively, the “Statements and together with the Schedules, the “Schedules and Statements”) with the United States Bankruptcy Court for the District of Delaware (the “Bankruptcy Court”), pursuant to section 521 of title 11 of the United States Code, §§ 101- 1532, et seq. -

Major Retail Specialty Area 250 Commercial Revalue for 2020 Assessment Roll

Major Retail Specialty Area 250 Commercial Revalue for 2020 Assessment Roll Department of Assessments Setting values, serving the community, and pursuing excellence 500 Fourth Avenue, ADM-AS 0708 Seattle, WA 98104-2384 OFFICE (206) 296-7300 FAX (206) 296-0595 Email: [email protected] http://www.kingcounty.gov/assessor/ Department of Assessments 1 Department of Assessments 500 Fourth Avenue, ADM-AS-0708 John Wilson Seattle, WA 98104-2384 OFFICE: (206) 296-7300 FAX (206) 296-0595 Assessor Email: [email protected] http://www.kingcounty.gov/assessor/ Dear Property Owners, Our field appraisers work hard throughout the year to visit properties in neighborhoods across King County. As a result, new commercial and residential valuation notices are mailed as values are completed. We value your property at its “true and fair value” reflecting its highest and best use as prescribed by state law (RCW 84.40.030; WAC 458-07-030). We continue to work to implement your feedback and ensure we provide you accurate and timely information. We have made significant improvements to our website and online tools to make interacting with us easier. The following report summarizes the results of the assessments for your area along with a map. Additionally, I have provided a brief tutorial of our property assessment process. It is meant to provide you with background information about our process and the basis for the assessments in your area. Fairness, accuracy and transparency set the foundation for effective and accountable government. I am pleased to continue to incorporate your input as we make ongoing improvements to serve you.