Top 100 Global Energy Leaders

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Oil & Gas, and Mining Associations, Organizations, and Company

2021 OIL & GAS, AND MINING ASSOCIATIONS, ORGANIZATIONS, AND COMPANY INFORMATION UNIVERSITY OF COLORADO DENVER ASSOCIATIONS AND ORGANIZATIONS Colorado Cleantech Industry Association – https://coloradocleantech.com/ Colorado Energy Coalition – http://www.metrodenver.org/news/news-center/2017/02/colorado-energy-coalition- takes-energy-%E2%80%98asks-to-congressional-delegation-in-washington,-dc/ Colorado Mining Association (CMA) – https://www.coloradomining.org/default.aspx Colorado Oil and Gas Association (COGA) – http://www.coga.org/ Colorado Petroleum Association – http://www.coloradopetroleumassociation.org/ Colorado Renewable Energy Society (CRES) – https://www.cres-energy.org/ Society of Petroleum Engineers – https://www.spe.org/en/ United States Energy Association – https://www.usea.org/ OIL AND GAS Antero Resources – http://www.anteroresources.com/ Antero Resources is an independent exploration and production (E&P) company engaged in the exploitation, development, and acquisition of natural gas, NGLs and oil properties located in the Appalachia Basin. Headquartered in Denver, Colorado, we are focused on creating value through the development of our large portfolio of repeatable, low cost, liquids-rich drilling opportunities in two of the premier North American shale plays. Battalion Oil – https://battalionoil.com/ http://www.forestoil.com/ Battalion Oil (Formerly Halcón Resources Corporation) is an independent energy company focused on the acquisition, production, exploration and development of onshore liquids-rich assets in the United States. While Battalion is a new venture, we operate on a proven strategy used in prior, successful ventures. We have experienced staff and use the most advanced technology, enabling us to make informed and effective business decisions. Spanish for hawk, Halcón embraces the vision and agility to become a resource powerhouse in the oil and gas industry. -

Market Index Uniflex 10%

Investment and retirement 5% 10% Market Index Uniflex 10% 25% Main Product Features 25% 6-year term (not redeemable before maturity) Guarantee of principal on maturity of 100% Low management fees of 1% per year 10% 15% $500 minimum deposit An easy way to diversify Cut-off age: 64 y/o (registered) and 70 y/o (non-registered) Even under a scenario where the return of each share is negative, this product may produce a global positive return Sector diversification of the Market Index Uniflex How it works On the settlement date, a starting level will be determined for each Canadian share included in the portfolio. On the maturity date, a ratio of the closing level over the starting level for each share will be computed. The 8 best performing shares during the 6-year term will be automatically assigned a fixed return of 60%, regardless of whether the actual return was positive or negative. The remaining 12 shares will be assigned their actual return. The global return (maximum 60%) will be calculated by averaging these 20 returns. The value at maturity will be the highest value between: the initial deposit; or the initial deposit PLUS global return (maximum 60%) Exposure to 20 Canadian companies included in the S&P/TSX 60 Index Company Sector Company Sector Metro Inc. Scotiabank Consumer staples Loblaw Companies Limited The Toronto-Dominion Bank Royal Bank of Canada Financial services Bank of Montreal Enbridge Inc. Sun Life Financial Inc. TransCanada Corporation Cenovus Energy Inc. Energy Canadian Natural Resources Limited Canadian National Railway Industrials Suncor Energy Inc. -

Secure Fuels from Domestic Resources ______Profiles of Companies Engaged in Domestic Oil Shale and Tar Sands Resource and Technology Development

5th Edition Secure Fuels from Domestic Resources ______________________________________________________________________________ Profiles of Companies Engaged in Domestic Oil Shale and Tar Sands Resource and Technology Development Prepared by INTEK, Inc. For the U.S. Department of Energy • Office of Petroleum Reserves Naval Petroleum and Oil Shale Reserves Fifth Edition: September 2011 Note to Readers Regarding the Revised Edition (September 2011) This report was originally prepared for the U.S. Department of Energy in June 2007. The report and its contents have since been revised and updated to reflect changes and progress that have occurred in the domestic oil shale and tar sands industries since the first release and to include profiles of additional companies engaged in oil shale and tar sands resource and technology development. Each of the companies profiled in the original report has been extended the opportunity to update its profile to reflect progress, current activities and future plans. Acknowledgements This report was prepared by INTEK, Inc. for the U.S. Department of Energy, Office of Petroleum Reserves, Naval Petroleum and Oil Shale Reserves (DOE/NPOSR) as a part of the AOC Petroleum Support Services, LLC (AOC- PSS) Contract Number DE-FE0000175 (Task 30). Mr. Khosrow Biglarbigi of INTEK, Inc. served as the Project Manager. AOC-PSS and INTEK, Inc. wish to acknowledge the efforts of representatives of the companies that provided information, drafted revised or reviewed company profiles, or addressed technical issues associated with their companies, technologies, and project efforts. Special recognition is also due to those who directly performed the work on this report. Mr. Peter M. Crawford, Director at INTEK, Inc., served as the principal author of the report. -

Trade Remedies, Targeting the Renewable Energy Sector

Green Economy and Trade. Ad hoc Expert Group 2: Trade Remedies in Green Sectors: the Case of Renewables 3−4 April 2014 Salle XXVI, Palais des Nations Geneva Trade Remedies Targeting the Renewable Energy Sector Report by 1 Cathleen Cimino & Gary Hufbauer 1 Cathleen Cimino is a Research Analyst at the Peterson Institute for International Economics and Gary Hufbauer is the Reginald Jones Senior Fellow. The views expressed are their own. Table of Contents I. Introduction .............................................................................................................................. 3 Clash between trade remedies and environmental goals ....................................................... 3 Outline of the report ............................................................................................................ 4 II. Overview of trade remedies ...................................................................................................... 5 III. Trade in renewable energy products affected by AD/CVD cases ............................................... 8 Methodology for the trade remedy survey ............................................................................ 9 Findings from the surveyt .................................................................................................. 10 IV. Renewable energy costs .......................................................................................................... 17 V. WTO disputes relating to renewable energy ........................................................................... -

Science for Energy Technology: Strengthening the Link Between Basic Research and Industry

ďŽƵƚƚŚĞĞƉĂƌƚŵĞŶƚŽĨŶĞƌŐLJ͛ƐĂƐŝĐŶĞƌŐLJ^ĐŝĞŶĐĞƐWƌŽŐƌĂŵ ĂƐŝĐŶĞƌŐLJ^ĐŝĞŶĐĞƐ;^ͿƐƵƉƉŽƌƚƐĨƵŶĚĂŵĞŶƚĂůƌĞƐĞĂƌĐŚƚŽƵŶĚĞƌƐƚĂŶĚ͕ƉƌĞĚŝĐƚ͕ĂŶĚƵůƟŵĂƚĞůLJĐŽŶƚƌŽů ŵĂƩĞƌĂŶĚĞŶĞƌŐLJĂƚƚŚĞĞůĞĐƚƌŽŶŝĐ͕ĂƚŽŵŝĐ͕ĂŶĚŵŽůĞĐƵůĂƌůĞǀĞůƐ͘dŚŝƐƌĞƐĞĂƌĐŚƉƌŽǀŝĚĞƐƚŚĞĨŽƵŶĚĂƟŽŶƐ ĨŽƌŶĞǁĞŶĞƌŐLJƚĞĐŚŶŽůŽŐŝĞƐĂŶĚƐƵƉƉŽƌƚƐKŵŝƐƐŝŽŶƐŝŶĞŶĞƌŐLJ͕ĞŶǀŝƌŽŶŵĞŶƚ͕ĂŶĚŶĂƟŽŶĂůƐĞĐƵƌŝƚLJ͘dŚĞ ^ƉƌŽŐƌĂŵĂůƐŽƉůĂŶƐ͕ĐŽŶƐƚƌƵĐƚƐ͕ĂŶĚŽƉĞƌĂƚĞƐŵĂũŽƌƐĐŝĞŶƟĮĐƵƐĞƌĨĂĐŝůŝƟĞƐƚŽƐĞƌǀĞƌĞƐĞĂƌĐŚĞƌƐĨƌŽŵ ƵŶŝǀĞƌƐŝƟĞƐ͕ŶĂƟŽŶĂůůĂďŽƌĂƚŽƌŝĞƐ͕ĂŶĚƉƌŝǀĂƚĞŝŶƐƟƚƵƟŽŶƐ͘ ďŽƵƚƚŚĞ͞ĂƐŝĐZĞƐĞĂƌĐŚEĞĞĚƐ͟ZĞƉŽƌƚ^ĞƌŝĞƐ KǀĞƌƚŚĞƉĂƐƚĞŝŐŚƚLJĞĂƌƐ͕ƚŚĞĂƐŝĐŶĞƌŐLJ^ĐŝĞŶĐĞƐĚǀŝƐŽƌLJŽŵŵŝƩĞĞ;^ͿĂŶĚ^ŚĂǀĞĞŶŐĂŐĞĚ ƚŚŽƵƐĂŶĚƐŽĨƐĐŝĞŶƟƐƚƐĨƌŽŵĂĐĂĚĞŵŝĂ͕ŶĂƟŽŶĂůůĂďŽƌĂƚŽƌŝĞƐ͕ĂŶĚŝŶĚƵƐƚƌLJĨƌŽŵĂƌŽƵŶĚƚŚĞǁŽƌůĚƚŽƐƚƵĚLJ ƚŚĞĐƵƌƌĞŶƚƐƚĂƚƵƐ͕ůŝŵŝƟŶŐĨĂĐƚŽƌƐ͕ĂŶĚƐƉĞĐŝĮĐĨƵŶĚĂŵĞŶƚĂůƐĐŝĞŶƟĮĐďŽƩůĞŶĞĐŬƐďůŽĐŬŝŶŐƚŚĞǁŝĚĞƐƉƌĞĂĚ ŝŵƉůĞŵĞŶƚĂƟŽŶŽĨĂůƚĞƌŶĂƚĞĞŶĞƌŐLJƚĞĐŚŶŽůŽŐŝĞƐ͘dŚĞƌĞƉŽƌƚƐĨƌŽŵƚŚĞĨŽƵŶĚĂƟŽŶĂůĂƐŝĐZĞƐĞĂƌĐŚEĞĞĚƐƚŽ ƐƐƵƌĞĂ^ĞĐƵƌĞŶĞƌŐLJ&ƵƚƵƌĞǁŽƌŬƐŚŽƉ͕ƚŚĞĨŽůůŽǁŝŶŐƚĞŶ͞ĂƐŝĐZĞƐĞĂƌĐŚEĞĞĚƐ͟ǁŽƌŬƐŚŽƉƐ͕ƚŚĞƉĂŶĞůŽŶ 'ƌĂŶĚŚĂůůĞŶŐĞƐĐŝĞŶĐĞ͕ĂŶĚƚŚĞƐƵŵŵĂƌLJƌĞƉŽƌƚEĞǁ^ĐŝĞŶĐĞĨŽƌĂ^ĞĐƵƌĞĂŶĚ^ƵƐƚĂŝŶĂďůĞŶĞƌŐLJ&ƵƚƵƌĞ ĚĞƚĂŝůƚŚĞŬĞLJďĂƐŝĐƌĞƐĞĂƌĐŚŶĞĞĚĞĚƚŽĐƌĞĂƚĞƐƵƐƚĂŝŶĂďůĞ͕ůŽǁĐĂƌďŽŶĞŶĞƌŐLJƚĞĐŚŶŽůŽŐŝĞƐŽĨƚŚĞĨƵƚƵƌĞ͘dŚĞƐĞ ƌĞƉŽƌƚƐŚĂǀĞďĞĐŽŵĞƐƚĂŶĚĂƌĚƌĞĨĞƌĞŶĐĞƐŝŶƚŚĞƐĐŝĞŶƟĮĐĐŽŵŵƵŶŝƚLJĂŶĚŚĂǀĞŚĞůƉĞĚƐŚĂƉĞƚŚĞƐƚƌĂƚĞŐŝĐ ĚŝƌĞĐƟŽŶƐŽĨƚŚĞ^ͲĨƵŶĚĞĚƉƌŽŐƌĂŵƐ͘;ŚƩƉ͗ͬͬǁǁǁ͘ƐĐ͘ĚŽĞ͘ŐŽǀͬďĞƐͬƌĞƉŽƌƚƐͬůŝƐƚ͘ŚƚŵůͿ ϭ ^ĐŝĞŶĐĞĨŽƌŶĞƌŐLJdĞĐŚŶŽůŽŐLJ͗^ƚƌĞŶŐƚŚĞŶŝŶŐƚŚĞ>ŝŶŬďĞƚǁĞĞŶĂƐŝĐZĞƐĞĂƌĐŚĂŶĚ/ŶĚƵƐƚƌLJ Ϯ EĞǁ^ĐŝĞŶĐĞĨŽƌĂ^ĞĐƵƌĞĂŶĚ^ƵƐƚĂŝŶĂďůĞŶĞƌŐLJ&ƵƚƵƌĞ ϯ ŝƌĞĐƟŶŐDĂƩĞƌĂŶĚŶĞƌŐLJ͗&ŝǀĞŚĂůůĞŶŐĞƐĨŽƌ^ĐŝĞŶĐĞĂŶĚƚŚĞ/ŵĂŐŝŶĂƟŽŶ ϰ ĂƐŝĐZĞƐĞĂƌĐŚEĞĞĚƐĨŽƌDĂƚĞƌŝĂůƐƵŶĚĞƌdžƚƌĞŵĞŶǀŝƌŽŶŵĞŶƚƐ ϱ ĂƐŝĐZĞƐĞĂƌĐŚEĞĞĚƐ͗ĂƚĂůLJƐŝƐĨŽƌŶĞƌŐLJ -

ANNUAL INFORMATION FORM for the YEAR ENDED DECEMBER 31, 2015 February 19, 2016

ENBRIDGE INC. ANNUAL INFORMATION FORM FOR THE YEAR ENDED DECEMBER 31, 2015 February 19, 2016 Enbridge Inc. 2015 Annual Information Form TABLE OF CONTENTS DOCUMENTS INCORPORATED BY REFERENCE As of the date hereof, portions of the MD&A and the audited consolidated financial statements of Enbridge as at and for the year ended December 31, 2015, as filed with the securities commissions or similar authorities in each of the provinces of Canada, as detailed below, are specifically incorporated by reference into and form an integral part of this AIF. These documents are available on SEDAR which can be accessed at www.sedar.com. Page Reference From Annual Financial AIF Statements MD&A GLOSSARY ................................................................................................... 1 PRESENTATION OF INFORMATION ........................................................... 4 12 FORWARD-LOOKING INFORMATION .........................................................5 CORPORATE STRUCTURE ......................................................................... 6 GENERAL DESCRIPTION OF THE BUSINESS ............................................ 7 1-2, 14-19 GENERAL DEVELOPMENT OF THE BUSINESS ....................................... 10 2-4, 8-9, 16-21, 23-39, 59-60, 67-69, 73-74 LIQUIDS PIPELINES ................................................................................... 16 1, 40-52 GAS DISTRIBUTION ................................................................................... 17 1, 52-55 GAS PIPELINES, PROCESSING AND ENERGY SERVICES -

Use of Environmental Management Systems and Renewable Energy Sources in Selected Food Processing Enterprises in Poland

energies Article Use of Environmental Management Systems and Renewable Energy Sources in Selected Food Processing Enterprises in Poland Stanisław Bielski 1 , Anna Zieli ´nska-Chmielewska 2 and Renata Marks-Bielska 3,* 1 Faculty of Agriculture and Forestry, University of Warmia and Mazury in Olsztyn, M. Oczapowskiego 8, 10-719 Olsztyn, Poland; [email protected] 2 Institute of Economics, Pozna´nUniversity of Economics and Business, Al. Niepodległo´sci10, 61-875 Pozna´n,Poland; [email protected] 3 Faculty of Economic Sciences, University of Warmia and Mazury in Olsztyn, M. Oczapowskiego 4, 10-719 Olsztyn, Poland * Correspondence: [email protected] Abstract: The issue of environmental management systems in food processing companies is gaining importance due to the need to reduce water withdrawal, wastewater, air emissions, and waste generation. New technological solutions and innovations can reduce the negative effects of the enterprises’ production facilities on the environment. In Poland, the phenomenon of increasing use of the amount of renewable energy sources is influenced by, e.g., adopted national and EU legislation, development of new technologies in the field of energy, and increasing awareness of producers and consumers in the field of ecology and environmental protection. It is also important that the state creates favorable conditions for the use of renewable energy in micro-installations. Citation: Bielski, S.; The application goal of the study is to develop a procedure for improvement of the environmental Zieli´nska-Chmielewska,A.; management systems for food processing companies and increase the awareness of potential use and Marks-Bielska, R. Use of implementation of renewable energy sources by food processing entities. -

Exploring Regional Opportunities in the U.S. for Clean Energy Technology Innovation Volume 1

About the Cover The images on the cover represent regional capabilities and resources of energy technology innovation across the United States from nuclear energy to solar and photovoltaics, and smart grid electricity to clean coal and carbon capture. Disclaimer This volume is one of two volumes and was written by the Department of Energy. This volume summarizes the results of university-hosted regional forums on regional clean energy technology innovation. The report draws on the proceedings and reports produced by the universities noted in Volume 2 for some of its content; as a result, the views expressed do not necessarily represent the views of the Department or the Administration. Neither the United States government nor any agency thereof, nor any of their employees, makes any warranty, express or implied, or assumes any legal liability or responsibility for the accuracy, completeness, or usefulness of any information, apparatus, product, or process disclosed, or represents that its use would not infringe privately owned rights. Reference herein to any specific commercial product, process, or service by trade name, trademark, manufacturer, or otherwise does not necessarily constitute or imply its endorsement, recommendation, or favoring by the United States government or any agency thereof. Message from the Secretary of Energy The U.S. Department of Energy (Department or DOE) is pleased to present this report, Exploring Regional Opportunities in the U.S. for Clean Energy Technology Innovation. The report represents DOE’s summary of the insights gained through fourteen university-hosted workshop events held nationwide during the spring and summer of 2016. These events brought together members of Congress, governors, other federal, state, tribal, and local officials, academic leaders, private sector energy leaders, DOE officials, and other stakeholders from economic development organizations and nongovernmental organizations to examine clean energy technology innovation from a regional perspective. -

Top News Before the Bell Stocks To

TOP NEWS • A hunt for any storage space turns urgent as oil glut grows With oil depots that normally store crude oil onshore filling to the brim and supertankers mostly taken, energy companies are desperate for more space. The alternative is to pay buyers to take their U.S. crude after futures plummeted to a negative $37 a barrel on Monday. • Corporate America seeks legal protection for when coronavirus lockdowns lift Major U.S. business lobbying groups are asking Congress to pass measures that would protect companies large and small from coronavirus-related lawsuits when states start to lift pandemic restrictions and businesses begin to reopen. • Teck Resources profit falls short as lockdowns, energy unit bite Teck Resources reported a much bigger-than-expected 84% plunge in quarterly profit, hit by shutdowns due to the coronavirus outbreak and weak performance in its energy unit. • U.S. energy industry steps up lobbying for Fed's emergency aid -letters The U.S. energy industry has asked the Federal Reserve to change the terms of a $600 billion lending facility so that oil and gas companies can use the funds to repay their ballooning debts, according to a letter seen by Reuters. • Coca-Cola sees 2nd quarter sales hit from coronavirus lockdown Coca-Cola forecast a significant hit to current-quarter results as restaurants, theaters and other venues that represent about half of the company's revenue remain closed because of the coronavirus pandemic. BEFORE THE BELL Canada's main stock index futures slid as U.S. oil futures continued to trade in the negative after their first ever sub-zero dive on Monday, furthering concerns of a global recession in the coming months. -

Sustainable Energy for Food Challenges and Solutions for Sustainable Energy Use in the Agriculture and Food Industry

Sustainable Energy for Food Challenges and Solutions for Sustainable Energy Use in the Agriculture and Food Industry Preface According to conservative estimates, producing food and getting it to the table accounts for around 30% of energy Be part of the solution! consumed worldwide, most of which is provided by fossil fuels. In places where renewable energies such as biomass Contribute to the global knowledge network for energy and already drive agricultural value chains, particularly in the food. Subscribe to the PoweringAg Newsletter at developing world, they often originate from traditional → www.PoweringAg.org sources – fuelwood, for example, which in most cases is or register at harvested in unsustainable ways. With world population on a path of unbridled expansion and energy resources in → https://energypedia.info/wiki/Portal: dwindling supply, experts in science, business, civil society Powering_Agriculture and development cooperation who are active in the energy More than 4,000 users have already signed up! and food sectors all face the same problem: how do we produce more food using as little energy as possible, while increasing the share of renewable energy? The GIZ-DIE symposium ʻSustainable Energy for Food’, held on 12 June 2014 in Bonn, Germany, placed itself at just this juncture. forces with the United States Agency for International With a line-up of 16 speakers drawn from development Development (USAID) the Swedish International Develop- cooperation and research in energy and agriculture, the ment Cooperation Agency (SIDA), OPIC and Duke Energy symposium sought to provide a comprehensive overview to found to found the global initiative ʻPowering Agricul- of where the various stakeholders stand on the issue. -

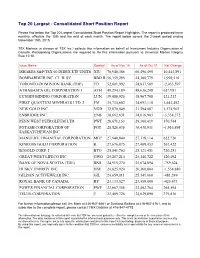

Top 20 Largest - Consolidated Short Position Report

Top 20 Largest - Consolidated Short Position Report Please find below the Top 20 Largest Consolidated Short Position Report Highlights. The report is produced twice monthly, effective the 15th and the end of each month. The report below covers the 2-week period ending November 15th, 2015. TSX Markets (a division of TSX Inc.) collects this information on behalf of Investment Industry Organization of Canada. Participating Organizations are required to file this information pursuant to Universal Market Integrity Rule 10.10. Issue Name Symbol As of Nov 15 As of Oct 31 Net Change ISHARES S&P/TSX 60 INDEX ETF UNITS XIU 70,940,386 60,496,495 10,443,891 BOMBARDIER INC. CL 'B' SV BBD.B 56,359,295 54,360,779 1,998,516 TORONTO-DOMINION BANK (THE) TD 52,801,992 54,837,589 -2,035,597 ATHABASCA OIL CORPORATION J ATH 49,294,189 48,636,208 657,981 LUNDIN MINING CORPORATION LUN 39,088,920 38,967,708 121,212 FIRST QUANTUM MINERALS LTD. J FM 35,734,602 34,091,110 1,643,492 NEW GOLD INC. NGD 32,870,049 31,294,087 1,575,962 ENBRIDGE INC. ENB 30,662,631 34,016,903 -3,354,272 PENN WEST PETROLEUM LTD. PWT 28,671,163 28,300,419 370,744 POTASH CORPORATION OF POT 28,520,036 30,436,931 -1,916,895 SASKATCHEWAN INC. MANULIFE FINANCIAL CORPORATION MFC 27,940,840 27,318,114 622,726 KINROSS GOLD CORPORATION K 27,676,875 27,409,453 267,422 B2GOLD CORP. -

Enbridge 2012 Corporate Social Responsibility Report Social

ENBRIDGE 2012 CORPORATE SOCIAL RESPONSIBILITY REPORT SOCIAL PERFORMANCE ENBRIDGE 2012 CORPORATE SOCIAL RESPONSIBILITY REPORT TABLE OF CONTENTS ABOUT ENBRIDGE .............................................................. 1 LA6 Percentage of total workforce represented in formal joint management-worker health and safety committees that help ABOUT THE ENBRIDGE 2012 CORPORATE SOCIAL monitor and advise on occupational health and safety RESPONSIBILITY REPORT ................................................. 2 programs. ............................................................................... 43 FORWARD-LOOKING INFORMATION ................................ 3 LA7 Rates of injury, occupational diseases, lost days and absenteeism, and number of work-related fatalities by region AWARDS AND RECOGNITION ............................................ 4 and by gender. ....................................................................... 44 STRATEGY AND PROFILE ................................................. 5 LA8 Education, training, counseling, prevention and risk- control programs in place to assist workforce members, their ORGANIZATIONAL PROFILE ............................................ 5 families or community members regarding serious diseases. REPORT PARAMETERS .................................................. 6 ................................................................................................ 44 GOVERNANCE, COMMITMENTS AND ENGAGEMENT ... 12 LA9 Health and safety topics covered in formal agreements with trade unions. ..................................................................