Investigation on Design Support of Automobile Industry System in South Africa

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2002 Ford Motor Company Annual Report

2228.FordAnnualCovers 4/26/03 2:31 PM Page 1 Ford Motor Company Ford 2002 ANNUAL REPORT STARTING OUR SECOND CENTURY STARTING “I will build a motorcar for the great multitude.” Henry Ford 2002 Annual Report STARTING OUR SECOND CENTURY www.ford.com Ford Motor Company G One American Road G Dearborn, Michigan 48126 2228.FordAnnualCovers 4/26/03 2:31 PM Page 2 Information for Shareholders n the 20th century, no company had a greater impact on the lives of everyday people than Shareholder Services I Ford. Ford Motor Company put the world on wheels with such great products as the Model T, Ford Shareholder Services Group Telephone: and brought freedom and prosperity to millions with innovations that included the moving EquiServe Trust Company, N.A. Within the U.S. and Canada: (800) 279-1237 P.O. Box 43087 Outside the U.S. and Canada: (781) 575-2692 assembly line and the “$5 day.” In this, our centennial year, we honor our past, but embrace Providence, Rhode Island 02940-3087 E-mail: [email protected] EquiServe Trust Company N.A. offers the DirectSERVICE™ Investment and Stock Purchase Program. This shareholder- paid program provides a low-cost alternative to traditional retail brokerage methods of purchasing, holding and selling Ford Common Stock. Company Information The URL to our online Investor Center is www.shareholder.ford.com. Alternatively, individual investors may contact: Ford Motor Company Telephone: Shareholder Relations Within the U.S. and Canada: (800) 555-5259 One American Road Outside the U.S. and Canada: (313) 845-8540 Dearborn, Michigan 48126-2798 Facsimile: (313) 845-6073 E-mail: [email protected] Security analysts and institutional investors may contact: Ford Motor Company Telephone: (313) 323-8221 or (313) 390-4563 Investor Relations Facsimile: (313) 845-6073 One American Road Dearborn, Michigan 48126-2798 E-mail: [email protected] To view the Ford Motor Company Fund and the Ford Corporate Citizenship annual reports, go to www.ford.com. -

Second Amended Complaint for Patent Infringement

Case 3:17-cv-03201-N Document 79 Filed 11/17/16 Page 1 of 44 PageID 3978 UNITED STATES DISTRICT COURT EASTERN DISTRICT OF MICHIGAN FORD GLOBAL TECHNOLOGIES, LLC, Case No. 2:15-CV-10394-LJM-SDD Plaintiff, HON. LAURIE J. MICHELSON v. NEW WORLD INTERNATIONAL JURY TRIAL DEMANDED INC., AUTO LIGHTHOUSE PLUS, LLC, and UNITED COMMERCE CENTERS, INC. Defendants. SECOND AMENDED COMPLAINT FOR PATENT INFRINGEMENT Case 3:17-cv-03201-N Document 79 Filed 11/17/16 Page 2 of 44 PageID 3979 Plaintiff Ford Global Technologies, LLC (“FGTL”) by and through their undersigned counsel, as and for its Complaint against defendants United Commerce Centers, Inc., New World International Inc., and Auto Lighthouse Plus, LLC (collectively, “Defendants”) alleges as follows: I. THE PARTIES 1. Ford Global Technologies LLC (hereinafter “FGTL”) is a limited liability company organized and existing under the laws of the State of Michigan, having a principal place of business at 330 Townsend Drive, Suite 800 South, Dearborn, MI 48126. 2. On information and belief, Defendant United Commerce Centers, Inc. (hereinafter “UCC”) is a Texas Corporation, with a principal place of business at 1720 E. State Highway 356, Irving, TX 75060. 3. On information and belief, UCC is doing business as New World International. 4. On information and belief, Peter Tsai is registered agent, president and treasurer of UCC and Grace Tsai is Director, Vice President and Secretary of UCC. 1 Case 3:17-cv-03201-N Document 79 Filed 11/17/16 Page 3 of 44 PageID 3980 5. On information and belief, Defendant New World International Inc. -

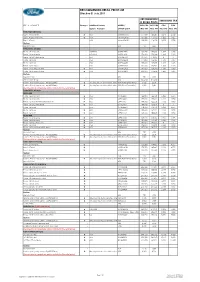

New Vehicle Price List 1 July.Xls Date Revised: 2011/06/29 RECOMMENDED RETAIL PRICE LIST Effective 01 July 2011

RECOMMENDED RETAIL PRICE LIST Effective 01 July 2011 RECOMMENDE EMISSIONS TAX D RETAIL PRICE KEY: @ = CHANGE Changes Additional Factory MODEL / INCL CO2 INCL CO2 CO2 CO2 Options Available OPTION CODE INCL VAT EXCL VAT INCL VAT EXCL VAT FORD FIGO (MY2010) Figo 1.4 Ambiente @ A54 MAMAB4101 117,490 103,061 3,078 2,700 Figo 1.4 TDCi Ambiente @ A54 MAMAC4101 131,300 115,175 1,625 1,425 Figo 1.4 Trend - A54 MAMAD4101 130,080 114,105 3,078 2,700 Options Metallic Paint - A54 710 623 FORD FIESTA MY2008 Fiesta 1.4 Ambiente - A54+R43 CVFNL4403 163,740 143,632 1,539 1,350 Fiesta 1.6 Ambiente - A54+R43 CVFUL4403 174,420 153,000 1,625 1,425 Fiesta 1.6 TDCi Ambiente - A54 CVFRM4403 197,570 173,307 0 0 Fiesta 1.4 Trend - A54 CVFNM4403 177,880 156,035 1,539 1,350 Fiesta 1.6 Trend - A54 CVFUM4403 188,600 165,439 1,625 1,425 Fiesta 1.6 Titanium - A54 CVFUH4403 201,600 176,842 1,625 1,425 Fiesta 1.4 Titanium 3 door @ A54 CVFNH2403 191,600 168,070 1,539 1,350 Fiesta 1.6 Titanium 3 door @ A54 CVFUH2403 200,020 175,456 1,625 1,425 Options Metallic Paint - A54 750 658 Local Radio & CD - R43 (16,240) (14,246) Service Plan (compulsory - 4yr/60'000km) @ Already included in vehicle price S08 (Petrol Derivatives) 3,026 2,654 Service Plan (compulsory - 4yr/60'000km) @ Already included in vehicle price S08 (Diesel Derivative) 3,969 3,482 (Service plan is compulsory and is included in the retail price) FORD FIESTA MY2010 FIESTA 5DR Fiesta 1.4 Ambiente @ A54 CTFNL4401 164,990 144,728 2,822 2,475 Fiesta 1.6 Ambiente @ A54 CTFUL4401 177,180 155,421 2,223 1,950 Fiesta 1.6 -

Ford Motor Company One American Road Dearborn, MI 48126 U.S.A

Report Home | Contact | GRI Index | Site Map | Glossary & Key Terms This report is structured according to our Business Principles, which you can access using the colored tabs above. This report is aligned with the Global Reporting Initiative (GRI) G3 Sustainability Reporting Guidelines released in October 2006, at an application level of A+. See the GRI Index ● Print this report "Welcome to our 2006/7 Sustainability Report. These are challenging times, not only for our Company but for our planet and its inhabitants. The markets for our products are changing rapidly, and there is fierce competition everywhere we operate. Collectively, we face daunting global sustainability ● Download resources challenges, including climate change, depletion of natural resources, poverty, population growth, urbanization and congestion." ● Send feedback Alan Mulally, President and CEO Read the full letter from Bill Ford, Executive Chairman Alan Mulally and Bill Ford Fast track to data: ● Products and Customers ● Vehicle Safety ● Environment ● Quality of Relationships ● Community ● Financial Health ● Workplace Safety Overview Our industry, the business environment and societal expectations continue to evolve, and so does our reporting. Learn about our Company and our vision for sustainability. Our Impacts As a major multinational enterprise, our activities have far-reaching impacts on environmental, social and economic systems. Read about our analysis and prioritization of these issues and impacts. Voices Nine people from inside and outside Ford provide their perspectives on key challenges facing our industry and how Ford is responding, including “new mobility,” good practices in the supply chain and the auto industry’s economic impact. This report was published in June 2007. -

Download Catalog

*We import and supply top of the range auto accessories for the Southern African market to ensure that all the vehicles keep up to trendy and latest auto accessories* STYLEQUIP PTY LTD Add:Unit 13, Eastborough Business Park, 15-21 Olympia Street, Eastgate, Sandton Tel:011-2620127 Add:Shop 15, Kong’s Court Shopping Center,Walmer Heights Port Elizbeth Tel:041-3671045 Add:Shop 32 China Town Shoprite Park Parow Tel:021-9113964 2021 Add:Shop 15A China Town Ottery STYLEQUIP PTY LTD Tel:021-7040215 Auto accessories and 4*4 accessories Add:Shop C3 Promenade Mall Mitchells Plain Tel:021-3760214 Web: graystoneautoparts.co.za ◎ FORD RANGER 2012-2015 1-3 STYLE-QUIP ◎ FORD RANGER T7 3 ◎ TOYOTA HILUX 4-5 CONTENTS ◎ ISUZU D-MAX 6 ◎ FORTUNER&MAZDA BT-50 7 ◎ 4X4 NUDGE BAR 8 ◎ LED LIGHT 24-25 ◎ FRONT SPOILER 9-10 ◎ AIR INTAKE 25-26 ◎ DIFFUSER 10-11 ◎ SILICON PIPE 26-27 ◎ SIDE SKIRT 11 ◎ WHEEL COVER 27-28 ◎ ROOF SPOILER 12 ◎ MAG WHEEL 28 ◎ GRILL BODY KIT 13 ◎ LIGHTING 29 ◎ WINDSHIELDS 14-17 ◎ HEAD LIGHTS 30-31 ◎ BONNET GUARDS 18-19 ◎ TAIL LIGHTS 31-32 ◎ MUD FLAPS 20-21 ◎ CONNER LAMPS AND BUMPER LAMPS 32 ◎ FOG LIGHT 21-23 ◎ LOWERING SPRINGS 32 ◎ SHOCK ABSORBER 33 ◎ FLAMINGO 34-35 ◎ CAR MATS 36 ◎ SEAT COVER 36 ◎ ACCESSORIES 37-38 ◎ REVO CHANGE TO ROCCO TRD BODY KITS 39 ◎ FOR 2015+ RANGER 40 FORD RANGER 2012-2015 FORD RANGER 2012-2015 1234567894506 1234567890256 1234567899943 FORD RANGER 2016 BONNET SCOOP FORD RANGER 2016 BONNET SCOOP FORD RANGER 2012-2016 WIND SHIELDS 6922266441240 1234567896789 1234567892345 2112345678856 FORD RANGER 12-15 NUDGE BAR CHROME -

Disbursements Private Cars and MPV's

Disbursements This Schedule has been obtained using information available as follows: 1. Vehicles: The cost of vehicles has been obtained from the lists of vehicle prices in the November issue of CAR magazine and the running costs have been obtained from the AA tables assuming an annual total kolometres of 25 000. 2. Other: Costs have been obtained from prices quoted by third party suppliers and service providers. Private Cars and MPV's Cost ex Car Magazine - November 2005 AA Tables - Fixed Costs Car Type Engine capacity 1.4 Litre 1.6 Litre 2.0 Litre 2.5 Litre VW Citi Golf Chico R 66,270.00 Opel Corsa Lite R 68,600.00 Toyota TazzZ R 73,242.00 Ford Fiesta R 99,850.00 Ford Ikon R 105,915.00 Opel Corsa Classic R 114,800.00 VW Polo R 121,510.00 Toyota Corolla R 152,775.00 Ford Focus R 184,900.00 VW Golf R 188,370.00 Mazda 6 R 199,990.00 BMW 118i R 203,000.00 Volvo S60 R 303,000.00 BMW 325i R 290,500.00 Alfa 156 R 266,000.00 Ford Mondeo (2.9) R 286,035.00 Total Cost R 307,962.00 R 495,000.00 R 776,260.00 R 1,145,535.00 Average Cost R 76,990.50 R 123,750.00 R 194,065.00 R 286,383.75 Kilometres per Year 25,000.00 25,000.00 25,000.00 25,000.00 Cost per KM in Cents 105.00 127.00 198.00 288.00 AA Tables - Running Costs Service & Repairs 14.96 16.74 20.10 22.43 Tyres 10.25 13.71 17.12 20.17 Fuel (R5,75 per litre) R 51.64 R 57.33 R 59.80 R 68.88 Factor (8.98) (9.97) (10.4) (11.98) Cost per Km in Cents R 181.85 R 214.78 R 295.02 R 399.48 Total Cost per Km R 1.85 R 2.15 R 2.95 R 4.00 AA Tables - Fixed Costs Pick Up Vans & Bakkies Cost ex Car Magazine -

Annexure A-Fleet & Equipment List for Disposal

Annexure A-Fleet & equipment list for disposal Vehicle registration Year Item Airport Name Vehicle Vin number Asset Description No. number Model Bram Fischer MNTVCUD40Z0038173 International FCD 106 FS Nissan Navara 2,5TDCi double cab 4x2 MT 2012 1 Airport Bram Fischer MNTVCUD40Z0038186 International FCD 103 FS Nissan Navara 2,5TDCi double cab 4x2 MT 2012 2 Airport Bram Fischer MNTVCUD40Z0600166 International FFW 089 FS Nissan Navara 2,5TDCi double cab 4x2 MT 2012 3 Airport Bram Fischer MNTVCUD40Z0047896 International FFW 088 FS Nissan Navara 2,5TDCi double cab 4x2 MT 2012 4 Airport Bram Fischer AHTLB58EX03033805 International FCB 388 FS Toyota Corolla 1,6 Professional MT 2009 5 Airport Bram Fischer KMHWH81RLDU529755 International FHC 771 FS Hyundai H1, 2.4 GLS 9 seater Bus 2013 6 Airport Bram Fischer MNTVCUD40Z0608470 International FMC101FS Nissan Navara 2,5TDCi double cab 4x2 MT 2014 7 Airport Bram Fischer International unknown unknown Runway Closure Trailer 2015 8 Airport Bram Fischer International unknown unknown Runway Closure Trailer 2015 9 Airport Bram Fischer International unknown unknown Runway Closure Trailer 2015 10 Airport Annexure A-Fleet & equipment list for disposal Bram Fischer International unknown unknown Yamaha All Terrain Vehicle 2014 11 Airport Bram Fischer International unknown unknown Yamaha All Terrain Vehicle 2014 12 Airport Cape Town AHTFR22G806056435 International CA 429132 TOYOTA HI-LUX 2.5D-4D - Manual 2012 13 Airport Cape Town MHKM1BA1NBK000672 International CY 290188 TOYOTA AVANZA 1.3 SX - Manual 2012 14 Airport -

Starter Bosch

STARTER BOSCH www.auto-marco.com Experience Service Trust O.E.M names and numbers are used for reference purposes only. www.auto-marco.com BOSCH 106 SBO417 SBO418 SBO222 Replace1: 0001106001 0001114005 Replace1: 0001106011 Replace1: 0001106014 Replace2: 055911023E Replace2: 09117037 90535261 Replace2: 0051513801 References: CS294 30561 References: CS519 31222 References: CS1241 Applications: Volkswagen Caddy Applications: Opel Agila Applications: Smart Cabrio Descriptions: 0.8KW 12V 9T Descriptions: 0.9KW 12V 9T Descriptions: 1.1KW 12V 9T SBO332 SBO419 SBO015 Replace1: 0001106016 Replace1: 0001106019 Replace1: 0001106023 Replace2: NAD101260 Replace2: 12411489994 Replace2: 8200069377 8200186148 References: CS610 31207 References: CS1254 17855 References: CS1255 32545 Applications: Rover 25 VW passat Applications: Mini Cooper Applications: Renault Espace Descriptions: 1.1KW 12V 9T Descriptions: 1.1KW 12V 9T Descriptions: 0.9KW 12V 9T SBO420 Replace1: 0001106405 Replace2: 5802AR V7540897 References: CS1417 19000 Applications: Mini Cooper Descriptions: 0.9KW 12V 10T www.auto-marco.com 02 BOSCH 107 SBO421 SBO018 SBO313 Replace1: 0001107005 0001107006 Replace1: 0001107009 Replace1: 0001107011 Replace2: 02B911023B Replace2: 605629740 60562974 Replace2: 2330099B00 References: CS597 33033 References: CS687 References: JS1081 Applications: Volkswagen Caravelle Applications: Alfa Romeo 145 Applications: Nissan Micra Descriptions: 1.1KW 12V 10T Descriptions: 1.1KW 12V 9T Descriptions: 1.1KW 12V 8T SBO422 SBO423 SBO424 Replace1: 0001107012 0001107013 -

Download Guide Here

18 SMF = Sealed Maintenance Free · AGM = Absorbed Glass Mat · SSM = Start Stop Motion SMF = Sealed Maintenance Free · AGM = Absorbed Glass Mat · SSM = Start Stop Motion 19 Replacement Battery Selection Guide Replacement Battery Selection Guide Passenger Cars and SUV’s Passenger Cars and SUV’s Recommended Recommended Year Make and Model Replacement Alternative Technology Year Make and Model Replacement Alternative Technology ABARTH ASTON MARTIN 2014> Abarth 500 All 621 SMF 2007> Aston Martin DB9 Coupé 2007> Aston Martin DB9 Volante ALFA ROMEO 2007> Aston Martin Vanquish S 2007> Aston Martin Vantage 1978-83 Alfetta Sedan, Exec, GTtV2000,Giulietta 621 639 SMF 2007> Aston Martin Vantage Sportshift 1981-83 2.0 GTV Sprint and Export Models 621 639 SMF 2007> Aston Martin Vantage Roadster 1981-83 Alfetta Automatic 622 638 SMF 2007> Aston Martin Vantage Roadster S’shift 1981-87 2.5 GTV 6, Alfa 6 and 3, OL and GTV 6 647 646 SMF 2010> Aston Martin All Models 658 AGM 1982-85 Alfa GTV 6 638 SMF 1983-85 Alfa 33 639 621 SMF AUDI 1983-85 Alfetta 1591, Sprint MK3 621 639 SMF 1983-85 Alfa 33 Ti with A/C, Giulietta Gold and Silver 646 652 SMF 1981-94 All Audi Models 100, 200, 500, 500E, 500SE 647 661 SMF 1993> 33 and 155, 164TS Super, 3 OL V6 and 164 Quad 647 SMF 1995-99 All Models A4, A6, A8, Quattro’s, Coupe’s and Cabrio’s 652 661 SMF 1993> GTV, Spider 652 651 SMF 1997- A3 1.8 and 1.8 Turbo, S3 646 658 SMF 1995> Quad 145. -

Passenger & Lcv Applications Catalogue

2014 ISSUE 12 Passenger & LCV Applications Catalogue PASSENGER CATALOGUE A VALEO EXEDY VPH ALFA ROMEO YEAR VALEO EXEDY VPH DIMENSIONS FLYWHEEL PROFILE 147 147 2.0 TWIN SPARK 16V (AR32310) (2 in 1 kit) 00-04 AR04 230 X 23.1 - 20 0.5mm step 147 2.0 TWIN SPARK 16V (AR32310) (2 in 1 kit) 04- AR04 230 X 23.1 - 20 0.5mm step 156 156 2.0 16V SELESPEED 16V (AR937A1) (2 in 1 kit) 03- AR04 230 X 23.1 - 20 0.5mm step GTV 156 2.0 16V SELESPEED 16V (AR937A1) (2 in 1 kit) 03- AR04 230 X 23.1 - 20 0.5mm step SPIDER GTV 2.0i TWIN SPARK (AR32310) (2 in 1 kit) 96-99 AR04 230 X 23.1 - 20 0.5mm step AMC YEAR VALEO EXEDY VPH DIMENSIONS FLYWHEEL PROFILE AMC BUS (14B) 93- TY41 275 X 28.9 - 21 flat ASIA YEAR VALEO EXEDY VPH DIMENSIONS FLYWHEEL PROFILE ROCSTA 1.8 (JF8) 96- AS01 225 X 24.5 - 22 20.0mm recess ROCSTA 2.2 DIESEL (R2) 96- AS01 225 X 24.5 - 22 20.0mm recess ASIA COMMERCIAL YEAR VALEO EXEDY VPH DIMENSIONS FLYWHEEL PROFILE ASIA MINIBUS 4L (ZB) 96- AS02 280 X 29.0 - 10 flat ASIAWING YEAR VALEO EXEDY VPH DIMENSIONS FLYWHEEL PROFILE ASIA MINIBUS 4L (ZB) 96- AS02 280 X 29.0 - 10 flat AUDI YEAR VALEO EXEDY VPH DIMENSIONS FLYWHEEL PROFILE 80 GL 1.5 (2F) 1.6 GLS (YP) 75-81 VW02 190 X 20.6 - 24 flat 100 LS 1.6 100 LS 100-4 1.6 (YV) 77-84 VW02 190 X 20.6 - 24 flat 100 LS 1.6 100-4 1.6 (YV) 77-84 VW12 210 X 20.6 - 24 flat 100 5S 1.9 5 Cyl & GL 2.0 4 Cylinder (WB) 82-84 VW09 215 X 20.6 - 24 flat 100 GLS DIESEL 200 GLX 5E 100 GLS 500 80-88 VW11 228 X 20.6 - 24 24.5mm recess 200 GLX 5E 2.1 5 Cylinder (WC) 78-83 VW11 228 X 20.6 - 24 24.5mm recess 400 1781cc (JW) 87-91 -

Swaziland Government Gazette

RECEIVED I 2001 -11- 02 ^RKSMANS LIBRARY Swaziland Government Gazette VOL. XLIV] MBABANE, Friday, OCTOBER 13th 2006 No. 121 CONTENTS No. Page ADVERTISEMENTS 848 PUBLISHED BY AUTHORITY S.G.G.NO. 121 FRIDAY, OCTOBER 13, 2006, 848 NOTICE Notice is hereby given that I, Juliana Thoko Dlamini of Lobamba Hhohho Region intend to apply to the Honourable Minister of Justice of the Kingdom of Swaziland for authorisation to assume the surname Shoisa after the fourth publication of this notice in each of four consecutive weeks in the Times of Swaziland and The Swazi Observer being the newspapers circulating in the region where I reside and designated for this purpose by the Regional Secretary for the Hhohho Region and in the government Gazette. The reason I want to assume the surname Shoisa is because it is my natural surname. Any person or persons likely to object to my assuming the surname Shoisa should lodge their objections in writing with me at the address given below and with the Regional Secretary for Hhohho Region. Royal Swaziland Police P.O. Box 29 Manzini Hl 767 4x13-10-2006 NOTICE Notice is hereby given that I, Sipho Simon Sibandze of Mlambo Shiselweni Region intend to apply to the Honourable Minister of Justice of the Kingdom of Swaziland for authorisation to assume the surname Banda after the fourth publication of this notice in each of four consecutive weeks in the Times of Swaziland and The Swazi Observer being the newspapers circulating in the region where I reside and designated for this purpose by the Regional Secretary for the Shiselweni Region and in the government Gazette. -

Ford Festiva 88-93

FORD FESTIVA 88-93 FD04022BA FD04029BA C. Certified Parts *. ADD Products C * ITEM NO. DESCRIPTION YEAR PART NO PARTS LINK MEASURE FD04022BA FRT BUMPER MAT-COLOR DARK GRAY 88-94 E8BZ-17D957A FO1000428 1pc / 3.50 (E9BZ-17D957A) FD04022BB FRT BUMPER MAT-COLOR W/STRAP DARK GRAY 88-94 F0BZ-17D957B FO1000187 1pc / 3.50 (E8BZ-17D957B) FD04029BA RR BUMPER MAT-COLOR DARK GRAY 88-94 FOBZ-17K835A FO1100126 1pc / 3.50 FD04029BB RR BUMPER MAT-COLOR W/STRAP DARK GRAY 88-94 E8BZ-17K835A FO1100126 1pc / 4.30 FD04059BA RR BUMPER MAT-COLOR DARK GRAY 94-00 KK12BE50220 1pc / 4.00 CNO 110 - 1 FORD FESTIVA/ASPIRE 94-97 KIA PRIDE FD04068BA FD04075BA FD07109GA FD10074AL FD10074BL FD20060A KA07001GA KA10007AL C. Certified Parts *. ADD Products C * ITEM NO. DESCRIPTION YEAR PART NO PARTS LINK MEASURE FD04059BA RR BUMPER MAT-COLOR DARK GRAY 94-00 KK12BE50220 1pc / 4.00 FD04068BA FRT BUMPER MAT-COLOR BLACK 94-96 F4BZ-17D957A FO1000124 5pc / 21.52 FD04075BA RR BUMPER MAT-COLOR BLACK 94-97 F4BZ-17K835A FO1100253 1pc / 3.20 FD07109GA GRILLE MAT-COLOR BLACK 94-97 F4BZ-8200F FO1200331 5pc / 1.76 KA07001GA GRILLE MAT-COLOR BLACK 94-00 KK12B-50-710 5pc / 2.71 CFD10074AR FENDER RH . 94-97 F4BZ-16005A FO1241181 1pc / 2.50 CFD10074AL FENDER LH . 94-97 F4BZ-16006A FO1240181 1pc / 2.50 FD10074BR FENDER RH W/S.L.HOLE 95-97 MDX90-52-110A 1pc / 2.50 FD10074BL FENDER LH W/S.L.HOLE 95-97 MDX90-52-210A 1pc / 2.50 KA10007AR FENDER RH . 94-03 KK135-52-111 1pc / 1.20 KA10007AL FENDER LH .