Briefing Residential Sales July 2014

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

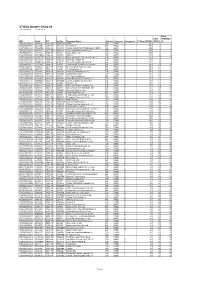

STOXX Greater China 80 Last Updated: 01.08.2017

STOXX Greater China 80 Last Updated: 01.08.2017 Rank Rank (PREVIOU ISIN Sedol RIC Int.Key Company Name Country Currency Component FF Mcap (BEUR) (FINAL) S) TW0002330008 6889106 2330.TW TW001Q TSMC TW TWD Y 113.9 1 1 HK0000069689 B4TX8S1 1299.HK HK1013 AIA GROUP HK HKD Y 80.6 2 2 CNE1000002H1 B0LMTQ3 0939.HK CN0010 CHINA CONSTRUCTION BANK CORP H CN HKD Y 60.5 3 3 TW0002317005 6438564 2317.TW TW002R Hon Hai Precision Industry Co TW TWD Y 51.5 4 4 HK0941009539 6073556 0941.HK 607355 China Mobile Ltd. CN HKD Y 50.8 5 5 CNE1000003G1 B1G1QD8 1398.HK CN0021 ICBC H CN HKD Y 41.3 6 6 CNE1000003X6 B01FLR7 2318.HK CN0076 PING AN INSUR GP CO. OF CN 'H' CN HKD Y 32.0 7 9 CNE1000001Z5 B154564 3988.HK CN0032 BANK OF CHINA 'H' CN HKD Y 31.8 8 7 KYG217651051 BW9P816 0001.HK 619027 CK HUTCHISON HOLDINGS HK HKD Y 31.1 9 8 HK0388045442 6267359 0388.HK 626735 Hong Kong Exchanges & Clearing HK HKD Y 28.0 10 10 HK0016000132 6859927 0016.HK 685992 Sun Hung Kai Properties Ltd. HK HKD Y 20.6 11 12 HK0002007356 6097017 0002.HK 619091 CLP Holdings Ltd. HK HKD Y 20.0 12 11 CNE1000002L3 6718976 2628.HK CN0043 China Life Insurance Co 'H' CN HKD Y 20.0 13 13 TW0003008009 6451668 3008.TW TW05PJ LARGAN Precision TW TWD Y 19.7 14 15 KYG2103F1019 BWX52N2 1113.HK HK50CI CK Property Holdings HK HKD Y 18.3 15 14 CNE1000002Q2 6291819 0386.HK CN0098 China Petroleum & Chemical 'H' CN HKD Y 16.4 16 16 HK0823032773 B0PB4M7 0823.HK B0PB4M Link Real Estate Investment Tr HK HKD Y 15.4 17 19 HK0883013259 B00G0S5 0883.HK 617994 CNOOC Ltd. -

Company News

August 31, 2017 COMPANY NEWS China Glass Holdings Limited [3300.HK; HK$0.70; Not Rated] Key takeaways from 1H 2017 results presentation and detailed discussion with management Market Cap: US$162m; Free Float: 41.1%; 3-months Average Daily Turnover: US$0.13m Analyst: Mark Po [China Glass Holding Limited] The Company. China Glass Holdings Limited (CGH) produces float glass in (HK$) (HK$ million) 1.5 10 China, and markets its glass under the SUBO brand name in China and internationally. 8 CGH held its 1H 2017 results presentation yesterday. Management discussed 1 the Company’s 1H 2017 results, the outlook for industry and the Company, and 6 its near-term expansion plan. We also had a detailed discussion with CGIH’s 4 new management regarding the Company’s relationship with CNBM Group, its 0.5 roadmap and strategy, and its overseas business development. We believe that 2 CGH is likely to be the platform for CNBM Group to develop glass operations in both China and overseas markets. 0 0 1H 2017 results highlights. CGH’s 1H 2017 net profit was RMB22.9m, which is Aug16 Oct16 Dec16 Feb17 Apr17 Jun17 Turnover (RHS) Price (LHS) a turnaround from a net loss of RMB93.9m in 1H 2016. Turnover increased by Key Financials 2013 2014 2015 2016 about 20% YoY, from RMB918m in 1H 2016 to RMB1,101m in 1H 2017. The (in RMB m) increase in turnover was attributable mainly to a 13% YoY increase in the average selling price (ASP), from RMB60.5/DWC in 1H 2016 to RMB68.6/DWC Revenue 2,760.4 2,489.4 1,968.9 2,139.7 Gross Profit 537.2 372.2 78.3 327.3 in 1H 2017. -

STOXX Changes Composition of Benchmark Indices Effective on June 21St, 2021

Zug, June 11th, 2021 STOXX Changes composition of Benchmark Indices effective on June 21st, 2021 Dear Sir and Madam, STOXX Ltd., the operator of Qontigo’s index business and a global provider of innovative and tradable index concepts, today announced the new composition of STOXX Benchmark Indices as part of the regular quarterly review effective on June 21st, 2021 Date Symbol Index name Internal Key ISIN Company name Changes 11.06.2021 BDXP STOXX Nordic Total Market SE10V2 SE0001174970 MILLICOM INTL.CELU. SDR Addition 11.06.2021 BDXP STOXX Nordic Total Market NO112F NO0010823131 KAHOOT! Addition 11.06.2021 BDXP STOXX Nordic Total Market SE10W3 SE0015483276 CINT GROUP Addition 11.06.2021 BDXP STOXX Nordic Total Market SE10X4 SE0015671995 HEMNET Addition 11.06.2021 BDXP STOXX Nordic Total Market DK3011 DK0060497295 MATAS Addition 11.06.2021 BDXP STOXX Nordic Total Market FI10JH FI4000480215 SITOWISE GROUP Addition 11.06.2021 BDXP STOXX Nordic Total Market FI10HF FI4000049812 VERKKOKAUPPA COM Addition 11.06.2021 BDXP STOXX Nordic Total Market FI10FD FI0009001127 ALANDSBANKEN B Addition 11.06.2021 BDXP STOXX Nordic Total Market FI6036 FI4000048418 AHLSTROM-MUNKSJO Addition 11.06.2021 BDXP STOXX Nordic Total Market FI10IG FI4000062195 TAALERI Addition 11.06.2021 BDXP STOXX Nordic Total Market FI10GE FI4000029905 SCANFIL Addition 11.06.2021 BDXP STOXX Nordic Total Market NO90I2 NO0010861115 NORSKE SKOG Addition 11.06.2021 BDXP STOXX Nordic Total Market NO111E NO0010029804 SPAREBANK 1 HELGELAND Addition 11.06.2021 BDXP STOXX Nordic Total Market NO113G NO0010886625 AKER BIOMARINE Addition 11.06.2021 BDXP STOXX Nordic Total Market NO114H NO0010936792 FROY Addition 11.06.2021 BDXP STOXX Nordic Total Market NO110D BMG9156K1018 2020 BULKERS Addition 11.06.2021 BDXP STOXX Nordic Total Market NO10R3 NO0010196140 NORWEGIAN AIR SHUTTLE Addition 11.06.2021 BDXP STOXX Nordic Total Market NO809S NO0010792625 FJORD1 Deletion 11.06.2021 BKXA STOXX Europe ex Eurozone Total Market SE10V2 SE0001174970 MILLICOM INTL.CELU. -

Fact Book 2012 2012 Fact Book III Contents

Fact Book 2012 2012 Fact Book III Contents Shanghai Securities Market.......................................................1 Historical Review .........................................................................................................................................1 Securities Products ......................................................................................................................................1 2011 Market Review ....................................................................5 Overview ....................................................................................................................................................5 Securities Issuance and Listing ......................................................................................................................5 Introduction of New Products ........................................................................................................................6 Pledge-style Bond Repo ...............................................................................................................................6 Securities Repo ...........................................................................................................................................6 Major Events in the Securities Market 2011 ....................................................................................................7 Market Highlights ........................................................................................................................................10 -

Stake in WCC Likely to Cement Leadership in Northwest China

June 19, 2015 COMPANY UPDATE Anhui Conch Cement (H) (0914.HK) Buy Equity Research Stake in WCC likely to cement leadership in Northwest China What's changed Investment Profile Anhui Conch Cement announced that its wholly-owned subsidiary Conch Low High International will acquire 16.7% of the enlarged equity of West China Growth Growth Returns * Returns * Cement (2233 HK, Not Covered) for a consideration of HK$1,527mn. The Multiple Multiple implied EV/t is Rmb355/t, compared with Conch’s 2015E EV/t of Rmb492/t. Volatility Volatility Percentile 20th 40th 60th 80th 100th Implications Anhui Conch Cement (H) (0914.HK) We see strategic merit for both West China Cement and Anhui Conch. Asia Pacific Metals & Mining Peer Group Average * Returns = Return on Capital For a complete description of the investment West China Cement is Shaanxi’s biggest cement producer, with dominant profile measures please refer to the market position in South Shaanxi (75% market share), while Conch is its disclosure section of this document. major competitor in Central Shaanxi. After the acquisition, Conch and Key data Current West China Cement could control 46% of Central and South Shaanxi Price (HK$) 29.10 12 month price target (HK$) 35.80 capacity, and we note that better market cooperation should enhance 600585.SS Price (Rmb) 24.88 600585.SS 12 month price target (Rmb) 28.00 profitability in the region. Market cap (HK$ mn / US$ mn) 154,209.7 / 19,891.4 Foreign ownership (%) -- Ytd Shaanxi cement price is down 5% due to weak demand. We think any 12/14 12/15E 12/16E 12/17E EPS (Rmb) 2.07 2.11 2.44 2.54 potential improvement in the market structure post the proposed deal could EPS growth (%) 17.0 1.9 15.8 4.0 EPS (diluted) (Rmb) 2.07 2.11 2.44 2.54 help stabilize pricing in the region, and note that WCC and Conch’s Shaanxi EPS (basic pre-ex) (Rmb) 2.07 2.11 2.44 2.54 plants are well positioned to benefit from any demand uptick. -

HKEX Environmental, Social and Governance Reporting Guide

About This Report This report is a true reflection of how BBMG Corporation (hereinafter referred to as "BBMG" or the "Company") has actively fulfilled its economic, social and environmental responsibilities and in addition, has achieved comprehensive, coordinated and sustainable development. Statements concerning future business plans, development strategies, and any other future endeavors herein do not constitute a substantial commitment of the Company to investors. Reporting Period This report covers the period from 1 January 2018 to 31 December 2018. Part of the contents of the report may cover periods outside of the above reportin period. Scope of the Report All cases and materials in this report are from BBMG and its subsidiaries. Sources of Information The data and information used in this report come from the following sources: internal data collection and statistics systems of BBMG, report preparation from qualitative and quantitative information collection tools, and cases of social responsibility practice submitted by subsidiary companies. Basis of Reporting This report has been prepared in compliance with the social responsibility information disclosure standards that are commonly accepted in the industry. Based on the industry background, this report highlights the characteristics of the Company. In accordance with the ESG Reporting Guide of the Hong Kong Stock Exchange Limited, the report was prepared in strict compliance with the four principles for ESG reporting - “Materiality”, “Quantitative”, “Balance”, and “Consistency” - and the requirements of “Director Responsibility” with reference to the Guidelines for Environmental Information Disclosure of Listed Companies of the Shanghai Stock Exchange, the Guidelines for Preparation of Social Responsibility Report for Cement Enterprises of China Cement Association, and the Global Reporting Initiative (GRI) Standards. -

Bilag 3. Negativlister I Relation Til Producenter Af Fossile Brændstoffer M.V. Københavns Kommunes Finansielle Strategi Og Risikopolitik

Bilag 3. Negativlister i relation til producenter af fossile brændstoffer m.v. Københavns Kommunes finansielle strategi og risikopolitik D. 8. juni 2016 Læsevejledning til negativlisten: Moderselskab / øverste ejer vises med fed skrift til venstre. Med almindelig tekst, indrykket, er de underliggende selskaber, der udsteder aktier og erhvervsobligationer. Det er de underliggende, udstedende selskaber, der er omfattet af negativlisten Moderselskab / øverste ejer – udstedende selskab Acergy SA SUBSEA 7 Inc Subsea 7 SA Adani Enterprises Ltd Adani Enterprises Ltd Adani Power Ltd Adani Power Ltd Adaro Energy Tbk PT Adaro Energy Tbk PT Adaro Indonesia PT Alam Tri Abadi PT Advantage Oil & Gas Ltd Advantage Oil & Gas Ltd Afren PLC Afren PLC Africa Oil Corp Africa Oil Corp AGL Energy Ltd AGL Electricity VIC Pty Ltd AGL Energy Ltd AGL Sales Pty Ltd Victorian Energy Pty Ltd Aker Solutions ASA Akastor ASA Aker Solutions Holding ASA Aker Solutions ASA Alliant Energy Corp Alliant Energy Corp Alliant Energy Resources LLC Interstate Power & Light Co Wisconsin Power & Light Co Alpha Natural Resources Inc Alex Energy Inc Alliance Coal Corp Alpha Appalachia Holdings Inc Alpha Appalachia Services Inc Alpha Natural Resource Inc/Old Alpha Natural Resources Inc Alpha Natural Resources LLC Alpha Natural Resources LLC / Alpha Natural Resources Capital Corp Alpha NR Holding Inc Aracoma Coal Co Inc AT Massey Coal Co Inc Bandmill Coal Corp Bandytown Coal Co Belfry Coal Corp Belle Coal Co Inc Ben Creek Coal Co Big Bear Mining Co Big Laurel Mining Corp Black King Mine -

2012 Annual Report

2012 AnnuAl RepoRt IllInoIs state Board of Investment Table of Contents INTRODUCTION 2 Board Members 3 Letter to Trustees 8 Financial Highlights 9 Ten Year Summary FINANCIAL STATEMENTS 10 Independent Auditors’ Report 11 Financial Statements 12 Management’s Discussion and Analysis 14 Statements of Net Assets 15 Statements of Changes in Net Assets 16 Notes to Financial Statements SUPPLEMENTAL FINANCIAL INFORMATION 32 Portfolio of Investments 118 Portfolio Data 120 Investment Transactions with Brokers and Dealers 122 Restricted Investments 124 Staff and Investment Managers Printed on contract by authority of the State of Illinois, December 13, 2012 (100 copies at $17.80 each) ILLINOIS STATE BOARD OF INVESTMENT 1 Board Members Devon Bruce Roderick Bashir Justice Thomas E. Hoffman CHAIRMAN EXECUTIVE COMMITTEE Devon Bruce Devon Bruce Appointed Member Chairman VICE CHAIRMAN Roderick Bashir Roderick Bashir Vice Chairman Appointed Member Thomas E. Hoffman RECORDING SECRETARY Recording Secretary Justice Thomas E. Hoffman Michele Bush John Casey Michele Bush Chairman, Board of Trustees Judges’ Retirement System of Illinois Member at Large Steven Powell AUDIT & COMPLIANCE COMMITTEE Appointed Member Michele Bush, Chairman James Clayborne, Jr. Michele Bush Thomas E. Hoffman Appointed Member Steven Powell Judy Baar Topinka John Casey Appointed Member INVESTMENT POLICY COMMITTEE Devon Bruce Senator James Clayborne, Jr. Roderick Bashir Chairman, Board of Trustees James Clayborne, Jr. Steven Powell Michele Bush General Assembly Retirement System John Casey -

Annual Report

(a joint stock company incorporated in the People’s Republic of China with limited liability) Stock Code : 2009 Tower D, Global Trade Center No. 36, North Third Ring Road East Dongcheng District, Beijing, China (100013) www.bbmg.com.cn/listco ANNUAL REPORT For Identication Purposes Only CONTENTS 2 FINANCIAL HIGHLIGHTS 3 CORPORATE INFORMATION 6 CORPORATE PROFILE 9 BIOGRAPHIES OF DIRECTORS, SUPERVISORS AND SENIOR MANAGEMENT 22 CHAIRMAN’S STATEMENT 26 MANAGEMENT DISCUSSION & ANALYSIS 73 REPORT OF THE DIRECTORS 88 REPORT OF THE SUPERVISORY BOARD 94 INVESTOR RELATIONS REPORT 98 CORPORATE GOVERNANCE REPORT 132 AUDITORS’ REPORT 139 AUDITED CONSOLIDATED BALANCE SHEET 142 AUDITED CONSOLIDATED INCOME STATEMENT 144 AUDITED CONSOLIDATED STATEMENT OF CHANGES IN SHAREHOLDERS’ EQUITY 148 AUDITED CONSOLIDATED STATEMENT OF CASH FLOWS 150 AUDITED BALANCE SHEET OF THE COMPANY 152 AUDITED INCOME STATEMENT OF THE COMPANY 153 AUDITED STATEMENT OF CHANGES IN SHAREHOLDERS’ EQUITY OF THE COMPANY 155 AUDITED STATEMENT OF CASH FLOWS OF THE COMPANY 157 NOTES TO FINANCIAL STATEMENTS 406 SUPPLEMENTARY INFORMATION TO FINANCIAL STATEMENTS 408 FIVE YEARS FINANCIAL SUMMARY 2 BBMG CORPORATION FINANCIAL HIGHLIGHTS 2020 2019 Change Operating revenue (RMB’000) 108,004,884 91,829,311 16,175,573 17.6% Decreased by 6.7 Gross profit margin from principal business (%) 19.8 26.5 percentage points Net profit attributable to the shareholders of the parent company (RMB’000) 2,843,773 3,693,583 -849,810 -23.0% Core net profit attributable to the shareholders of the parent company (excluding -

CHINA ENERGY ENGINEERING CORPORATION LIMITED* (A Joint Stock Company Incorporated in the People’S Republic of China with Limited Liability) (Stock Code: 3996)

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. CHINA ENERGY ENGINEERING CORPORATION LIMITED* (A joint stock company incorporated in the People’s Republic of China with limited liability) (Stock Code: 3996) ANNOUNCEMENT PROPOSED APPOINTMENT OF THE DIRECTORS FOR THE THIRD SESSION OF THE BOARD OF DIRECTORS The term of the second session of the board of directors of China Energy Engineering Corporation Limited (the “Company”) expired on 28 December 2020. On 12 January 2021, the board of directors of the Company (the “Board”) is pleased to announce that it had agreed to nominate Mr. Song Hailiang, Mr. Sun Hongshui and Mr. Ma Mingwei as the candidates for executive director for the third session of the Board of the Company, Mr. Li Shulei, Mr. Liu Xueshi and Mr. Si Xinbo as the candidates for non-executive director for the third session of the Board of the Company as well as Mr. Zhao Lixin, Mr. Cheng Niangao and Dr. Ngai Wai Fung as the candidates for independent non- executive director for the third session of the Board of the Company (collectively, the “Director Candidates”). Pursuant to the articles of association of the Company and the applicable laws and regulations in the People’s Republic of China, the aforesaid proposals will be submitted to the first extraordinary general meeting of the Company of 2021 for consideration and approval. -

Capturing the Chinese A-Shares and H-Shares Anomaly 2017 | Ftserussell.Com 1

Research Capturing the Chinese A-shares and H-shares Anomaly 2017 | ftserussell.com 1. Introduction The Chinese equity market is composed of a domestic and an offshore market. The Shanghai Stock Exchange and the Shenzhen Stock Exchange are the two exchanges operating in mainland China and they were established in the early 1990s. The majority of Chinese stocks are listed on the Shanghai or Shenzhen Stock Exchanges and these stocks are generally known as China A-shares. A-shares constitute China’s domestic market. In addition, there is an offshore market. Twenty five years ago the then China Vice Premier Zhu Rongji gave his approval for Chinese State Owned Enterprises (SOEs) to list their stocks on the Hong Kong Stock Exchange. The intention, in addition to capital raising, was to upgrade the SOEs’ corporate governance and management standards through fulfilling international practices. The offshore Chinese equity market has grown rapidly since. Nowadays it is easy to find Chinese companies listed on different exchanges globally including Hong Kong, New York, London or Singapore etc. In order to form a complete picture of the Chinese market both the domestic and offshore markets must be considered together. When a PRC-incorporated company is listed on the Hong Kong Stock Exchange (HKEx), it is regarded as the H-share, with the letter H referring to Hong The existence Kong. According to information provided by HKEx, nine state enterprises were approved for listing in Hong Kong on October 6, 1992. Tsingtao Brewery was of A-share and the first company to be listed. Its shares started trading on the Hong Kong Stock H-share markets Exchange on July 15, 1993. -

FTSE Publications

2 FTSE Russell Publications FTSE Global All Cap ex Canada 19 August 2019 China A Inclusion Indicative Index Weight Data as at Closing on 28 June 2019 Index Index Index Constituent Country Constituent Country Constituent Country weight (%) weight (%) weight (%) 1&1 Drillisch <0.005 GERMANY Accell Group <0.005 NETHERLANDS Advanced Wireless Semiconductor <0.005 TAIWAN 1st Source <0.005 USA Accent Group <0.005 AUSTRALIA AdvanSix <0.005 USA 21Vianet Group (ADS) (N Shares) <0.005 CHINA Accenture Cl A 0.23 USA Advantech 0.01 TAIWAN 2U <0.005 USA Acciona S.A. <0.005 SPAIN Advantest Corp 0.01 JAPAN 360 Security (A) <0.005 CHINA ACCO Brands <0.005 USA Advtech <0.005 SOUTH AFRICA 361 Degrees International (P Chip) <0.005 CHINA Accor 0.02 FRANCE Adyen 0.02 NETHERLANDS 3-D Systems <0.005 USA Accordia Golf Trust <0.005 SINGAPORE Aecc Aero Engine Control (A) <0.005 CHINA 3i Group 0.03 UNITED Accton Technology <0.005 TAIWAN Aecc Aero Science Technology (A) <0.005 CHINA KINGDOM Ace Hardware Indonesia <0.005 INDONESIA AECC Aviation Power (A) <0.005 CHINA 3M Company 0.19 USA Acea <0.005 ITALY AECI <0.005 SOUTH AFRICA 3M India <0.005 INDIA Acer <0.005 TAIWAN AECOM 0.01 USA 3SBio (P Chip) <0.005 CHINA Acerinox <0.005 SPAIN Aedas Homes <0.005 SPAIN 51job ADR (N Shares) <0.005 CHINA Achilles <0.005 JAPAN Aedifica <0.005 BELGIUM 58.com ADS (N Shares) 0.01 CHINA ACI Worldwide 0.01 USA Aegean Airlines SA <0.005 GREECE 5I5j Holding Group (A) <0.005 CHINA Ackermans & Van Haaren 0.01 BELGIUM Aegion Corp.