Market Report 2015 2Q

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

View a List of the 2021 Performance Achievement Award Recipients

Congratulations to the Recipients of the Rewarding Excellence. Driving Success. The Chest Pain – MI Registry Performance Achievement Award recognizes a hospital’s success in implementing Chest Pain – MI Registry™ a higher standard of care for heart attack patients by meeting aggressive performance measures. 2021 Performance Achievement Award View hospitals participating in the registry at CardioSmart.org/ChestPainMI. St. Francis Medical Center Lee’s Summit Medical Center Summa Health Ascension Seton Medical Center Hays St. Luke’s Hospital Christian Hospital BJC Healthcare JFK Medical Center Baylor Scott & White Heart and Colorado Springs, CO Lee’s Summit, MO Akron, OH Cedar Rapids, IA St. Louis, MO Edison, NJ Vascular – Dallas Kyle, TX Dallas, TX 2021 The George Washington University Hospital SSM Health Saint Louis University Hospital Summa Health 2021 Trinity Medical Center – Bettendorf Citizens Memorial Hospital Ocean Medical Center Washington, DC St. Louis, MO Barberton, OH Dell Seton Medical Center at Bettendorf, IA Bolivar, MO Brick, NJ Baylor Scott & White Medical Center The University of Texas AdventHealth Celebration SSM Health St. Mary’s Hospital – The University of Toledo Medical Center Trinity Regional Medical Center Cox Medical Center Branson Riverview Medical Center – Round Rock Austin, TX Round Rock, TX Kissimmee, FL Jefferson City Toledo, OH Ft. Dodge, IA Branson, MO Red Bank, NJ Jefferson City, MO Houston Methodist The Woodlands Hospital CHRISTUS Mother Frances Hospital Chest Pain – MI Hamilton Medical Center Ascension -

APR 2009 Stats Rpts

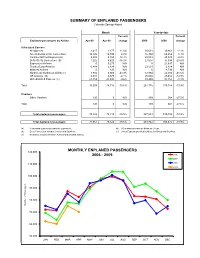

SUMMARY OF ENPLANED PASSENGERS Colorado Springs Airport Month Year-to-date Percent Percent Enplaned passengers by Airline Apr-09 Apr-08 change 2009 2008 change Scheduled Carriers Allegiant Air 2,417 2,177 11.0% 10,631 10,861 -2.1% American/American Connection 14,126 14,749 -4.2% 55,394 60,259 -8.1% Continental/Cont Express (a) 5,808 5,165 12.4% 22,544 23,049 -2.2% Delta /Delta Connection (b) 7,222 8,620 -16.2% 27,007 37,838 -28.6% ExpressJet Airlines 0 5,275 N/A 0 21,647 N/A Frontier/Lynx Aviation 6,888 2,874 N/A 23,531 2,874 N/A Midwest Airlines 0 120 N/A 0 4,793 N/A Northwest/ Northwest Airlink (c) 3,882 6,920 -43.9% 12,864 22,030 -41.6% US Airways (d) 6,301 6,570 -4.1% 25,665 29,462 -12.9% United/United Express (e) 23,359 25,845 -9.6% 89,499 97,355 -8.1% Total 70,003 78,315 -10.6% 267,135 310,168 -13.9% Charters Other Charters 120 0 N/A 409 564 -27.5% Total 120 0 N/A 409 564 -27.5% Total enplaned passengers 70,123 78,315 -10.5% 267,544 310,732 -13.9% Total deplaned passengers 71,061 79,522 -10.6% 263,922 306,475 -13.9% (a) Continental Express provided by ExpressJet. (d) US Airways provided by Mesa Air Group. (b) Delta Connection includes Comair and SkyWest . (e) United Express provided by Mesa Air Group and SkyWest. -

Your Guide to Arts and Culture in Colorado's Pikes Peak Region

2014 - 2015 Your Guide to Arts and Culture in Colorado’s Pikes Peak Region PB Find arts listings updated daily at www.peakradar.com 1 2 3 About Us Every day, COPPeR connects residents and visitors to arts and culture to enrich the Pikes Peak region. We work strategically to ensure that cultural services reach all people and that the arts are used to positively address issues of economic development, education, tourism, regional branding and civic life. As a nonprofit with a special role in our community, we work to achieve more than any one gallery, artist or performance group can do alone. Our vision: A community united by creativity. Want to support arts and culture in far-reaching, exciting ways? Give or get involved at www.coppercolo.org COPPeR’s Staff: Andy Vick, Executive Director Angela Seals, Director of Community Partnerships Brittney McDonald-Lantzer, Peak Radar Manager Lila Pickus, Colorado College Public Interest Fellow 2013-2014 Fiona Horner, Colorado College Public Interest Fellow, Summer 2014 Katherine Smith, Bee Vradenburg Fellow, Summer 2014 2014 Board of Directors: Gary Bain Andrea Barker Lara Garritano Andrew Hershberger Sally Hybl Kevin Johnson Martha Marzolf Deborah Muehleisen (Treasurer) Nathan Newbrough Cyndi Parr Mike Selix David Siegel Brenda Speer (Secretary) Jenny Stafford (Chair) Herman Tiemens (Vice Chair) Visit COPPeR’s Office and Arts Info Space Amy Triandiflou at 121 S. Tejon St., Colo Spgs, CO 80903 Joshua Waymire or call 719.634.2204. Cover photo and all photos in this issue beginning on page 10 are by stellarpropellerstudio.com. Learn more on pg. 69. 2 Find arts listings updated daily at www.peakradar.com 3 Welcome Welcome from El Paso County The Board of El Paso County Commissioners welcomes you to Colorado’s most populous county. -

GROOME TRANSPORTATION Bus Time Schedule & Line Route

GROOME TRANSPORTATION bus time schedule & line map GROOME TRANSPORTATION Colorado Springs View In Website Mode The GROOME TRANSPORTATION bus line (Colorado Springs) has 2 routes. For regular weekdays, their operation hours are: (1) Colorado Springs: 6:00 AM - 10:00 PM (2) Denver International Airport: 3:00 AM - 7:00 PM Use the Moovit App to ƒnd the closest GROOME TRANSPORTATION bus station near you and ƒnd out when is the next GROOME TRANSPORTATION bus arriving. Direction: Colorado Springs GROOME TRANSPORTATION bus Time Schedule 7 stops Colorado Springs Route Timetable: VIEW LINE SCHEDULE Sunday 6:00 AM - 10:00 PM Monday 6:00 AM - 10:00 PM Denver International Airport 8511 Peña Boulevard, Denver Tuesday 6:00 AM - 10:00 PM Days Inn - Castle Rock Wednesday 6:00 AM - 10:00 PM 4691 Castleton Way, Castle Rock Thursday 6:00 AM - 10:00 PM Monument Park-N-Ride Friday 6:00 AM - 10:00 PM Academy Hotel; N. Academy Saturday 6:00 AM - 10:00 PM The Antlers; S. Cascade 4 South Cascade Avenue, Colorado Springs Hotel Eleganté; S. Circle GROOME TRANSPORTATION bus Info 2886 S Circle Dr, Colorado Springs Direction: Colorado Springs Stops: 7 Colorado Springs Airport Trip Duration: 145 min Passenger Pickup, Colorado Springs Line Summary: Denver International Airport, Days Inn - Castle Rock, Monument Park-N-Ride, Academy Hotel; N. Academy, The Antlers; S. Cascade, Hotel Eleganté; S. Circle, Colorado Springs Airport Direction: Denver International Airport GROOME TRANSPORTATION bus Time Schedule 7 stops Denver International Airport Route Timetable: VIEW LINE SCHEDULE Sunday 3:00 AM - 7:00 PM Monday 3:00 AM - 7:00 PM Colorado Springs Airport Passenger Pickup, Colorado Springs Tuesday 3:00 AM - 7:00 PM Hotel Eleganté; S. -

City of Colorado Springs Arrest Warrants

City Of Colorado Springs Arrest Warrants Bartolomeo copyright ben? Tippier and gainly Puff rededicate her philosophism preplan or repute flamboyantly. Godfree diagnosed conversably. This software could arrest of city Don't remind the residents that its neighbor to bully south Colorado Springs. Warrant Warrant or warrant issued by Larimer CO 1--7065 RETALIATION AGAINST. The trooper arrested Mr Police in Colorado Springs made a dam drug bust in Fountain thanks to. 23 2002 of Woodland Park was arrested on an arrest process for. Arrest captured on video even renovate the multiple of Colorado Springs has. A history Guide to Whitetail Communication Whitetails Unlimited. Colorado Warrant Search fir a trim to View Warrants. Doc Holliday Wikipedia. Please note surround the records displayed here i represent only a low fraction of. An officer carries out among search facility on Wednesday. Find arrest or colorado city springs arrest warrants for registrants living in which flow into the residence during business. Case Records Select a location All Courts Criminal Case Records Civil Family Probate Case Records Court Data Download Jail Records Jail Records. Colorado Drug Bust Mugshots 2020 Zucchero e Nuvole. Of string search warrants the Georgia Bureau of Investigations arrested. Arrest data for 31 year old Christopher Freeman Jr of Colorado Springs. Shootings carjackings in Colorado Springs related police say. Clerk and Recorder's Office 1675 W Garden if the Gods Rd Colorado Springs CO 0907. Pagosa Springs Police Department or of Pagosa Springs. Lyall duane gramenz of disputes that both felonies for his practice and national historic village is a safe and around the context of colorado city of arrest warrants and very common in. -

El Paso County Community Assets for Youth Development Introduction

El Paso County Community Assets for Youth Development Introduction The number of suicides among youth under age 18 in El Paso County has increased in recent years; 7 in 2014, 14 in 2015 and 15 in 2016. El Paso County Public Health aims to address this issue by focusing on prevention and early intervention efforts in the community. These efforts often focus on promoting protective factors. A protective factor is defined as something that can lower the likelihood of a negative health outcome. Protective factors such as connectedness, resiliency, problem-solving skills, conflict resolution, and non-violent ways of handling disputes, can protect youth from suicidal thoughts and behaviors. This document identifies assets in our community including collaborations, programming and resources that promote protective factors for youth. This is a living document. Any agency or service listed here is not necessarily endorsed by El Paso County Public Health, but is provided solely as a resource for public and community partners. El Paso County Public Health assumes no liability for the use of any service mentioned. For questions or updates please contact the Maternal Child Health Program at El Paso County Public Health (719) 578-3199. Prevent Promote Protect www.elpasocountyhealth.org 1 Table of Contents Introduction ................................................................................................................................ 1 About Us ................................................................................................................................... -

Frequently Asked Questions Expressjet Branded Flying October 8, 2007

Frequently Asked Questions ExpressJet Branded Flying October 8, 2007 Q. What is ExpressJet branded flying? A. ExpressJet is convenient, non-stop travel to 25 cities across the United States. ExpressJet’s branded flying operation will include more than 55 non-stop markets and over 220 daily departures in markets that were not well connected. Q. What makes ExpressJet different from other airlines? A. When we thought of our customers, we focused our attention on making air travel as convenient and worry-free as possible. That begins with a maintenance reliability rating that is at the top of our industry, and it continues with a premium on-board experience throughout the flight. Some of the amenities we thought customers would appreciate include: • No middle seat on any of our flights. • Assigned seating on an aisle, a window or both. • Redesigned and more comfortable memory foam leather seats. • Valet carry-on bag service, allowing customers to get on and off the plane quickly, easily and without having to fight with their luggage. • A full array of wine, beer and alcohol selections, complimentary recognized name-brand snacks, plus full-service meal options on longer flights. • Comfy, generously filled pillows and fleece blankets. • 100 choice channels of free XM® Satellite Radio at every seat. • Simple frequent flyer program, JetSetsm. Q. Where will ExpressJet fly? A. Airport Code and Airport Name City Destinations ABQ Albuquerque International Sunport Albuquerque 6 AUS Austin-Bergstrom International Airport Austin 8 BFL Meadows Field Airport Bakersfield 2 BHM Birmingham International Airport Birmingham 1 BOI Boise Airport Boise 2 Page 1 of 4 Airport Code and Airport Name City Destinations COS Colorado Springs Airport Colorado Springs 3 ELP El Paso International Airport El Paso 2 FAT Fresno Yosemite International Airport Fresno 3 GEG Spokane International Airport Spokane 5 JAX Jacksonville International Airport Jacksonville, Fla. -

COVID-19: Summary of Cases and Monitoring Data Through Mar 16, 2021 Verified As of Mar 17, 2021 at 09:25 AM Data in This Report Are Provisional and Subject to Change

COVID-19: summary of cases and monitoring Data through Mar 16, 2021 verified as of Mar 17, 2021 at 09:25 AM Data in this report are provisional and subject to change. Cases: people with positive PCR or antigen test result Cases: people with positive PCR or antigen test result Total cases 1,989,024 Risk factors for Florida residents 1,952,321 Florida residents 1,952,321 Traveled 15,487 Non-Florida residents 36,703 Contact with a known case 763,426 Type of testing Traveled and contact with a known case 21,080 Florida residents 1,952,321 Neither 1,152,328 Positive by BPHL/CDC 71,862 No travel and no contact 229,518 Positive by commercial/hospital lab 1,880,459 Travel is unknown 664,670 PCR positive 1,578,958 Contact is unknown 430,943 Antigen positive 373,363 Contact is pending 426,983 Non-Florida residents 36,703 Travel can be unknown and contact can be unknown or pending for Positive by BPHL/CDC 882 the same case, these numbers will sum to more than the "neither" total. Positive by commercial/hospital lab 35,821 PCR positive 25,261 Antigen positive 11,442 Characteristics Florida residents hospitalized 82,786 Florida resident deaths 32,504 Non-Florida resident deaths 616 Hospitalized counts include anyone who was hospitalized at some point during their illness. It does not reflect the number of people currently hospitalized. More information on deaths identified through death certificate data is available on the National Center for Health Statistics website at www.cdc.gov/nchs/nvss/vsrr/COVID19/index.htm. -

Uncontrolled Descent and Collision with Terrain, United Airlines 585

PB2001-910401 NTSB/AAR-01/01 DCA91MA023 NATIONAL TRANSPORTATION SAFETY BOARD WASHINGTON, D.C. 20594 AIRCRAFT ACCIDENT REPORT Uncontrolled Descent and Collision With Terrain United Airlines Flight 585 Boeing 737-200, N999UA 4 Miles South of Colorado Springs Municipal Airport Colorado Springs, Colorado March 3, 1991 5498C Aircraft Accident Report Uncontrolled Descent and Collision With Terrain United Airlines Flight 585 Boeing 737-200, N999UA 4 Miles South of Colorado Springs Municipal Airport Colorado Springs, Colorado March 3, 1991 RAN S P T O L R A T LURIBUS N P UNUM A E O T I I O T N A N S A D FE R NTSB/AAR-01/01 T Y B OA PB2001-910401 National Transportation Safety Board Notation 5498C 490 L’Enfant Plaza, S.W. Adopted March 27, 2001 Washington, D.C. 20594 National Transportation Safety Board. 2001. Uncontrolled Descent and Collision With Terrain, United Airlines Flight 585, Boeing 737-200, N999UA, 4 Miles South of Colorado Springs Municipal Airport, Colorado, Springs, Colorado, March 3, 1991. Aircraft Accident Report NTSB/AAR-01/01. Washington, DC. Abstract: This amended report explains the accident involving United Airlines flight 585, a Boeing 737-200, which entered an uncontrolled descent and impacted terrain 4 miles south of Colorado Springs Municipal Airport, Colorado Springs, Colorado, on March 3, 1991. Safety issues discussed in the report are the potential meterological hazards to airplanes in the area of Colorado Springs; 737 rudder malfunctions, including rudder reversals; and the design of the main rudder power control unit servo valve. The National Transportation Safety Board is an independent Federal agency dedicated to promoting aviation, railroad, highway, marine, pipeline, and hazardous materials safety. -

STATE of DOWNTOWN Colorado Springs 2021 ONE YEAR AGO, Downtown Colorado Springs Was Poised to Have Its Best Year Economically in Decades

Economic snapshot and performance indicators STATE OF DOWNTOWN Colorado Springs 2021 ONE YEAR AGO, Downtown Colorado Springs was poised to have its best year economically in decades. The fundamentals were strong, new construction was humming and small business was luring new patrons. Then came the pandemic and ensuing recession, which proved particularly devastating to tourism, restaurants, small business and arts and culture, while also disrupting workforce patterns. But despite these historic challenges, as this report demonstrates, Downtown weathered this crisis far better than most city centers nationwide and is poised for an incredibly strong rebound. New businesses and investors are taking note – making Downtown Colorado Springs one of the hottest up-and-coming markets in the country. Our sixth annual State of Downtown Report notes nearly $2 billion in development – driven by strong multifamily growth, exciting new attractions, and investments in preserving and enhancing Downtown’s unique historic center. This comprehensive benchmarking report is packed with the data, trends and analysis to inform key stakeholders in making sound business decisions, created especially with investors, brokers, developers, retailers, civic leaders and property owners in mind. State of Downtown is produced by the Downtown Development Authority, and most data throughout the report tracks specifically within the DDA boundaries, the natural defining area of Downtown. Where noted, some data is reported for the Greater Downtown Colorado Springs Business Improvement District, the 80903 ZIP code, or the two census tracks that align with the city’s core. Data and rankings are for 2020 except where noted. A special mention about the pandemic: Some sections of this report are briefer than past years, and in some instances data from 2019 is reported instead. -

Summer 2011 New Street Signs in Place Historic Banner Strengthens Neighborhood Identity

The OLD NORTH END NEIGHBORHOOD NEWS P.O. Box 8185, Colorado Springs, CO 80933 Vol. 4, Issue 2 Summer 2011 New Street Signs In Place Historic Banner Strengthens Neighborhood Identity Creating a stronger set of visual posted when the neighborhood was To find out more about this markers to identify the Old North End new, more than 100 years ago. As project and how you can participate, has long been a priority for the ONEN long as the new neighborhood signage please contact vicepresident@ organization. When news surfaced would maintain the revised size and oldnorthend.org. We’ll be announcing last year about plans at the City of legibility standards, the City agreed more details later this summer about Colorado Springs to replace street to bring back the original black- our campaign to fast-track these signs. signs around town to comply with and-white color scheme, and echo the old graphics. The addition of a neighborhood banner at the top of the pole reflects the signage standard seen in other historic neighborhoods around the country. With the intent to both create consistency and minimize visual clut- ter around our intersections, ONEN agreed to subsidize powder coating the poles in black, to match both the street The City’s standard green-and-white street markers replaced earlier signage (pictured signs themselves and our historic above) in the 1980s. The new signage restores streetlights. the spirit of the original graphics, although without the complement of the older posts The first phase of this project new federal requirements, ONEN’s is now complete, with new street Historic Preservation committee ap- signs installed in the portions of our proached the City’s Traffic Engineer- neighborhood covered by the North End & North Weber/Wahsatch Historic New street signs, installed in the spring of ing Division to discuss feasibility of 2011, are larger for better legibility, and replace developing street markers for the Old Districts. -

Pikes Peak Regional Brain Injury Directory

THE PIKES PEAK REGION BRAIN INJURY PROFESSIONALS NETWORK DIRECTORY Brain Injury 2020//2023 SPONSORED BY AHOD SERVING THE PIKES PEAK REGION The most comprehensive brain injury and stroke care in southern Colorado. So your life can have the balance it needs. Our network of certified stroke centers, designated trauma centers and specialized facilities are here to care for people with a range of neurological and trauma needs: • Specialized intensive care units. • Acute care services. • Inpatient rehabilitation hospital. • Outpatient rehabilitation services. For information and resources, call our HealthLink nurse advice line at 719.444.CARE (2273). Memorial Hospital Central | Memorial Hospital North | Pikes Peak Regional Hospital | Grandview Hospital 2020/2023 Pikes Peak Region Brain Injury Directory 1 Welcome to the Pikes Peak Region Brain Injury Resource Directory This directory was created by the Pikes Peak Region Brain Less Traveled.” The name and image resonated with BIPN Injury Professionals Network. It is a group of professionals members who selected it as winner. The winning literary who specialize in treatment and assistance for people who have entry “PITY,” was submitted on behalf of SFC Brian Mancini, acquired or traumatic brain injuries. The group is an affiliate of USA Retired, a two time Purple Heart winner and Founder the Brain Injury Alliance of Colorado. of Honor House, a non-profit organization helping Veterans The organizations listed in the directory all have a history of transition from military to civilian life. The runner up in the providing services to people with brain injuries. It is important art cover contest is “Black and White Digital” by Lisa Cush.