A Guide to Going

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Initial Public Offerings

November 2017 Initial Public Offerings An Issuer’s Guide (US Edition) Contents INTRODUCTION 1 What Are the Potential Benefits of Conducting an IPO? 1 What Are the Potential Costs and Other Potential Downsides of Conducting an IPO? 1 Is Your Company Ready for an IPO? 2 GETTING READY 3 Are Changes Needed in the Company’s Capital Structure or Relationships with Its Key Stockholders or Other Related Parties? 3 What Is the Right Corporate Governance Structure for the Company Post-IPO? 5 Are the Company’s Existing Financial Statements Suitable? 6 Are the Company’s Pre-IPO Equity Awards Problematic? 6 How Should Investor Relations Be Handled? 7 Which Securities Exchange to List On? 8 OFFER STRUCTURE 9 Offer Size 9 Primary vs. Secondary Shares 9 Allocation—Institutional vs. Retail 9 KEY DOCUMENTS 11 Registration Statement 11 Form 8-A – Exchange Act Registration Statement 19 Underwriting Agreement 20 Lock-Up Agreements 21 Legal Opinions and Negative Assurance Letters 22 Comfort Letters 22 Engagement Letter with the Underwriters 23 KEY PARTIES 24 Issuer 24 Selling Stockholders 24 Management of the Issuer 24 Auditors 24 Underwriters 24 Legal Advisers 25 Other Parties 25 i Initial Public Offerings THE IPO PROCESS 26 Organizational or “Kick-Off” Meeting 26 The Due Diligence Review 26 Drafting Responsibility and Drafting Sessions 27 Filing with the SEC, FINRA, a Securities Exchange and the State Securities Commissions 27 SEC Review 29 Book-Building and Roadshow 30 Price Determination 30 Allocation and Settlement or Closing 31 Publicity Considerations -

PPD Initial Public Offering

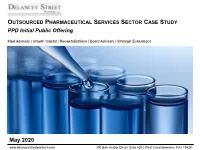

OUTSOURCED PHARMACEUTICAL SERVICES SECTOR CASE STUDY PPD Initial Public Offering M&A Advisory | Growth Capital | Recapitalizations | Board Advisory | Strategic Evaluations May 2020 www.delanceystreetpartners.com 300 Barr Harbor Drive | Suite 420 | West Conshohocken | PA | 19428 PPD INITIAL PUBLIC OFFERING Transaction Overview PPD (NASDAQ: PPD) Stock Price Performance $34.00 On February 5, 2020, Pharmaceutical Product $33.00 2/11/20 Closing Price: $32.87 Development (PPD) announced it raised $1.86 billion in its $32.00 initial public offering (IPO) $31.00 The company announced it priced 60 million primary shares of its common stock at the top end of its targeted range or $27.00 per share $30.00 2/6/20 Opening Price: $30.99 ‒ The underwriters simultaneously exercised the greenshoe option, $29.00 offering an additional 9 million primary shares of PPD’s common stock $28.00 at the IPO price, resulting in total IPO shares and gross proceeds of 69 million and $1.86 billion, respectively $27.00 3/6/20 Closing Price: $28.60 ‒ Implied Enterprise Value of $13.1 billion $26.00 ‒ Implied Enterprise Value / LTM Adjusted EBITDA multiple of 16.9x $25.00 PPD used the net proceeds from the offering to redeem a portion of its 5-Mar 1-Mar 2-Mar 3-Mar 4-Mar 6-Mar 7-Feb 8-Feb 9-Feb senior notes that were due to retire in 2022 and will use any remaining 6-Feb 11-Feb 10-Feb 12-Feb 13-Feb 14-Feb 15-Feb 16-Feb 17-Feb 18-Feb 19-Feb 20-Feb 21-Feb 22-Feb 23-Feb 24-Feb 25-Feb 26-Feb 27-Feb 28-Feb 29-Feb proceeds for general corporate purposes On February 6th, shares -

How Risky Is the Debt in Highly Leveraged Transactions?*

Journal of Financial Economics 27 (1990) 215-24.5. North-Holland How risky is the debt in highly leveraged transactions?* Steven N. Kaplan University of Chicago, Chicago, IL 60637, USA Jeremy C. Stein Massachusetts Institute of Technology Cambridge, MA 02139, USA Received December 1989, final version received June 1990 This paper estimates the systematic risk of the debt in public leveraged recapitalizations. We calculate this risk as a function of the difference in systematic equity risk before and after the recapitalization. The increase in equity risk is surprisingly small after a recapitalization, ranging from 37% to 57%, depending on the estimation method. If total company risk is unchanged, the implied systematic risk of the post-recapitalization debt in twelve transactions averages 0.65. Alternatively, if the entire market-adjusted premium in the leveraged recapitalization represents a reduction in fixed costs, the implied systematic risk of this debt averages 0.40. 1. Introduction Highly leveraged transactions such as leveraged buyouts (LBOs) and lever- aged recapitalizations have grown explosively in number and size over the last several years. These transactions are largely financed with a combination of senior bank debt and subordinated lower-grade or ‘junk’ debt. Recently, the debt in these transactions has come under increasing scrutiny from investors, politicians, and academics. All three groups have asked in one way or another how risky leveraged buyout debt is in relation to the return it *Cedric Antosiewicz provided excellent research assistance. Paul Asquith, Douglas Diamond, Eugene Fama, Wayne Person, William Fruhan (the referee), Kenneth French, Robert Korajczyk, Richard Leftwich, Jeffrey Mackie-Mason, Merton Miller, Stewart Myers, Krishna Palepu, Richard Ruback (the editor), Andrei Shleifer, Robert Vishny, and seminar participants at the Securities and Exchange Commission, the University of Chicago, and MIT’s Sloan School made helpful comments on earlier drafts. -

A Roadmap to Initial Public Offerings

A Roadmap to Initial Public Offerings 2019 The FASB Accounting Standards Codification® material is copyrighted by the Financial Accounting Foundation, 401 Merritt 7, PO Box 5116, Norwalk, CT 06856-5116, and is reproduced with permission. This publication contains general information only and Deloitte is not, by means of this publication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor. Deloitte shall not be responsible for any loss sustained by any person who relies on this publication. As used in this document, “Deloitte” means Deloitte & Touche LLP, Deloitte Consulting LLP, Deloitte Tax LLP, and Deloitte Financial Advisory Services LLP, which are separate subsidiaries of Deloitte LLP. Please see www.deloitte.com/us/about for a detailed description of our legal structure. Certain services may not be available to attest clients under the rules and regulations of public accounting. Copyright © 2019 Deloitte Development LLC. All rights reserved. Other Publications in Deloitte’s Roadmap Series Business Combinations Business Combinations — SEC Reporting Considerations Carve-Out Transactions Consolidation — Identifying a Controlling Financial Interest Contracts on an Entity’s Own Equity -

Vantage Towers AG

Prospectus dated March 8, 2021 Prospectus for the public offering in the Federal Republic of Germany of 88,888,889 existing ordinary registered shares with no par value (Namensaktien ohne Nennbetrag) from the holdings of the Existing Shareholder, of 22,222,222 existing ordinary registered shares with no par value (Namensaktien ohne Nennbetrag) from the holdings of the Existing Shareholder, with the number of shares to be actually placed with investors subject to the exercise of an Upsize Option upon the decision of the Existing Shareholder, in agreement with the Joint Global Coordinators, on the date of pricing, and of 13,333,333 existing ordinary registered shares with no par value (Namensaktien ohne Nennbetrag) from the holdings of the Existing Shareholder in connection with a possible over-allotment, and at the same time for the admission to trading on the regulated market (regulierter Markt) of the Frankfurt Stock Exchange (Frankfurter Wertpapierbörse) with simultaneous admission to the sub- segment of the regulated market with additional post-admission obligations (Prime Standard) of the Frankfurt Stock Exchange (Frankfurter Wertpapierbörse) of 505,782,265 existing ordinary registered shares with no par value (Namensaktien ohne Nennbetrag) (existing share capital), each such share with a notional value of EUR 1.00 in the Company’s share capital and full dividend rights as of April 1, 2020 of Vantage Towers AG Düsseldorf, Germany Price Range: EUR 22.50 – EUR 29.00 International Securities Identification Number (ISIN): DE000A3H3LL2 German Securities Code (Wertpapierkennnummer, WKN): A3H 3LL Common Code: 230832161 Ticker Symbol: VTWR Joint Global Coordinators BofA Securities Morgan Stanley UBS Joint Bookrunners Barclays Berenberg BNP PARIBAS Deutsche Bank Goldman Sachs Jefferies TABLE OF CONTENTS Page I. -

ALFI TASC~Investment Fund Processing in Luxembourg Versio…

Investment Fund Processing Guidelines Order and Settlement of Investment Funds in Luxembourg A Working Document By the ALFI TA Forum Steering Committee Fund Processing Standardisation Working Group February 2007 Version 1.0 Table of Contents 1 Introduction ................................................................................................................................................ 3 1.1 European Fund Processing Standardisation ....................................................................................... 3 1.2 Luxembourg Fund Processing Standardisation ................................................................................... 3 2 Background ................................................................................................................................................ 5 ISO 20022 .................................................................................................................................................... 5 3 Objective and benefits ............................................................................................................................... 5 4 The Luxembourg fund processing landscape .......................................................................................... 6 4.1 The Investment Management Business Model.................................................................................... 6 4.2 Fund Administration Functions............................................................................................................ 6 4.3 -

Recapitalization: Voting & Non- Voting Interests

Recapitalization: Voting & Non- Voting Interests Overview Recapitalization is basically a change in a corporation’s capital structure. Corporations recapitalize for a variety of reasons, but generally to make the company more stable or to bring in new investors. For closely held companies, recapitalizations can also be very effective in estate planning. When business interests pass to a successive generation, senior family members can transfer company stock in a tax-efficient manner by generating discounts. If the business agreement restricts certain rights, such as the right to vote or the ability to freely transfer the stock, those restricted business interests are typically worth less to an outside buyer, and hence “discountable” for valuation purposes. Regardless of whether the transfer is by gift or by sale, recapitalization into voting and non-voting stock can allow the assets to be transferred at a lower value. Description and Operations The process by which an existing corporation can be reconfigured to create different classes of stock—such as voting and non-voting stock—is called “recapitalization.” Though not labeled a “recapitalization,” a limited liability company or a partnership can undergo a similar transformation by establishing voting and non-voting interests. Creation of Preferred and Common Stock with C Corporations Recapitalization can refer to the creation of common and preferred stock. Preferred stock has dividend and liquidation priority over common stock. In other words, the owner of preferred stock has a greater degree of security than the owner of common stock. Before 1990, a parent would shift common stock to a child and keep the preferred stock. -

Dmitri V. Kovalenko

Dmitri V. Kovalenko Partner, Moscow Mergers and Acquisitions; Private Equity; Capital Markets Dmitri Kovalenko is co-head of the Moscow office and represents international and Russian clients on a broad range of mergers and acquisitions, private equity and joint venture transac- tions in Russia and other countries covering various industries and sectors. Mr. Kovalenko has practiced law in Skadden’s Moscow, Chicago and Paris offices since 1994. He is ranked in the top tier for Russia M&A and Russia capital markets work by Chambers Global and Chambers Europe, as well as for private equity in Russia by Chambers Europe. Mr. Kovalenko also was named as the 2021 Mergers and Acquisitions Lawyer of the Year and the 2020 Capital Markets Lawyer of the Year by The Best Lawyers in Russia, and was listed in the publication’s Global Business Edition. Additionally, he is listed as a leading individual in IFLR1000 and Who’s Who Legal, as well as repeatedly in The Legal 500 EMEA as a member of its Commercial, Corporate and M&A: Moscow Hall of Fame. T: 7.495.797.4600 F: 7.495.797.4601 His M&A and private equity experience has included advising: [email protected] - Mercury Retail Group in its US$1.2 billion sale of JSC Dixy Group to PJSC Magnit; - Horvik Limited in relation to its preconditional mandatory offer to acquire Trans-Siberian Gold Education plc, an AIM-quoted gold producer; LL.M. (with honors), Northwestern - Kismet Acquisition One, a special purpose acquisition company, in its US$1.9 billion initial University School of Law, Chicago, merger with Nexters Global Limited, the first-ever de-SPAC transaction involving a Russian USA, 1996 company. -

Can Underwriters Profit from IPO Underpricing?

Footloose with Green Shoes: Can Underwriters Profit from IPO Underpricing? Patrick M. Corrigan† Why are green shoe options used in initial public offerings (IPOs)? And why do underwriters usually short sell an issuer’s stock in connection with its IPO? Are underwriters permitted to profit from these trading po- sitions? Scholars have long argued that underwriters use green shoe options together with short sales to facilitate price stabilizing activities, and that U.S. securities laws prohibit underwriters from using green shoe options to profit from IPO underpricing. This Article finds the conventional wisdom lacking. I find that underwriters may permissibly profit from IPO under- pricing by pairing purchases under a green shoe option with offshore short sales. I also find that underwriters may permissibly profit from IPO over- pricing by short selling the issuer’s stock in the initial distribution. The possession of a green shoe option and the ability to short sell IPOs effectively makes underwriters long a straddle at the IPO price. This posi- tion creates troubling incentivizes for underwriters to underprice or over- price IPOs, but not to price them accurately. This new principal trading theory for green shoe options and under- writer short sales provides novel explanations for systematic IPO mispric- ing, the explosive initial return variability during the internet bubble, and the observation of “laddering” in severely underpriced IPOs. This Article concludes by charting a new path for the regulatory scheme that applies to principal trading by underwriters in connection with securities offerings. Consistent with the purpose of preserving the integrity of securities markets, regulators should address the incentives of under- writers directly by prohibiting underwriters of an offering from enriching themselves through trading in the issuer’s securities. -

CASE STUDY How Carlyle Creates Value Deep Industryhow Expertise.Carlyle Global Creates Scale and Value Presence

CASE STUDY How Carlyle Creates Value Deep industryHow expertise.Carlyle Global Creates scale and Value presence. Extensive network of Operating Executives. And a wealth of investment portfolio data; we call it The Carlyle Edge. These are the four pillars of Carlyle’s value creation model. By leveragingDeep these industry core expertise. capabilities Global and scaleresources—Carlyle and presence. hasExtensive established network a 30-year of Operating overall Executives. track record And of investinga wealth in companies,of investment working portfolio to make data; them we better call it Theand Carlyleserving Edge. our investors’ These are needs. the four pillars of Carlyle’s value creation model. By leveraging these core capabilities and resources—Carlyle has established a 25-year overall track record of investing in companies, working to make them better and serving our investors’ needs. Carlyle, along with several other investors, led the recapitalization of the Bank of N.T. Butterfield & Son Limited. The new equity capital, which allowed the bank to remain independent, was part of a comprehensive plan to increase equity capital and de-risk Butterfield’s balance sheet. In addition, the new capital provided flexibility to restructure Butterfield’s investment portfolio, provision for non-performing loans, decrease earnings volatility, and maintain capital ratios well in excess of regulatory requirements. About Butterfield and the Transaction Carlyle invested in Butterfield in March 2010 through Carlyle Global Financial Services Partners. Established in 1958, Butterfield is the largest independent Bermuda-based depository institution. A publicly traded company, Butterfield shares are listed on the New York (NYSE), Bermuda (BSX) and Cayman Islands (CSX) stock exchanges. -

Is a Mezzanine Recapitalization Right for Your Business? Prepared By

Is a mezzanine recapitalization right for your business? Prepared by: Steve McCann, Manager, Center for Business Transition, RSM US LLP [email protected], +1 563 888 4015 October 2017 Owners of middle market companies still in growth mode face a • Subordinated, mezzanine debt. Pricing is typically in the variety of challenges and options in terms of raising capital to fund 12 to 15 percent range, with 11 to 13 percent being cash their continued growth. Likewise, owners of these companies may and the remainder payment in kind (PIK). This option also be searching for optimal ways to exit their business, when the may include warrants. time is right. The financing levels within a company usually have • Preferred equity. Pricing is typically in the 8 to 14 percent morphed into the present state and create a need for a fresh, real range, mostly PIK. This option may also include warrants viewpoint to fund an expansion or a business transition. but is less dilutive than common equity. Common equity. This option includes 35 to 40 percent In both these instances there are a variety of options available • of total capitalization, with a target internal rate of return to finance growth or provide shareholder liquidity, including: of 18 to 25 percent. • Senior secured debt, or first lien. In this option pricing tends In addition to the above alternatives, shareholders have other to increase with leverage, is dependent on availability of options to grow and achieve liquidity, including: collateral and is typically the London Interbank Offered Rate (LIBOR) plus 3 to 5 percent. -

Investments Statistical Digest 2006

INVESTMENTS STATISTICAL DIGEST C-0% M-18% Y-100% K-27% C-100% M-57% Y-0% K-40% 2 Highlights Introduction 3 E-Reporting The Cayman Islands Monetary Authority (CIMA) is pleased to release this 4 Hedge Funds Industry first edition of the Investments Statistical Digest, which presents never-before- 6 Financial Position 7 Fund Structure compiled information on the hedge funds industry. 8 Investment Management 9 Investment Strategy Drawn from the filings of over 5,000 CIMA-regulated funds, the digest provides 10 Asset Allocation the most accurate statistical snapshot of the Cayman Islands hedge funds industry 10 Fund Administration available to date. 11 Subscription Information 12 Glossary of Terms With the Cayman Islands being the premier jurisdiction for hedge fund domiciliation, the information in this digest is not only relevant to Cayman; it provides crucial insights into the nature, scope and performance of the hedge fund industry worldwide. It is CIMA’s hope that this data will contribute to the transparency and increased understanding of this dynamic global industry. Copyright (c) 2008 by the Cayman Islands Monetary Authority. All text, designs, graphics and other works in this document are the copyrighted works of the Cayman Islands Monetary Authority. All rights reserved. Any redistribution or reproduction, in whole or in part, without the permission of the Cayman Islands Monetary Authority, is strictly prohibited. 1.387 US$ Trillion Net Asset Value The data shows the diversification Highlights and financial strength of Cayman- domiciled funds The information presented in this digest is drawn from data that 5,052 Cayman-domiciled funds filed with CIMA via the Authority’s new Electronic Reporting (“E-Reporting”) System, which was launched in March 2007.