V. Overallotment Facility and Greenshoe

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Initial Public Offerings

November 2017 Initial Public Offerings An Issuer’s Guide (US Edition) Contents INTRODUCTION 1 What Are the Potential Benefits of Conducting an IPO? 1 What Are the Potential Costs and Other Potential Downsides of Conducting an IPO? 1 Is Your Company Ready for an IPO? 2 GETTING READY 3 Are Changes Needed in the Company’s Capital Structure or Relationships with Its Key Stockholders or Other Related Parties? 3 What Is the Right Corporate Governance Structure for the Company Post-IPO? 5 Are the Company’s Existing Financial Statements Suitable? 6 Are the Company’s Pre-IPO Equity Awards Problematic? 6 How Should Investor Relations Be Handled? 7 Which Securities Exchange to List On? 8 OFFER STRUCTURE 9 Offer Size 9 Primary vs. Secondary Shares 9 Allocation—Institutional vs. Retail 9 KEY DOCUMENTS 11 Registration Statement 11 Form 8-A – Exchange Act Registration Statement 19 Underwriting Agreement 20 Lock-Up Agreements 21 Legal Opinions and Negative Assurance Letters 22 Comfort Letters 22 Engagement Letter with the Underwriters 23 KEY PARTIES 24 Issuer 24 Selling Stockholders 24 Management of the Issuer 24 Auditors 24 Underwriters 24 Legal Advisers 25 Other Parties 25 i Initial Public Offerings THE IPO PROCESS 26 Organizational or “Kick-Off” Meeting 26 The Due Diligence Review 26 Drafting Responsibility and Drafting Sessions 27 Filing with the SEC, FINRA, a Securities Exchange and the State Securities Commissions 27 SEC Review 29 Book-Building and Roadshow 30 Price Determination 30 Allocation and Settlement or Closing 31 Publicity Considerations -

Registration Statement Under Securities Act of 1933

UNITED STATES SECURITIES AND EXCHANGE COMMISSION OMB APPROVAL OMB Number: 3235-0065 Washington, D.C. 20549 Expires: October 31, 2021 Estimated average burden FORM S-1 hours per response ............653.54 REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 (Exact name of registrant as specified in its charter) (State or other jurisdiction of incorporation or organization) (Primary Standard Industrial Classification Code Number) (I.R.S. Employer Identification Number) (Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices) (Name, address, including zip code, and telephone number, including area code, of agent for service) (Approximate date of commencement of proposed sale to the public) If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box: If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. -

Class Action Complaint

1 Laurence M. Rosen, Esq. (SBN 219683) THE ROSEN LAW FIRM, P.A. 2 FI fL tE B 355 South Grand Avenue, Suite 2450 . AN MATEO COUNTY Los Angeles, CA 90071 3 Telephone: (213) 785-2610 4 Facsimile: (213) 226-4684 Email: [email protected] 5 SARRAF GENTILE LLP 6 Ronen Sarraf . Joseph Gentile 7 14 Bond Street, Suite 212 8 Great Neck, New York (516) 699-8890 9 Attorneys for Plaintiffs 10 11 SUPERIOR COURT OF THE STATE OF CALIFORNIA 12 COUNTY OF SAN MATEO 18 e , v8 2 2 ~ 8 m 13 ~----------- OHNNY HOSEY and GEORGE SHILLIARE, ) Case No.: _______ -< 14 ndividually and on behalf of all others similarly ) 'T1 ituated, ) )> 15 ) CLASS ACTION COMPLAINT )< Plaintiffs, ) 16 ) s. ) 17 I I ) RICHARD 9,osTOLO, MIKE.,,PUPTA, LUCA ) DEMAND FOR JURY TRIAL 18 BARATTA, JACK DORSEY, BETER ) CHERNIN, :PETER CURRIE(I>ETER" ) 19 FENTON,1)AVIDROSENBLATT:'EVAN / ) ) 20 WJLLIAMS, GOLDMAN, SACHS & CO., -'/ ) MORGAN STANLEY & CO. LkC, J.P. 1/ I ) 21 MORGAN SECURITIES LLC,"TWITTER, ) /1~-CIV0;228 ... INC., MERRILL LYNCH, PIERCE, FENNER ) I CMP i Complaint Filed 22 & SMITH INCORPORATElt), DEUTSCHE ) BANK SECURITIES INC./ALLEN & ) 23 COMPANY LLC, and CODE ADVISORS LLC, ) ) ; 1i1111111111111111111rnm1 ~ 24 ) 25 26 27 28 COMPLAINT Plaintiffs Johnny Hosey ("Hosey") and George Shilliare ("Shilliare")( collectively 2 "Plaintiffs") make the following allegations, individually and on behalf of all others similarly 3 situated, based upon the investigation by Plaintiffs' counsel, which included among other things, an 4 analysis of publicly available news articles, reports, corporate webcasts with analysts, public filings 5 made with the Securities and Exchange Commission ("SEC"), and securities analysts' reports about 6 Twitter, Inc. -

Security Prospectus

Security Prospectus Issue of DX1S Token by DXone Ltd. ISIN LI0550102979 This Securities Prospectus was approved by the Liechtenstein Financial Market Authority on 18.06.2020 and is valid until 17.06.2021. In case of significant new factors, material mistakes or material inaccuracies the Issuer is obliged to establish a supplement to the Prospectus. The Issuers obligation to supplement a prospectus does not apply when a prospectus is no longer valid. 2 Index I. Summary .............................................................................................................................................. 5 Introduction and Warnings ............................................................................................................. 5 Key Information on the Issuer ........................................................................................................ 5 Key Information on the Securities .................................................................................................. 7 Key Information on the offer of the Notes to the Public .............................................................. 10 a) Offer Period ............................................................................................................................... 10 b) Conditions .................................................................................................................................. 10 c) Issue Price ................................................................................................................................. -

Stock in a Closely Held Corporation:Is It a Security for Uniform Commercial Code Purposes?

Vanderbilt Law Review Volume 42 Issue 2 Issue 2 - March 1989 Article 6 3-1989 Stock in a Closely Held Corporation:Is It a Security for Uniform Commercial Code Purposes? Tracy A. Powell Follow this and additional works at: https://scholarship.law.vanderbilt.edu/vlr Part of the Securities Law Commons Recommended Citation Tracy A. Powell, Stock in a Closely Held Corporation:Is It a Security for Uniform Commercial Code Purposes?, 42 Vanderbilt Law Review 579 (1989) Available at: https://scholarship.law.vanderbilt.edu/vlr/vol42/iss2/6 This Note is brought to you for free and open access by Scholarship@Vanderbilt Law. It has been accepted for inclusion in Vanderbilt Law Review by an authorized editor of Scholarship@Vanderbilt Law. For more information, please contact [email protected]. Stock in a Closely Held Corporation: Is It a Security for Uniform Commercial Code Purposes? I. INTRODUCTION ........................................ 579 II. JUDICIAL DECISIONS ................................... 582 A. The Blasingame Decision ......................... 582 B. Article 8 Generally .............................. 584 C. Cases Deciding Close Stock is Not a Security ...... 586 D. Cases Deciding Close Stock is a Security .......... 590 E. Problem Areas Created by a Decision that Close Stock is Not a Security .......................... 595 III. STATUTORY ANALYSIS .................................. 598 A. Statutory History ................................ 598 B. Official Comments to the U.C.C. .................. 599 1. In G eneral .................................. 599 2. Official Comments to Article 8 ................ 601 3. Interpreting the U.C.C. as a Whole ........... 603 IV. CONCLUSION .......................................... 605 I. INTRODUCTION The term security has many applications. No application, however, is more important than when an interest owned or traded is determined to be within the legal definition of security. -

PPD Initial Public Offering

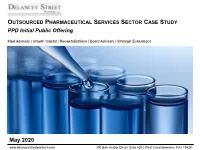

OUTSOURCED PHARMACEUTICAL SERVICES SECTOR CASE STUDY PPD Initial Public Offering M&A Advisory | Growth Capital | Recapitalizations | Board Advisory | Strategic Evaluations May 2020 www.delanceystreetpartners.com 300 Barr Harbor Drive | Suite 420 | West Conshohocken | PA | 19428 PPD INITIAL PUBLIC OFFERING Transaction Overview PPD (NASDAQ: PPD) Stock Price Performance $34.00 On February 5, 2020, Pharmaceutical Product $33.00 2/11/20 Closing Price: $32.87 Development (PPD) announced it raised $1.86 billion in its $32.00 initial public offering (IPO) $31.00 The company announced it priced 60 million primary shares of its common stock at the top end of its targeted range or $27.00 per share $30.00 2/6/20 Opening Price: $30.99 ‒ The underwriters simultaneously exercised the greenshoe option, $29.00 offering an additional 9 million primary shares of PPD’s common stock $28.00 at the IPO price, resulting in total IPO shares and gross proceeds of 69 million and $1.86 billion, respectively $27.00 3/6/20 Closing Price: $28.60 ‒ Implied Enterprise Value of $13.1 billion $26.00 ‒ Implied Enterprise Value / LTM Adjusted EBITDA multiple of 16.9x $25.00 PPD used the net proceeds from the offering to redeem a portion of its 5-Mar 1-Mar 2-Mar 3-Mar 4-Mar 6-Mar 7-Feb 8-Feb 9-Feb senior notes that were due to retire in 2022 and will use any remaining 6-Feb 11-Feb 10-Feb 12-Feb 13-Feb 14-Feb 15-Feb 16-Feb 17-Feb 18-Feb 19-Feb 20-Feb 21-Feb 22-Feb 23-Feb 24-Feb 25-Feb 26-Feb 27-Feb 28-Feb 29-Feb proceeds for general corporate purposes On February 6th, shares -

Base Prospectus

Base prospectus Final Terms for ISIN NO0010868318 Tomra Systems ASA FRN Senior Unsecured Open Bond Issue 2019/2022 Final Terms and the Base Prospectus dated 5 March 2020 together constitute the Base Prospectus for NO0010868318 Tomra Systems ASA FRN Senior Unsecured Open Bond Issue 2019/2022. The Base Prospectus contains complete information about the Issuer and the bond issue. The Base Prospectus is available on the Issuer's website https://www.tomra.com, or on the Issuer's visit address, Drengsrudhagen 2, 1385 Asker, or their successor (s). Asker/Oslo, 17 March 2020 Tomra Systems ASA Final Terms - Tomra Systems ASA FRN Senior Unsecured Open Bond Issue 2019/2022 ISIN NO0010868318 Terms used herein shall be deemed to be defined as such for the purposes of the conditions set forth in the Base Prospectus clause 2 Definition, 15.1.2 Definition and in the attached Bond Terms for each bond issue. Set out below is the form of Final Terms which will be completed for each bond issue which are issued under the Base Prospectus. MiFID II product governance / Retail investors, professional investors and ECPs target market – Solely for the purposes of each manufacturer’s product approval process, the target market assessment in respect of the notes has led to the conclusion that: (i) the target market for the notes is eligible counterparties, professional clients and retail clients each as defined in Directive 2014/65/EU (as amended, “MiFID II”); (ii) all channels for distribution to eligible counterparties and professional clients are appropriate; and (iii) the following channels for distribution of the notes to retail clients are appropriate – investment advice, portfolio management, non-advised sales and pure execution services – subject to the distributor’s suitability and appropriateness obligations under MiFID II, as applicable. -

Upsizing and Downsizing Your IPO

Upsizing and Downsizing Your IPO Posted by Charles M. Nathan, Latham & Watkins LLP, on Thursday July 29, 2010 Editor’s Note: Charles Nathan is Of Counsel at Latham & Watkins LLP and is co-chair of the firm’s Corporate Governance Task Force. This post is based on a Latham & Watkins Client Alert by Brian G. Cartwright, Alexander F. Cohen, Kirk A. Davenport and Joel H. Trotter. The reds have been printed; the deal is on the road; and the champagne is on ice. Now, all that is left is for the IPO investors to step up and buy the stock. It’s a tempting moment to relax — but an experienced deal lawyer knows better. This is the time to start preparing for the possibility that the deal will be wildly oversubscribed or will struggle mightily. In either case, the question that will shortly come your way is ―How much can the deal be upsized or downsized at pricing?‖ To answer that seemingly simple question, you will need to break it into three component parts: Was your registration statement accurate and complete as of the time it became effective? Have you provided investors with all the information they need to make an informed investment decision prior to confirming orders? Do you owe the SEC any additional filing fees? Getting to the bottom of these points is a surprisingly complex undertaking. The rules in this area are technical and not always intuitive, and you may be asked to make some difficult judgment calls under significant time pressure. The purpose of this Client Alert is to provide you with the tools you need to react quickly and wisely to questions about pricing outside the range when the moment of truth arrives. -

The Importance of the Capital Structure in Credit Investments: Why Being at the Top (In Loans) Is a Better Risk Position

Understanding the importance of the capital structure in credit investments: Why being at the top (in loans) is a better risk position Before making any investment decision, whether it’s in equity, fixed income or property it’s important to consider whether you are adequately compensated for the risks you are taking. Understanding where your investment sits in the capital structure will help you recognise the potential downside that could result in permanent loss of capital. Within a typical business there are various financing securities used to fund existing operations and growth. Most companies will use a combination of both debt and equity. The debt may come in different forms including senior secured loans and unsecured bonds, while equity typically comes as preference or ordinary shares. The exact combination of these instruments forms the company’s “capital structure”, and is usually designed to suit the underlying cash flows and assets of the business as well as investor and management risk appetites. The most fundamental aspect for debt investors in any capital structure is seniority and security in the capital structure which is reflected in the level of leverage and impacts the amount an investor should recover if a company fails to meet its financial obligations. Seniority refers to where an instrument ranks in priority of payment. Creditors (debt holders) normally have a legal right to be paid both interest and principal in priority to shareholders. Amongst creditors, “senior” creditors will be paid in priority to “junior” creditors. Security refers to a creditor’s right to take a “mortgage” or “lien” over property and other assets of a company in a default scenario. -

In Re Security Finance Co

University of California, Hastings College of the Law UC Hastings Scholarship Repository Opinions The onorH able Roger J. Traynor Collection 11-12-1957 In re Security Finance Co. Roger J. Traynor Follow this and additional works at: http://repository.uchastings.edu/traynor_opinions Recommended Citation Roger J. Traynor, In re Security Finance Co. 49 Cal.2d 370 (1957). Available at: http://repository.uchastings.edu/traynor_opinions/526 This Opinion is brought to you for free and open access by the The onorH able Roger J. Traynor Collection at UC Hastings Scholarship Repository. It has been accepted for inclusion in Opinions by an authorized administrator of UC Hastings Scholarship Repository. For more information, please contact [email protected]. 370 IN BE SECURITY FINANCE CO. [49 C.2d [So F. No. 19455. In Bank. Nov. 12, 1957.] In re SECURITY FINANCE COMPANY (a Corporation), in Process of Voluntary Winding Up. EARL R. ROUDA, Respondent, V. GEORGE N. CROCKER et at, Appellants. [1] Corporations-DissolutioD.-At common law a corporation had no power to end its existence; the shareholder.- could surrender the charter, but actual dissolution depended on acceptance by the sovereign. [2] ld.-Voluntary Dissolution-Judicial SupervisioD.-The su perior court has jurisdiction to supervise the dissolution of a corporation by virtue of Corp. Code, § 4607, only if the cor poration is "in the process of voluntary winding up," and the corporation is in the process of voluntary winding up only if a valid election to wind up has been made pursuant to § 4600. [3] 1d.-Volunta17 Dissolution-Rights of Shareholders.-Share holders representing 50 per cent of the voting power do not have an absolute right under Corp. -

United States

Equity Capital Markets 2006/07 Country Q&A United States United States Stephen Giove, Danielle Carbone and Ferdinand Erker, Shearman & Sterling LLP www.practicallaw.com/0-203-1882 EQUITY CAPITAL MARKETS: GENERAL Requirements for registration 1. Please give a brief overview of the equity market in your ju- Public offerings of securities must be registered under the risdiction. Has it been active? What were the large deals over Securities Act of 1933 (Securities Act). Registration is the past year? accomplished by publicly filing a registration statement with the SEC and the SEC declaring the registration statement effective. A registration statement contains two parts: Overall activity in the US equity markets has increased signif- icantly over the last several years. Although there were fewer ■ A prospectus, which is the main marketing document for the than 90 initial public offerings (IPOs) in 2003, there were offering (see Questions 8 to 12). more than 200 in each of 2004 and 2005. The aggregate value of IPOs has also increased significantly, from over ■ Other technical information that is made public but is not US$17 billion (about EUR13.5 billion) in 2003 to more than distributed to investors, including undertakings by the com- US$36 billion (about EUR28.5 billion) in 2005, although pany and exhibits. 2005 was down from more than US$46 billion (about EUR36.4 billion) offered in 2004. The results for the first half If the offered securities will be listed on an exchange, a separate of 2006 − over 100 completed IPOs with an aggregate value registration statement must be filed with the SEC under the of over US$20 billion (about EUR15.87 billion) − are slightly Securities Exchange Act of 1934 (Exchange Act). -

A Guide to Going

AST Business Cycle Momentum Series A GUIDE TO GOING PUBLIC AST is a leading provider of ownership data management, analytics and advisory services to public and private companies as well as mutual funds. AST’s comprehensive product set includes transfer agency services, employee stock plan administration services, proxy solicitation and advisory services and bankruptcy claims administration services. Read AST’s Thought Leadership Series: To, Through and Beyond the IPO. Visit AST’s IPO Content Library (lp.astfinancial.com/ipo-content-library2.html)with a dozen helpful articles for your reference before, during and after the IPO. 1 Table of Contents 1 Initial Public Offering Services 4 The Process 6 The IPO Timetable 10 After Going Public 12 Your First Annual Meeting 15 FAQs 17 Additional Ways AST Can Help 19 Corporate Governance Advisory and Proxy Solicitation Services Closed-End Fund IPO Services Equity Plan Solutions IPO Services Special Purpose Acquisition Company (SPAC) IPO Services Appendices 25 Direct Registration System (DRS) Frequently Asked Questions Sample Client Lock-up Release Reminder Sample Shareowner Lock-up Expiration Notice Sample Shareowner Lock-up Conversion Portal Notice Glossary 33 2 EVERY COMPANY BEGINS AS AN IDEA. When nurtured, that idea has the potential to grow into something big. Shifting from a privately held company to a public entity can be like moving from a calm country bike ride to the fast-paced streets of New York. Along even the greatest rides, you are bound to encounter rocky paths alongside the smooth roads of reward. At AST ®,we put great emphasis on helping navigate the full range of these transitional processes.