Global Insurance Industry Year in Review

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Post Event Report

presents 9th Asian Investment Summit Building better portfolios 21-22 May 2014, Ritz-Carlton, Hong Kong Post Event Report 310 delegates representing 190 companies across 18 countries www.AsianInvestmentSummit.com Thank You to our sponsors & partners AIWEEK Marquee Sponsors Co-Sponsors Associate Sponsors Workshop Sponsor Supporting Organisations alternative assets. intelligent data. Tech Handset Provider Education Partner Analytics Partner ® Media Partners Offical Broadcast Partner 1 www.AsianInvestmentSummit.com Delegate Breakdown 310 delegates representing 190 companies across 18 countries Breakdown by Organisation Institutional Investors 46% Haymarket Financial Media delegate attendee data is Asset Managemer 19% independently verified by the BPA Consultant 8% Fund Distributor / Private Wealth Management 5% Media & Publishing 4% Commercial Bank 4% Index / Trading Platform Provider 3% Association 2% Other 9% Breakdown of Institutional Investors Insurance 31% Endowment / Foundation 27% Corporation 13% Pension Fund 13% Family Office 8% Breakdown by Country Sovereign Wealth Fund 6% PE Funds of Funds 1% Mulitlateral Finance Hong Kong 82% Institution 1% ASEAN 10% North Asia 5% Australia 1% Europe 1% North America 1% Breakdown by Job Function Investment 34% Finance / Treasury 20% Marketing and Investor Relations 19% Other 11% CEO / Managing Director 7% Fund Selection / Distribution 7% Strategist / Economist 2% 2 www.AsianInvestmentSummit.com Participating Companies Haymarket Financial Media delegate attendee data is independently verified by the BPA 310 institutonal investors, asset managers, corporates, bankers and advisors attended the Forum. Attending companies included: ACE Life Insurance CFA Institute Board of Governors ACMI China Automation Group Limited Ageas China BOCOM Insurance Co., Ltd. Ageas Hong Kong China Construction Bank Head Office Ageas Insurance Company (Asia) Limited China Life Insurance AIA Chinese YMCA of Hong Kong AIA Group CIC AIA International Limited CIC International (HK) AIA Pension and Trustee Co. -

Allianz Se Allianz Finance Ii B.V. Allianz

2nd Supplement pursuant to Art. 16(1) of Directive 2003/71/EC, as amended (the "Prospectus Directive") and Art. 13 (1) of the Luxembourg Act (the "Luxembourg Act") relating to prospectuses for securities (loi relative aux prospectus pour valeurs mobilières) dated 12 August 2016 (the "Supplement") to the Base Prospectus dated 2 May 2016, as supplemented by the 1st Supplement dated 24 May 2016 (the "Prospectus") with respect to ALLIANZ SE (incorporated as a European Company (Societas Europaea – SE) in Munich, Germany) ALLIANZ FINANCE II B.V. (incorporated with limited liability in Amsterdam, The Netherlands) ALLIANZ FINANCE III B.V. (incorporated with limited liability in Amsterdam, The Netherlands) € 25,000,000,000 Debt Issuance Programme guaranteed by ALLIANZ SE This Supplement has been approved by the Commission de Surveillance du Secteur Financier (the "CSSF") of the Grand Duchy of Luxembourg in its capacity as competent authority (the "Competent Authority") under the Luxembourg Act for the purposes of the Prospectus Directive. The Issuer may request the CSSF in its capacity as competent authority under the Luxemburg Act to provide competent authorities in host Member States within the European Economic Area with a certificate of approval attesting that the Supplement has been drawn up in accordance with the Luxembourg Act which implements the Prospectus Directive into Luxembourg law ("Notification"). Right to withdraw In accordance with Article 13 paragraph 2 of the Luxembourg Act, investors who have already agreed to purchase or subscribe for the securities before the Supplement is published have the right, exercisable within two working days after the publication of this Supplement, to withdraw their acceptances, provided that the new factor arose before the final closing of the offer to the public and the delivery of the securities. -

International Rating Agency Advisory Newsletter November 2012 Update Welcome to Aon Benfield’S Updated Rating Agency Advisory Newsletter

International Rating Agency Advisory Newsletter November 2012 Update Welcome to Aon Benfield’s updated Rating Agency Advisory Newsletter. In this edition, matters of interest include rating agencies global reinsurance and country risk outlooks, as well as our regular features on : Selected regulatory activities or updates throughout APAC and EMEA. List of rating actions in APAC and EMEA during the 3rd quarter. Links to reports released by Aon Benfield Analytics. We will continuously scan for new content to provide greater value to our clients. We will be glad to hear your feedback so that we can continue to provide the most relevant ratings news and information in future editions. Rating Agency Activity (Data source: Standard & Poor’s, A.M.Best, Fitch, and Moody’s) Standard & Poor’s Numerous market participants provided feedback on S&P’s proposed criteria for rating insurers, “Request for Comment: Insurers Rating Methodology”, published 9 July 2012. S&P has stated in its recent report “S&P Summarizes Submissions On Request For Comments” on 18 October 2012 that it received formal feedback from about 100 market participants, varying from rated insurers, insurance brokers, rating advisors, and industry trade associations. S&P is not yet in a position to comment on the final criteria. However S&P expects to respond to the comments in one of three ways: by changing the proposed criteria, by explaining the original proposals more clearly to remove ambiguity, or by leaving the proposal unchanged. S&P states that it is in the process of analyzing the feedback and testing the impact of various alternatives. -

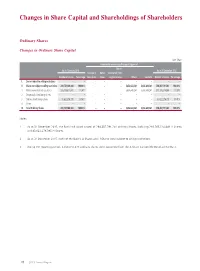

Changes in Share Capital and Shareholdings of Shareholders

Changes in Share Capital and Shareholdings of Shareholders Ordinary Shares Changes in Ordinary Share Capital Unit: Share Increase/decrease during the reporting period Shares As at 1 January 2015 As at 31 December 2015 Issuance of Bonus transferred from Number of shares Percentage new shares shares surplus reserve Others Sub-total Number of shares Percentage I. Shares subject to selling restrictions – – – – – – – – – II. Shares not subject to selling restrictions 288,731,148,000 100.00% – – – 5,656,643,241 5,656,643,241 294,387,791,241 100.00% 1. RMB-denominated ordinary shares 205,108,871,605 71.04% – – – 5,656,643,241 5,656,643,241 210,765,514,846 71.59% 2. Domestically listed foreign shares – – – – – – – – – 3. Overseas listed foreign shares 83,622,276,395 28.96% – – – – – 83,622,276,395 28.41% 4. Others – – – – – – – – – III. Total Ordinary Shares 288,731,148,000 100.00% – – – 5,656,643,241 5,656,643,241 294,387,791,241 100.00% Notes: 1 As at 31 December 2015, the Bank had issued a total of 294,387,791,241 ordinary shares, including 210,765,514,846 A Shares and 83,622,276,395 H Shares. 2 As at 31 December 2015, none of the Bank’s A Shares and H Shares were subject to selling restrictions. 3 During the reporting period, 5,656,643,241 ordinary shares were converted from the A-Share Convertible Bonds of the Bank. 79 2015 Annual Report Changes in Share Capital and Shareholdings of Shareholders Number of Ordinary Shareholders and Shareholdings Number of ordinary shareholders as at 31 December 2015: 963,786 (including 761,073 A-Share Holders and 202,713 H-Share Holders) Number of ordinary shareholders as at the end of the last month before the disclosure of this report: 992,136 (including 789,535 A-Share Holders and 202,601 H-Share Holders) Top ten ordinary shareholders as at 31 December 2015: Unit: Share Number of Changes shares held as Percentage Number of Number of during at the end of of total shares subject shares Type of the reporting the reporting ordinary to selling pledged ordinary No. -

Global Insurance Stock Review

GLOBAL INSURANCE STOCK REVIEW GLOBAL INSURANCE STOCK REVIEW: RETURNS BY SECTOR* *Weighted Return FIRST HALF 2019 MSCI ACWI IMI 15.38% These are exciting times for holders of insurance stocks, whether institutional investors or insurance Insurance 20.14% executives themselves. Approximately 70% of the P&C 16.41% world’s insurance premiums are written by stockholder-owned insurers, so rising share prices L&H 21.18% provides added financial security to all stakeholders in the insurance value chain. Multi-line 21.56% Global stocks continued their bull run in the Reinsurance 15.79% second quarter of 2019, so that for the first half of the year the Morgan Stanley All Countries World Brokers 28.68% Index rose 15% to a record high. Insurance stocks 0% 5% 10% 15% 20% 25% 30% 35% not only participated in the broad gain, as they did in the first quarter, but substantially outperformed RETURNS BY MARKET CAP in the second stanza. The IIS global insurance stock aggregate thus gained a robust 20% for the Small 5.15% half year, with market-beating advances in every industry sector. Small/Medium 12.76% Medium 19.83% Insurance Brokers continued their performance Medium/Large 19.45% dominance, climbing 27%. While mainstream brokers performed reasonably well, the stars were Large 8.09% niche specialists. EHealth rocketed 124%, as the 0% 5% 10% 15% 20% 25% web portal/online marketplace for US government Medicare, Medigap and Medicare supplement RETURNS BY MARKET TYPE plans saw its revenues soar. Brazilian broker Wiz Solutions jumped 79%, and controversial Chinese US 15.57% broker Fanhua gained 55% to lead the sector. -

AIA Group (1299 HK) INSURANCE

27 June 2016 EQUITIES AIA Group (1299 HK) INSURANCE Buy: Our conviction still high after examining bear case Hong Kong AIA is our most preferred Asian insurance stock; the ultimate MAINTAIN BUY ‘compounder’ for a quality-biased investor TARGET PRICE (HKD) PREVIOUS TARGET (HKD) We are even more positive on AIA after examining the 10 56.00 54.00 main bear arguments SHARE PRICE (HKD) UPSIDE/DOWNSIDE Reiterate Buy, raise target price to HKD56 (from HKD54), 45.50 +23.1% implying 23% potential share price upside (as of 22 Jun 2016) MARKET DATA AIA is our most preferred Asian insurance stock. We regard AIA as the ultimate Market cap (HKDm) 542,225 Free float 100% ‘compounder’ stock for a quality-biased investor in the high growth potential Asian Market cap (USDm) 69,880 BBG 1299 HK 3m ADTV (USDm) 121 RIC 1299.HK insurance sector where shareholder returns are not always prioritized (they are at AIA). We have a high conviction Buy rating on AIA for many reasons, not least its FINANCIALS AND RATIOS (HKD) Year to 11/2015a 11/2016e 11/2017e 11/2018e defensive qualities, growth outlook, management quality, high free cash flow generation, IFRS EPS 1.81 2.13 2.91 3.20 attractive valuation (with catalysts), diversified country exposure, conservative risk IFRS EPS (prev) - 2.35 3.04 3.44 Change (%) - -9.6 -4.3 -7.0 management and focused Asian life strategy. Although AIA shares have outperformed Consensus EPS - 2.29 2.79 3.07 the Asian insurance sector by a notable 74% since listing on 29 October 2010 and PE (x) 25.1 21.4 15.6 14.2 Dividend yield (%) 1.5 1.7 2.0 2.2 18% over the past 12 months, we believe AIA shares should have delivered more were it not for several niggling bear concerns, which we address in this report. -

Allianz Se Allianz Finance Ii B.V

3rd Supplement pursuant to Art. 16(1) of Directive 2003/71/EC, as amended (the "Prospectus Directive") and Art. 13 (1) of the Luxembourg Act (the "Luxembourg Act") relating to prospectuses for securities (loi relative aux prospectus pour valeurs mobilières) dated 25 November 2016 (the "Supplement") to the Base Prospectus dated 2 May 2016, as supplemented by the 1st Supplement dated 24 May 2016 and the 2nd Supplement dated 12 August 2016 (the "Prospectus") with respect to ALLIANZ SE (incorporated as a European Company (Societas Europaea – SE) in Munich, Germany) ALLIANZ FINANCE II B.V. (incorporated with limited liability in Amsterdam, The Netherlands) ALLIANZ FINANCE III B.V. (incorporated with limited liability in Amsterdam, The Netherlands) € 25,000,000,000 Debt Issuance Programme guaranteed by ALLIANZ SE This Supplement has been approved by the Commission de Surveillance du Secteur Financier (the "CSSF") of the Grand Duchy of Luxembourg in its capacity as competent authority (the "Competent Authority") under the Luxembourg Act for the purposes of the Prospectus Directive. The Issuer may request the CSSF in its capacity as competent authority under the Luxemburg Act to provide competent authorities in host Member States within the European Economic Area with a certificate of approval attesting that the Supplement has been drawn up in accordance with the Luxembourg Act which implements the Prospectus Directive into Luxembourg law ("Notification"). Right to withdraw In accordance with Article 13 paragraph 2 of the Luxembourg Act, investors who have already agreed to purchase or subscribe for the securities before the Supplement is published have the right, exercisable within two working days after the publication of this Supplement, to withdraw their acceptances, provided that the new factor arose before the final closing of the offer to the public and the delivery of the securities. -

© 2020 Thomson Reuters. No Claim to Original U.S. Government Works. 1 AB STABLE VIII LLC, Plaintiff/Counterclaim-Defendant, V...., Not Reported in Atl

AB STABLE VIII LLC, Plaintiff/Counterclaim-Defendant, v...., Not Reported in Atl.... 2020 WL 7024929 Only the Westlaw citation is currently available. MEMORANDUM OPINION UNPUBLISHED OPINION. CHECK *1 AB Stable VIII LLC (“Seller”) is an indirect subsidiary COURT RULES BEFORE CITING. of Dajia Insurance Group, Ltd. (“Dajia”), a corporation organized under the law of the People's Republic of China. Court of Chancery of Delaware. Dajia is the successor to Anbang Insurance Group., Ltd. (“Anbang”), which was also a corporation organized under AB STABLE VIII LLC, Plaintiff/ the law of the People's Republic of China. For simplicity, Counterclaim-Defendant, and because Anbang was the pertinent entity for much of v. the relevant period, this decision refers to both companies as MAPS HOTELS AND RESORTS ONE LLC, “Anbang.” MIRAE ASSET CAPITAL CO., LTD., MIRAE ASSET DAEWOO CO., LTD., MIRAE ASSET Through Seller, Anbang owns all of the member interests in GLOBAL INVESTMENTS, CO., LTD., and Strategic Hotels & Resorts LLC (“Strategic,” “SHR,” or the MIRAE ASSET LIFE INSURANCE CO., “Company”), a Delaware limited liability company. Strategic in turn owns all of the member interests in fifteen limited LTD., Defendants/Counterclaim-Plaintiffs. liability companies, each of which owns a luxury hotel. C.A. No. 2020-0310-JTL | Under a Sale and Purchase Agreement dated September 10, Date Submitted: October 28, 2020 2019 (the “Sale Agreement” or “SA”), Seller agreed to sell | all of the member interests in Strategic to MAPS Hotel and Date Decided: November 30, 2020 Resorts One LLC (“Buyer”) for a total purchase price of $5.8 billion (the “Transaction”). -

Key Actuarial Employers in Hong Kong – 2020

KEY ACTUARIAL EMPLOYERS IN HONG KONG – 2020 A.M. Best Asia-Pacific Ltd Suite 4004, Central Plaza, 18 Harbour Road, Wanchai, Hong Kong Tel: (852) 2827 3400 Website: http://www.ambest.com/about/ http://www.ambest.com/careers/index.html Accenture Suites 4103-10, 41/F One Island East, Taikoo Place, 18 Westlands Road, Quarry Bay, Hong Kong Tel: (852) 2850 8956 Website: https://www.accenture.com/hk-en https://www.accenture.com/hk-en/careers/jobsearch?jk=&sb=1 Actuarial Group 35/F Central Plaza, 18 Harbour Road, Wanchai, Hong Kong Tel: (852) 3960 6576 Website: https://www.actuarial.pt/ https://actuarial.pt/ing/recrutamento.php Aegon Insights Suites 5705-5708, One Island East, 18 Westlands Road, Island East, Hong Kong Tel: (852) 3655 8228 Website: https://www.aegon.com/home/ https://careers.aegon.com/en/vacancies/?page=1&query=&Countries=Countries-Hong-Kong Ageas Insurance Company (Asia) Limited 27/F, Cambridge House, Taikoo Place, 979 King's Road, Quarry Bay, Hong Kong Tel: (852) 2126 2280 Website: https://www.ageas.com/ https://www.ageas.com/careers AIA Company Limited 18/F, AIA Hong Kong Tower, 734 King's Road, Quarry Bay, Hong Kong Tel: (852) 2832 8888 Website: https://www.aia.com.hk/zh-hk/index.html https://www.aia.com.hk/en/about-aia/careers.html AIA Group 30/F, Hopewell Center, 183 Queen's Road East, Wanchai, Hong Kong Tel: (852) 2832 1800 Website: https://www.aia.com/en/index.html https://www.aia.com/en/careers.html AIG 7/F, One Island East, 18 Westlands Road, Island East, Hong Kong Tel: (852) 3555 0000 Website: https://www.aig.com.hk/ -

2016 Sidley Global Insurance Review

OFFICES BEIJING DALLAS LOS ANGELES SINGAPORE Suite 608, Tower C2 2001 Ross Avenue 555 West Fifth Street Level 31 Oriental Plaza Suite 3600 Los Angeles, California 90013 Six Battery Road No. 1 East Chang An Avenue Dallas, Texas 75201 +1 213 896 6000 Singapore 049909 Dong Cheng District +1 214 981 3300 +65 6230 3900 Beijing 100738, China NEW YORK +86 10 5905 5588 GENEVA 787 Seventh Avenue SYDNEY Rue du Pré-de-la-Bichette 1 New York, New York 10019 Level 10, 7 Macquarie Place BOSTON 1202 Geneva, Switzerland +1 212 839 5300 Sydney NSW 2000, Australia 60 State Street +41 22 308 00 00 +61 2 8214 2200 36th Floor PALO ALTO Boston, Massachusetts 02109 HONG KONG 1001 Page Mill Road TOKYO +1 617 223 0300 39/F, Two Int’l Finance Centre Building 1 Sidley Austin Nishikawa Central, Hong Kong Palo Alto, California 94304 Foreign Law Joint Enterprise BRUSSELS +852 2509 7888 +1 650 565 7000 Marunouchi Building 23F NEO Building 4-1, Marunouchi 2-chome Rue Montoyer 51 HOUSTON SAN FRANCISCO Chiyoda-Ku, Tokyo 100-6323, Japan Montoyerstraat 1000 Louisiana Street 555 California Street +81 3 3218 5900 B-1000 Brussels, Belgium Suite 6000 Suite 2000 +32 2 504 6400 Houston, Texas 77002 San Francisco, California 94104 WASHINGTON, D.C. March 2016 +1 713 495 4500 +1 415 772 1200 CENTURY CITY 1501 K Street N.W. Washington, D.C. 20005 1999 Avenue of the Stars LONDON SHANGHAI +1 202 736 8000 SIDLEY GLOBAL Los Angeles, California 90067 Woolgate Exchange Suite 2009 +1 310 595 9500 25 Basinghall Street 5 Corporate Avenue London, EC2V 5HA, United Kingdom 150 Hubin Road INSURANCE REVIEW CHICAGO +44 20 7360 3600 Shanghai 200021, China One South Dearborn +86 21 2322 9322 Chicago, Illinois 60603 +1 312 853 7000 sidley.com AMERICA • ASIA PACIFIC • EUROPE Attorney Advertising - For purposes of compliance with New York State Bar rules, our headquarters are Sidley Austin LLP, 787 Seventh Avenue, New York, NY 10019, 212 839 5300; One South Dearborn, Chicago, IL 60603, 312 853 7000; and 1501 K Street, N.W., Washington, D.C. -

Asian Insurance Industry 2020

PRODUCT DETAILS Included with Purchase y Asian Insurance Industry 2020 y Digital report in PDF format Key findings Knowing Your Insurance Clients y Unlimited online firm-wide access y Analyst support y Exhibits in Excel y Interactive Report Dashboards OVERVIEW & METHODOLOGY This report analyzes Asia’s life insurance industry through the asset management lens. It Interactive Report provides both qualitative and quantitative information, including life insurance assets and Dashboards premiums, asset allocations, investment practices, and outsourcing trends. The report discusses Interact and explore select both institutional (general account) and retail (separate account or investment-linked product) report data with Cerulli’s segments, and covers China, Taiwan, Hong Kong, Korea, Singapore, Malaysia, Thailand, visualization tool. and Indonesia. The report also details key factors that influence insurers’ investments, such as regulations, asset-liability management, products, distribution landscapes, and other key developments. In addition to covering two region-wide themes on insurtech for distribution and investments y Asian Insurance Investment Landscape: in the low-interest-rate-environment, the report provides in-depth analysis of Asia ex-Japan y Review five years of historical life insurance premiums, assets, and insurance markets, capturing trends in both chart and text forms. investable assets in Asia ex-Japan by region and country, and view growth rates by asset type. USE THIS REPORT TO y Analyze the marketshare of life insurance -

2019 Insurance Fact Book

2019 Insurance Fact Book TO THE READER Imagine a world without insurance. Some might say, “So what?” or “Yes to that!” when reading the sentence above. And that’s understandable, given that often the best experience one can have with insurance is not to receive the benefits of the product at all, after a disaster or other loss. And others—who already have some understanding or even appreciation for insurance—might say it provides protection against financial aspects of a premature death, injury, loss of property, loss of earning power, legal liability or other unexpected expenses. All that is true. We are the financial first responders. But there is so much more. Insurance drives economic growth. It provides stability against risks. It encourages resilience. Recent disasters have demonstrated the vital role the industry plays in recovery—and that without insurance, the impact on individuals, businesses and communities can be devastating. As insurers, we know that even with all that we protect now, the coverage gap is still too big. We want to close that gap. That desire is reflected in changes to this year’s Insurance Information Institute (I.I.I.)Insurance Fact Book. We have added new information on coastal storm surge risk and hail as well as reinsurance and the growing problem of marijuana and impaired driving. We have updated the section on litigiousness to include tort costs and compensation by state, and assignment of benefits litigation, a growing problem in Florida. As always, the book provides valuable information on: • World and U.S. catastrophes • Property/casualty and life/health insurance results and investments • Personal expenditures on auto and homeowners insurance • Major types of insurance losses, including vehicle accidents, homeowners claims, crime and workplace accidents • State auto insurance laws The I.I.I.