FTA Television Double-Digit Growth in Streams Across Stan Across All Platforms and BVOD, and Improving Trends in and 9Now Publishing and Radio

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Full Year Statutory Accounts

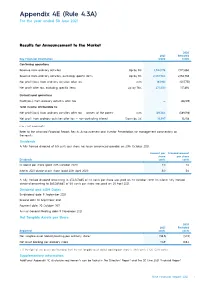

Appendix 4E (Rule 4.3A) For the year ended 30 June 2021 Results for Announcement to the Market 2020 2021 Restated Key Financial Information $’000 $’000 Continuing operations Revenue from ordinary activities Up by 8% 2,342,178 2,172,060 Revenue from ordinary activities, excluding specific items Up by 8% 2,332,984 2,156,785 Net profit/(loss) from ordinary activities after tax n/m 183,961 (507,751) Net profit after tax, excluding specific items Up by 76% 277,530 157,694 Discontinued operations Profit/(loss) from ordinary activities after tax — (66,189) Total income attributable to: Net profit/(loss) from ordinary activities after tax — owners of the parent n/m 169,364 (589,198) Net profit from ordinary activities after tax — non-controlling interest Down by 4% 14,597 15,258 n/m = not meaningful Refer to the attached Financial Report, Results Announcement and Investor Presentation for management commentary on the results. Dividends A fully franked dividend of 5.5 cents per share has been announced payable on 20th October 2021. Amount per Franked amount share per share Dividends cents cents Dividend per share (paid 20th October 2020) 2.0 2.0 Interim 2021 dividend per share (paid 20th April 2021) 5.0 5.0 A fully franked dividend amounting to $34,107,865 of 2.0 cents per share was paid on 20 October 2020. An interim fully franked dividend amounting to $85,269,663 of 5.0 cents per share was paid on 20 April 2021. Dividend and AGM Dates Ex-dividend date: 9 September 2021 Record date: 10 September 2021 Payment date: 20 October 2021 Annual General Meeting date: 11 November 2021 Net Tangible Assets per Share 2020 2021 Restated Reported cents cents Net tangible asset (deficit)/backing per ordinary share 1 (38.3) (40.9) Net asset backing per ordinary share 114.9 108.4 1. -

Week 03 2021 (27/12 - 16/01) 06:00 - 23:59 Total Individuals - Including Guests

Consolidated Metropolitan Total TV Share of All Viewing 5 City Share Report - All Homes Week 01 - Week 03 2021 (27/12 - 16/01) 06:00 - 23:59 Total Individuals - including Guests ABC SBS ABC ABC ABC ABC Seven Nine 10 10 10 10 SBS SBS SBS Total Total Network Share % Kids/ABC Seven 7TWO 7mate 7flix Nine GO! Gem 9Life 9Rush 10 SBS NITV World TV ME NEWS NET NET NET Bold Peach Shake NET VICELAND Food NET FTA STV TV Plus Movies Wk01-06 Wk01 (27/12) 7.7 4.1 0.8 3.9 16.5 18.6 2.2 2.2 0.9 24.0 12.4 1.5 1.7 2.1 1.4 19.2 5.5 2.7 2.1 0.5 10.9 3.2 0.8 0.9 0.1 0.8 5.9 78.7 21.3 Wk02 (03/01) 7.3 3.6 0.8 4.8 16.5 17.5 2.1 2.3 0.9 22.8 12.2 1.4 1.8 1.9 1.3 18.5 9.2 2.5 1.9 0.6 14.1 3.2 0.8 0.9 0.1 0.7 5.7 80.0 20.0 Wk03 (10/01) 7.2 3.8 0.8 3.8 15.6 19.4 2.1 2.2 1.0 24.6 12.0 1.5 1.7 1.9 1.2 18.2 8.6 2.6 2.0 0.6 13.8 3.3 0.8 0.9 0.1 0.7 5.9 80.5 19.5 Wk04 (17/01) Wk05 (24/01) Wk06 (31/01) Share Data for Progressive, Total and Year To Date figures excludes Easter - Wk14 (28/03/2021) and Wk15 (04/04/2021) Consolidated Metropolitan Total TV Share of All Viewing Sydney Share Report - All Homes Week 01 - Week 03 2021 (27/12 - 16/01) 06:00 - 23:59 Total Individuals - including Guests ABC SBS ABC ABC ABC ABC Seven Nine 10 10 10 10 SBS SBS SBS Total Total Network Share % Kids/ABC Seven 7TWO 7mate 7flix Nine GO! Gem 9Life 9Rush 10 SBS NITV World TV ME NEWS NET NET NET Bold Peach Shake NET VICELAND Food NET FTA STV TV Plus Movies Wk01-06 Wk01 (27/12) 8.5 3.5 0.7 4.0 16.8 17.3 1.7 1.8 0.8 21.5 13.5 1.2 1.5 1.4 1.6 19.1 5.4 2.7 1.9 0.4 10.4 3.2 0.7 0.7 0.2 0.6 5.4 76.0 24.0 Wk02 (03/01) 7.1 3.3 0.6 4.6 15.6 17.5 1.8 1.9 0.9 22.1 13.0 1.4 1.7 1.3 1.4 18.7 8.6 2.5 1.8 0.5 13.4 3.2 0.8 0.8 0.1 0.7 5.5 78.3 21.7 Wk03 (10/01) 6.8 3.2 0.7 3.4 14.2 18.5 1.6 1.9 1.0 23.0 13.1 1.2 1.6 1.3 1.2 18.4 8.3 2.9 2.1 0.7 14.0 3.5 0.7 0.8 0.1 0.8 5.9 78.1 21.9 Wk04 (17/01) Wk05 (24/01) Wk06 (31/01) Share Data for Progressive, Total and Year To Date figures excludes Easter - Wk14 (28/03/2021) and Wk15 (04/04/2021) Data © OzTAM Pty Limited 2020. -

Presentation to Macquarie Conference

4 May 2021 ASX Markets Announcements Office ASX Limited 20 Bridge Street Sydney NSW 2000 PRESENTATION TO MACQUARIE CONFERENCE 4 May 2021: Attached is a copy of Nine’s presentation to the Macquarie Australia Conference 2021. Authorised for lodgment by Mike Sneesby, Chief Executive Officer. Further information: Nola Hodgson Victoria Buchan Head of Investor Relations Director of Communications +61 2 9965 2306 +61 2 9965 2296 [email protected] [email protected] nineforbrands.com.au Nine Sydney - 1 Denison Street, North Sydney, NSW, 2060 ABN 60 122 203 892 MIKE SNEESBY | CHIEF EXECUTIVE OFFICER Important Notice and Disclaimer as a result of reliance on this document. as a general guide only, and should not be relied on This document is a presentation of general as an indication or guarantee of future performance. background information about the activities of Nine Forward Looking Statements Forward looking statements involve known and unknown risks, uncertainty and other factors which Entertainment Co. Holdings Limited (“NEC”) current This document contains certain forward looking can cause NEC’s actual results to differ materially at the date of the presentation, (4 May 2021). The statements and comments about future events, from the plans, objectives, expectations, estimates information contained in this presentation is of including NEC’s expectations about the performance and intentions expressed in such forward looking general background and does not purport to be of its businesses. Forward looking statements can statements and many of these factors are outside complete. It is not intended to be relied upon as generally be identified by the use of forward looking the control of NEC. -

Streaming Yujin Luo Final

The Streaming War During the Covid-19 Pandemic Yujin Luo The Streaming War During the Covid-19 Pandemic 2 home, which is the ideal condition for The Covid-19 pandemic has drastically binge-watching. disrupted all business sectors. The arts, culture, and entertainment industries have To understand how the pandemic is shaping been hit exceptionally hard since the virus’ the streaming industry, it is important to first outbreak in January. In response to the understand its pre-Covid and current status. crisis, businesses have taken immediate The following analysis will divide the actions: transitioning to remote work, timeline into before 2020 and in 2020 based canceling and postponing live events on Covid-19’s first outbreak in January nationwide, shutting down entertainment 2020. venues, etc., resulting in lost revenues from sales, merchandising, advertising, and The Streaming Industry’s Pre-Covid promotions. Unfortunately, the Covid-19 State of the Major Players in the pandemic’s impacts are far more Streaming War permanent for an audience-oriented industry that requires a high level of Early adopters and fast followers used to be engagement. The business model might be the main audiences of streaming services, fundamentally changed and there will or in other words, streaming used to be a certainly be a shift in how content is niche add-on to traditional TV. Now, it is produced and consumed. transitioning to a new stage as a mainstream element in the entertainment While lockdowns and social distancing industry. The major streaming services from measures to contain the pandemic have before Covid are shown in the table below, had a huge impact on the traditional movie except for HBO Max, Peacock, and Quibi industry, the video streaming model seems (RIP) that just launched in 2020. -

Timber Lines

TIMBER LINES S VOL. VIII JUNE 19 THIRTY-YEAR CLUB R-6 FOREST SERVICE V TIMBER LINES NO. VIII - PUBLISHED NOW MD THEN 13Y R-6 THIRTY-YEAR CLUB - JUNEl9SL When things go wrong, as they sometimes will, When the road you're trudging seenis all up hill, Whe funds are low and the debts are high And you want to smile, but you have to sigh When care is pressing you doun a bit, Rest, if you must - but don't you quit. Success Is failure turned inside out, The silver tint on the clouds of doubt, And you never can tell how cl6se you are, It may be near when it seems afar; 'So stick to the fight when you're hardest hit - It'swhenthings seem worst that you niust'nt. quit.. Anonymous S .. :.:THE PURPOSE OF TIER LINES To provide a means of keeping the clib informed on matters of common interest, to provide a nidiuzn of communication between members, to assist in making real the objectives of our constitution arid to' provide a bridge to span the gap between membersinretirement arid those stillin active service. To these things we dedicate Timber Lines. Editor Ny greetings to the 30-Year Club with some notes of major happenings in F.Y. 1951i. The past year has been a busy one for Region Six. That's not new. There has never been a year since the Region was formed that has not been a busy one..This year our timber cut is up slightly. It is close to 2billionfeet, although prices are down and our receipts will be less than last year. -

SI Allocations

Free TV Australia DTTB SI Register Transport Stream Service Information for Television Market Area All values are hexadecimal Issue 15 Date: October 2020 Western Australia Tasmania Northern Territory Remote Remote Queensland, Mandurah (Turner NSW, Vic, SA, Tas Perth Bunbury Albany Remote Hobart Launceston Darwin Alice Springs Northern Territory Hill) (See Note 3) (See Notes 1 and 2) (See notes 1 and 2) LCN Broadcaster Service Name SID SID SID SID SID SID SID SID SID SID SID NID NID NID NID NID NID NID NID NID NID NID TSID TSID TSID TSID TSID TSID TSID TSID TSID TSID TSID ONID ONID ONID ONID ONID ONID ONID ONID ONID ONID (dec) ONID 3201 3239 0261 1010 3256 0263 1010 3256 0263 1010 3256 0263 1010 3256 0263 1010 325B 0271 1010 3257 0273 1010 325C 0281 1010 325B 0283 ABC1 2 02E1 02E1 02E1 02E1 02E1 0271 0291 0281 02F1 ABC News 24 24 02E0 02E0 02E0 02E0 02E0 0270 0290 0280 02F0 ABC ABC1 21 02E3 02E3 02E3 02E3 02E3 0273 0293 0283 02F3 ABC2 / ABC4 22 02E2 02E2 02E2 02E2 02E2 0272 0292 0282 02F2 ABC3 23 02E4 02E4 02E4 02E4 02E4 0274 0294 0284 02F4 ABC Dig Music 200 02E6 02E6 02E6 02E6 02E6 0276 0296 0286 02F6 ABC Jazz 201 02E7 02E7 02E7 02E7 02E7 0277 0297 0287 02F7 3202 3202 0320 3202 3202 03A0 3202 3202 03A0 3202 3202 03A0 3202 3202 03A0 3202 3202 0380 3202 3202 0380 3202 3202 0360 SBS ONE 3 0321 03A1 03A1 03A1 03A1 0381 0381 0361 SBS ONE HD 30 0325 03A5 03A5 03A5 03A5 0385 0385 0365 SBS VICELAND HD 31 0326 03A6 03A6 03A6 03A6 0386 0386 0366 SBS World Movies 32 0327 03A7 03A7 03A7 03A7 0387 0387 0367 SBS Food 33 0323 03A3 03A3 03A3 03A3 0383 -

AUSTRALIAN PODCAST RANKER TOP 100 PODCASTS Reporting Period: 25 November - 22 December

AUSTRALIAN PODCAST RANKER TOP 100 PODCASTS Reporting Period: 25 November - 22 December RANK PODCAST PUBLISHER SALES REPRESENTATION RANK CHANGE 1 Hamish & Andy SCA-PodcastOne Australia PodcastOne Australia 0 2 The Lighthouse News Corp Australia News Corp / Nova Ent h5 3 Kate, Tim & Marty Nova Nova Entertainment 0 4 7am Schwartz Media Schwartz Media New 5 The Kyle & Jackie O Show Australian Radio Network Australian Radio Network i3 6 Life and Crimes with Andrew Rule News Corp Australia News Corp / Nova Ent h2 7 SEN Breakfast SEN / Crocmedia SEN / Crocmedia i2 8 Whateley SEN / Crocmedia SEN / Crocmedia i4 9 Sky News - News Bulletin News Corp Australia News Corp / Nova Ent h5 10 WILOSOPHY with Wil Anderson TOFOP Productions Whooshkaa New 11 Money News with Ross Greenwood Nine Radio1 Nine Radio i5 12 The Alan Jones Breakfast Show Nine Radio Nine Radio i2 13 Bedtime Explorers The Parent Brand The Parent Brand New 14 Kennedy Molloy SCA-Triple M SCA i5 15 The Howie Games SCA-PodcastOne Australia PodcastOne Australia i4 16 Hughesy and Kate SCA-Hit SCA i1 17 Moonman In The Morning - 104.9 SCA-Triple M SCA i5 Triple M Sydney 18 The Hot Breakfast SCA-Triple M SCA h1 19 Who the Hell is Hamish? News Corp Australia News Corp / Nova Ent i6 20 Chrissie, Sam & Browny Nova Nova Entertainment i4 21 Jase & PJ Australian Radio Network Australian Radio Network i1 22 Tech News News Corp Australia News Corp / Nova Ent h3 23 Police Tape News Corp Australia News Corp / Nova Ent h24 24 The Ray Hadley Morning Show Nine Radio Nine Radio i3 25 Motley Fool Money Australia -

Ofve' NEW RESIDENTIALCHANNEL LINEUP Effective 2/1 6/16

Odessa, TX CABLEOfVE' NEW RESIDENTIALCHANNEL LINEUP Effective 2/1 6/16 ECONOMY STAN DARD/ D I G ITAL VALU E PACK* xDigital Standard Cable includes Economy. Value Pack Channels noted in yellow. Additional fee applies. 3 455 ABC.KMID Women's Programming Fomily Programming "too7 .ll 'r,t'¡., I 7 cBs-KosA 1260 Animal Planet 100 1 100 Lifetime 260 B 475 FOX-KPEJ 1262 National Geographic Wild 102 1 102 LMN 262 9 1 009 NBC.KWES 103 OWN 263 1263 Discovery Channel Channel 13 1013 PB5-KPBT "t04 1 104 Bravo 26s 1265 Science Channel 16 1016 MyNetwork-KOSA 108 WE 266 1266 Hallmark 268 1264 Hallmark Movies & Mysteries 17 CW-KWES 112 lnvestigation DiscoverY 114 Oxygen 270 1270 Food Network 1B 1018 Univision-KUPB 1"16 Discovery Life 272 1272 HGTV 20 Telemundo-KTLE 274 1274 History Channel 2',! Galavision Sports 276 1276 H2 (Viceland) 22 UniMas 133 1 133 ESPN 277 1277 National Geographic Ch. '134 "t134 25 MeTV-KWWT ESPN2 241 Travel Channel 135 ESPN News 26 Decades 136 ESPNU Ch il dren's Proqra m m i n q 27 Movies 1 NBC Sports 137 137 300 1 300 Sprout 52 God's Learning Channel-KMLM "t39 ',t39 1 CBS Sports 302 1302 Disney Channel 56 Goverment Access 140 FCS Atlantic 304 Disney XD '141 72 Leased Access FCS Central 307 1307 FreeForm FCS Pacific 7B C-SPAN 142 311 Discovery Family 146 1146 FOX Sports 1 79 C-SPAN2 313 Disney Jr. 144 1 144 FOX Sports 2 Boomerang BO BYU 316 1 FOX Sports SW 155 155 317 1317 Cartoon Network 82 INSP 157 1157 NFL Network TBN 1 Golf Channel B4 158 158 News 85 EWTN 160 1 160 Outdoor €hannel 333 TheWeather Channel 161 ESPN Classic B6 -

1 Transcript of 2019 Nine Entertainment AGM Sydney

1 Transcript of 2019 Nine Entertainment AGM Sydney, November 12, 2019 Chairman Peter Costello Good morning ladies and gentleman. As your Chairman, it's my pleasure to welcome you to the 2019 AGM of Nine Entertainment Company. My name is Peter Costello. Before opening the meeting, I refer you to the disclaimer here on the screen behind me and available through our ASX lodgement. It is now shortly after 10am and I am advised that this is a properly constituted meeting. There's a quorum of at least two shareholders present so I declare the 2019 Annual General Meeting open. Unless there are any objections, I propose to take the Notice of Meeting as read. Copies of the Notice of Meeting are available from the registration desk outside should you require them. Let me now introduce the people who are with us this morning. To my immediate left is Rachel Launders, our General Counsel and Company Secretary. Then Hugh Marks, our Chief Executive Officer, who will address the meeting a little later. Next to Hugh is Nick Falloon, the Independent, Non-Executive Director and Deputy Chair and Member of the People and Remuneration Committee. Then we have Patrick Alloway, Independent, Non-Executive Director and a member of the Audit and Risk Management Committee. Next to Patrick is Sam Lewis, Independent, Non-Executive Director, Chair of the Audit and Risk Committee and a Member of the People and Remuneration Committee. Then we have Mickie Rosen, Independent, Non-Executive Director. At the far end, we have Catherine West, Independent, Non-Executive Director, the Chair of the People and Remuneration Committee and a member of the Audit and Risk Committee. -

2020 Full Year Results Announcement

27 August 2020 ASX Markets Announcement Office ASX Limited 20 Bridge Street Sydney NSW 2000 2020 FULL YEAR RESULTS ANNOUNCEMENT Attached is a copy of the ASX release relating to the 2020 Full Year Financial Results for Nine Entertainment Co. Holdings Limited Rachel Launders Company Secretary Authorised for release: Nine Board sub-committee Further information: Nola Hodgson Victoria Buchan Head of Investor Relations Director of Communications +61 2 9965 2306 +61 2 9965 2296 [email protected] [email protected] nineforbrands.com.au Nine Sydney - 1 Denison Street, North Sydney, NSW, 2068 ABN 60 122 203 892 NINE ENTERTAINMENT CO. FY20 FINAL RESULTS 27 August 2020: Nine Entertainment Co. (ASX: NEC) has released its FY20 results for the 12 months to June 2020. On a Statutory basis, Nine reported Revenue of $2.2b and a Net Loss of $575m, which included a post-tax Specific Item cost of $665m, largely relating to impairment of goodwill. On a pre AASB16 and Specific Item basis, Nine reported Group EBITDA of $355m, down 16% on the Pro Forma results in FY19 for its Continuing Businesses. On the same basis, Net Profit After Tax and Minority Interests was $160m, down 19%. Key takeaways include: • Audience growth across all key platforms – Metro Publishing, Stan, 9Now, Radio and FTA • Strong growth from digital video businesses o $51m EBITDA improvement at Stan1, with current active subscribers of 2.2m o 36% EBITDA growth at 9Now1 to $49m, with market leading BVOD revenue share of ~50% • Ad markets heavily impacted by COVID-19 from March 2020 • Nine was quick to mitigate the associated fallout with o $225m cost-out program – cash basis, CY20 o Including increasing and expediting previous cost initiatives • 40% growth in digital EBITDA to $166m ($178m post AASB16) • Evolution of Metro Media business to consumer focus, with reader revenue now accounting for almost 60% of total revenue • Strong balance sheet, with (wholly-owned) leverage ratio <1X 1 like-basis, pre AASB16 Hugh Marks, Chief Executive Officer of Nine Entertainment Co. -

9RUSH Apr 12

Page 1 of 27 9RUSH Sydney Program Guide Sun Apr 12, 2020 06:00 SALVAGE HUNTERS WS G Meet modern-day treasure hunter Drew Pritchard. With demanding customers, high turnover, and one of the biggest decorative salvage yards in the UK, Drew is constantly on the road, crisscrossing the country in search of derelict gems and forgotten remnants. 07:00 OVERHAULIN' WS PG Snaked A woman, dealing with a serious illness, would be overjoyed if her Mustang were overhauled. Cons.Advice: Themes, Mild Coarse Language 08:00 WHEELER DEALERS WS PG TVR Cerbera Mike tracks down a TVR Cerbera for just $16,000. However, these classic sports cars are notoriously susceptible to rust. Can Edd patch it up or will the chassis need replacing? 09:00 TANKED WS PG Old School vs. New School Brett and Wayde attempt to transform a pinball machine into a state-of-the art aquarium. Plus, can a high-tech robot function inside a series of tanks? 10:00 WEATHER GONE VIRAL Repeat WS PG Without Warning In this episode of Weather Gone Viral - heart-stopping moments when ice forces an airplane down and passengers must prepare for a crash landing; powerful winds flip a semi-truck; a tornado is caught on security cameras as it tears through a school gym. Cons.Advice: Realistic Violence 11:00 SALVAGE HUNTERS WS G Meet modern-day treasure hunter Drew Pritchard. With demanding customers, high turnover, and one of the biggest decorative salvage yards in the UK, Drew is constantly on the road, crisscrossing the country in search of derelict gems and forgotten remnants. -

Nine Network Australia Selects Intelsat to Distribute Domestic Television Programming

Nine Network Australia Selects Intelsat to Distribute Domestic Television Programming October 24, 2016 Intelsat will provide satellite connectivity and global fiber services via the IntelsatOne network to bring news content from around the world to Australia LUXEMBOURG--(BUSINESS WIRE)--Oct. 24, 2016-- Intelsat (NYSE: I), operator of the world’s first Globalized Network, powered by its leading satellite backbone, today announced a contract with Nine Network Australia to distribute programming to the company’s six domestic television stations as well as provide global satellite and fiber connectivity using the IntelsatOne terrestrial network to bring news content and special events from around the world to Australia for its network affiliates. Nine Network Australia (NNA) is one of the country’s top-rated commercial television networks, with local stations in Sydney, Melbourne, Brisbane, Adelaide, Perth and Darwin, along with a regional broadcaster, NBN. The network also has news bureaus in Canberra, London and Los Angeles. NNA is a subsidiary of Nine Entertainment Co., one of Australia’s leading media companies. Intelsat initially is providing services via the Australia/New Zealand Ku-Band beam on Intelsat 19 for the network’s broadcasting requirement. Under the agreement, Intelsat’s network support will extend well into the next decade. “Our Globalized Network allows us to meet NNA’s needs today and to increase our level of support if the network expands over time to meet the demands of multi-platform coverage,” said Terry Bleakley, Regional Vice President, Asia Pacific Sales, Intelsat. “NNA will also benefit from Intelsat’s global coverage for international contribution and distribution requirements.” NNA previously used Intelsat for its domestic and international occasional use requirements.