Macc/Pdf/2004-05 Annual Report.Pdf

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Legislative Assembly of Manitoba DEBATES and PROCEEDINGS Official Report

First Session - Thirty-Eighth Legislature of the Legislative Assembly of Manitoba DEBATES and PROCEEDINGS Official Report (Hansard) Published under the authority of The Honourable George Hickes Speaker Vol. LIV No. 5b – 1:30 p.m., Thursday, September 11, 2003 MANITOBA LEGISLATIVE ASSEMBLY First Session–Thirty-Eighth Legislature Member Constituency Political Affiliation AGLUGUB, Cris The Maples N.D.P. ALLAN, Nancy St. Vital N.D.P. ALTEMEYER, Rob Wolseley N.D.P. ASHTON, Steve, Hon. Thompson N.D.P. BJORNSON, Peter Gimli N.D.P. BRICK, Marilyn St. Norbert N.D.P. CALDWELL, Drew, Hon. Brandon East N.D.P. CHOMIAK, Dave, Hon. Kildonan N.D.P. CUMMINGS, Glen Ste. Rose P.C. DERKACH, Leonard Russell P.C. DEWAR, Gregory Selkirk N.D.P. DOER, Gary, Hon. Concordia N.D.P. DRIEDGER, Myrna Charleswood P.C. DYCK, Peter Pembina P.C. EICHLER, Ralph Lakeside P.C. FAURSCHOU, David Portage la Prairie P.C. GERRARD, Jon, Hon. River Heights Lib. GOERTZEN, Kelvin Steinbach P.C. HAWRANIK, Gerald Lac du Bonnet P.C. HICKES, George, Hon. Point Douglas N.D.P. IRVIN-ROSS, Kerri Fort Garry N.D.P. JENNISSEN, Gerard Flin Flon N.D.P. JHA, Bidhu Radisson N.D.P. KORZENIOWSKI, Bonnie St. James N.D.P. LAMOUREUX, Kevin Inkster Lib. LATHLIN, Oscar, Hon. The Pas N.D.P. LEMIEUX, Ron, Hon. La Verendrye N.D.P. LOEWEN, John Fort Whyte P.C. MACKINTOSH, Gord, Hon. St. Johns N.D.P. MAGUIRE, Larry Arthur-Virden P.C. MALOWAY, Jim Elmwood N.D.P. MARTINDALE, Doug Burrows N.D.P. McGIFFORD, Diane, Hon. -

Cfa-Winnipeg-Luncheon-M-Wowchuk-Nov-15

CFA Winnipeg Notice of Seminar and Luncheon The State of the Province 2010/2011 Board of Directors Speaker: President Dalbir Bains, CFA (204) 934-8874 Vice-President Glenn Bunston, CFA (204) 985-7170 Treasurer Leney Richardson, CFA (204) 479-3365 Secretary Honourable Rosann Wowchuk Stephen Gannon, CFA (204) 946-3204 DEPUTY PREMIER Minister of Finance Programming Chris Richard As the finance minister of Manitoba, the Honourable Rosann Wowchuk has a unique (204) 946-7378 perspective on the financial health of our province. She will deliver an address on the University Relations fiscal position of the province. She will also discuss the financial strengths of the Joe Brekelmans, CFA province as well as the obstacles that she sees in the near and distant future. (204) 946-4873 Candidate Relations Adam Wylychenko Rosann Wowchuk is Manitoba's Minister of Finance, Minister responsible for (204) 934-8855 the Manitoba Hydro Act and the Province's Deputy Premier. She was first elected as the MLA for Swan River in 1990 and has been re-elected in every Advocacy Richard Iwuc, CFA general election since then. (204) 792-5975 Membership On October 5, 1999, Rosann became Minister of Agriculture and Food and in Graeme Hay 2003 was reappointed Minister of Agriculture, Food and Rural Initiatives and (204) 925-7963 named Deputy Premier. On September 14, 2009 she was appointed Minister of Public Relations & Awareness Finance and Minister responsible for Manitoba Hydro and remained Deputy Val Wowryk, CFA Premier. Minister Wowchuk is the first female minister of finance in the history (204) 254-6480 of Manitoba. -

Legislative Assembly Officers and Staff

4th Session - 38th Legislature Legislative Assembly Officers and Staff Lieutenant Governor of Manitoba ................................... Hon. John Harvard, P.C., O.M. Speaker of the Legislative Assembly ..................................... Hon. George Hickes, MLA Deputy Speaker and Chairperson of Committees of the Whole House ............................................. Mr. Conrad Santos, MLA Deputy Chairpersons of Committees of the Whole House ........................................................................................... Mr. Harry Schellenberg, MLA ....................................................................................... Ms. Bonnie Korzeniowski, MLA Government House Leader ................................................. Hon. Gord Mackintosh, MLA Opposition House Leader ............................................................ Mr. Len Derkach, MLA ............................................................... Mr. Kelvin Goertzen, MLA – as of May 8, 2006 Government Whip .................................................................... Mr. Gregory Dewar, MLA Opposition Whip ................................................................. Mr. Peter George Dyck, MLA Clerk of the Legislative Assembly ................................................ Ms. Patricia Chaychuk Deputy Clerk of the Legislative Assembly....................................... Ms. Beverley Bosiak Clerk Assistant/Clerk of Committees ..................................... Ms. JoAnn McKerlie-Korol ................................................................................................................ -

Legislators Forum

9TH ANNUAL INTERNATIONAL LEGISLATORS FORUM MANITOBA| MINNESOTA| NORTH DAKOTA| SOUTH DAKOTA GIMLI MANITOBA • JUNE 24-26 2009 FRONT ROW (left to right): Representative Val Rausch-SD, Representative Lois Delmore-ND, Ms. Mavis Taillieu-MB, Ms. Jennifer Howard-MB, Honourable RosannWowchuk-MB SECOND ROW: Representative Paul Dennert-SD, Senator Tom Hanson-SD, Senator Jim Peterson-SD, Senator Rich Wardner-ND, Mr. Ralph Eichler-MB THIRD ROW: Senator Rod Skoe-MN, Mr. Larry Maguire-MB, Representative Morrie Lanning-MN, Senator Gary Hanson-SD, Senator Arden Anderson-ND, Senator Dan Skogen-MN, Representative Dennis Johnson-ND FOURTH ROW: Senator Tom Fiebiger-ND, Senator Tom Saxhaug-MN, Mr. Greg Dewar-MB, Mr. Peter Bjornson-MB, Representative David Monson-ND LEGISLATORS FORUM STEERING COMMITTEE The Steering Committee, appointed to continue activity between annual meetings, is composed of legislators from each of the four jurisdictions. Members are: • Manitoba: Honourable Rosann Wowchuk and Ms. Mavis Taillieu • Minnesota: Senator Tom Saxhaug and Representative Morrie Lanning • North Dakota: Senator Tom Fischer and Representative Lois Delmore • South Dakota: Senator Gary Hanson and Representative Carol Pitts. 2009 LEGISLATORS FORUM ATTENDEES MANITOBA • Honourable Rosann Wowchuk • Ms. Mavis Taillieu • Mr. Larry Maguire • Mr. Rob Altemeyer Th e ninth annual meeting of the Legislators THE DELEGATES TO THE NINTH • Mr. Ralph Eichler Forum began with a reception at the Lakeview ANNUAL INTERNATIONAL • Ms. Jennifer Howard Resort in Gimli Manitoba on Wednesday, June LEGISLATORS FORUM GRATEFULLY • The Honourable Bill Blaikie 24, 2009. Th ere to greet delegates, presenters, ACKNOWLEDGE THE SUPPORT OF • Mr. Peter Bjornson spouses, and staff were co-hosts of this year’s THE FOLLOWING SPONSORS: • Mr. -

2008 Annual Report 3

2 ANNUAL0 008REPORT8 An independent office of the Legislative Assembly/Un bureau indépendant de l’Assemblée législative December 29, 2009 The Honourable George Hickes Speaker of the Legislative Assembly Room 244 Legislative Building Winnipeg, Manitoba R3C 0V8 Dear Mr. Speaker: I have the honour of submitting to you my annual report on the activities of Elections Manitoba for the 2008 calendar year. This report is submitted pursuant to subsection 32(1) of The Elections Act and subsection 99(1) of The Elections Finances Act. In accordance with subsection 32(5) of The Elections Act and subsection 99(2.1) of The Elections Finances Act, annual reporting under these statutes has been combined. The applicable legislation states that the Speaker shall lay the report before the Legislative Assembly forthwith if the Assembly is in session or, if not, within 15 days after the beginning of the next session. Pursuant to subsection 32(4) of The Elections Act and subsection 99(3) of The Elections Finances Act, an annual report that contains recommendations for amendments to these Acts stands referred to the Standing Committee on Legislative Aff airs for consideration of those matters. Furthermore, these subsections provide that the Committee shall begin its consideration of the report within 60 days after the report is laid before the Assembly. Respectfully yours, ORIGINAL SIGNED BY Richard D. Balasko Chief Electoral Offi cer 120 - 200 Vaughan Street, 120 - 200 rue Vaughan Winnipeg, Manitoba R3C 1T5 Phone/Téléphone : 204.945.3225 Fax/Télécopieur : 204.945.6011 -

Legislative Assembly Officers and Staff

5th Session - 38th Legislature Legislative Assembly Officers and Staff Lieutenant Governor of Manitoba ................................... Hon. John Harvard, P.C., O.M. Speaker of the Legislative Assembly ..................................... Hon. George Hickes, MLA Deputy Speaker and Chairperson of Committees of the Whole House ............................................. Mr. Conrad Santos, MLA Deputy Chairpersons of Committees of the Whole House ........................................................................................... Mr. Harry Schellenberg, MLA ....................................................................................... Ms. Bonnie Korzeniowski, MLA Government House Leader .................................................... Hon. Dave Chomiak, MLA Opposition House Leader ....................................................... Mr. Kelvin Goertzen, MLA Government Whip .................................................................... Mr. Gregory Dewar, MLA Opposition Whip ................................................................Mrs. Heather Stefanson, MLA Clerk of the Legislative Assembly ................................................ Ms. Patricia Chaychuk Deputy Clerk of the Legislative Assembly....................................... Ms. Beverley Bosiak Clerk Assistant/Clerk of Committees ........................................... Ms. Tamara Pomanski ................................................................................................................. Mr. Rick Yarish Clerk Assistant/Journals -

*2006 Amm Annual Report

THE ASSOCIATION OF MANITOBA MUNICIPALITIES September 1, 2005 to August 31, 2006 AMM Annual Report • September 1, 2005 to August 31, 2006 AMM Members Financial Statement Urban Centres Pinawa, LGD Clanwilliam Park Altona, Town Arborg, Town Plum Coulee, Town Coldwell Pembina Beausejour, Town Portage la Prairie, City Cornwallis Piney Benito, Village Powerview, Village Daly Pipestone Binscarth, Village Rapid City, Town Dauphin Portage la Prairie Birtle, Town Rivers, Town De Salaberry Reynolds Boissevain, Town Riverton, Village Dufferin Rhineland Bowsman, Village Roblin, Town East St. Paul Ritchot Brandon, City Rossburn, Town Edward Riverside Carberry, Town Russell, Town Ellice Roblin Carman, Town Selkirk, City Elton Rockwood Cartwright, Village Shoal Lake, Town Eriksdale Roland Churchill, Town Snow Lake, Town Ethelbert Rosedale Crystal City, Village Somerset, Village Fisher Rossburn Dauphin, City Souris, Town Franklin Rosser Deloraine, Town St. Claude, Village Gilbert Plains Russell Dunnottar, Village St. Lazare, Village Gimli Saskatchewan Elkhorn, Village St. Pierre-Jolys, Village Glenella Shell River Emerson, Town Ste. Anne, Town Glenwood Shellmouth-Boulton Erickson, Town Ste. Rose du Lac, Town Grahamdale Shoal Lake Ethelbert, Village Steinbach, City Grandview Sifton Flin Flon, City Stonewall, Town Grey Siglunes Gilbert Plains, Town Swan River, Town Hamiota Silver Creek Gillam, Town Teulon, Town Hanover South Cypress Gladstone, Town The Pas, Town Harrison South Norfolk Mission Statement Thompson, City Headingley Springfield Glenboro, Village Grand Rapids, Town Treherne, Town Hillsburg St. Andrews Grandview, Town Virden, Town Kelsey St. Clements The Association of Manitoba Waskada, Village La Broquerie St. Francois Xavier Gretna, Town Municipalities identifies and addresses Hamiota, Town Wawanesa, Village Lac du Bonnet St. Laurent Hartney, Town Winkler, City Lakeview Stanley the needs and concerns of its members Killarney, Town Winnipeg Beach, Town Langford Ste. -

Trailblazers of the FIRST 100 YEARS

Women of the Legislative Assembly of Manitoba Trailblazers OF THE FIRST 100 YEARS 1916 – 2016 TIVE ASS LA EM IS B G L E Y L MANITOBA On January 28, 1916, Bill No. 4 – An Act to amend “The Manitoba Election Act” received Royal Assent. The passage of this Act granted most Manitoba women the right to vote and to run for public office. Manitoba was the first province in Canada to win the right to vote for women. Nellie McClung was one of the Manitoba women involved in campaigning for the women’s right to vote in 1916. She was also one of Canada’s Famous Five who initiated and won the Persons Case, to have women become recognized as persons under Canadian law in 1929. In recognition of Manitoba’s centennial of most women receiving the right to vote, we pay tribute to a select handful of women trailblazers who achieved first in their field since that time. 2 TRAILBLAZERS 1916 - 2016 Trailblazers OF THE FIRST 100 YEARS Foreword by JoAnn McKerlie-Korol, Director of Education and Outreach Services of the Legislative Assembly of Manitoba On January 28, 1916, legislation passed that granted women the right to vote and to run for public office. On June 29, 1920, the first woman, Edith Rogers, was elected to represent the constituency of Winnipeg. This was just the beginning of the “firsts” for Manitoba’s women in the Legislative Assembly. Celebrating the first 100 years since the passage of this legislation, only 51 women have been elected to the Manitoba Legislative Assembly as elected MLAs and only a small number have served as Officers of the Legislative Assembly. -

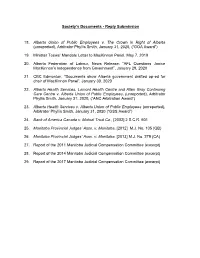

Peace Compensation Commission Reply Submissions of the Crown in Right of Alberta Submitted by Phyllis A. Smith

Society’s Documents - Reply Submission 18. Alberta Union of Public Employees v. The Crown in Right of Alberta (unreported), Arbitrator Phyllis Smith, January 31, 2020, (“GOA Award”) 19. Minister Toews’ Mandate Letter to MacKinnon Panel, May 7, 2019 20. Alberta Federation of Labour, News Release: “AFL Questions Janice MacKinnon’s Independence from Government”, January 29, 2020 21. CBC Edmonton, “Documents show Alberta government drafted op-ed for chair of MacKinnon Panel”, January 30, 2020 22. Alberta Health Services, Lamont Health Centre and Allen Gray Continuing Care Centre v. Alberta Union of Public Employees, (unreported), Arbitrator Phyllis Smith, January 31, 2020, (“ANC Arbitration Award”) 23. Alberta Health Services v. Alberta Union of Public Employees (unreported), Arbitrator Phyllis Smith, January 31, 2020 (“GSS Award”) 24. Bank of America Canada v. Mutual Trust Co., [2002] 2 S.C.R. 601 25. Manitoba Provincial Judges’ Assn. v. Manitoba, [2012] M.J. No. 105 (QB) 26. Manitoba Provincial Judges’ Assn. v. Manitoba, [2013] M.J. No. 279 (CA) 27. Report of the 2011 Manitoba Judicial Compensation Committee (excerpt) 28. Report of the 2014 Manitoba Judicial Compensation Committee (excerpt) 29. Report of the 2017 Manitoba Judicial Compensation Committee (excerpt) Bank of America Canada v. Mutual Trust Co., [2002] 2 S.C.R. 601 Supreme Court Reports Supreme Court of Canada Present: McLachlin C.J. and L'Heureux-Dubé, Gonthier, Iacobucci, Major, Bastarache, Binnie, Arbour and LeBel JJ. 2001: December 11 / 2002: April 26. File No.: 27898. [2002] 2 S.C.R. 601 | [2002] 2 R.C.S. 601 | [2002] S.C.J. No. 44 | [2002] A.C.S. -

DEBATES and PROCEEDINGS

Fourth Session - Thirty-Eighth Legislature of the Legislative Assembly of Manitoba DEBATES and PROCEEDINGS Official Report (Hansard) Published under the authority of The Honourable George Hickes Speaker Vol. LVII No. 70A - 10 a.m., Tuesday, May 16, 2006 MANITOBA LEGISLATIVE ASSEMBLY Thirty-Eighth Legislature Member Constituency Political Affiliation AGLUGUB, Cris The Maples N.D.P. ALLAN, Nancy, Hon. St. Vital N.D.P. ALTEMEYER, Rob Wolseley N.D.P. ASHTON, Steve, Hon. Thompson N.D.P. BJORNSON, Peter, Hon. Gimli N.D.P. BRICK, Marilyn St. Norbert N.D.P. CALDWELL, Drew Brandon East N.D.P. CHOMIAK, Dave, Hon. Kildonan N.D.P. CULLEN, Cliff Turtle Mountain P.C. CUMMINGS, Glen Ste. Rose P.C. DERKACH, Leonard Russell P.C. DEWAR, Gregory Selkirk N.D.P. DOER, Gary, Hon. Concordia N.D.P. DRIEDGER, Myrna Charleswood P.C. DYCK, Peter Pembina P.C. EICHLER, Ralph Lakeside P.C. FAURSCHOU, David Portage la Prairie P.C. GERRARD, Jon, Hon. River Heights Lib. GOERTZEN, Kelvin Steinbach P.C. HAWRANIK, Gerald Lac du Bonnet P.C. HICKES, George, Hon. Point Douglas N.D.P. IRVIN-ROSS, Kerri Fort Garry N.D.P. JENNISSEN, Gerard Flin Flon N.D.P. JHA, Bidhu Radisson N.D.P. KORZENIOWSKI, Bonnie St. James N.D.P. LAMOUREUX, Kevin Inkster Lib. LATHLIN, Oscar, Hon. The Pas N.D.P. LEMIEUX, Ron, Hon. La Verendrye N.D.P. MACKINTOSH, Gord, Hon. St. Johns N.D.P. MAGUIRE, Larry Arthur-Virden P.C. MALOWAY, Jim Elmwood N.D.P. MARTINDALE, Doug Burrows N.D.P. McFADYEN, Hugh Fort Whyte P.C. -

2009 Annual Report of the Association of Manitoba Challenging in So Many Ways.” Municipalities (AMM)

THE ASSOCI A TION OF MA NITOB A MUNICIPALITIES 2009 ANNU A L REPO R T SEPTE M BE R 1, 2008 TO AUGUST 31, 2009 AMM 2009 ANNU A L REPO R T 1 The AMM Board of Directors is comprised of the members of the Executive Committee, who shall not hold any other Board position, plus fifteen (15) additional Board Members. The Board Members are comprised of Elected Officials representing one of seven (7) Districts. Parkland, Western, Midwestern, Central, Eastern, and Interlake districts are comprised of one (1) representative from an urban municipality and one (1) representative from a rural municipality in each of the respective Districts. The representation to the Board for Northern District shall be comprised of one (1) representative from The Pas, RM of Kelsey, Flin Flon, Snow Lake or Grand Rapids, and one (1) representative from Thompson, Lynn Lake, Leaf Rapids, Churchill, Gillam or LGD of Mystery Lake. The Director for the City of Winnipeg shall be appointed by the council of the City of Winnipeg. The President of the Manitoba Municipal Administrators’ Association also sits as an ex-officio representative to the Board of Directors. The Executive Committee consists of a President, a Vice-President Rural, and a Vice-President Urban. The Executive are elected for a one-year term at every Annual Convention. The term of office for all Directors shall be for two years. Each Director shall hold office until the second annual District Meeting following their election to office. TA BLE OF CONTENTS Map of Municipalities 4 AMM Members 5 President’s Message -

DEBATES and PROCEEDINGS

Third Session - Thirty-Eighth Legislature of the Legislative Assembly of Manitoba DEBATES and PROCEEDINGS Official Report (Hansard) Published under the authority of The Honourable George Hickes Speaker Vol. LVI No. 53A - 10 a.m., Thursday, May 26, 2005 MANITOBA LEGISLATIVE ASSEMBLY Thirty-Eighth Legislature Member Constituency Political Affiliation AGLUGUB, Cris The Maples N.D.P. ALLAN, Nancy, Hon. St. Vital N.D.P. ALTEMEYER, Rob Wolseley N.D.P. ASHTON, Steve, Hon. Thompson N.D.P. BJORNSON, Peter, Hon. Gimli N.D.P. BRICK, Marilyn St. Norbert N.D.P. CALDWELL, Drew Brandon East N.D.P. CHOMIAK, Dave, Hon. Kildonan N.D.P. CULLEN, Cliff Turtle Mountain P.C. CUMMINGS, Glen Ste. Rose P.C. DERKACH, Leonard Russell P.C. DEWAR, Gregory Selkirk N.D.P. DOER, Gary, Hon. Concordia N.D.P. DRIEDGER, Myrna Charleswood P.C. DYCK, Peter Pembina P.C. EICHLER, Ralph Lakeside P.C. FAURSCHOU, David Portage la Prairie P.C. GERRARD, Jon, Hon. River Heights Lib. GOERTZEN, Kelvin Steinbach P.C. HAWRANIK, Gerald Lac du Bonnet P.C. HICKES, George, Hon. Point Douglas N.D.P. IRVIN-ROSS, Kerri Fort Garry N.D.P. JENNISSEN, Gerard Flin Flon N.D.P. JHA, Bidhu Radisson N.D.P. KORZENIOWSKI, Bonnie St. James N.D.P. LAMOUREUX, Kevin Inkster Lib. LATHLIN, Oscar, Hon. The Pas N.D.P. LEMIEUX, Ron, Hon. La Verendrye N.D.P. LOEWEN, John Fort Whyte P.C. MACKINTOSH, Gord, Hon. St. Johns N.D.P. MAGUIRE, Larry Arthur-Virden P.C. MALOWAY, Jim Elmwood N.D.P. MARTINDALE, Doug Burrows N.D.P.