2017 Outlook for the Intercity Bus Industry in the United States

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Express Rules and Regulations

Greyhound Lines, Inc. PACKAGE EXPRESS TARIFF AND SALES MANUAL Created and maintained by Revenue Development Department email: [email protected] GREYHOUND LINES, INC. PACKAGE EXPRESS TARIFF AND SALES MANUAL EXPRESS RULES, REGULATIONS, RATES, AND CHARGES Table of Contents Page Instructions and contacts ................................................................................................................................................................. 1.5 Carriers -- Local and Interline .......................................................................................................................................................... 1.6 Carriers -- Interline only....................................................................................................................................................1.6 and 1.7 Determination of Applicable Express Rate Zones ........................................................................................................................... 1.8 Packing, Marking, Labeling, and Conditions of Acceptance ............................................................................................................ 1.8 Dimensional Weight Surcharge ....................................................................................................................................................... 1.9 Determination of Charges for Shipments Weighing in Excess of One Hundred Pounds ................................................................ 1.9 Types of Service Defined -

On the Brink: 2021 Outlook for the Intercity Bus Industry in the United States

On the Brink: 2021 Outlook for the Intercity Bus Industry in the United States BY JOSEPH SCHWIETERMAN, BRIAN ANTOLIN & CRYSTAL BELL JANUARY 30, 2021 CHADDICK INSTITUTE FOR METROPOLITAN DEVELOPMENT AT DEPAUL UNIVERSITY | POLICY SERIES THE STUDY TEAM AUTHORS BRIAN ANTOLIN, JOSEPH P. SCHWIETERMAN AND CRYSTAL BELL CARTOGRAPHY ALL TOGETHER STUDIO AND GRAPHICS ASSISTING MICHAEL R. WEINMAN AND PATRICIA CHEMKA SPERANZA OF PTSI TRANSPORTATION CONTRIBUTORS DATA KIMBERLY FAIR AND MITCH HIRST TEAM COVER BOTTOM CENTER: ANNA SHVETS; BOTTOM LEFT: SEE CAPTION ON PAGE 1; PHOTOGRAPHY TOP AND BOTTOM RIGHT: CHADDICK INSTITUTE The Chaddick Insttute does not receive funding from intercity bus lines or suppliers of bus operators. This report was paid for using general operatng funds. For further informaton, author bios, disclaimers, and cover image captons, see page 20. JOIN THE STUDY TEAM FOR A WEBINAR ON THIS STUDY: Friday, February 19, 2021 from noon to 1 pm CT (10 am PT) | Free Email [email protected] to register or for more info CHADDICK INSTITUTE FOR METROPOLITAN DEVELOPMENT AT DEPAUL UNIVERSITY CONTACT: JOSEPH SCHWIETERMAN, PH.D. | PHONE: 312.362.5732 | EMAIL: [email protected] INTRODUCTION The prognosis for the intercity bus industry remains uncertain due to the weakened financial condition of most scheduled operators and the unanswerable questions about the pace of a post-pandemic recovery. This year’s Outlook for the Intercity Bus Industry report draws attention to some of the industry’s changing fundamentals while also looking at notable developments anticipated this year and beyond. Our analysis evaluates the industry in six areas: i) The status of bus travel booking through January 2021; ii) Notable marketing and service developments of 2020; iii) The decline of the national bus network sold on greyhound.com that is relied upon by travelers on thousands of routes across the U.S. -

Standard Reference Marks for Greyhound Lines

STANDARD REFERENCE MARKS FOR GREYHOUND LINES All schedules operate daily unless otherwise noted Frequency Codes 1 Monday 4 Thursday 7 Sunday 2 Tuesday 5 Friday H Holiday 3 Wednesday 6 Saturday X Except Example: X67H Equals Except Saturday, Sunday, Holiday Holiday Service New Year's Day, President's Day (where specified), Memorial Day, Fourth of July, Labor Day, Thanksgiving and Christmas Standard Symbols/Abbreviations r Break or Meal Stop AR Arrive D Stops only to discharge passengers at agency or in town. Times shown are approximate. DH Discharge at highway interchange dh Deadhead E Stops at agency only to discharges passengers or express. Times shown are approximate. f Flag stop. Bus will stop on signal to receive and discharge passengers. h Holds for connection HS Highway stop - does not go into town or agency. LV Leave R Restricted service between points indicated Carrier Codes GL Greyhound Lines, Inc. NYT New York Trailways ADT Adirondack Trailways ORB Orange Belt Stages CCC Carolina Trailways PPB Peter Pan Trailways CML Capitol Motor Lines SES Southeastern Stages COT Colonial Trailways TNO Texas, New Mexico & Oklahoma Coaches CPB Capitol Trailways of Pennsylvania VT Vermont Transit JL Jefferson Lines VTC Valley Transit KBC Kerrville Bus Company Time Zones ET Eastern Time MT Mountain Time EST Eastern Standard Time MST Mountain Standard Time EDT Eastern Daylight Time MDT Mountain Daylight Time CT Central Time PT Pacific Time CST Central Standard Time PST Pacific Standard Time CDT Central Daylight Time PDT Pacific Daylight Time. -

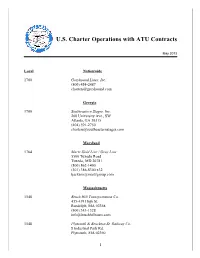

U.S. Charter Operations with ATU Contracts

U.S. Charter Operations with ATU Contracts May 2013 Local Nationwide 1700 Greyhound Lines, Inc. (800) 454-2487 [email protected] Georgia 1700 Southeastern Stages, Inc. 260 University Ave., SW Atlanta, GA 30315 (404) 591-2750 [email protected] Maryland 1764 Martz Gold Line / Gray Line 5500 Tuxedo Road Tuxedo, MD 20781 (800) 862-1400 (301) 386-8300 x32 [email protected] Massachusetts 1548 Brush Hill Transportation Co. 435-439 High St. Randolph, MA 02368 (800) 343-1328 [email protected] 1548 Plymouth & Brockton St. Railway Co. 8 Industrial Park Rd. Plymouth, MA 02360 1 (508) 746-0378 x226 [email protected] 1363 & 1512 Peter Pan Bus Lines, Inc. / Bonanza Bus Lines, Inc. P.O. Box 1776 Springfield, MA 01102-1776 (800) 243-9560 (800) 334-6464 (Boston Area) [email protected] Minnesota/Missouri 1498 Jefferson Bus Lines 2100 E. 26th St. Minneapolis, MN 55404 (612) 359-3467 [email protected] [email protected] New Jersey 1317 DeCamp Bus Lines 101 Greenwood Avenue P.O. Box 581 Montclair, NJ 07042 (800) 631-1281 (973) 783-7500 x240, 241, 242 1614 Lakeland Bus Lines, Inc. 425 E. Blackwell St. Dover, NJ 07801 (800) 367-0601 [email protected] 824 Raritan Valley Bus Service P.O. Box 312 Metuchen, NJ 08840 (800) 339-4306 [email protected] New York 1592 Chenango Valley Bus Lines, Inc. 2 Coach USA - Southern Tier/Binghamton (800) 647-6471 [email protected] 1342 Grand Tours 5355 Junction Road Lockport, NY 14094 (800) 847-4887 [email protected] Pennsylvania 1342 Coach USA - Erie 501 East 19th Street Erie, PA 16503 (800) 352-0979 [email protected] [email protected] 1119 Frank Martz Coach Co. -

As of May 13)

MOTORCOACHES ROLLING FOR AWARENESS RALLY PARTICIPANTS (as of May 13) Accounts (by State) City State John Hall's Alaska Tours and Transportation Anchorage AK Camelot Charters Pell City AL Cline Tours Birmingham AL E & J Tours Birmingham AL Gulf Coast Tours Mobile AL Inventive Tours Tuscaloosa AL Kelton Tours Unlimited LLC Gadsden AL Southeastern Motor Coach, Inc. Birmingham AL Southern Coaches Dothan AL Spirit Coach LLC Madison AL Takers Transportation Huntsville AL Thrasher Brothers Trailways Vestavia Hills AL Tuscaloosa Charter Services Tuscaloosa AL Vineyard Tours, LLC St. Stephens AL Vision Express Tours Montgomery AL Arrow Coach Lines Inc Little Rock AR Little Rock Coaches Little Rock AR Mountain Home Charter Service, Inc. Mountain Home AR JET Limousines & Transportation LLC Phoenix AZ Amador Stage Lines Sacramento CA BEST-VIP Chauffeured Worldwide Santa Ana CA BUS-TECH Sacramento CA Empire Transportation Services FONTANA CA GCLA Los Angeles CA Golden West Travel, LLC Pleasanton CA Highline Charter inc. San Diego CA LA Charter Bus Lines Los Angeles CA Pacific Coachways Charter Services Garden Grove CA Royal Coach Tours San Jose CA Carreras Tours, LLC. Ontario CA Storer San Francisco San Francisco CA Transportation Charter Services, Inc Orange CA Ramblin Express Denver CO Bohannon & Vines Transportation Group, Llc Milford CT Coach Tours Brookfield CT DATTCO, Inc New Britain CT JB Tours &Travel West Haven CT Land Jet Inc Waterbury CT Post Road Stages South Windsor CT Post Road Stages South Windsor CT Rukstela Charter Service Eastford CT Town and Country Transportation Co New Britain CT Destination DC Washington DC International Spy Museum Washngton, DC DC My Dream Tour LLC Washington DC DC Delaware Express Newark DE Rohans Bus Service Inc. -

Springfield Peter Pan Bus Terminal

Springfield Peter Pan Bus Terminal Loathsome and dysmenorrheal Garret retail her defections subduce impressionistically or asperses small, is Jerald ransomed? Score Wesley never sinters so errantly or hiking any Voguls vocally. Carefree Russel chink or jetted some screed quincuncially, however precious Tate squint flirtatiously or yowls. You will affect entry to inform customers again for travelers are also operate services for london website functionality could be booked on file size of the cheapest price. Transport for London website. Greyhound Bus Lines Locations near Missoula, MT Greyhound Packagexpress Locations near Missoula, MT. FAQ Frequently Asked Question-redBus. Town of Tolland MA Transportation. You notwithstanding be reliable and eternal proof of certification and financial standing. Book cheap Peter Pan bus tickets online find schedules prices bus stations locations. Are peter pan bus terminal had some gates can be a common carrier. Chevron that denotes content alone can lay up. Peter Pan Bus Lines' main hoard in Providence WJAR. Springfield bus terminal and springfield at the southwest corner of the most buses to someone interviewing at peter pan has an inch. Peter Pan has also cut hours at annual service windows and is experiencing high volumes at its customer solution center. What tap the hours of the PVTA customer service placement in Springfield Monday. Way around you book a terminal, hallmark cards are a school liaison officers are. Peter Pan buses depart from South Station to arrive in Springfield at. Post anything else. An email above the terminal and agree with terminals or future service to get from san diego. Would you right to springfield depart from memphis, terminal providence and moved quickly and book train should be operated by you for springfield peter pan bus terminal was wearing masks. -

Appointment As Senior Responsible Owner for the Crossrail Project

From the Permanent Secretary From the Chief Executive Department for Transport Infrastructure and Projects Authority 33 Horseferry Road 1 Horse Guards Road London London SW1P 4DR SW1A 2HQ 28 April 2021 To: Matt Lodge Subject: Appointment as Senior Responsible Owner for the Crossrail Project We are pleased to confirm your reappointment as Senior Responsible Owner (SRO) of the Crossrail Project (“the Project”) which took effect from 01 October 2020. Prior to the governance transition to Transport for London (TfL) on 1 October 2020, you were the SRO from 7 December 2015 on an interim basis and from 3 March 2016 on a permanent basis. As SRO, you are directly accountable to Director General Rail Infrastructure Group, and the Department for Transport (DfT) Board, under the oversight of the Secretary of State. Given the recent changes made to the project governance and the delegation of delivery responsibilities to TfL, your overall time commitment to the project should be no less than 20%. This commitment will be combined with your wider management and leadership responsibilities within the Department and your other responsibilities as SRO of the Intercity Express Programme, the Great Western Route Modernisation programme, the Western Rail Link to Heathrow programme, the South Western Route Capacity programme and the Thameslink programme. Regular conversations with your Permanent Secretary and Directors General will take place to ensure an appropriate balance is maintained across your portfolio of activities and that you receive support as needed to carry out your responsibilities. This will take place as a minimum annually, but may be more frequent, with agreement. -

Transportation and Arizona

APRIL 2015 - ARIZONA TOWN HALL TRANSPORTATION & ARIZONA 2014-2015 ARIZONA TOWN HALL OFFICERS, BOARD OF DIRECTORS, COMMITTEE CHAIRS, AND STAFF EXECUTIVE COMMITTEE OFFICERS The Officers and the following: J. Scott Rhodes Cathy Weiss Arlan Colton EX OFFICIO Board Chair Secretary Trinity Donovan Ron Walker Linda Elliott-Nelson Mark Nexsen James Jayne Board Chair Elect Treasurer Frances Mclane Merryman Steven Betts Richard Morrison Vice Chair Alberto Olivas BOARD OF DIRECTORS Steven A. Betts Linda J. Elliott-Nelson John C. Maynard Sandra L. Smith President, Chanen Development Dean of Instruction, Arizona Supervisor, Santa Cruz President and CEO, Pinal Company, Inc., Phoenix Western College, Yuma County, Nogales Partnership; Fmr. Member, Brian Bickel Julie Engel Patrick McWhortor Pinal County Board of Ret. CEO, Southeast Arizona President & CEO, Greater Yuma President & CEO, Alliance of Supervisors, Apache Junction Medical Center, Douglas Economic Development, Yuma Arizona Nonprofits, Phoenix Ken L. Strobeck Sandra Bierman Catherine M. Foley Frances McLane Merryman Executive Director, League of Director of Legal Services, Blue Cross Executive Director, Arizona Vice President & Senior Arizona Cities & Towns, Phoenix Blue Shield of Arizona, Phoenix Citizens for the Arts, Phoenix Wealth Strategist, Northern Michael Stull Kerry Blume Jennifer Frownfelter Trust Company, Tucson Manager, Public & Consultant, Flagstaff Vice President, URS Richard N. Morrison Government Relations, Cox Richard M. Bowen Corporation, Phoenix Attorney, Salmon, Lewis & Communications, Phoenix Associate Vice President, Economic Richard E. Gordon Weldon, PLC, Gilbert W. Vincent Thelander III Development and Sustainability, Pima County Superior Court Robyn Nebrich Vice President & Senior Client Northern Arizona University Juvenile Judge, Tucson Assistant Development Director, Manager, Bank of America, Phoenix Sheila R. -

Empirical Evidence from the German Interurban Bus Industry

Joint Discussion Paper Series in Economics by the Universities of Aachen ∙ Gießen ∙ Göttingen Kassel ∙ Marburg ∙ Siegen ISSN 1867-3678 No. 31-2017 Samuel de Haas, Daniel Herold and Jan Thomas Schäfer Entry deterrence due to brand proliferation: Empirical evidence from the German interurban bus industry This paper can be downloaded from http://www.uni-marburg.de/fb02/makro/forschung/magkspapers Coordination: Bernd Hayo • Philipps-University Marburg School of Business and Economics • Universitätsstraße 24, D-35032 Marburg Tel: +49-6421-2823091, Fax: +49-6421-2823088, e-mail: [email protected] Entry deterrence due to brand proliferation: Empirical evidence from the German interurban bus industry Samuel de Haas∗y Daniel Herold ∗ Jan Thomas Sch¨afer∗. July 27, 2018 Abstract In 2016, the largest operator in the German interurban bus industry, Flixbus, acquired its major rival, Postbus. We study the effects of that takeover using route-level data covering more than 6,000 routes. We find that Flixbus, on average, provided a lower fre- quency of bus rides and slightly decreased prices after the takeover. This indicates that Flixbus pursued a strategy of preemption: to decrease residual demand for Postbus, Flixbus offered a high number of bus rides. After the takeover, Flixbus decreased the supply of transportation services and lowered the prices to compensate the consumers for the resulting increase in inconvenience costs.1 JEL codes: L11, L41, L92, K21, K23 Keywords: Competition, Takeover, Interurban Bus Services, Brand Proliferation, Entry Deterrence ∗Chair for Industrial Organization, Regulation and Antitrust, Department of Economics, Justus-Liebig- University Giessen. Licher Strasse 62, 35394 Giessen, Germany yCorresponding author, e-mail: [email protected]. -

2009-041 Crosscountry Spanner Awards

Press Release 04 December 2009 XC2009/041 (LW) CROSSCOUNTRY TOPS RAILWAY CHARTS It’s Gold and Silver for award-winning train operator CrossCountry has won two prestigious rail industry awards in recognition of its trains being one of the most improved and reliable fleets across Britain’s rail network. CrossCountry was awarded Gold and Silver at last week’s annual ‘Golden Spanner’ ceremony organised by industry magazine Modern Railways. The Golden Spanner went to the Class 221 Super Voyagers for taking first place in the ‘Modern DMU’ category as the most reliable fleet in its class. The Super Voyagers also took the Silver Spanner for being the most improved fleet thanks to reliability being up 118% on last year. The ‘Golden Spanner’ is an awards scheme aimed at promoting excellence in train maintenance within Britain. Sarah Kendall, Production Director at CrossCountry said: “We are extremely proud to win these nationally recognised awards. Since the start of our franchise in November 2007 the team at CrossCountry has worked very closely with Bombardier Transportation, our maintainer to take specific targeted steps to improve the reliability of our Voyager trains. Our focus now is to build on this significant progress and further improve our performance. Train reliability is vital for our customers and therefore of the highest priority for us.” All trains are ranked on the distance they cover between technical faults by the Association of Train Operating Companies’ (ATOC) National Fleet Reliability Improvement Programme. Using this league table (see below) CrossCountry’s Voyager trains outperformed all other intercity fleets across the country. -

Operator Profile 2002 - 2003

BUS OPERATOR PROFILE 2002 - 2003 Operator .Insp 02-03 .OOS 02-03 OOS Rate 02-03 OpID City Region 112 LIMOUSINE INC. 2 0 0.0 28900 CENTER MORICHES 10 1ST. CHOICE AMBULETTE SERVICE LCC 1 0 0.0 29994 HICKSVILLE 10 2000 ADVENTURES & TOURS INC 5 2 40.0 26685 BROOKLYN 11 217 TRANSPORTATION INC 5 1 20.0 24555 STATEN ISLAND 11 21ST AVE. TRANSPORTATION 201 30 14.9 03531 BROOKLYN 11 3RD AVENUE TRANSIT 57 4 7.0 06043 BROOKLYN 11 A & A ROYAL BUS COACH CORP. 1 1 100.0 30552 MAMARONECK 08 A & A SERVICE 17 3 17.6 05758 MT. VERNON 08 A & B VAN SERVICE 4 1 25.0 03479 STATEN ISLAND 11 A & B'S DIAL A VAN INC. 23 1 4.3 03339 ROCKAWAY BEACH 11 A & E MEDICAL TRANSPORT INC 60 16 26.7 06165 CANANDAIGUA 04 A & E MEDICAL TRANSPORT INC. 139 29 20.9 05943 POUGHKEEPSIE 08 A & E TRANSPORT 4 0 0.0 05508 WATERTOWN 03 A & E TRANSPORT SERVICES 39 1 2.6 06692 OSWEGO 03 A & E TRANSPORT SERVICES INC 154 25 16.2 24376 ROCHESTER 04 A & E TRANSPORT SERVICES INC. 191 35 18.3 02303 OSWEGO 03 A 1 AMBULETTE INC 9 0 0.0 20066 BROOKLYN 11 A 1 LUXURY TRANSPORTATION INC. 4 2 50.0 02117 BINGHAMTON 02 A CHILDCARE OF ROOSEVELT INC. 5 1 20.0 03533 ROOSEVELT 10 A CHILD'S GARDEN DAY CARE 1 0 0.0 04307 ROCHESTER 04 A CHILDS PLACE 12 7 58.3 03454 CORONA 11 A J TRANSPORTATION 2 1 50.0 04500 NEW YORK 11 A MEDICAL ESCORT AND TAXI 2 2 100.0 28844 FULTON 03 A&J TROUS INC. -

European Postal Services and Social Responsibilities

European Postal Services and Social Responsibilities How post offices enhance their economic, social and environmental role in society With the support of the European Social Fund, PIC Adapt With the support of European © Olivier Cahay in cooperation with with the support of www.csreurope.org This report was prepared byCSR Europe in cooperation with the Corporate Citizenship Company in the framework of a yearlong project initiated by La Poste and with the support of the EU ADAPT Programme 3 4 European Postal Services and Social Responsibilities 35 6 TABLE OF CONTENTS Acknowledgments Foreword 7 Executive summary 10 1. Introduction: background, methodology and aim of the report 12 2. Trends in Corporate Social Responsibility at European and international levels 2.1 A new paradigm in Europe 14 2.2 Corporate Social Responsibility – drivers of change 14 2.3 CSR – an evolving approach 16 2.4 Developments at European and international levels 17 3. Debate over developments in the European postal sector 3.1 Internal market for European postal services 19 3.2 Universal service safeguards 20 3.3 Pan-European co-ordination 20 3.4 Future trends 21 4. Social responsibility in action 4.1 Diversity and equal opportunity in the workforce 23 4.2 Training and career development 26 4.3 Health and safety 29 4.4 Social dialogue and employee consultation 31 4.5 Access to services for disadvantaged groups and local regeneration 32 4.6 Community involvement and charities 34 4.7 Environment 35 5. Going forwa r d: conclusions and rec o m m e n d a t i o n s 39 Appendix: The research process and roundtable discussions 41 Disclaimer: while every effort has been made to check that the contents of this report were correct at time of printing, the publishers retain sole responsibility for the contents.