MCIL2 Examiner's Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

KINGSTON Upon THAMES - LOCAL SERVICES April 2014 KINGSTON Upon THAMES

KINGSTON upon THAMES - LOCAL SERVICES April 2014 KINGSTON upon THAMES 1. SPEECH AND LANGUAGE THERAPY SERVICE(s) Your Health Care www.yourhealthcare.org/Services/speech-and-language-therapy.htm Various clinics & locations Pre-school children: Carmel Brady 020 8274 7814 online email form School age children: Linda Talbot 020 8547 6670 SLT at Services for Disabled Children, The Moor Lane Centre 020 8547 6527 www.kingston.gov.uk/info/200247/supporting_disabled_children_and_their_families/510/services_for_disabled_children/7 2. Royal Borough of KINGSTON upon THAMES 020 8547 5000 www.kingston.gov.uk Guildhall, High Street, Kingston upon Thames KT1 1EU [email protected] • SPECIAL EDUCATIONAL NEEDS Special Educational Needs 020 8547 5004 www.kingston.gov.uk/info/200230/special_education_needs_sen Children, Schools and Families, [email protected] Guildhall 2, High Street, Kingston upon Thames KT1 1EU • EDUCATIONAL PSYCHOLOGY Educational Psychology Team The Moor Lane Centre, Moor Lane, Chessington, Surrey KT9 2AA (referral through schools only) 3. SCHOOLS with specialist Speech and Language provision The following school has specialist provision for Speech & Language difficulties: Castle Hill Primary School 020 8397 2006 www.castlehill.kingston.sch.uk Buckland Road, Chessington, Surrey KT9 1JE [email protected] 4. PARENT PARTNERSHIP EnhanceAble Anna Fayda: PPS officer 020 8547 6200 www.enhanceable.org/parentpartnership.htm EnhanceAble Children's Services, The Moor Lane Centre, [email protected] Moor Lane, Chessington, Surrey KT9 2AA 5. PARENT and CARER FORUM Kingston Parents Forum 020 8546 3258 http://e-voice.org.uk/parentsforum/ KINGSTON upon THAMES - LOCAL SERVICES April 2014 53-55 Canbury Park Road, Kingston upon Thames, Surrey KT2 6LQ [email protected] 6. -

The Growth of London Through Transport Map of London’S Boroughs

Kingston The growth of London through transport Map of London’s boroughs 10 The map shows the current boundaries of London’s Key boroughs. The content of 2 1 Barking 17 Hillingdon this album relates to the & Dagenham 15 31 18 Hounslow area highlighted on the map. 14 26 2 Barnet 16 19 Islington This album is one of a 3 Bexley 20 Kensington series looking at London 17 4 6 12 19 4 Brent & Chelsea boroughs and their transport 1 25 stories from 1800 to the 5 Bromley 21 Kingston 9 30 present day. 33 7 6 Camden 22 Lambeth 23 Lewisham 7 City of London 13 20 28 8 Croydon 24 Merton 18 11 3 9 Ealing 25 Newham 22 32 23 26 Redbridge 27 10 Enfield 11 Greenwich 27 Richmond 28 Southwark 24 12 Hackney 29 Sutton Kingston 13 Hammersmith 21 5 & Fulham 30 Tower Hamlets 29 8 14 Haringey 31 Waltham Forest 15 Harrow 32 Wandsworth 16 Havering 33 Westminster A3 RICHMOND RIVER A307 THAMES ROAD KINGSTON A308 UPON Kingston Hill THAMES * * Kings Road Kingston A238 Turks Pier Norbiton * * Bentalls A3 * Market Place NEW * Cambridge* A2043 Road MALDEN Estates New Malden A307 Kingston Bridge Berrylands KINGSTON SURBITON RIVER THAMES UPON KINGSTON BY PASS THAMES Surbiton A240 A3 Malden Beresford Avenue* Manor Worcester Park A243 A309 A240 A3 Tolworth Haycroft* Estate HOOK A3 0 miles ½ 1 Manseld* Chessington Road North 0 kilometres 1 Chessington South A243 A3 A243 * RBK. marked are at theLocalHistoryRoom page. Thoseinthecollection atthebottomofeach are fortheimages References the book. can befoundatthebackof contributing tothisalbum Details ofthepartner theseries. -

THOMSON REUTERS MAP.Ai

PUBLIC TRANSPORT PUBLIC TRANSPORT Watford M Hatfield A1 2 LIMEHOUSE DOCKLAND 1 M25 1 DLR 1 N TRAIN STATION LIGHT RAILWAY M Hendon A1 27 Situated on Commercial Road Canary Wharf Station. Situated High A406 (A13), walk to the Limehouse at the centre of North and South Wycombe Basildon The Thomson Reuters Building M 2 DLR Station and catch a Colonnade. The Station is a two M4 5 South Colonnade 0 A40 A1 3 connecting train to Canary minute walk from our building. A1 3 Slough Canary Wharf Wharf. CITY OF • London C ity LONDON Airport London M4 Tilbury LONDON CITY LONDON UNDERGROUND • A20 5 2 E14 5ep CANARY WHARF • AIRPORT Heathrow A205 M Airport Jubilee Line Extention – links Catch a connecting London Gravesend A3 Croydon Canary Wharf with Waterloo City Airport shuttle bus to SECTION M 2 +44 (0)20 7250 1122 0 Station and London Bridge, Canary Wharf DETAILED M3 BELOW M25 thomsonreuters.com also other tube lines. Wok ing Limehouse MANOR Train Station A Docklands B BURDETT 1 ROAD 1 0 A1 206 2 ROAD Blackwell Tunnel 2 Isle of Dogs 1 Dover A1 02 N C anary Wharf WESTFERRY C IRC US (A1 3) Folkestone COMMERCIAL Royal Docks ROAD C ity 3 C anary A1 Wharf Airport C . London A1 3 One Way COMMERCIAL EAST INDIA ROAD C abot Square DOCK ROAD A1 3 L I M E H O U S E P P C anary Wharf Start here DLR A1 3 A1 3 From the East To Tower Gateway A L L (A1 3) & Central London 6 S A I N T S 0 2 1 P O P L A R Start here W E S T F E R R Y A C . -

Local Support Services Guide

LOCAL SUPPORT SERVICES GUIDE Kingston Race and Equalities Council Neville House 55 Eden Street Kingston upon Thames Surrey KT1 1BW Phone: 0208 547 2332 Fax: 0208 547 1510 Website: www.kingstonrec.org Asylum and Immigration Tribunal (A.I.T.) 17 Ewell Road Sessions House Surbiton Surrey, KT6 6AQ Tel: 0845 6000 877 Website: www.ait.gov.uk Refugee Action Kingston Kathryn Betham Siddeley House, 50 Canbury Park Road, Kingston Upon Thames, Surrey KT26LX Tel:020 8547 0115 Fax: 020 8547 1114 Website: www.refugeeactionkingston.org.uk Kingston Racial Equality Council. John Azah, DirectorWelcare House53-55 Canbury Park RoadKingston upon Thames Surrey KT26LQ Tel: 020 8547 2332 Website: www.kingstonrec.org Kingston Interpreting Service Barbara Morton: Guildhall 1 Kingston upon Thames KT11EU Tel: 020 8547 5822 Kingston Churches Action for Homeless People 36a Fife Rd, Kingston upon Thames, Surrey KT1 1SU Telephone: 020 8255 7400 Website: www.kcah.org.uk Gypsy & Traveller Education Service Co-ordinator (Royal Borough of Kingston Traveller Education Service) Tel: 07826 955 967 Website: www.kingston.gov.uk/gypsyandtravellersupportservice.htm Domestic Violence - Domestic Violence Helpline: 0808 2000 247 this is a free 24 hour helpline run by women’s aid and refuge Website: www.kingston.gov.uk/domestic_violence - Kingston Domestic Violence One Stop Shop is a service providing information and confidential support to people who have experienced domestic violence. It is held every Monday 9.30am to 12.30pm In the Baptist Church Union Street Kingston KT1 1RP - -

19+Neville+Avenue.Pdf

Amberwood 19 Neville Avenue, New Malden, Surrey, KT3 4SN GUIDE PRICE £4,250,000 WWW.COOMBERESIDENTIAL.COM LOCATION Neville Avenue is one of the premiere roads within the exclusive Coombe House Private estate which is approached from top off Traps Lane or from Warren Rise off Coombe Lane West. This wonderfully friendly estate is equidistant between Kingston and Wimbledon town centres. Both have excellent shopping facilities, from department stores housing concessions found in famous West End streets and specialised boutiques to a wide range of restaurants meeting the palates from across the world. The A3 trunk road offers fast access to central London and both Gatwick and Heathrow airports via the M25 motorway network. The nearest train station at New Malden is within walking distance and the 57 bus route runs along nearby Coombe Lane West to Wimbledon from where there are frequent services to Waterloo with its underground links to points throughout the city. The immediate area offers a wide range of recreational facilities including five golf courses, tennis and squash clubs and many leisure centres. The 2,360 acres of Richmond Park, an area of outstanding beauty easily accessed from Kingston Gate and Ladderstile Gate, provide a picturesque setting in which to picnic, go horse riding, jogging or just take a leisurely walk. Theatres at Wimbledon and Richmond are also popular alternatives to the West End. There are numerous excellent local schools for all ages, private, state and a variety of international educational establishments, many within walking distance. The Coombe House private estate is extremely well run and managed by the residents. -

PORTSMOUTH ROAD the Thames Landscape Strategy Review 1 9 7

REACH 03 PORTSMOUTH ROAD The Thames Landscape Strategy Review 1 9 7 Landscape Character Reach No 3 PORTSMOUTH ROAD 4.03.1 Overview 1994-2012 • Construction of new cycle/footpath along Barge Walk and the opening of views across the river • Habitat enhancement in the Home Park including restoration of acid grassland • Long-running planning process for the Seething Wells fi lter beds • TLS initiative to restore the historic Home Park water meadows. • RBKuT Kingston Town Centre Area Action Plan K+20 • RBK and TLS Integrated Moorings Business Plan • Management of riverside vegetation along the Barge Walk • Restoration of the Long Water Avenue in 2006 LANDSCAPE CHARACTER 4.03.2 The Portsmouth Road Reach runs north from Seething Wells up to Kingston. The reach has a character of wide open grassland, interrupted only by trees, park and water-works walls and the Portsmouth Road blocks of fl ats. Hampton Court Park extends over the entire Middlesex side right up to Hampton Wick, while the Surrey bank divides between the former Water Works and the Queen’s Promenade. The Portsmouth Road follows the river the length of the reach on the Surrey side. This is one of the only sections of the upstream London Thames where a road has been built alongside the river. The busy road and associated linear developments make a harsh contrast with the rhythm of parkland and historic town waterfronts which characterise the rest of the river. Portsmouth Road 4.03.3 Hampton Court Park is held in the circling sweep of the Thames, as its fl ow curves from south to north. -

Leamouth Leam

ROADS CLOSED SATURDAY 05:00 - 21:00 ROADS CLOSED SUNDAY 05:00TO WER 4 2- 12:30 ROADS CLOSED SUNDAY 05:00 - 14:00 3 3 ROUTE MAP ROADS CLOSED SUNDAY 05:00 - 18:00 A1 LEA A1 LEA THE GHERR KI NATCLIFF RATCLIFF RATCLIFF CANNING MOUTH R SATURDAY 4th AUGUST 05:00 – 21:00 MOUTH R SUNDAY 5th AUGUST 05:00 – 14:00 LIMEHOUSE WEST BECKTON AD AD BANK OF WHITECHAPEL BECKTON DOCK RO SUNDAY 5th AUGUST 14:00 – 18:00 TOWN OREGANO DRIVE OREGANO DRIVE CANNING LLOYDS BUILDING SOUTH ST PAUL S ENGL AND Limehouse DLR SEE MAP CUSTOM HOUSE EAST INDIA O EAST INDIA DOCK RO O ROYAL OPER A AD AD CATHED R AL LEAMOUTH DLR PARK OHO LIMEHOUSE LIMEHOUSBecktonE Park Y Y HOUSE Cannon Street Custom House DLR Prince Regent DLR Cyprus DLR Gallions Reach DLR BROMLEY RIGHT A A ROADS CLOSED SUNDAY 05:00 - 18:00 Royal Victoria DLR W W Mansion House COVENT Temple Blackfriars POPLAR DLR DLR Tower Gateway LE A MOUTH OCEA OCEA Monument COMMERC COMMERC V V GARDEN IAL ROAD East India RO UNDABOU T IAL ROAD ExCEL UNIVERSI T Y ROYAL ALBERT SIL SIL ITETIONAL CHASOPMERSETEL Tower Hill Blackwall DLR OF EAST LONDON SEE MAP BELOW RT R AIT HOUSE MILLENIUM ROUNDABOUT DLR Poplar E TOWN GALLE RY BRIDGE A13 VENU A13 VENUE SAFFRON A SAFFRON A SOUTHWARK THE TO WER Westferry DLR DLR BLACKWALL Embankment ROTHERHITH E THE MUSEUM AD AD CLEOPATRA’S BRIDGE OF LONDON EAST INDIA DOCK RO EAST INDIA DOCK RO LONDON WAPPING T UNNEL OF LONDON West India A13 A13 LEAMOUTH NEED LE SHADWELL LONDON CI T Y BRIDGE DOCK L A NDS Quay BILLINGSGATE AIRPOR T A13 K WEST INDIA DOCK RD K WEST INDIA DOCK RD LEA IN M ARKET IN LEAM RATCLIFF L L SE SE MOUT WAY TATE MODERN HMS BELFAST U U SPEN O O AD A N H H A AY A N W E TOWER E E 1 ASPEN 1 H R W E G IM IM 2 2 L L OREGANO DRIVE 0 W 0 OWER LEA CROSSING L CANNING P LOWER LEA CROSSIN BRIDGE 6 O 6 O EAST INDIA DOCK RO POR AD R THE O2 BL ACK WAL L Y T LIMEHOUSE PR ESTO NS A T A A C C HORSE SOUTHWARK W V RO AD T UNNEL O O E V T T . -

Mobile-Friendly Guide

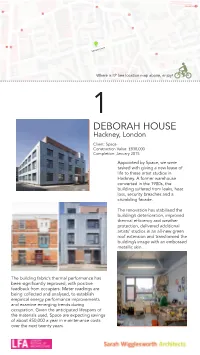

Retreat place Where is it? See location map above, enjoy! 1 DEBORAH HOUSE Hackney, London Client: Space Construction Value: £838,000 Completion: January 2015 Appointed by Space, we were tasked with giving a new lease of life to these artist studios in Hackney. A former warehouse converted in the 1980s, the building suffered from leaks, heat loss, security breaches and a crumbling facade. The renovation has stabilised the building’s deterioration, improved thermal efficiency and weather protection, delivered additional artists’ studios in an all-new green roof extension and transformed the building’s image with an embossed metallic skin. The building fabric’s thermal performance has been significantly improved, with positive feedback from occupiers. Meter readings are being collected and analysed, to establish empirical energy performance improvements and examine emerging trends during occupation. Given the anticipated lifespans of the materials used, Space are expecting savings of about £50,000 a year in maintenance costs over the next twenty years. Tower Bridge Rd Where is it? See location map above, enjoy! 2 BERMONDSEY BICYCLE STORE Bermondsey, London Client: Igloo Regeneration Construction Value: £120,000 Completion: 2008 Bermondsey Bicycle Store forms a striking entrance to Bermondsey Square – a lively public space at the heart of an ambitious regeneration project in south-east London. Embedding green transport values within the local community, the store accommodates 76 bikes belonging to the square’s workers and residents. Using ordinary materials in an original and exciting manner, the intervention adds sparkle to Igloo’s vision for inner city living. Drawing on the narrative of silver trinkets and treasures past, the landscaping is conceived as a textured carpet adorned with jewel-like street objects. -

The Crystal Palace

The Crystal Palace The Crystal Palace was a cast-iron and plate-glass structure originally The Crystal Palace built in Hyde Park, London, to house the Great Exhibition of 1851. More than 14,000 exhibitors from around the world gathered in its 990,000-square-foot (92,000 m2) exhibition space to display examples of technology developed in the Industrial Revolution. Designed by Joseph Paxton, the Great Exhibition building was 1,851 feet (564 m) long, with an interior height of 128 feet (39 m).[1] The invention of the cast plate glass method in 1848 made possible the production of large sheets of cheap but strong glass, and its use in the Crystal Palace created a structure with the greatest area of glass ever seen in a building and astonished visitors with its clear walls and ceilings that did not require interior lights. It has been suggested that the name of the building resulted from a The Crystal Palace at Sydenham (1854) piece penned by the playwright Douglas Jerrold, who in July 1850 General information wrote in the satirical magazine Punch about the forthcoming Great Status Destroyed Exhibition, referring to a "palace of very crystal".[2] Type Exhibition palace After the exhibition, it was decided to relocate the Palace to an area of Architectural style Victorian South London known as Penge Common. It was rebuilt at the top of Town or city London Penge Peak next to Sydenham Hill, an affluent suburb of large villas. It stood there from 1854 until its destruction by fire in 1936. The nearby Country United Kingdom residential area was renamed Crystal Palace after the famous landmark Coordinates 51.4226°N 0.0756°W including the park that surrounds the site, home of the Crystal Palace Destroyed 30 November 1936 National Sports Centre, which had previously been a football stadium Cost £2 million that hosted the FA Cup Final between 1895 and 1914. -

New Southwark Plan BACKGROUND PAPER

New Southwark Plan BACKGROUND PAPER Offices December 2019 1 Contents 1. Executive Summary ............................................................................................. 3 2. Policy Background ............................................................................................... 5 3. Southwark’s approach to office development .................................................... 23 4. Research and Evidence Base for London ......................................................... 24 5. Research and Evidence Base for Southwark .................................................... 41 6. Delivery of Offices and Business Development in Southwark ........................... 51 7. Marketing Strategy for office and business development in Southwark ............. 55 8. Summary ........................................................................................................... 56 Appendix 1 - LDD Appendix 2 – Guidance on Marketing Statements Glossary AAP – Area Action Plan CAZ – Central Activities Zone CIL – Community Infrastructure Levy ELR - Employment Land Review FTE – Full time equivalent GIA – Gross Internal Area GEA – Gross External Area GLA – Greater London Authority LDD – London Development Database MSEs – Micro and Small Enterprises NIOD – Northern part of the Isle of Dogs NPPF – National Planning Policy Framework NSP – New Southwark Plan NSP PSV – New Southwark Plan Proposed Submission Version PDR – Permitted Development Rights SPD – Supplementary Planning Guidance 2 1. Executive Summary 1.1 There is a need -

The Isle of Dogs: Four Development Waves, Five Planning Models, Twelve

Progress in Planning 71 (2009) 87–151 www.elsevier.com/locate/pplann The Isle of Dogs: Four development waves, five planning models, twelve plans, thirty-five years, and a renaissance ... of sorts Matthew Carmona * The Bartlett School of Planning, UCL, 22 Gordon Street, London WC1H 0QB, United Kingdom Abstract The story of the redevelopment of the Isle of Dogs in London’s Docklands is one that has only partially been told. Most professional and academic interest in the area ceased following the property crash of the early 1990s, when the demise of Olympia & York, developers of Canary Wharf, seemed to bear out many contemporary critiques. Yet the market bounced back, and so did Canary Wharf, with increasingly profound impacts on the rest of the Island. This paper takes an explicitly historical approach using contemporaneous professional critiques and more reflective academic accounts of the planning and development of the Isle of Dogs to examine whether we can now conclude that an urban renaissance has taken place in this part of London. An extensive review of the literature is supplemented with analysis of physical change on the ground and by analysis of the range of relevant plans and policy documents that have been produced to guide development over the 35-year period since the regeneration began. The paper asks: What forms of planning have we seen on the Island; what role has design played in these; what outcomes have resulted from these processes; and, as a result, have we yet seen an urban renaissance? # 2009 Elsevier Ltd. All rights reserved. Keywords: Isle of Dogs; Urban design; Planning; Urban renaissance Contents 1. -

404 Ewell Road TOLWORTH Surrey KT6 7HG New Lease Or

020 7493 9911 15 Bolton Street, Mayfair, London, W1J 8BG w: www.ianscott.com 402 – 404 Ewell Road TOLWORTH Surrey KT6 7HG New Lease or Freehold ( with VP ) Available Location: Tolworth is a popular London suburb some 3 miles south of Kingston Upon Thames whilst close to Surbiton, New Malden and Wimbledon with excellent road communications to the A3, and therefore easy access to both Central London and M25 motorway. The famous 22 storey Tolworth Tower nearby has recently received planning consent for conversion of the offices into over 100 new homes as well as 68 serviced apartments. The property is prominently situated just off the Broadway in a parade of other shops with on street parking available at the front. Nearby occupiers include B & M, Sainsbury Local, Iceland, Tesco Express / Esso Garage and M & S Simply Food. Accommodation: The property comprises the following approximate dimensions and floor areas - Net Frontage - 41' ( 12.49 m ) Internal Width - 40' 7'' (12.36 m ) Shop Depth - 40' 4'' ( 12.29 m ) Built Depth - 73' 4'' ( 22.35 m ) Ground Floor retail - 1890 sq ft ( 175.5 sq m ) Ground Floor - Rear External Self contained storeroom - 656 sq ft ( 61 sq m ) First Floor Offices / ancillary / WC's - 1508 sq ft ( 140 sq m ) Tenure: The property is available (subject to agreeing vacant possession ) on a new lease for a term to be agreed seeking rental offers of £50,000 pax. Freehold: Our client may also consider a FH sale (with full vacant possession) seeking offers in excess of £675,000 excl. Vat .