Vehicle Use Tax and Calculator Questions and Answers

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Creating Market Incentives for Greener Products Policy Manual for Eastern Partnership Countries

Creating Market Incentives for Greener Products Policy Manual for Eastern Partnership Countries Creating Incentives for Greener Products Policy Manual for Eastern Partnership Countries 2014 About the OECD The OECD is a unique forum where governments work together to address the economic, social and environmental challenges of globalisation. The OECD is also at the forefront of efforts to understand and to help governments respond to new developments and concerns, such as corporate governance, the information economy and the challenges of an ageing population. The Organisation provides a setting where governments can compare policy experiences, seek answers to common problems, identify good practice and work to co-ordinate domestic and international policies. The OECD member countries are: Australia, Austria, Belgium, Canada, Chile, the Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Iceland, Ireland, Israel, Italy, Japan, Korea, Luxembourg, Mexico, the Netherlands, New Zealand, Norway, Poland, Portugal, the Slovak Republic, Slovenia, Spain, Sweden, Switzerland, Turkey, the United Kingdom and the United States. The European Union takes part in the work of the OECD. Since the 1990s, the OECD Task Force for the Implementation of the Environmental Action Programme (the EAP Task Force) has been supporting countries of Eastern Europe, Caucasus and Central Asia to reconcile their environment and economic goals. About the EaP GREEN programme The “Greening Economies in the European Union’s Eastern Neighbourhood” (EaP GREEN) programme aims to support the six Eastern Partnership countries to move towards green economy by decoupling economic growth from environmental degradation and resource depletion. The six EaP countries are: Armenia, Azerbaijan, Belarus, Georgia, Republic of Moldova and Ukraine. -

City of San Marcos Sales Tax Update Q22018 Third Quarter Receipts for Second Quarter Sales (April - June 2018)

City of San Marcos Sales Tax Update Q22018 Third Quarter Receipts for Second Quarter Sales (April - June 2018) San Marcos SALES TAX BY MAJOR BUSINESS GROUP In Brief $1,400,000 2nd Quarter 2017 $1,200,000 San Marcos’ receipts from April 2nd Quarter 2018 through June were 3.9% below the $1,000,000 second sales period in 2017 though the decline was the result of the State’s transition to a new software $800,000 and reporting system that caused a delay in processing thousands of $600,000 payments statewide. Sizeable local allocations remain outstanding, par- $400,000 ticularly for home furnishings, build- ing materials, service stations and $200,000 casual dining restaurants. Partial- ly offsetting these impacts, the City received an extra department store $0 catch-up payment that had been General Building County Restaurants Business Autos Fuel and Food delayed from last quarter due to the Consumer and and State and and and Service and Goods Construction Pools Hotels Industry Transportation Stations Drugs same software conversion issue. Excluding reporting aberrations, ac- tual sales were up 3.0%. Progress was led by higher re- TOP 25 PRODUCERS ceipts at local service stations. The IN ALPHABETICAL ORDER REVENUE COMPARISON price of gas has been driven high- ABC Supply Co Hughes Water & Four Quarters – Fiscal Year To Date (Q3 to Q2) Sewer er over the past year by simmering Albertsons Hunter Industries global political tension and robust Ashley Furniture 2016-17 2017-18 economic growth that has lifted de- Homestore Jeromes Furniture mand. Best Buy Kohls Point-of-Sale $14,377,888 $14,692,328 The City also received a 12% larg- Biggs Harley KRC Rock Davidson County Pool er allocation from the countywide Landsberg Orora 2,217,780 2,261,825 use tax pool. -

Bundle of S Cks—Real Property Rights and Title Insurance Coverage

Bundle of Scks—Real Property Rights and Title Insurance Coverage Marc Israel, Esq. What Does Title Insurance “Insure”? • Title is Vested in Named Insured • Title is Free of Liens and Encumbrances • Title is Marketable • Full Legal Use and Access to Property Real Property Defined All land, structures, fixtures, anything growing on the land, and all interests in the property, which may include the right to future ownership (remainder), right to occupy for a period of +me (tenancy or life estate), the right to build up (airspace) and drill down (minerals), the right to get the property back (reversion), or an easement across another's property.” Bundle of Scks—Start with Fee Simple Absolute • Fee Simple Absolute • The Greatest Possible Rights Insured by ALTA 2006 Policy • “The greatest possible estate in land, wherein the owner has the right to use it, exclusively possess it, improve it, dispose of it by deed or will, and take its fruits.” Fee Simple—Lots of Rights • Includes Right to: • Occupy (ALTA 2006) • Use (ALTA 2006) • Lease (Schedule B-Rights of Tenants) • Mortgage (Schedule B-Mortgage) • Subdivide (Subject to Zoning—Insurable in Certain States) • Create a Covenant Running with the Land (Schedule B) • Dispose Life Estate S+ck • Life Estate to Person to Occupy for His Life+me • Life Estate can be Conveyed but Only for the Original Grantee’s Lifeme • Remainderman—Defined in Deed • Right of Reversion—Defined in Deed S+cks Above, On and Below the Ground • Subsurface Rights • Drilling, Removing Minerals • Grazing Rights • Air Rights (Not Development Rights—TDRs) • Canlever Over a Property • Subject to FAA Rules NYC Air Rights –Actually Development Rights • Development Rights are not Real Property • Purely Statutory Rights • Transferrable Development Rights (TDRs) Under the NYC Zoning Resoluon and Department of Buildings Rules • Not Insurable as They are Not Real Property Title Insurance on NYC “Air Rights” • Easement is an Insurable Real Property Interest • Easement for Light and Air Gives the Owner of the Merged Lots Ability to Insure. -

Westvirginia

W E S T V I R G I N I A DEPARTMENT OF REVENUE Joint Select Committee on Tax Reform Current Tax Structure DEPUTY REVENUE SECRETARY MARK B. MUCHOW West Virginia State Capitol May 4, 2015 Secretary Robert S. Kiss Governor Earl Ray Tomblin Some Notes Concerning Taxation • Tax = price paid for government goods and services – Higher price = less demand (budget surplus) – Lower price = more demand • Federal deficit spending • Exporting of tax (e.g., Destination gaming, tourism, certain taxes) • All taxes are paid by individuals – economic incidence • Two principles of taxation – Ability to Pay (Federal Government) – Benefits (State and Local Governments) • Three broad categories of taxation – Property (Real estate taxes, ad valorem tax, franchise tax) – Consumption (General sales, gross receipt, excise) – Income (personal income, profits, wages, dividends) State and Local Government Expenditures 2011: WV Ranks 14th in Per Pupil K-12 Education Funding; 16th in Per Capita Higher Education Funding; 11th in Per Capita Highways Funding; 48th in Per Capita Police Protection Sources: U.S. Census Bureau & State Higher Education Executive Officers Association Historical Events Shape Tax System • Prohibition: (WV goes Dry in 1914: New Tax System ) – Move to State consumption taxes (B&O and gasoline) • Great Depression of the 1930s – Property Tax Revolt (Move toward government centralization) – Move to more State consumption taxation (Sales Tax and more) – Roads transferred from counties to State • Educating Baby Boomers in 1960s: – Higher sales tax rates -

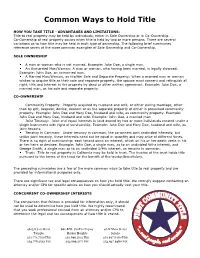

Common Ways to Hold Title

Common Ways to Hold Title HOW YOU TAKE TITLE - ADVANTAGES AND LIMITATIONS: Title to real property may be held by individuals, either in Sole Ownership or in Co-Ownership. Co-Ownership of real property occurs when title is held by two or more persons. There are several variations as to how title may be held in each type of ownership. The following brief summaries reference seven of the more common examples of Sole Ownership and Co-Ownership. SOLE OWNERSHIP A man or woman who is not married. Example: John Doe, a single man. An Unmarried Man/Woman: A man or woman, who having been married, is legally divorced. Example: John Doe, an unmarried man. A Married Man/Woman, as His/Her Sole and Separate Property: When a married man or woman wishes to acquire title as their sole and separate property, the spouse must consent and relinquish all right, title and interest in the property by deed or other written agreement. Example: John Doe, a married man, as his sole and separate property. CO-OWNERSHIP Community Property: Property acquired by husband and wife, or either during marriage, other than by gift, bequest, devise, descent or as the separate property of either is presumed community property. Example: John Doe and Mary Doe, husband and wife, as community property. Example: John Doe and Mary Doe, husband and wife. Example: John Doe, a married man Joint Tenancy: Joint and equal interests in land owned by two or more individuals created under a single instrument with right of survivorship. Example: John Doe and Mary Doe, husband and wife, as joint tenants. -

Common Ways of Holding Title to Real Property

NORTH AMERICAN TITLE COMPANY Common Ways of Holding Title to Real Property Tenancy in Common Joint Tenancy Parties Any number of persons. Any number of persons. (Can be husband and wife) (Can be husband and wife) Division Ownership can be divided into any number of Ownership interests cannot be divided. interests, equal or unequal. Title Each co-owner has a separate legal title to his There is only one title to the entire property. undivided interest. Possession Equal right of possession. Equal right of possession. Conveyance Each co-owner’s interest may be conveyed Conveyance by one co-owner without the separately by its owner. others breaks the joint tenancy. Purchaser’s Status Purchaser becomes a tenant in common with Purchaser becomes a tenant in common with other co-owners. other co-owners. Death On co-owner’s death, his interest passes by On co-owner’s death, his interest ends and will or intestate succession to his devisees or cannot be willed. Surviving joint tenants heirs. No survivorship right. own the property by survivorship. Successor’s Status Devisees or heirs become tenants in common. Last survivor owns property in severalty. Creditor’s Rights Co-owner’s interest may be sold on execution Co-owner’s interest may be sold on execu- sale to satisfy his creditor. Creditor becomes a tion sale to satisfy creditor. Joint tenancy is tenant in common. broken, creditor becomes tenant in common. Presumption Favored in doubtful cases. None. Must be expressly declared. This is provided for informational puposes only. Specific questions for actual real property transactions should be directed to your attorney or C.P.A. -

The High Burden of State and Federal Capital Gains Tax Rates in the United FISCAL FACT States Mar

The High Burden of State and Federal Capital Gains Tax Rates in the United FISCAL FACT States Mar. 2015 No. 460 By Kyle Pomerleau Economist Key Findings · The average combined federal, state, and local top marginal tax rate on long-term capital gains in the United States is 28.6 percent – 6th highest in the OECD. · This is more than 10 percentage points higher than the simple average across industrialized nations of 18.4 percent, and 5 percentage points higher than the weighted average. · Nine industrialized countries exempt long-term capital gains from taxation. · California has the 3rd highest top marginal capital gains tax rate in the industrialized world at 33 percent. · The taxation of capital gains places a double-tax on corporate income, increases the cost of capital, and reduces investment in the economy. · The President’s FY 2016 budget would increase capital gains tax rates in the United States from 28.6 percent to 32.8, the 5th highest rate in the OECD. 2 Introduction Saving is important to an economy. It leads to higher levels of investment, a larger capital stock, increased worker productivity and wages, and faster economic growth. However, the United States places a heavy tax burden on saving and investment. One way it does this is through a high top marginal tax rate on capital gains. Currently, the United States’ top marginal tax rate on long-term capital gains income is 23.8 percent. In addition, taxpayers face state and local capital gains tax rates between zero and 13.3 percent. As a result, the average combined top marginal tax rate in the United States is 28.6 percent. -

Moving to Arkansas a Tax Guide for New Residents 2017 Tax Year

Moving to Arkansas A Tax Guide for New Residents 2017 Tax Year Facts about Arkansas The scenic beauty of the Natural State appeals to travelers from all over the country. Among the state’s greatest assets are its six national park sites, 2.6 million acres of national forest lands, 13 major lakes, and two mountain ranges. Scenic drives lead to breathtaking vistas in the Ozarks and the Ouachita, more than 9,000 miles of streams and rivers provide incomparable canoeing and fishing opportunities, and over 16,000 publicly and privately- owned campsites allow access to the outdoor world in every corner of the state. The only diamond mine in the nation is in Murfreesboro, Arkansas, at the Crater of Diamonds State Park. Arkansas offers choice retirement communities like Hot Springs Village or Bella Vista, major tourist attractions like Oaklawn Park in historic Hot Springs, picturesque vistas like Eureka Springs and Petit Jean Mountain, and the caverns in Blanchard Springs. For more information on Arkansas state parks, please go to the following website: Arkansas State Parks. Department of Finance and Administration P. O. Box 1272 Little Rock, Arkansas 72203 Moving To Arkansas TABLE OF CONTENTS Page Arkansas Facts and Folklore ............................................................................................. 1 Seventy-five Counties in Arkansas and State Symbols .................................................. 2 Individual Income Tax ........................................................................................................ -

An Overview of Capital Gains Taxes FISCAL Erica York FACT Economist No

An Overview of Capital Gains Taxes FISCAL Erica York FACT Economist No. 649 Apr. 2019 Key Findings • Comparisons of capital gains tax rates and tax rates on labor income should factor in all the layers of taxes that apply to capital gains. • The tax treatment of capital income, such as capital gains, is often viewed as tax-advantaged. However, capital gains taxes place a double-tax on corporate income, and taxpayers have often paid income taxes on the money that they invest. • Capital gains taxes create a bias against saving, which encourages present consumption over saving and leads to a lower level of national income. • The tax code is currently biased against saving and investment; increasing the capital gains tax rate would add to the bias against saving and reduce national income. The Tax Foundation is the nation’s leading independent tax policy research organization. Since 1937, our research, analysis, and experts have informed smarter tax policy at the federal, state, local, and global levels. We are a 501(c)(3) nonprofit organization. ©2019 Tax Foundation Distributed under Creative Commons CC-BY-NC 4.0 Editor, Rachel Shuster Designer, Dan Carvajal Tax Foundation 1325 G Street, NW, Suite 950 Washington, DC 20005 202.464.6200 taxfoundation.org TAX FOUNDATION | 2 Introduction The tax treatment of capital income, such as from capital gains, is often viewed as tax-advantaged. However, viewed in the context of the entire tax system, there is a tax bias against income like capital gains. This is because taxes on saving and investment, like the capital gains tax, represent an additional layer of tax on capital income after the corporate income tax and the individual income tax. -

The Dual-System of Water Rights in Nebraska George Rozmarin University of Nebraska College of Law

Nebraska Law Review Volume 48 | Issue 2 Article 6 1968 The Dual-System of Water Rights in Nebraska George Rozmarin University of Nebraska College of Law Follow this and additional works at: https://digitalcommons.unl.edu/nlr Recommended Citation George Rozmarin, The Dual-System of Water Rights in Nebraska, 48 Neb. L. Rev. 488 (1969) Available at: https://digitalcommons.unl.edu/nlr/vol48/iss2/6 This Article is brought to you for free and open access by the Law, College of at DigitalCommons@University of Nebraska - Lincoln. It has been accepted for inclusion in Nebraska Law Review by an authorized administrator of DigitalCommons@University of Nebraska - Lincoln. 488 NEBRASKA LAW REVIEW-VOL. 48, NO. 2 (1969) Co'mment THE DUAL-SYSTEM OF WATER RIGHTS IN NEBRASKA I. INTRODUCTION In Nebraska, rights to waters in streams and lakes have been regulated through a dual-system which utilizes both the riparian doctrine of the common law and the statutory scheme of appropri- ative rights. Although the two doctrines are divergent in many instances, the judiciary has recognized this and attempted to main- tain a balance between them. Despite these efforts, however, inconsistent principles of law developed over the years until finally in Wasserburgerv. Coffee1 the Nebraska Supreme Court attempted to reconcile the relative status of riparians and appropriators. In doing so the court prescribed a flexible method of equitable balance rather than a static formula of distribution. This article will give a brief introduction to some of the problems faced in distributing water rights under this dual-system, and will attempt to determine what effect Wasserburger may have on these rights that are so intimately linked with the prosperity of the state and Eill of its citizens. -

A Local Excise Tax on Sugary Drinks

DENVER: Sugary Drink Excise Tax Executive Summary Continually rising rates of obesity represent one of the greatest public health threats facing the United States. Obesity has been linked to excess consumption of sugary drinks. Federal, state, and local governments have considered implementing excise taxes on sugary drinks to reduce consumption, reduce obesity and provide a new source of government revenue.1-4 We modeled implementation of a city excise tax, a tax on sugary drinks only, at a tax rate of $0.02/ ounce. The tax model was projected to be cost-saving and resulted in lower levels of sugary drink consumption, thousands of cases of obesity prevented, and hundreds of millions of dollars in health care cost savings. Health care cost savings per dollar invested was $11 in the model. Results prepared by Denver Public Health and the CHOICES Project team at the Harvard T.H. Chan School of Public Health: Moreland J, Kraus (McCormick) E, Long MW, Ward ZJ, Giles CM, Barrett JL, Cradock AL, Resch SC, Greatsinger A, Tao H, Flax CN, and Gortmaker SL. Funded by The JPB Foundation. Results are those of the authors and not the funders. For further information, contact cgiles@ hsph.harvard.edu and visit www.choicesproject.org The information in this report is intended to provide educational information on the cost-effectiveness of Sugary Drink Taxes. 1 DENVER: Sugary Drink Excise Tax Background Although sugary drink consumption has declined in recent years, adolescents and young adults in the United States consume more sugar than the Dietary Guidelines -

The Law of Prior Appropriation: Possible Lessons for Hawaii

Volume 25 Issue 4 Symposium on International Resources Law Fall 1985 The Law of Prior Appropriation: Possible Lessons for Hawaii Stephen F. Williams Recommended Citation Stephen F. Williams, The Law of Prior Appropriation: Possible Lessons for Hawaii, 25 Nat. Resources J. 911 (1985). Available at: https://digitalrepository.unm.edu/nrj/vol25/iss4/5 This Article is brought to you for free and open access by the Law Journals at UNM Digital Repository. It has been accepted for inclusion in Natural Resources Journal by an authorized editor of UNM Digital Repository. For more information, please contact [email protected], [email protected], [email protected]. STEPHEN F. WILLIAMS* The Law of Prior Appropriation: Possible Lessons for Hawaii- INTRODUCTION Hawaiian water law has been in turmoil for nearly thirteen years. On January 10, 1973, in McBryde Sugar Co. v. Robinson,' the Supreme Court of Hawaii overturned a long-established system of rights.2 Liti- gation testing the validity of McBryde has since wended its way through the federal and state courts. On February 20, 1985, the United States Court of Appeals for the Ninth Circuit effectively overturned McBryde.3 In the meantime, the Hawaiian legislature established an Advisory Study Commission on Water Resources ("Advisory Commission"). The Com- mission issued its report ("Commission Report") on January 14, 1985.' The stage is thus set for Hawaii now to resolve its water conflicts. Hawaii's key choice relates to transferability. Pre-McBryde law, like that of most prior appropriation states, permitted transfer of water rights as long as the transfer inflicted no injury on other water users.5 This *Professor of Law, University of Colorado.