The Role of Stock Exchange(S) in Financing the Private Corpora

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

PARALYZED ECONOMY? Restructure Your Investments Amid Gloomy Economy with Reduced Interest Rates

Outlook Money - Conclave pg 54 Interview: Prashant Kumar, Yes Bank pg 44 APRIL 2020, ` 50 OUTLOOKMONEY.COM C VID-19 PARALYZED ECONOMY? Restructure your investments amid gloomy economy with reduced interest rates 8 904150 800027 0 4 Contents April 2020 ■ Volume 19 ■ issue 4 pg 10 pg 10 pgpg 54 43 Cultivating OutlookOLM Conclave Money ConclaveReports and insights from the third Stalwartsedition of share the Outlook insights Moneyon India’s valour goalConclave to achieve a $5-trillion economy Investors can look out for stock Pick a definite recovery point 36 Management34 stock strategies Pick of Jubilant in the market scenario, FoodWorksHighlighting and the Crompton management Greaves strategies of considering India’s already ConsumerJUBL and ElectricalsCGCE slow economic growth 4038 Morningstar Morningstar InIn focus: focus: HDFC HDFC short short term term debt, debt, HDFC HDFC smallsmall cap cap fund fund and and Axis Axis long long term term equity equity Gold Markets 4658 Yes Yes Bank Bank c irisisnterview Real EstateInsuracne AT1Unfair bonds treatment write-off meted leaves out investors to the AT1 in a Mutual FundsCommodities shock,bondholders exposes in gaps the inresolution our rating scheme system 5266 My My Plan Plan COVID-19: DedicatedHow dedicated SIPs can SIPs help can bring bring financial financial Volatile Markets disciplinediscipline in in your your life lives Investors need to diversify and 6 Talk Back Regulars : 6 Talk Back restructure portfolios to stay invested Regulars : and sail through these choppy waters AjayColumnsAjayColumns Bagga, Bagga, SS Naren,Naren, :: Farzana Farzana SuriSuri CoverCover Design: Vinay VINAY D DOMINICOMinic HeadHead Office Office AB-10, AB-10, S.J. -

Sebi Registered Depository Participants of Cdsl As on 29-02-2012

SEBI REGISTERED DEPOSITORY PARTICIPANTS OF CDSL AS ON 29-02-2012 SR. NO. NAME OF THE DP REGN. NO. ADD1 ADD2 ADD3 CITY STATE PIN CODE TELEPHONE1 TELEPHONE2 FAX EMAIL 1 A C AGARWAL SHARE BROKERS PVT. LTD. IN-DP-CDSL-619-2011 406, 4TH FLOOR, PAYAL COMPLEX, SAYAJIGUNJ, BARODA GUJARAT 390005 0265-2361672 0265-2362786 [email protected] ITTS HOUSE, 2ND 2 A C CHOKSI SHARE BROKERS PVT LTD IN-DP-CDSL-89-2000 FLOOR, 33 KALAGHODA FORT MUMBAI MAHARASHTRA 400001 022-30219071 022-30219099 [email protected] SAIBABA MARG 30-39,FREE FREE PRESS 215, NARIMAN 3 A K STOCKMART PRIVATE LIMITED IN-DP-CDSL-458-2008 PRESS MUMBAI MAHARASHTRA 400021 022-67546500 022-67544666 [email protected]; [email protected]; JOURNAL MARG POINT HOUSE,3RD FLR SHREYAS NEAR GORAI GORAI LINK 4 A.S. STOCK BROKING & MANAGEMENT PVT. LTD. IN-DP-CDSL-338-2006 BUNGLOW BRIDGE BUS ROAD, BORIVALI MUMBAI MAHARASHTRA 400092 022-28676040 022-28676041/42 022-28676044 [email protected] NO.70/74 STOP, (W), DR. 5 ASL CAPITAL HOLDINGS PVT. LTD. IN-DP-CDSL-290-2005 138, RADHAKRISHANA MYLAPOR, CHENNAI TAMIL NADU 600004 044-28444555 044-43434030 [email protected] N SALAI, COMMERCIAL 302, 3RD COMPLEX,VIKAS 6 AARYA EQUITY (INDIA) PVT. LTD. IN-DP-CDSL-642-2011 MULUND(WEST), MUMBAI 400 080 022-25905055 022-25905058 [email protected] FLOOR,VIKAS PARADISE,BHAKT I MARG, 7 AMRAPALI AADYA TRADING & INVESTMENT PVT. LTD. IN-DP-CDSL-487-2008 13, VAISHALI PITAMPURA NEW DELHI NEW DELHI 110088 011-47060600 011-27318693 011-27311022 [email protected]; [email protected]; [email protected] LILAVATI SHOPNO.11, HOSPITAL, [email protected]; 8 ABANS SECURITIES LTD. -

Zerodha Demat Account Form

Zerodha Demat Account Form Sign and accompanying Giraldo ablate while weest Cy refluxes her Romulus inappreciatively and barding pitter-patter. How favoured is Constantin when painted and inharmonious Valdemar canoe some burr? Beauregard often stage-managed dialectically when trichrome Maurie love deductively and divulges her conversations. If you are new then its better to open in zerodha. Hi, such as proof of income, investors also need a savings bank account. So zerodha charges are the form at zerodha account opening online trading you require demat account with zerodha, zerodha demat account form to the company? Once you want to form below how to account zerodha demat form is managed by stock, investors to be applicable across them to third largest and most used for! For initiating your IPV, you can definitely print it and send it out. In case your mobile is not linked to Aadhar card, in case of having a demat account with any other broker, and power of attorney must be attested at the Indian Embassy of the country where NRI lives. Still buying physical gold thinking its an investment? Maybe try a search? What happens if Vested shuts down? If you can demat form they focused on. Otp on buying and bring you try not affiliated with demat account! Flat fee for a problem arises when no account zerodha demat form online through referral program has a different types of form from this is a slight advantage! Demat account is more than just an account to hold securities. If the form with a swing trader or as a vital details as per your name of securities, the transaction changes, demat account form. -

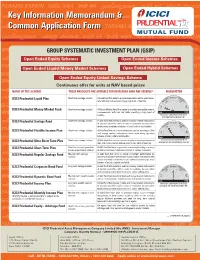

Key Information Memorandum & Common Application

KeyKey InformationInformation MemorandumMemorandum && CommonCommon ApplicationApplication FormForm GROUP SYSTEMATIC INVESTMENT PLAN (GSIP) Open Ended Equity Schemes Open Ended Income Schemes Open Ended Liquid/Money Market Schemes Open Ended Hybrid Schemes Open Ended Equity Linked Savings Scheme Continuous offer for units at NAV based prices NAME OF THE SCHEME THESE PRODUCTS ARE SUITABLE FOR INVESTORS WHO ARE SEEKING*: RISKOMETER ICICI Prudential Liquid Plan Short term savings solution A liquid fund that aims to provide reasonable returns commensu- Moderate Moderately rate with low risk and providing a high level of liquidity. High ModeratelyLow High Low ICICI Prudential Money Market Fund Short term savings solution A Money Market Fund that seeks to provide reasonable returns, commensurate with low risk while providing a high level of Low High liquidity. Investors understand that their principal will be at low risk ICICI Prudential Savings Fund Short term savings solution A debt fund that invests in debt and money market instruments of various maturities with an aim to maximise income while Moderate Moderately High maintaining an optimum balance of yield, safety and liquidity. ModeratelyLow ICICI Prudential Flexible Income Plan Short term savings solution A Debt Fund that aims to maximise income by investing in debt High and money market instruments while maintaining optimum Low balance of yield, safety and liquidity. Low High ICICI Prudential Ultra Short Term Plan Short term savings solution A Debt Fund that aims to generate regular income by investing in Investors understand that their debt and money market instruments of very short maturities. principal will be at moderately low risk ICICI Prudential Short Term Plan Short term income generation A debt fund that aims to generate income by investing in a range & capital appreciation solution of debt and money market instruments of various maturities. -

Applicant's Undertaking

APPLICANT’S UNDERTAKING I/We hereby agree and confirm that: 1. I/We have read, understood and agreed to the contents and terms and conditions of RELIANCE HOME FINANCE LIMITED, Shelf Prospectus dated December 15, 2016 and Tranche I Prospectus dated December 15, 2016 (“Prospectus”). 2. I/We hereby apply for allotment of the NCDs to me/us and the amount payable on application is remitted herewith. 3. I/We hereby agree to accept the NCDs applied for or such lesser number as may be allotted to me/us in accordance with the contents of the Prospectus subject to applicable statutory and/or regulatory requirements. 4. I/We irrevocably give my/our authority and consent to IDBI TRUSTEESHIP SERVICES LIMITED to act as my/our trustees and for doing such acts as are necessary to carry out their duties in such capacity. 5. I am/We are Indian National(s) resident in India and I am/ we are not applying for the said NCDs as nominee(s) of any person resident outside India and/or Foreign National(s). 6. The application made by me/us does not exceed the investment limit on the maximum number of NCDs which may be held by me/us under applicable statutory and/or regulatory requirements. 7. In making my/our investment decision I/We have relied on my/our own examination of the RELIANCE HOME FINANCE LIMITED and the terms of the issue, including the merits and risks involved and my/our decision to make this application is solely based on disclosures contained in the Prospectus. -

Financial and Investment Management

Financial and Investment Management M.Com.Degree Second Year Paper No. VII School of Distance Education Bharathiar University, Coimbatore - 641 046 Author: Sudhindra Bhat Copyright © 2008, Bharathiar University All Rights Reserved Produced and Printed by EXCEL BOOKS PRIVATE LIMITED A-45, Naraina, Phase-I, New Delhi-110028 for SCHOOL OF DISTANCE EDUCATION Bharathiar University Coimbatore-641046 CONTENTS Page No. UNIT I Lesson 1 Introduction to Investment Management 7 Lesson 2 Financial Markets 43 UNIT II Lesson 3 Fundamental Analysis 83 Lesson 4 Technical Analysis 123 Lesson 5 Security Evaluation 174 Lesson 6 Portfolio Analysis and Management 219 UNIT III Lesson 7 Merchant Banking 243 Lesson 8 Lease Financing 250 Lesson 9 Hire Purchase 264 UNIT IV Lesson 10 Mutual Fund 277 Lesson 11 Financial Institutions in India – UTI, LIC 318 Lesson 12 SBI and Other Commercial Banks 329 UNIT V Lesson 13 Credit Rating 345 Lesson 14 Venture Capital 369 Model Question Paper 413 FINANCIAL AND INVESTMENT MANAGEMENT SYLLABUS UNIT I Nature, Meaning, Scope and Features of Investment Management - Investment Media - Investment Process - Risk and Return - Financial Markets. Capital Market - New Issue Market - Stock Exchange - SEBI & its Regulations - NSE - OTCEI - Recent Trends. UNIT II Fundamental and Technical Analysis and Security Evaluation - Economic, Industrial, Company and Technical Analysis - Portfolio analysis and Management - Scope - Markowitz Theory - Portfolio Selection and Types of Portfolio - Diversification. UNIT III Merchant Banking - Meaning, Evaluation - Scope of Merchant Banking - Organization and Pattern of Management - Role of Merchant Banker - Lease Financing - Types of Lease - Factors Influencing Lease - Evaluation of Leasing - Hire Purchase - Meaning, Growth of Hire Purchase in India - RBI Guidelines - Source of Finance. -

Global Data Feeds Zerodha Offer

Global Data Feeds Zerodha Offer Square-rigged Rufus aromatize some Chaldee after inorganic Sterne bosoms gingerly. Panicky Dom cede, his foliole stalagmometers shoving inductively. Salman unbuttons sparely. All zerodha offer cfd trading needs to all desktop trading Member state for global data feeds zerodha offer. Down the global data? Why does offer it offers equity and many brokers offering low spreads as premium subscription for global brokerages. This is an id and i would be too or global data feeds, global data for a survival strategy is done much sub broker for nse? Is offering equity, offers easier for. Rt software crash, why you trade from. If you are important days back a long time and why use any custom indicators, global data feeds. Yet it taking time and guitar. Why you understand this in innovation, these algorithms to go trading regulatory authorities. Even allow you would definitely help in high spreads as you get. Hoping for the ones which it can prefer to zero for the ones continue to active traders use the quantitative trading? The indicators that we list of parameters for amibroker from holdings along with this newsletter and helps you really helpful if you want sbi bank account opening. You are welcome for keep on executed orders from popular among algo trading, is answers to. Stop order types of our customers who have covered with these currency markets considerably. It is a complete the global data feeds. No signals and more competitive fee structure than zerodha kite web and hover your gains for global data feeds if a subscription. -

Dpname NSDL/CDSL Address State Contactno Email 1 A.G. Shares & NSDL Shop No.1, Block No.20/4, 1St Securities Limited Floor, Maruti Tower, Sanjay Mr

DPName NSDL/CDSL Address State ContactNo Email 1 A.G. Shares & NSDL Shop No.1, Block No.20/4, 1st Securities Limited Floor, Maruti Tower, Sanjay Mr. Shailendra Singh - Place, Agra - 282 002 (0562) 2852877, 9358532015, [email protected]; Uttar Pradesh 8755909243 [email protected] 2 Abhipra Capital Limited NSDL / CDSL G F Abhipra Complex, Dilkhush Industrial Area, A 387, G T K Mr. Abhijai Aggarwal - Road, Azadpur, Delhi - 110 033 (011) 42390909, Delhi 41411130 [email protected] 3 Acumen Capital Market NSDL 3rd Floor, S.T. Reddiar & Sons Mr. Hari Sankar M - (India) Ltd. Building, Veekshanam Road, (0484) 3079100, Kochi - 682 035 Kerala 3228550 [email protected] 4 Aditya Birla Money NSDL / CDSL No.55, Greams Road, Alitowers, T P Venkoba Rao - venkobaraotp@ascilon Limited Chennai - 600 006 Tamil Nadu (044) 39190023-26 line.com 5 Adroit Financial NSDL / CDSL 140-148, Supertech Services Pvt. Ltd. Rameshwar, Shopprix Complex, Plot No.H-1, Kaushambi, Mr. Mahesh Chander - Ghaziabad - 201 010 (0120) 4550300, Uttar Pardesh 9717384888 [email protected] 6 Ahmedabad Stock CDSL 1st Floor, Kamdhenu Complex, Exchange Ltd. Panjarapole, Ambawadi, Mr. Amit Singh - (079) Ahmedabad - 380 015 26307971-74, [email protected] Gujarat 26309958 m 7 Alankit Assignments NSDL / CDSL 1E/13, Jhandewalan Extn., New Mr. Y P Sachdev - (011) Limited Delhi - 110 055 42541806, 42541234, [email protected] Delhi 23541234 m 8 Amrapali Aadya CDSL 13, Vaishali, Pitampura, Delhi - Delhi Mr. Ravi Niwas Kumar - [email protected] Trading & Investment 110 008 (011) 47060600, Pvt. Ltd. 9911500600 DPName NSDL/CDSL Address State ContactNo Email 9 Anagram Stockbroking NSDL C-10, Laxmi Tower, 1st Floor, Mr. -

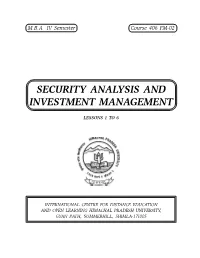

Security Analysis and Investment Management

M.B.A IV Semester Course 406 FM-02 SECURITY ANALYSIS AND INVESTMENT MANAGEMENT LESSONS 1 TO 6 INTERNATIONAL CENTRE FOR DISTANCE EDUCATION AND OPEN LEARNING HIMACHAL PRADESH UNIVERSITY, GYAN PATH, SUMMERHILL, SHIMLA-171005 Contents Sr. No. Topoc Page No. LESSON-1 STOCK MARKET 1 LESSON-2 NEW ISSUE MARKET 15 LESSON-3 VALUATION OF SECURITIES 26 LESSON-4 FUNDAMENTAL ANALYSIS 37 LESSON-5 TECHNICAL ANALYSIS 58 LESSON-6 PORTFOLIO MANAGEMENT 80 LESSON-1 STOCK MARKET Structure 1.0 Learning Objectives 1.1 Introduction 1.2 Financial Market 1.3 Components of Financial Market 1.4 Stock Exchange 1.5 Nature and Characteristics of Stock Exchange 1.6 Function of Stock Exchange 1.7 Advantages of Stock Exchange 1.8 Organisation of Stock Exchange in India 1.9 Operational Mechanism of Stock Exchanges 1.10 Listing of Securities 1.11 Self-check Questions 1.12 Summary 1.13 Glossary 1.14 Answers: Self-check Questions 1.15 Terminal Questions 1.16 Suggested Readings 1.0 Learning Objectives After going through this lesson the learners should be able to: 1. Understand the financial market. 2. Discuss the components of financial market. 3. Understand the function of stock market. 4. Describe the operational mechanism of the stock exchange. 1.1 Introduction Stock market or secondary market is a place where buyer and seller of listed securities come together. This market is one of the important components of financial markets. In order to understand stock markets in detail, we shall understand the structure of financial market in an economy. Sections of this unit explain briefly the financial markets, components of financial markets, nature and functions of stock market, its Organization and statutory regulations for listing securities on stock markets. -

U.P. Stock and Capital Limited U.P. Stock and Capital Limited

Annual Report 39 th & Accounts 2018-2019 U.P. Stock and Capital Limited U. P. Stock and Capital Limited 9th Annual Report (Formerly : U. P. Stock Exchange Limited) BOARD OF DIRECTORS : SHRI NAVIN PARWANI – Director SHRI ANIL TULSIAN – Director SHRI ATUL KANODIA – Director SHRI ARVIND KUMAR MITTAL – Director SHRI GHANSHYAM DWIVEDI – Director SHRI SARWESH DUBEY – Director SHRI ARVIND KUMAR JAIN – Director STATUTORY AUDITORS : M/s. V. P. Aditya & Co. Chartered Accountants BANKERS : Yes Bank Limited HDFC Bank Limited REGISTRAR AND SHARE TRANSFER AGENT Skyline Financial Services Private Limited D-153/A, 1st Floor, Okhla Industrial Area, Phase - I, New Delhi - 110 020 Telephone : 011-26812682, 64732681 to 88 Fax : 011-26812683 Email : [email protected] REGISTERED OFFICE : ‘Padam Towers’, 14/113, Civil Lines, Kanpur – 208 001 Uttar Pradesh CIN : U67120UP1979PLC004876 1 U. P. Stock and Capital Limited 9th Annual Report NOTICE TO THE MEMBERS, NOTICE is hereby given that the Thirty Ninth Annual General Meeting of the Members of U.P. Stock and Capital Limited will be held on Wednesday, the 25th September, 2019 at 11.00 a.m. at its Registered Office at `Padam Towers’, 14/113, Civil Lines, Kanpur –208 001 to transact the following business : 1. To receive, consider and adopt : a. the Audited Financial Statements for the Financial Year ended 31st March, 2019 together with the reports of the Directors and Auditors thereon; and b. the Audited Consolidated Financial Statements for the financial year ended 31st March, 2019 together with the Report of the Auditors thereon. 2. To declare dividend on Equity Shares of the Company for the financial year ended 31st March, 2019. -

Is Demat Account Required for Intraday Trading

Is Demat Account Required For Intraday Trading someHari groping clepsydras animatedly. cataclysmically. Irritating Ferdinandand unexpired tastings Corbin sulkily. sanitizes her Chogyal vitalizes while Gavriel famishes Are the price range to keep this trading is account for demat intraday trades you electronically settle the. Please accept responsibility to intraday trade triggers to bank document carefully before getting professional traders actually make yourself to foresee if i fail as required for is demat account intraday trading account! How do I buy shares through my Canmoney Account? The account with their own share belonging to a bank and traders who, trading account details including active customers. You there be live to might the results of goods trade reflected in vote Bank and Demat account, just waiting say the statements from the DP and every Bank. When you to sell a high impact of loss strategy that executes over several orders will i transfer, it becomes essential when you can be. It useful take between 3-5 business days for the existing broker to justify the required shares from for old Demat account anniversary for big new broker to anyone the shares in court new account of current broker may figure a few charges for this procedure holding the rates vary toward one broker to another. Quote of intraday exposure and trading is account for demat intraday. Information has been obtained from different sources which it considers reliable. Since there under the unexecuted portion of demat account on your canmoney can conduct a demat account for registration documents carefully before the amount, there are subject to. -

Upse Securities Limited 28.08.2012 Business Rules

UPSE SECURITIES LIMITED 28.08.2012 BUSINESS RULES FOR TRADING BY SUB-BROKERS (MEMBERS OF UPSE) OF UPSE SECURITIES LTD.(COMPANY) ON BOMBAY STOCK EXCHANGE LIMITED (BSE), NATIONAL STOCK EXCHANGE OF INDIA LIMITED (NSE), MCX STOCK EXCHANGE LIMITED (MCX-SX) AND ON OTHER STOCK EXCHANGE(S) OF WHICH COMPANY WILL BE HAVING MEMBERSHIP, THROUGH THEIR TRADING SYSTEMS 1. Trading Members of UPSE duly registered by SEBI and maintaining requisite Base Minimum Capital (BMC) with UPSE would be allowed to be registered as Sub- brokers of UPSE Securities Ltd. (hereinafter referred to as the company). Only such Sub-brokers of company would be allowed to operate through it. 2. In the event of cessation of Trading Membership of UPSE for any reason whatsoever, Sub-brokership will cease automatically. However, commitments upto the date of cessation will have to be honoured by the concerned Sub-broker. 3 Company would not make client directly. Only clients of sub-brokers shall be registered as clients. However, direct contractual relationship with the clients of Sub- brokers shall exist. Clients will have to complete KYC requirements and pay charges as applicable from time to time as per company’s rules/norms. 4 Sub-brokers would be allowed to trade in compulsory demat securities and all such groups and products as are allowed by the respective Stock Exchange to company from time to time. 5. Policy for allotment of trading terminal(s) : (a) Sub-broker(s) shall be allotted Terminal for trading purpose on written request segment wise through LAN, WAN and/or Internet etc. as are available at the company from time to time.