Kiama Local Government Area Final Report 2015 09 November 2015

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Great Walks Love’S Bay, Kiama Heights to Werri Lagoon, • Drink, and Take, Lots of Water, Especially in Werri Beach

12 LOVE’S BAY TO WERRI BEACH TIPS FOR SAFE WALKING COASTAL WALKING TRACK WALK IT KIAMA • Wear 30+ SPF sunscreen, a hat and This is a spectacular walking trail sunglasses. hugging the coastline, which was • Always make sure to wear comfortable previously inaccessible, stretching from and supportive shoes. Great Walks Love’s Bay, Kiama Heights to Werri Lagoon, • Drink, and take, lots of water, especially in Werri Beach. There are route markers warm weather. 1 MINNAMURRA TO BONEYARD 6 BLOWHOLE TO KENDALLS BEACH located approximately every 1km along • Cross at traffic lights or pedestrian crossings (southern side of river) eg cnr of The Things To See: Kiama Blowhole and the track. There are no drinking water where available. Village and Riverside Drive. Lighthouse, Surf Beach,Kendalls Beach. supplies (bubblers etc) and no toilets • Always warm up, stretch and cool down. • If you have chest discomfort, pain or Things To See: Minnamurra Headland, Distance: 2.1km Grade: Medium located along the track – make sure you palpitations while exercising, STOP Rangoon Island, Jones Beach, Cathedral Average walking time: 23 minutes are prepared for this. immediately and seek medical advice. Rocks. Werri Lagoon is open to the sea, so at • A Good Rule Of Thumb: Set a pace where Distance: 4.6km Grade: Medium 7 SADDLEBACK MOUNTAIN times, it is inaccessible to traverse and you Look out for the you are able to walk and talk at the same Average walking time: 51 minutes Things To See: Spectacular views of rural may need to return to Love’s Bay. “Walk It Kiama” symbol on time. -

Illawarra Business Chamber CONNECTING SUPPORTING AND

CONNECTING SUPPORTING AND GROWING ILLAWARRA BUSINESS ILLAWARRA BUSINESS CHAMBER ANNUAL REPORT 2011 SEE HOW WE CONNECT, SUPPORT & GROW ILLAWARRA BUSINESS CONTENTS BOARD OF DIRECTORS 02 PRESIdent’s MESSAGE 03 CEO’s MESSAGE 04 IBC CONNECTIONS 05 LEADERSHIP IN INDUSTRY & COMMUNITY 09 IBC MEMBERSHIP SUPPORT 10 BUSINESS LEADERSHIP 12 ILLAWARRA INDUSTRY APPRENTICESHIP PROJECT 14 EXPORT DOCUMENTATION 16 FINANCIAL REPORT 19 MEMBERSHIP LIST 40 PROMOTIONAL PARTNERS 58 BOARD OF DIRECTORS Les Dion Pat Nolan DION’S BUS SERVICES TELSTRA Sue Baker-Finch Stuart Barnes Michael Bassingthwaighte Noel Cornish ILLAWARRA HEALTH AND SPORTSGROUND TRUST, PEOPLECARE BLUESCOPE STEEL MEDICAL RESEARCH WIN SPORTS & 02 INSTITUTE ENTERTAINMENT CENTRES Janine Cullen Deborah De Santis Tony Emery Dom Figliomeni JC - THE PowER OF ONE DE SANTIS PUBLIC SOILCO PTY LTD - PORT KEMBLA PORT RELATIONS SHOALHAVEN REP. CORPORATION illawarrabusiness.com.au David Fuller Mark McDonald Dianne Murray Terry Oakes-Ash INNOVATION CAMPUS MAGUIRE TAFE NSW SOUTHERN HIGHLANDS & UNIVERSITY & MCINERNEY ILLAWARRA INSTITUTE BUSINESS CHAMBER - DEVELOPMENTS WINGECARRIBEE REP. P.4236 0513 - M. 0419 460 543 460 0419 M. - 0513 P.4236 Jessica Saad Terry Wetherall David Willcocks Mark Wilson JCI ILLAWARRA JBA URBAN PLANNING KPMG WOLLONGONG WISDOM ADVERTISING CONSULTANTS & DESIGN P.4236 0513 - M. 0419 460 543 460 0419 M. - 0513 P.4236 WWW.PROMOTEYOURSELFPRODUCT.COM EST 1999 promoteyourselfproducts MORE LOTS & PRINTING - PRODUCTS PROMOTIONAL Suppliers of Quality Promotional Merchandise and Printing P. 02 4236 -

Distribution and Transmission Annual Planning Report

Distribution and Transmission Annual Planning Report December 2019 Disclaimer Ausgrid is registered as both a Distribution Network Service Provider and a Transmission Network Service Provider. This Distribution and Transmission Annual Planning Report 2019 has been prepared and published by Ausgrid under clause 5.13.2 and 5.12.2 of the National Electricity Rules to notify Registered Participants and Interested Parties of the results of the distribution and transmission network annual planning review and should only be used for those purposes. This document does not purport to contain all of the information that a prospective investor or participant or potential participant in the National Electricity Market, or any other person or interested parties may require. In preparing this document it is not possible nor is it intended for Ausgrid to have regard to the investment objectives, financial situation and particular needs of each person who reads or uses this document. In all cases, anyone proposing to rely on or use the information in this document should independently verify and check the accuracy, completeness, reliability and suitability of that information for their own purposes. Accordingly, Ausgrid makes no representations or warranty as to the accuracy, reliability, completeness or suitability for particular purposes of the information in this document. Persons reading or utilising this document acknowledge that Ausgrid and their employees, agents and consultants shall have no liability (including liability to any person by reason of negligence or negligent misstatement) for any statements, opinions, information or matter (expressed or implied) arising out of, contained in or derived from, or for any omissions from, the information in this document, except insofar as liability under any New South Wales and Commonwealth statute cannot be excluded. -

Walks, Paddles and Bike Rides in the Illawarra and Environs

WALKS, PADDLES AND BIKE RIDES IN THE ILLAWARRA AND ENVIRONS Mt Carrialoo (Photo by P. Bique) December 2012 CONTENTS Activity Area Page Walks Wollongong and Illawarra Escarpment …………………………………… 5 Macquarie Pass National Park ……………………………………………. 9 Barren Grounds, Budderoo Plateau, Carrington Falls ………………….. 9 Shoalhaven Area…..……………………………………………………….. 9 Bungonia National Park …………………………………………………….. 10 Morton National Park ……………………………………………………….. 11 Budawang National Park …………………………………………………… 12 Royal National Park ………………………………………………………… 12 Heathcote National Park …………………………………………………… 15 Southern Highlands …………………………………………………………. 16 Blue Mountains ……………………………………………………………… 17 Sydney and Campbelltown ………………………………………………… 18 Paddles …………………………………………………………………………………. 22 Bike Rides …………………………………………………………………………………. 25 Note This booklet is a compilation of walks, paddles, bike rides and holidays organised by the WEA Illawarra Ramblers Club over the last several years. The activities are only briefly described. More detailed information can be sourced through the NSW National Parks & Wildlife Service, various Councils, books, pamphlets, maps and the Internet. WEA Illawarra Ramblers Club 2 October 2012 WEA ILLAWARRA RAMBLERS CLUB Summary of Information for Members (For a complete copy of the “Information for Members” booklet, please contact the Secretary ) Participation in Activities If you wish to participate in an activity indicated as “Registration Essential”, contact the leader at least two days prior. If you find that you are unable to attend please advise the leader immediately as another member may be able to take your place. Before inviting a friend to accompany you, you must obtain the leader’s permission. Arrive at the meeting place at least 10 minutes before the starting time so that you can sign the Activity Register and be advised of any special instructions, hazards or difficulties. Leaders will not delay the start for latecomers. -

First Choice Couriers

First Choice Couriers Make Your First Choice The Best Choice BLUE COUPON - SUBURB LISTING - WOLLONGONG Suburbs in BLUE are included in our LOCAL SAME DAY service - Pick-up cut-offs depend on location OVERNIGHT - Pick-up cut-off ex Wollongong is 3.00pm, unless stated otherwise in RED Albion Park (2:00) Dapto Kiama Heights (10:00) Shell Cove (2:00) Albion Park Rail Darkes Forest (10:00) Koonawarra Shellharbour (10:00) Austinmer (10:00) Dombarton (9:30) Lake Heights Shellharbour City Centre Avondale (10:00) Dunmore (9:30) Lake Illawarra Shellharbour Village (10) Balgownie East Corrimal Macquarie Pass Spring Hill Barrack Heights Fairy Meadow Mangerton Stanwell Park (10:00) Barrack Point Farmborough Heights Marshall Mount Stanwell Tops (10:00) Bellambi Fernhill Minnamurra (10:00) Tarrawanna Berkeley Figtree Mount Keira Thirroul (10:00) Blackbutt Flinders (2:00) Mount Kembla (9:30) Tongarra Bombo (10:00) Gwynneville Mount Ousley (10:00) Towradgi Brownsville Haywards Bay Mount Pleasant Tullimbar (9:30) Bulli Helensburgh (10:00) Mount Saint Thomas Unanderra Calderwood Horsley Mount Warrigal Warilla Cleveland (10:00) Huntley (9:30) North Wollongong Warrawong Clifton (10:00) Jamberoo (9:30) Oak Flats West Wollongong Coalcliff (10:00) Jerrara (9:30) Otford (10:00) Windang Coledale (10:00) Kanahooka Penrose Wollongong Coniston Keiraville Port Kembla Wombarra (10:00) Cordeaux Heights Kembla Grange Primbee Wongawilli (9:30) Corrimal Kembla Heights (9:30) Russell Vale Woonona Cringila Kiama (10:00) Saddleback Mountain Yallah Croom Kiama Downs (10:00) -

Invasive Plant Management in Complex Social Landscapes: a Case Study in Coastal New South Wales in Australia Mohammed Jahangir Alam University of Wollongong

University of Wollongong Research Online University of Wollongong Thesis Collection University of Wollongong Thesis Collections 2012 Invasive plant management in complex social landscapes: a case study in coastal New South Wales in Australia Mohammed Jahangir Alam University of Wollongong Recommended Citation Alam, Mohammed Jahangir, Invasive plant management in complex social landscapes: a case study in coastal New South Wales in Australia, Master of Science thesis, School of Earth and Environmental Sciences, University of Wollongong, 2012. http://ro.uow.edu.au/theses/3703 Research Online is the open access institutional repository for the University of Wollongong. For further information contact the UOW Library: [email protected] School of Earth and Environmental Sciences Faculty of Science, University of Wollongong Invasive plant management in complex social landscapes: a case study in coastal New South Wales in Australia Mohammed Jahangir Alam BSc. (H) in Forestry & Environmental Sciences University of Chittagong, Bangladesh Master of Professional Accounting University of Wollongong, Australia This thesis is submitted as part of the requirements for the award of the degree of Master of Science in the School of Earth and Environmental Sciences, University of Wollongong MARCH, 2012 Thesis certification I, Mohammed J. Alam, declare that this thesis, submitted as part of the requirements for the award of Master of Science, in the School of Earth and Environmental Sciences, University of Wollongong, is wholly my own work unless otherwise referenced or acknowledged. This document has not been submitted for any qualifications at any other academic institution. Mohammed Alam March, 2012 ii Abstract Climate change, landowner diversity, human socio-cultural and political attitudes, the biological and ecological characteristics of invasive plants and the nature of the communities they invade are the major drivers of plant invasion. -

Australian Bureau of Statistics

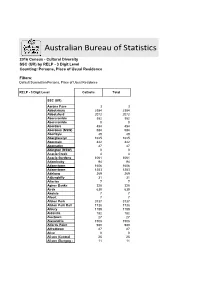

Australian Bureau of Statistics 2016 Census - Cultural Diversity SSC (UR) by RELP - 3 Digit Level Counting: Persons, Place of Usual Residence Filters: Default Summation Persons, Place of Usual Residence RELP - 3 Digit Level Catholic Total SSC (UR) Aarons Pass 3 3 Abbotsbury 2384 2384 Abbotsford 2072 2072 Abercrombie 382 382 Abercrombie 0 0 Aberdare 454 454 Aberdeen (NSW) 584 584 Aberfoyle 49 49 Aberglasslyn 1625 1625 Abermain 442 442 Abernethy 47 47 Abington (NSW) 0 0 Acacia Creek 4 4 Acacia Gardens 1061 1061 Adaminaby 94 94 Adamstown 1606 1606 Adamstown 1253 1253 Adelong 269 269 Adjungbilly 31 31 Afterlee 7 7 Agnes Banks 328 328 Airds 630 630 Akolele 7 7 Albert 7 7 Albion Park 3737 3737 Albion Park Rail 1738 1738 Albury 1189 1189 Aldavilla 182 182 Alectown 27 27 Alexandria 1508 1508 Alfords Point 990 990 Alfredtown 27 27 Alice 0 0 Alison (Central 25 25 Alison (Dungog - 11 11 Allambie Heights 1970 1970 Allandale (NSW) 20 20 Allawah 971 971 Alleena 3 3 Allgomera 20 20 Allworth 35 35 Allynbrook 5 5 Alma Park 5 5 Alpine 30 30 Alstonvale 116 116 Alstonville 1177 1177 Alumy Creek 24 24 Amaroo (NSW) 15 15 Ambarvale 2105 2105 Amosfield 7 7 Anabranch North 0 0 Anabranch South 7 7 Anambah 4 4 Ando 17 17 Anembo 18 18 Angledale 30 30 Angledool 20 20 Anglers Reach 17 17 Angourie 42 42 Anna Bay 789 789 Annandale (NSW) 1976 1976 Annangrove 541 541 Appin (NSW) 841 841 Apple Tree Flat 11 11 Appleby 16 16 Appletree Flat 0 0 Apsley (NSW) 14 14 Arable 0 0 Arakoon 87 87 Araluen (NSW) 38 38 Aratula (NSW) 0 0 Arcadia (NSW) 403 403 Arcadia Vale 271 271 Ardglen -

20/01/2021 Northern Beaches Local Government Areas Allambie

Northern Beaches Local Government Areas Allambie Heights Avalon Beach Balgowlah Balgowlah Heights Bayview Beacon Hill Belrose Bilgola Beach Bilgola Plateau Brookvale Church Point Clareville Clontarf Coasters Retreat Collaroy Collaroy Plateau Cottage Point Cromer Curl Curl Currawong Beach Davidson Dee Why Duffys Forest Elanora Heights Elvina Bay Fairlight Forestville Frenchs Forest Freshwater Great Mackerel Beach Ingleside Killarney Heights Lovett Bay Manly Manly Vale McCarrs Creek Mona Vale Morning Bay Narrabeen Narraweena Newport North Balgowlah North Curl Curl North Manly North Narrabeen Oxford Falls 20/01/2021 Palm Beach Queenscliff Salt Pan Cove Scotland Island Seaforth Terrey Hills Warriewood Whale Beach Wheeler Heights Wollongong Local Government Area Albion Park (Shell) Albion Park Rail (Shell) Austinmer (CoW) Avon (SCA, Wollondilly, CoW) Avondale (CoW) Balgownie (CoW) Barrack Heights (Shell) Barrack Point (Shell) Bellambi (CoW) Berkeley (CoW) Blackbutt (Shell) Bombo (Kiama) Broughton Village (Kiama) Brownsville (CoW) Bulli (CoW) Calderwood Carrington Falls (Kiama) Cataract (CoW) Cleveland (CoW) Clifton (CoW) Coalcliff (CoW) Coledale (CoW) Coniston (CoW) Cordeaux (SCA, CoW) Cordeaux Heights (CoW) Corrimal (CoW) Cringila (CoW) Croom Curramore (Kiama) Dapto (CoW) Darkes Forest (Wollondilly, CoW) Dombarton (CoW) Dunmore (Shell) East Corrimal (CoW) Fairy Meadow (CoW) Farmborough Heights (CoW) 20/01/2021 Fernhill (CoW) Figtree (CoW) Flinders (Shell) Foxground (Kiama) Gerringong (Kiama) Gerroa (Kiama) Gwynneville (CoW) Haywards Bay (CoW) -

Region Localities Inclusion Support Agency New South Wales

u Inclusion and Professional Support Program (IPSP) Grant Application Process 2013-2016 Region Localities Inclusion Support Agency New South Wales This document lists the localities which comprise each Statistical Area Level 2 within each ISA Region in New South Wales. Description This document provides greater detail on the Australian Bureau of Statistics, Statistical Areal Level 2 boundaries within each ISA Region. The localities listed in this document are the ‘gazetted locality boundaries’ supplied by the state or territory government and may differ from commonly used locality and/or suburb names. This document does not provide a definitive list of every suburb included within each ISA Region as this information is not available. Postcodes are provided for those localities which either: cross ISA boundaries or where the same locality name appears in more than one ISA region within the same state or territory. IPSP 2013-2016: ISA Region Localities – New South Wales ISA Region 1 – Sydney Inner – Localities Alexandria Eastlakes Point Piper Annandale Edgecliff Port Botany Balmain Elizabeth Bay Potts Point Balmain East Enmore Pyrmont Banksmeadow (Postcode: 2042) Queens Park Barangaroo Erskineville Randwick Beaconsfield Eveleigh Redfern Bellevue Hill Forest Lodge Rose Bay Birchgrove Glebe Rosebery Bondi Haymarket Rozelle Bondi Beach Hillsdale Rushcutters Bay Bondi Junction Kensington South Coogee Botany Kingsford St Peters Bronte La Perouse Stanmore Camperdown Leichhardt Surry Hills Centennial -

Million Dollar Markets

Million Dollar Markets Australia | Released June 2021 Data to May 2021 Contents Introduction 3 New South Wales 5 Victoria 7 Queensland 9 Western Australia 11 Adelaide 13 Australian Capital Territory 13 Hobart 15 Disclaimers 16 Lead Research Analyst: Jade Harling Introduction by: Eliza Owen 2 Introduction The current upswing in the Australian housing market has National Overview produced some extraordinary results. In the 12 months to May 2021, national dwelling market values increased 10.6%, In the year to March, CoreLogic collected 486,233 sales marking the highest growth rate since July 2010. The value of nationally, 16.6% of which were valued over $1 million. the national dwelling market hit a record high in January This marks a record high in the portion of sales over the $1 2021, and has continued to hit a fresh record high each million mark. month since. In the year to May, CoreLogic estimates there were 218 The wealth effect of house value increases has likely been a markets across Australia where either the house or unit key component of elevated consumer confidence, and median ticked over the $1 million. This includes 198 house Australia’s economic recovery from strict social distancing markets, and 20 unit markets. restrictions through 2020. The increased value of housing also cements the asset as a pillar of household wealth and The highest frequency of suburbs ticking over the million- security, making up 53.0% of household wealth through the dollar-median was in Sydney, with 54 markets seeing either fourth quarter of 2020. houses or units reach a median of $1 million or more. -

Kiama Local Strategic Planning Statement 2020

Kiama Local Strategic Planning Statement 2020 Acknowledgement of Country In preparation of this statement, Council acknowledges the traditional owners of the lands the Wadi Wadi people of the Dharawal nation, and pays respect to elders both past, present and emerging. Images © Peter Izzard Photography 2020 A message from the Mayor When I was first elected as Mayor, in 2016, I had a vision of consolidating a number of existing Council committees into a single, cohesive Planning Committee. It was my hope that the Planning Committee could determine what the expectations of the community are for the Kiama area in 20 years. This hope has become reality with the work done by the community, Planning Committee, elected Councillors and Council staff to prepare our LSPS. It has been encouraging to see the high level of community involvement in the preparation of our LSPS. It was particularly encouraging to see the positive and innovative ideas of our young people who attended the High School and Primary Schools workshop. been captured and the planning priorities and Our LSPS outlines what the community sees action contained within this document will help to as their vision for the Kiama in 20 years. As the achieve this vision. ‘highest’ planning document within Council, the planning priorities and associated actions will shape the comprehensive reviews of the Kiama Local Environmental Plan (LEP) 2011 and the Kiama Development Control Plan (DCP) 2012. Assessments for future developments are made against our LEP and DCP to achieve the Mayor, Cr Mark Honey community’s vision outlined in this document. Our LSPS will also provide a solid foundation for the review of Council’s Community Strategic Plan that is scheduled for 2020, with the election of the new Council. -

20/01/2021 (1) Albion Park (Shell)

Albion Park (Shell) Albion Park Rail (Shell) Allambie Heights Ashbury (with a minor portion within the Inner West Council) Auburn Austinmer (CoW) Avalon Beach Avon (SCA, Wollondilly, CoW) Avondale (CoW) Balgowlah Balgowlah Heights Balgownie (CoW) Bankstown Bankstown Aerodrome Barrack Heights (Shell) Barrack Point (Shell) Bass Hill Bayview Beacon Hill Belfield (with parts within the Municipality of Strathfield) Bellambi (CoW) Belmore Belrose Berala Berkeley (CoW) Beverly Hills (with parts within Georges River Council) Bidwell, Bilgola Beach Bilgola Plateau Birrong Blackbutt (Shell) Blackett, Bombo (Kiama) Brookvale Broughton Village (Kiama) Brownsville (CoW) Bulli (CoW) Calderwood Campsie Canterbury Carrington Falls (Kiama) Cataract (CoW) Chester Hill (shared with Canterbury-Bankstown) Chester Hill (with parts within Cumberland Council) Chullora Church Point Clareville Clemton Park 20/01/2021 (1) Cleveland (CoW) Clifton (CoW) Clontarf Coalcliff (CoW) Coasters Retreat Coledale (CoW) Collaroy Collaroy Plateau Condell Park Coniston (CoW) Cordeaux (SCA, CoW) Cordeaux Heights (CoW) Corrimal (CoW) Cottage Point Cringila (CoW) Cromer Croom Croydon Park (with parts within the Municipality of Burwood and the Inner West Council) Curl Curl Curramore (Kiama) Currawong Beach Dapto (CoW) Darkes Forest (Wollondilly, CoW) Davidson Dee Why Dharruk, Dombarton (CoW) Doonside, Duffys Forest Dunmore (Shell) Earlwood East Corrimal (CoW) East Hills Elanora Heights Elvina Bay Emerton, Fairfield (shared with Fairfield) Fairlight Fairy Meadow (CoW) Farmborough