Boyd Gaming Reports Third Quarter Results

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Lasvegasadvisor May 2021 • Vol

ANTHONY CURTIS’ LasVegasAdvisor May 2021 • Vol. 38 • Issue 5 $5 THE PASS OPENS Spruced up casino hits downtown Henderson … pgs. 1, 4, 5, 16 VIRGIN TERRITORY What’s the new joint all about? … pgs. 2, 8, 9, 12, 13, 14, 16 VAX PROMOS Take the shot, get a lot … pg. 3 BUFFETS Are they coming back? … pg. 7 POOL SEASON Cool pools open everywhere … pg. 14 CASINOS Local (702) Toll Free 2021 MEMBER Aliante Casino+Hotel+Spa ...................692-7777 ...... 877-477-7627 Aria .......................................................590-7111 ...... 866-359-7757 Arizona Charlie’s Boulder .....................951-5800 ...... 800-362-4040 REWARDS Arizona Charlie’s Decatur .....................258-5200 ...... 800-342-2695 Bally’s ...................................................739-4111 ...... 877-603-4390 Bellagio .................................................693-7111 ...... 888-987-7111 DINING, INCLUDING Binion’s .................................................382-1600 ...... 800-937-6537 “LOCAL CORNER”, DRINKS, Boulder Station .....................................432-7777 ...... 800-683-7777 Caesars Palace.....................................731-7110 ...... 866-227-5938 ATTRACTIONS, AND California ..............................................385-1222 ...... 800-634-6505 Cannery ................................................507-5700 ...... 866-999-4899 GAMBLING Casino Royale (Best Western Plus) ......737-3500 ...... 800-854-7666 Circa .....................................................247-2258 ...... 833-247-2258 Circus Circus ........................................734-0410 -

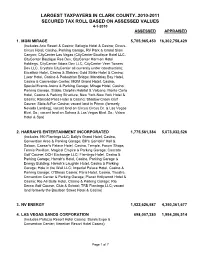

Largest Taxpayer Secured Values 2010-11

LARGEST TAXPAYERS IN CLARK COUNTY..2010-2011 SECURED TAX ROLL BASED ON ASSESSED VALUES 4-1-2010 ASSESSED APPRAISED 1. MGM MIRAGE 5,705,965,450 16,302,758,429 (Includes Aria Resort & Casino; Bellagio Hotel & Casino; Circus- Circus Hotel, Casino, Parking Garage, RV Park & Grand Slam Canyon; CityCenter Las Vegas (CityCenter Boutique Hotel LLC, CityCenter Boutique Res Dev, CityCenter Harmon Hotel Holdings, CityCenter Vdara Dev LLC, CityCenter Veer Towers Dev LLC, Crystals CityCenter all currently under construction); Excalibur Hotel, Casino & Stables; Gold Strike Hotel & Casino; Luxor Hotel, Casino & Pedestrian Bridge; Mandalay Bay Hotel, Casino & Convention Center; MGM Grand Hotel, Casino, Special Events Arena & Parking Garage; Mirage Hotel, Casino, Parking Garage, Stable, Dolphin Habitat & Volcano; Monte Carlo Hotel, Casino & Parking Structure; New York-New York Hotel & Casino; Railroad Pass Hotel & Casino; Shadow Creek Golf Course; Slots-A-Fun Casino; vacant land in Primm (formerly Nevada Landing); vacant land on Circus Circus Dr. & Las Vegas Blvd. So.; vacant land on Sahara & Las Vegas Blvd. So.; Vdara Hotel & Spa) 2. HARRAH'S ENTERTAINMENT INCORPORATED 1,775,561,384 5,073,032,526 (Includes 190 Flamingo LLC; Bally's Grand Hotel, Casino, Convention Area & Parking Garage; Bill's Gamblin' Hall & Saloon; Caesar's Palace Hotel, Casino, Temple, Forum Shops, Tennis Pavillion, Magical Empire & Parking Garage; Cascata Golf Course; DCH Exchange LLC; Flamingo Hotel, Casino & Parking Garage; Harrah's Hotel, Casino, Parking Garage & Energy Building; Harrah's Laughlin Hotel, Casino & Parking Garage; Hole in the Wall LLC; Imperial Palace Hotel, Casino & Parking Garage; O'Sheas Casino; Paris Hotel, Casino, Theatre, Convention Center & Parking Garage; Planet Hollywood Hotel & Casino; Rio All-Suite Hotel, Casino & Parking Garage; Rio Secco Golf Course, Club & School; TRB Flamingo LLC; vacant land formerly the Bourbon Street Hotel & Casino) 3. -

An Analysis of the Environmental Content of Las Vegas Strip Hotels

UNLV Theses, Dissertations, Professional Papers, and Capstones 12-2007 An Analysis of the environmental content of Las Vegas Strip hotels Andrew M. Levey Follow this and additional works at: https://digitalscholarship.unlv.edu/thesesdissertations Part of the Gaming and Casino Operations Management Commons, and the Sustainability Commons Repository Citation Levey, Andrew M., "An Analysis of the environmental content of Las Vegas Strip hotels" (2007). UNLV Theses, Dissertations, Professional Papers, and Capstones. 613. http://dx.doi.org/10.34917/1752239 This Professional Paper is protected by copyright and/or related rights. It has been brought to you by Digital Scholarship@UNLV with permission from the rights-holder(s). You are free to use this Professional Paper in any way that is permitted by the copyright and related rights legislation that applies to your use. For other uses you need to obtain permission from the rights-holder(s) directly, unless additional rights are indicated by a Creative Commons license in the record and/or on the work itself. This Professional Paper has been accepted for inclusion in UNLV Theses, Dissertations, Professional Papers, and Capstones by an authorized administrator of Digital Scholarship@UNLV. For more information, please contact [email protected]. AN ANALYSIS OF THE ENVIRONMENTAL CONTENT OF LAS VEGAS STRIP HOTELS Andrew M. Levey Bachelor of Science in Management Tulane University, New Orleans, Louisiana 2001 A professional paper submitted in partial fulfillment of the requirements for the Master Degree in Business Administration Department of College of Business College of Business Master of Science in Hotel Administration Department of William F. Harrah College of Hotel Administration William F. -

Las Vegas Casino & Hotel Market Outlook 2009

Las Vegas Casino & Hotel Market Outlook 2009 Shannon Okada, Associate Director, HVS Gaming Services HVS — Las Vegas HVS — LAS VEGAS 8170 W. Sahara Avenue, Suite 201 Las Vegas, NV 89117 United States of America +1 (702) 242-6723 OFFICE MAIN TELEPHONE HTTP://WWW.HVS.COM January 2009 New York San Francisco Boulder Denver Atlanta Miami Dallas Las Vegas Chicago Washington, D.C. Weston, CT Boston Mt. Lakes, NJ Mexico City Vancouver Toronto London Moscow Madrid Athens Dubai Mumbai New Delhi Singapore Hong Kong Beijing Shanghai São Paulo Buenos Aires Las Vegas Casino and Hotel Market Outlook 2009 Shannon S. Okada Associate Director Gaming Services Division, Vice President Consulting & Valuation HVS – Las Vegas Any previously held notion that the Las Vegas gaming-tourism industry is recession-proof was dispelled in 2008 as, to quote the Las Vegas Review Journal, “the imploding economy drove a stake though the heart of the Strip.” The downturn in the national and worldwide economies, and the resulting decrease in consumer consumption, has reduced visitation to the Las Vegas market in 2008 to levels not seen since 2004, which was prior to the opening of major properties including the Wynn Las Vegas, South Point, Red Rock Station, Palazzo, and Encore. As quality new supply is absorbed and operators have implemented strategies to compete for overnight guests to support gaming and other amenities, average daily room rate has dropped. The recession is prompting visitors and locals to gamble less. Challenging economic conditions, including the turmoil in the credit markets, have also resulted in a scaled-back development pipeline. -

18 Tommy Bridges, Industry Connector 22 the Theme Park Brains Behind Caesars’ High Roller 24 Las Vegas Reinvents Itself

New tech for museums, parks & rides #53 • volume 10, issue 3 • 2014 www.inparkmagazine.com 18 Tommy Bridges, industry connector 22 The theme park brains behind Caesars’ High Roller 24 Las Vegas reinvents itself www.inparkmagazine.com 1 © SHOW: ECA2 - PHOTOS: JULIEN PANIE THINK SPECTACULAR! SPECIAL EVENTS I THEME PARKS & PERMANENT SHOWS I EXPOS & PAVILIONS “WINGS OF TIME” I SENTOSA ISLAND, SINGAPORE. STARTED IN JUNE 2014. TEL: +33 1 49 46 30 40 I CONTACT: [email protected] I WWW.ECA2.COM I FACEBOOK.COM/ECA2PARIS www.inparkmagazine.com #53• volume 10, issue 3 Wings of Time 6 ECA2 creates new Sentosa spectacular• by Martin Palicki IAAPA Beijing 10 Asian Attractions Expo: Martin Palicki reports Civil war surround 13 BPI produces video diorama for Kenosha museum • by Martin Palicki Leave it to Holovis 16 Modern tools of simulation & visualization• by Stuart Hetherington Building Bridges 18 Tommy Bridges = technology + opportunity • by Judith Rubin Caesars’ High Roller 22 Theme park savvy reinvents the wheel Tomorrow’s Vegas 24 The new investments: Joe Kleiman reports RFID changes everything 29 Disney’s MyMagic+ gets off to a strong start • by Martin Palicki The museum network 31 Artifact Technologies introduces Mixby platform• by Joe Kleiman Immersion with dinosaurs 33 Movie Park Germany opens The Lost Temple • by Judith Rubin Gamification and dark rides 36 Innovations from Triotech, Sally & Alterface Projects • by Joe Kleiman staff & contributors advertisers EDITOR DESIGN Alcorn McBride 35 © SHOW: ECA2 - PHOTOS: JULIEN PANIE Martin Palicki mcp, llc Alterface Projects 29 Artifact Technologies 34 CO-EDITOR CONTRIBUTORS Judith Rubin Stuart Hetherington All Things Integrated 19 Super 78 Boston Productions Inc. -

Annual Report 2006

ANNUAL REPORT 2006 The Venetian Macao on the Cotai StripTM ~ Coming Summer 2007 The Venetain The Palazzo Sands Bethworks Sands Macao Marina Bay Sands Las Vegas ~ May 3, 1999 Las Vegas ~ 2007 Pennsylvania ~ 2008 Macao ~ May 18, 2004 Singapore ~ 2009 ellow Shareholders: I am pleased to present to you our third Annual Report. The Year 2006 was another record-setting year for our company as we executed on our operating and development plans around the globe. Our strong financial and operating performance, coupled with our victory in the global competition to build Singapore’s first Integrated Resort at Marina Bay, has clearly cemented our position as the preeminent worldwide developer and operator of premium convention-based destination hotel casino resorts. We again set occupancy and financial records at our flagship resort, The Venetian in Las Vegas. We also delivered record financial results at the Sands Macao, the first Las Vegas-style casino in The People’s Republic of China’s Special Administrative Region of Macao. In addition, we made substantial progress toward the completion of construction of two new mega-resorts, The Palazzo™, adjacent to The Venetian on the Las Vegas Strip, and The Venetian Macao, which will anchor our Cotai Strip™ development in Macao. Each of these resorts will open in 2007. In addition to our progress on The Venetian Macao, we continued to execute our master plan to develop the Cotai Strip into Asia’s premier leisure and convention destination. We began the development of six additional Cotai Strip properties, three of which will open in 2008, with the remainder to open in 2009. -

The Las Vegas Strip...The Early Years

The Las Vegas Strip the early years by Pam Goertler assisted by Brian Cashman El Rancho Vegas The first hotel on the Strip In the 1930’s there was no Las Vegas “Strip”. Las Vegas was a railroad town, built to house the railroad workers and their families. The clubs, casinos, stores, schools, hotels, professional offices, and railroad station were all downtown. Highway 91 (now the Strip) went from Los Angeles to Salt Lake City, passing through Las Vegas. Scattered along the highway, leading into Las Vegas, were some small clubs, but they were few and far between. his new hotel. Mrs. Jessie Hunt owned the proper- As the legend goes…in 1938 Tommy Hull and ty, and Tommy began negotiations with her. Mrs. a friend were driving along highway 91. They were Hunt felt that the property was worthless. She offered a few miles outside of Las Vegas when to give it to Tommy, just to get rid of it! She finally they got a flat tire. Tommy waited with accepted payment of $150 per acre, for about 33 acres. the car while his friend hitchhiked into Las Vegas to get help. While waiting, After months of planning and construction, El Rancho Tommy counted the cars that passed Vegas opened on April 3, 1941. Having seen the beautiful him on the highway, and began to get resort while it was being built, Las Vegans dressed in their an idea. Highway 91 was a long stretch of finest attire to attend the gala opening. Wanting a com- road through a hot, dusty desert. -

Largest Taxpayers in Clark County..2012-2013 Secured Tax Roll Based on Assessed Values 4-2-2012 Assessed Appraised

LARGEST TAXPAYERS IN CLARK COUNTY..2012-2013 SECURED TAX ROLL BASED ON ASSESSED VALUES 4-2-2012 ASSESSED APPRAISED 1. MGM RESORTS INTERNATIONAL 2,419,044,056 6,911,554,446 (Includes Aria Resort & Casino; Bellagio Hotel & Casino; Circus- Circus Hotel, Casino, Parking Garage, RV Park & Grand Slam Canyon; CityCenter Land LLC; Crystals Retail & Entertainment; Excalibur Hotel, Casino & Stables; Gold Strike Hotel & Casino; Harmon Hotel & Spa (construction halted); Jean Development Co. LLC; Jean Development North; Jean Development West; Luxor Hotel, Casino & Pedestrian Bridge; Mandalay Bay Hotel, Casino & Convention Center; Mandalay Resort Group; Mandarin Oriental Las Vegas; MGM Grand Hotel, Casino, Special Events Arena & Parking Garage; Mirage Hotel, Casino, Parking Garage, Stables, Dolphin Habitat & Volcano; Monte Carlo Hotel, Casino & Parking Structure; New York-New York Hotel & Casino; Railroad Pass Hotel & Casino; Shadow Creek Golf Course; Slots-A-Fun Casino; The Signature at MGM Grand; vacant land near S. Decatur Blvd. & W. Oquendo Rd.; vacant land in Jean (formerly Nevada Landing); vacant land on Circus Circus Dr. & Las Vegas Blvd. So.; vacant land on Sahara & Las Vegas Blvd. So.; Vdara Hotel & Spa & Veer Towers) 2. NV ENERGY 1,555,475,949 4,444,216,997 3. CAESARS ENTERTAINMENT CORPORATION 1,467,895,338 4,193,986,680 (Includes 190 Flamingo LLC; Bally's Grand Hotel, Casino, Convention Area & Parking Garage; Bill's Gamblin' Hall & Saloon; Caesar's Linq; Caesar's Palace Hotel, Casino, Temple, Forum Shops, Tennis Pavillion, Magical Empire -

Examining the Enviormental Policies of Las Vegas Strip Hotels Andrew M

Hospitality Review Volume 27 Article 1 Issue 2 Hospitality Review Volume 27/Issue 2 January 2009 How Green the Desert? Examining the Enviormental Policies of Las Vegas Strip Hotels Andrew M. Levey Pure Management Group, Inc., Nevada Karl J. Mayer University of Nevada, Las Vegas, [email protected] Karima Abdel-Moty University of Nevada, Las Vegas, [email protected] Follow this and additional works at: https://digitalcommons.fiu.edu/hospitalityreview Part of the Finance Commons, and the Hospitality Administration and Management Commons Recommended Citation Levey, Andrew M.; Mayer, Karl J.; and Abdel-Moty, Karima (2009) "How Green the Desert? Examining the Enviormental Policies of Las Vegas Strip Hotels," Hospitality Review: Vol. 27 : Iss. 2 , Article 1. Available at: https://digitalcommons.fiu.edu/hospitalityreview/vol27/iss2/1 This work is brought to you for free and open access by FIU Digital Commons. It has been accepted for inclusion in Hospitality Review by an authorized administrator of FIU Digital Commons. For more information, please contact [email protected]. How Green the Desert? Examining the Enviormental Policies of Las Vegas Strip Hotels Abstract This study analyzed the websites of major Las Vegas Strip hotels, examined their corporate financial reports, and conducted two in-depth telephone interviews with hotel managers, all with regard to their “green” (pro- environmental) policies. The tudys found a distinct lack of evidence to support assertions that these properties had truly “gone green” in their daily operations. Thus, although the hotels might actually have been engaged in green procedures, they did not express environmental policy in their corporate websites or financial reports. -

Harrah's Entertainment, Inc

Table of Contents SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 8-K CURRENT REPORT Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 Date of report (Date of earliest event reported): January 11, 2008 (January 11, 2008) HARRAH’S ENTERTAINMENT, INC. (Exact Name of Registrant as Specified in Charter) Delaware 1-8747 62-1411755 (State or Other Jurisdiction (Commission File Number) (IRS Employer of Incorporation) Identification No.) One Caesars Palace Drive, Las Vegas, Nevada 89109 (Address of Principal Executive Offices, including Zip Code) Registrant’s telephone number, including area code: (702) 407-6000 Not Applicable (Former Name or Former Address, if Changed Since Last Report) Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions: ☐ Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) ☐ Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) ☐ Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) ☐ Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) Table of Contents Item 7.01. Regulation FD Disclosure On December 19, 2006, Harrah’s Entertainment, Inc. (“Harrah’s Entertainment”) announced that it had entered into a definitive merger agreement with Hamlet Holdings LLC, a Delaware limited liability company (“Hamlet Holdings”), and Hamlet Merger Inc., a Delaware corporation and a wholly owned subsidiary of Hamlet Holdings (“Merger Sub”), pursuant to which Merger Sub will merge with and into Harrah’s Entertainment, and Harrah’s Entertainment will become a subsidiary of Hamlet Holdings (the “Acquisition”). -

2007 US Lodging Report

GLOBAL REAL ESTATE CENTER !@# The 2007 US Lodging Report i ntroduction Dear Colleague, We are pleased to present the 2007 edition of Ernst & Young’s US Lodging Report. Our report offers our assessment of the direction of the US lodging industry, including our thoughts on key lodging industry trends and segment performance, as well as our detailed outlook for major metropolitan markets. Additional copies of this report are available through our local offices or on our Website <http://www.ey.com/us/realestate>. I would like to thank the Hospitality Services professionals who contributed significant time and effort in preparing the 2007 US Lodging Report. Ernst & Young’s Hospitality Services professionals provide developers, lenders, owners, and operators with an array of advisory services each year. Please feel free to contact me or any of the professionals mentioned at the end of this report if we may be of service. Sincerely, Michael Fishbin National Director, Hospitality & Leisure Ernst & Young LLP contents p.1 ❮❮ Top 10 Thoughts p.67 ❮❮ Fort Lauderdale p.13 ❮❮ Industry Overview p.73 ❮❮ Hawaii p.25 ❮❮ Global Hospitality p.79 ❮❮ Las Vegas Insights p.83 ❮❮ Los Angeles ❮❮ Spotlight Segments p.89 ❮❮ Manhattan p.30 ❮❮ Luxury p.95 ❮❮ Miami p.32 ❮❮ Upper Upscale p.101❮❮ New Orleans p.34 ❮❮ Upscale p.107❮❮ Orlando p.36 ❮❮ Midscale with Food and Beverage p.113❮❮ Phoenix p.38 ❮❮ Midscale without Food and p.119❮❮ San Diego Beverage p.125❮❮ San Francisco p.40 ❮❮ Economy p.131❮❮ Washington, D.C. ❮❮ Spotlight Regions and Markets p.43 ❮❮ Atlanta p.49 ❮❮ Boston p.55 ❮❮ Chicago p.61 ❮❮ Dallas T HE 2007 US LODGING REPORT top 10 thoughts top 10 thoughts 1. -

Wynn Macaumacau Wynnwynn Laslas Vegasvegas $1,300 Million 1St Mortgage Notes Due 2014

Citigroup EMT Conference January 11, 2007 Ron Kramer ForwardForward LookingLooking StatementsStatements This presentation contains forward-looking statements regarding operating trends, future results of operations and the completion of new projects, which are subject to change. Such forward-looking information involves important risks and uncertainties that could significantly affect anticipated results in the future and, accordingly, such results may differ from those expressed in any forward-looking statements made by us. Additional information concerning potential factors that could affect the Company's financial results are included in the Company's Form 10-K for the year ended December 31, 2005 and the Company's other periodic reports filed with the Securities and Exchange Commission. The Company is under no obligation to (and expressly disclaims any such obligation to) update its forward-looking statements as a result of new information, future events or otherwise. 2 CorporateCorporate StructureStructure Outlined area shows issuers, borrowers, guarantors and restricted subsidiaries under facilities WynnWynn Resorts,Resorts, LimitedLimited $250 million Convertible Subordinated Notes 100% 100% $900 million Revolver $225 million Term Loan WynnWynn MacauMacau WynnWynn LasLas VegasVegas $1,300 million 1st Mortgage Notes due 2014 $764 million Bank Facility 3 235 Acres on the Las Vegas Strip Treasure Island Fashion Show Trump Towers Flamingo Mall Venetian L Palazzo as Montreux Ve ga Maxim s Blv Sands d Stardust Expo Wynn Las (Echelon Place) Center Vegas Encore Circus- 20 Acres Circus Koval Land 55 Acres 18 Acres Desert Inn Road Sands Ave. Ave. Ave. Sands Sands Sands Golf Course 142 Acres Hughes Center Chamber of Commerce Las Vegas Paradise Road LV Hilton Convention Center Projects slated for completion 5 WynnWynn LasLas VegasVegas Follow the non-casino revenues – Hotel: First hotel in Las Vegas to receive the Mobil Five Star Rating – Restaurants: Every prize winning chef is at the property cooking dinner every night.