2007 US Lodging Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Amendment to Division D of Rules Committee Print 116-59 (Military Construction, Veterans Affairs Appropriations Division)

AMENDMENT TO DIVISION D OF RULES COMMITTEE PRINT 116-59 (MILITARY CONSTRUCTION, VETERANS AFFAIRS APPROPRIATIONS DIVISION) OFFERED BY MR. COHEN OF TENNESSEE At the end of division D (before the short title), insert the following: SEC. __. (a.) None of the funds made available by this Act appropriated or otherwise made available by this Act may be made available to enter into any new contract, grant, or cooperative agreement with any entity listed in subsection (b). (b) The entities listed in this subsection are the following: 4T HOLDINGS TWO LLC New York, NY 1125 South Ocean LLC Palm Beach, Florida 1290 Avenue of the Americas, A Tenancy-In- New York, New York Common 40 Wall Street LLC New York, New York 401 North Wabash Venture LLC Chicago, IL 610 Park Avenue New York City, NY 809 North Canon LLC Beverly Hills, CA Albemarle Estate Charlottesville, VA Caribuslness Investments, S.R.L. Dominican Republic County Properties, LLC Norfolk, VA D B Pace Acquisition, LLC New York, NY DJT Aerospace LLC New York, New York DJT HOLDINGS LLC New York, NY DJT Operations I LLC New York, New York DT Bali Golf Manager LLC New York, New York DT Bali Golf Manager Member Corp New York, New York DT Bali Hotel Manager LLC New York, New York DT Bali Hotel Manager Member Corp New York, New York DT Bali Technical Services Manager LLC New York, New York DT Bali Technical Services Manager Member New York, New York Corp DT Connect Europe Limited Turnberry, Scotland DT Connect II LLC Palm Beach, Florida DT Dubai Golf Manager LLC New York, New York 7/20/2020 12:15 PM -

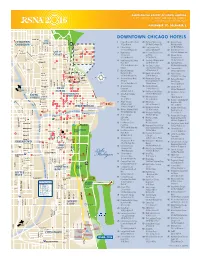

Hotel-Map.Pdf

RADIOLOGICAL SOCIETY OF NORTH AMERICA 102ND SCIENTIFIC ASSEMBLY AND ANNUAL MEETING McCORMICK PLACE, CHICAGO NOVEMBER 27 – DECEMBER 2 DOWNTOWN CHICAGO HOTELS OLD CLYBOURN 1 Palmer House Hilton Hotel 28 Fairmont Hotel Chicago 61 Monaco Chicago, CORRIDOR TOWN 17 East Monroe 200 North Columbus Dr. A Kimpton Hotel 2 Hilton Chicago 29 Four Seasons Hotel 225 North Wabash 23 720 South Michigan Ave. 120 East Delaware Pl. 62 Omni Chicago Hotel GOLD 60 70 3 Hyatt Regency 30 Freehand Chicago Hostel 676 North Michigan Ave. COAST 29 87 38 66 Chicago Hotel and Hotel 63 Palomar Chicago, 89 68 151 East Wacker Dr. 19 East Ohio St. A Kimpton Hotel 80 47 4 Hyatt Regency McCormick 31 The Gray, A Kimpton Hotel 505 North State St. Place Hotel 122 W. Monroe St. 64 Park Hyatt Hotel 2233 South Martin Luther 32 The Gwen, a Luxury 800 North Michigan Ave. King Dr. Collection Hotel, Chicago 65 Peninsula Hotel 5 Marriott Downtown 521 North Rush St. 108 East Superior St. 79 Magnificent Mile 33 Hampton Inn & Suites 66 Public Chicago 86 540 North Michigan Ave. 33 West Illinois St. 78 1301 North State Pkwy. Sheraton Chicago Hotel Hampton Inn Chicago 75 6 34 67 Radisson Blu Aqua & Towers Downtown Magnificent Mile 73 Hotel Chicago 301 East North Water St. 160 East Huron 221 N. Columbus Dr. 64 7 AC Hotel Chicago 35 Hampton Majestic 68 Raffaello Hotel NEAR 65 59 Downtown 22 West Monroe St. 201 East Delaware Pl. 62 10 34 42 630 North Rush St. NORTH 36 Hard Rock Hotel Chicago 69 Renaissance Chicago 46 21 MAGNIFICENT 230 North Michigan Ave. -

Lasvegasadvisor May 2021 • Vol

ANTHONY CURTIS’ LasVegasAdvisor May 2021 • Vol. 38 • Issue 5 $5 THE PASS OPENS Spruced up casino hits downtown Henderson … pgs. 1, 4, 5, 16 VIRGIN TERRITORY What’s the new joint all about? … pgs. 2, 8, 9, 12, 13, 14, 16 VAX PROMOS Take the shot, get a lot … pg. 3 BUFFETS Are they coming back? … pg. 7 POOL SEASON Cool pools open everywhere … pg. 14 CASINOS Local (702) Toll Free 2021 MEMBER Aliante Casino+Hotel+Spa ...................692-7777 ...... 877-477-7627 Aria .......................................................590-7111 ...... 866-359-7757 Arizona Charlie’s Boulder .....................951-5800 ...... 800-362-4040 REWARDS Arizona Charlie’s Decatur .....................258-5200 ...... 800-342-2695 Bally’s ...................................................739-4111 ...... 877-603-4390 Bellagio .................................................693-7111 ...... 888-987-7111 DINING, INCLUDING Binion’s .................................................382-1600 ...... 800-937-6537 “LOCAL CORNER”, DRINKS, Boulder Station .....................................432-7777 ...... 800-683-7777 Caesars Palace.....................................731-7110 ...... 866-227-5938 ATTRACTIONS, AND California ..............................................385-1222 ...... 800-634-6505 Cannery ................................................507-5700 ...... 866-999-4899 GAMBLING Casino Royale (Best Western Plus) ......737-3500 ...... 800-854-7666 Circa .....................................................247-2258 ...... 833-247-2258 Circus Circus ........................................734-0410 -

Golf Courses + Resorts Owned & Managed by TRUMP Domestic

Golf Courses + Resorts Owned & Managed by TRUMP Domestic: Trump International Golf Club, Palm Beach Trump National Golf Club, Jupiter Trump National Golf Club, Washington D.C. Trump National Doral, Miami (Hotel + Golf) Trump National Golf Club, Colts Neck Trump National Golf Club, Westchester Trump National Golf Club, Hudson Valley Trump National Golf Club, Bedminster Trump National Golf Club, Philadelphia Trump National Golf Club, Los Angeles Trump National Golf Club, Charlotte International: Trump International Golf Links, Aberdeen (Hotel + Golf) Trump International Golf Links & Hotel, Doonbeg, Ireland (Hotel + Golf) Trump Turnberry (Hotel + Golf) Golf Courses Developed + Managed by TRUMP Trump Golf Links at Ferry Point Golf Courses Managed by TRUMP Trump International Golf Club, Dubai Trump World Golf Club, Dubai Indonesia – Coming Soon Hotel Properties Owned & Managed by TRUMP Trump International Golf Links, Aberdeen (Hotel + Golf) Trump International Golf Links & Hotel, Doonbeg, Ireland (Hotel + Golf) Trump National Doral, Miami (Hotel + Golf) Trump Turnberry (Hotel + Golf) The Albemarle Estate at Trump Winery (Hotel) Trump International Hotel & Tower New York Trump International Hotel & Tower Chicago Trump International Hotel, Washington D.C. Hotel Properties Owned in Partnership & Managed by TRUMP Trump International Hotel Las Vegas – Partners with Phil Ruffin Hotel Properties Managed by TRUMP Trump SoHo New York Trump International Hotel & Tower Toronto Trump Ocean Club, Panama Trump International Hotel & Tower Vancouver – Coming -

Hyatt Place Chicago

USA-ILLINOIS-CHICAGO 2013 UNIVERSITY OF CHICAGO PREFERRED HOTEL PROGRAM USA-ILLINOIS-CHICAGO Hyatt Place Chicago - South Opening date in September, 2013 – Mar 31, 2014 Complimentary Amenities Include: 5225 S Harper Avenue $109 Standard Single Daily hot breakfast buffet Chicago, IL 60615 Internet access Phone: 773-752-5300 Apr 1 – Nov 30, 2014 Fitness center and indoor pool $159 Standard Single Local and (800) access telephone calls Waived early departure fees Closest hotel to the University, located in Dec 1 – Dec 31, 2014 the heart of Hyde Park’s vibrant Harper $109 Standard Single Court development offering restaurants, shopping and entertainment Rates: NLRA Cancellation Policy: By 6:00 PM local hotel, Twenty-four (24) Hyatt Place Chicago - South hours prior to day of arrival. These rates are provided to University faculty, staff, students, visitors, retirees, alumni, hospitals, and the Big Ten Universities. Rates are for individual travel only and may not apply to group bookings of 10 or more guest-rooms. Please ask for the “University of Chicago” rate. ** LRA (Last Room Availability) The traveler is allowed to book the last available room at the University rate. ** NLRA (Non-Last Room Availability) The University rate is available to travelers at the discretion of the hotel. In peak periods, hotels can block NLRA rates and charge a higher rate. As of 8/13/2013 CHINA-BEIJING 2013 UNIVERSITY OF CHICAGO PREFERRED HOTEL PROGRAM CHINA-BEIJING s Peninsula Beijing Jan 1 – Dec 31, 2013 2013 Blackout Periods: 8 Goldfish Lane, Wangfujing Deluxe -

Hotel Descriptions

2015 AERA Annual Meeting Thursday, April 16 – Monday, April 20 • Chicago, IL HOTEL DESCRIPTIONS *Chicago Marriot Downtown Magnificent Mile 540 North Michigan Avenue The Chicago Marriott Downtown Magnificent Mile is located on North Michigan Avenue in Chicago, IL. This property stands adjacent to Chicago’s Magnificent Mile shops where business and entertainment intersect. The hotel is centrally located to dining, shopping and entertainment. In addition, the hotel is conveniently located to some of Chicago’s premiere attractions to include Navy Pier, the John Hancock Building, and the Art Institute of Chicago, and the famous Willis Tower. The hotel features an urban style that reflects organic symmetry and clean architectural lines. A spiral staircase leads to the hotel's primary restaurant that serves contemporary and classic American fare enhanced with seasonal Midwest ingredients. A Starbucks outlet prepares coffee specialties and offers light fare. Additionally, a FedEx Kinko's Business Center offers extensive business services to include computer/printer stations. This 46-story hotel offers 1,198 earth-tone-decorated guestrooms and suites. Rooms are equipped with wired high-speed Internet access for a fee, and 32-inch flat-screen televisions. Beds are dressed with 300-thread count linens, down duvets and decorative bed scarves. Refrigerators are available, on request. Laptop-compatible in-room safes, and health club are complimentary. Courtyard By Marriott Magnificent Mile 165 East Ontario Street Ideally situated in the heart of Chicago, the Courtyard Chicago Downtown/Magnificent Mile is just a half block from Michigan Avenue and the legendary Magnificent Mile. This convenient location is also close to Millennium Park, the Art Institute of Chicago, and the Loop Business District. -

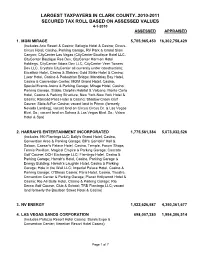

Largest Taxpayer Secured Values 2010-11

LARGEST TAXPAYERS IN CLARK COUNTY..2010-2011 SECURED TAX ROLL BASED ON ASSESSED VALUES 4-1-2010 ASSESSED APPRAISED 1. MGM MIRAGE 5,705,965,450 16,302,758,429 (Includes Aria Resort & Casino; Bellagio Hotel & Casino; Circus- Circus Hotel, Casino, Parking Garage, RV Park & Grand Slam Canyon; CityCenter Las Vegas (CityCenter Boutique Hotel LLC, CityCenter Boutique Res Dev, CityCenter Harmon Hotel Holdings, CityCenter Vdara Dev LLC, CityCenter Veer Towers Dev LLC, Crystals CityCenter all currently under construction); Excalibur Hotel, Casino & Stables; Gold Strike Hotel & Casino; Luxor Hotel, Casino & Pedestrian Bridge; Mandalay Bay Hotel, Casino & Convention Center; MGM Grand Hotel, Casino, Special Events Arena & Parking Garage; Mirage Hotel, Casino, Parking Garage, Stable, Dolphin Habitat & Volcano; Monte Carlo Hotel, Casino & Parking Structure; New York-New York Hotel & Casino; Railroad Pass Hotel & Casino; Shadow Creek Golf Course; Slots-A-Fun Casino; vacant land in Primm (formerly Nevada Landing); vacant land on Circus Circus Dr. & Las Vegas Blvd. So.; vacant land on Sahara & Las Vegas Blvd. So.; Vdara Hotel & Spa) 2. HARRAH'S ENTERTAINMENT INCORPORATED 1,775,561,384 5,073,032,526 (Includes 190 Flamingo LLC; Bally's Grand Hotel, Casino, Convention Area & Parking Garage; Bill's Gamblin' Hall & Saloon; Caesar's Palace Hotel, Casino, Temple, Forum Shops, Tennis Pavillion, Magical Empire & Parking Garage; Cascata Golf Course; DCH Exchange LLC; Flamingo Hotel, Casino & Parking Garage; Harrah's Hotel, Casino, Parking Garage & Energy Building; Harrah's Laughlin Hotel, Casino & Parking Garage; Hole in the Wall LLC; Imperial Palace Hotel, Casino & Parking Garage; O'Sheas Casino; Paris Hotel, Casino, Theatre, Convention Center & Parking Garage; Planet Hollywood Hotel & Casino; Rio All-Suite Hotel, Casino & Parking Garage; Rio Secco Golf Course, Club & School; TRB Flamingo LLC; vacant land formerly the Bourbon Street Hotel & Casino) 3. -

An Analysis of the Environmental Content of Las Vegas Strip Hotels

UNLV Theses, Dissertations, Professional Papers, and Capstones 12-2007 An Analysis of the environmental content of Las Vegas Strip hotels Andrew M. Levey Follow this and additional works at: https://digitalscholarship.unlv.edu/thesesdissertations Part of the Gaming and Casino Operations Management Commons, and the Sustainability Commons Repository Citation Levey, Andrew M., "An Analysis of the environmental content of Las Vegas Strip hotels" (2007). UNLV Theses, Dissertations, Professional Papers, and Capstones. 613. http://dx.doi.org/10.34917/1752239 This Professional Paper is protected by copyright and/or related rights. It has been brought to you by Digital Scholarship@UNLV with permission from the rights-holder(s). You are free to use this Professional Paper in any way that is permitted by the copyright and related rights legislation that applies to your use. For other uses you need to obtain permission from the rights-holder(s) directly, unless additional rights are indicated by a Creative Commons license in the record and/or on the work itself. This Professional Paper has been accepted for inclusion in UNLV Theses, Dissertations, Professional Papers, and Capstones by an authorized administrator of Digital Scholarship@UNLV. For more information, please contact [email protected]. AN ANALYSIS OF THE ENVIRONMENTAL CONTENT OF LAS VEGAS STRIP HOTELS Andrew M. Levey Bachelor of Science in Management Tulane University, New Orleans, Louisiana 2001 A professional paper submitted in partial fulfillment of the requirements for the Master Degree in Business Administration Department of College of Business College of Business Master of Science in Hotel Administration Department of William F. Harrah College of Hotel Administration William F. -

DONALD TRUMP REFLECTS on HIS BEGINNINGS, VENTURES, and PLANS for the FUTURE Donald Trump Chairman and President the Trump Organ

DONALD TRUMP REFLECTS ON HIS BEGINNINGS, VENTURES, AND PLANS FOR THE FUTURE Donald Trump Chairman and President The Trump Organization December 15, 2014 Excerpts from Mr. Trump's Remarks Are you considering running for President? I am considering it very strongly. How did you get started in business, buying a hotel, with almost no money? Well, it was owned by the Penn Central Railroad and it was run by some very good people. Actually, it's very interesting, because he happens to be a very good man. It was Victor Palmieri and Company. And one of the people is John Koskinen. Does anyone know John Koskinen? He's the head of the IRS. And he's a very good man. And while I'm a strong conservative and a strong Republican, he's a friend of mine. And he did a great job running Victor Palmieri. And I made deals with John and the people at Victor Palmieri and took options to the building. And after I took options to the Commodore, I then went to the city. Because the city was really in deep trouble. I was about 28 years old, and the city was really in trouble. And I said look, you're going to have to give me tax abatement. Otherwise this was never going to happen. Then I went to Hyatt. I said you guys put up all the money and I'll try and get the approvals. And I got all the approvals. And Hyatt, Jay Pritzker and the Pritzker family, they put up the money. -

Las Vegas Casino & Hotel Market Outlook 2009

Las Vegas Casino & Hotel Market Outlook 2009 Shannon Okada, Associate Director, HVS Gaming Services HVS — Las Vegas HVS — LAS VEGAS 8170 W. Sahara Avenue, Suite 201 Las Vegas, NV 89117 United States of America +1 (702) 242-6723 OFFICE MAIN TELEPHONE HTTP://WWW.HVS.COM January 2009 New York San Francisco Boulder Denver Atlanta Miami Dallas Las Vegas Chicago Washington, D.C. Weston, CT Boston Mt. Lakes, NJ Mexico City Vancouver Toronto London Moscow Madrid Athens Dubai Mumbai New Delhi Singapore Hong Kong Beijing Shanghai São Paulo Buenos Aires Las Vegas Casino and Hotel Market Outlook 2009 Shannon S. Okada Associate Director Gaming Services Division, Vice President Consulting & Valuation HVS – Las Vegas Any previously held notion that the Las Vegas gaming-tourism industry is recession-proof was dispelled in 2008 as, to quote the Las Vegas Review Journal, “the imploding economy drove a stake though the heart of the Strip.” The downturn in the national and worldwide economies, and the resulting decrease in consumer consumption, has reduced visitation to the Las Vegas market in 2008 to levels not seen since 2004, which was prior to the opening of major properties including the Wynn Las Vegas, South Point, Red Rock Station, Palazzo, and Encore. As quality new supply is absorbed and operators have implemented strategies to compete for overnight guests to support gaming and other amenities, average daily room rate has dropped. The recession is prompting visitors and locals to gamble less. Challenging economic conditions, including the turmoil in the credit markets, have also resulted in a scaled-back development pipeline. -

18 Tommy Bridges, Industry Connector 22 the Theme Park Brains Behind Caesars’ High Roller 24 Las Vegas Reinvents Itself

New tech for museums, parks & rides #53 • volume 10, issue 3 • 2014 www.inparkmagazine.com 18 Tommy Bridges, industry connector 22 The theme park brains behind Caesars’ High Roller 24 Las Vegas reinvents itself www.inparkmagazine.com 1 © SHOW: ECA2 - PHOTOS: JULIEN PANIE THINK SPECTACULAR! SPECIAL EVENTS I THEME PARKS & PERMANENT SHOWS I EXPOS & PAVILIONS “WINGS OF TIME” I SENTOSA ISLAND, SINGAPORE. STARTED IN JUNE 2014. TEL: +33 1 49 46 30 40 I CONTACT: [email protected] I WWW.ECA2.COM I FACEBOOK.COM/ECA2PARIS www.inparkmagazine.com #53• volume 10, issue 3 Wings of Time 6 ECA2 creates new Sentosa spectacular• by Martin Palicki IAAPA Beijing 10 Asian Attractions Expo: Martin Palicki reports Civil war surround 13 BPI produces video diorama for Kenosha museum • by Martin Palicki Leave it to Holovis 16 Modern tools of simulation & visualization• by Stuart Hetherington Building Bridges 18 Tommy Bridges = technology + opportunity • by Judith Rubin Caesars’ High Roller 22 Theme park savvy reinvents the wheel Tomorrow’s Vegas 24 The new investments: Joe Kleiman reports RFID changes everything 29 Disney’s MyMagic+ gets off to a strong start • by Martin Palicki The museum network 31 Artifact Technologies introduces Mixby platform• by Joe Kleiman Immersion with dinosaurs 33 Movie Park Germany opens The Lost Temple • by Judith Rubin Gamification and dark rides 36 Innovations from Triotech, Sally & Alterface Projects • by Joe Kleiman staff & contributors advertisers EDITOR DESIGN Alcorn McBride 35 © SHOW: ECA2 - PHOTOS: JULIEN PANIE Martin Palicki mcp, llc Alterface Projects 29 Artifact Technologies 34 CO-EDITOR CONTRIBUTORS Judith Rubin Stuart Hetherington All Things Integrated 19 Super 78 Boston Productions Inc. -

Case 8:17-Cv-01596-PJM Document 90-2 Filed 02/23/18 Page 1 of 49

Case 8:17-cv-01596-PJM Document 90-2 Filed 02/23/18 Page 1 of 49 IN THE UNITED STATES DISTRICT COURT FOR THE DISTRICT OF MARYLAND Greenbelt Division THE DISTRICT OF COLUMBIA 441 Fourth Street, N.W. Washington, D.C. 20001, and THE STATE OF MARYLAND 200 Saint Paul Place, 20th Floor Baltimore, Maryland 21202, Plaintiffs, Civil Action No. 8:17-cv-1596-PJM v. DONALD J. TRUMP, President of the United States of America, in his official capacity and in his individual capacity 1600 Pennsylvania Avenue, N.W. Washington, D.C. 20500, Defendant. AMENDED COMPLAINT BRIAN E. FROSH KARL A. RACINE Attorney General of Maryland Attorney General for the District of Columbia STEVEN M. SULLIVAN NATALIE O. LUDAWAY Federal Bar No. 24930 Chief Deputy Attorney General [email protected] Federal Bar No. 12533 PATRICK B. HUGHES [email protected] Federal Bar No. 19492 STEPHANIE E. LITOS* [email protected] Senior Counsel to the Attorney General Assistant Attorneys General [email protected] 200 Saint Paul Place, 20th Floor 441 Fourth Street, N.W. Baltimore, MD 21202 Washington D.C. 20001 T: (410) 576-6325 T: (202) 724-6650 F: (410) 576-6955 F. (202) 741-0647 Case 8:17-cv-01596-PJM Document 90-2 Filed 02/23/18 Page 2 of 49 NORMAN L. EISEN JOSEPH M. SELLERS Federal Bar No. 09460 Federal Bar No. 06284 [email protected] [email protected] NOAH D. BOOKBINDER* CHRISTINE E. WEBBER* [email protected] Cohen Milstein Sellers & Toll PLLC STUART C. MCPHAIL* 1100 New York Avenue, N.W.