Gaming Restructuring in Nevada

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Las Vegas Select Projects

BELLAGIO NOBU HOTEL AT CAESARS RED ROCK RESORT & SPA Las Vegas Select Projects American Airlines Admiral’s Club Golden Nugget Spa Palazzo Chairman Suites Aria Resort & Casino Green Valley Ranch Palms Casino Resort Aria Spa Hakkasan Executive Office Palms Fantasy Tower Bally’s Hard Rock PH Towers Westgate Bally’s South Tower Harrah’s Planet Hollywood Bellagio Hexx Restaurant RA Sushi Bellagio Entourage Suites Hilton Grand Vacations Paradise Red Rock Resort & Spa Bellagio Fitness Area Holiday Inn Express Renaissance Bellagio Spa Tower JW Marriott Rio Hotel & Casino Bellagio Steakhouse Las Vegas Arena Riviera Hotel & Casino Bellagio Suites Tower Las Vegas Arena MGM Suites Rock House Boca Park Las Vegas Fashion Show Mall Siena Trattoria Caesars Palace Augustus Tower Luxor Allied Esports Arena Stratosphere Caesars Palace Forum Tower Mandalay Bay The Linq Hotel & Casino Caesars Palace Roman Towers Mandarin Oriental The M Resort Spa & Casino Cosmopolitan Resort & Casino Marriott The Quad Resort & Casino Cosmopolitan East Tower Marriott Grand Chateau Tivoli Martini Bar Cosmopolitan Suites Metropolis Treasure Island Spa Court of Fountains MGM Grand Trophy Hills Drive Courtyard MGM Grand Stay Well Rooms Tru Las Vegas D Hotel MGM Grand Mansion Back Bay Trump Hotel D Hotel Suites MGM Mirage Vdara Condos Delano MGM Mirage Penthouses Vdara Hotel & Spa Delano Public Areas MGM Mirage Villas Veer Towers at City Center Drex Agency Monte Carlo Concert Hall Westin Embassy Suites Monte Carlo High Rise Park WLV Hotel & Spa Flamingo Hotel & Casino Monte Carlo Resort & Casino Wyndham Grand Desert Fontainebleau Resort Monte Carlo Resort Sambalatte Wynn Four Points MVC Grand Chateau Wynn Mojitos Four Seasons Nobu Hotel at Caesars Wynn Beauty Salon Golden Nugget One Summerlin ELECTRIC MIRROR® 425.776.4946 | electricmirror.com | [email protected] | © 2018 Electric Mirror. -

Lasvegasadvisor May 2021 • Vol

ANTHONY CURTIS’ LasVegasAdvisor May 2021 • Vol. 38 • Issue 5 $5 THE PASS OPENS Spruced up casino hits downtown Henderson … pgs. 1, 4, 5, 16 VIRGIN TERRITORY What’s the new joint all about? … pgs. 2, 8, 9, 12, 13, 14, 16 VAX PROMOS Take the shot, get a lot … pg. 3 BUFFETS Are they coming back? … pg. 7 POOL SEASON Cool pools open everywhere … pg. 14 CASINOS Local (702) Toll Free 2021 MEMBER Aliante Casino+Hotel+Spa ...................692-7777 ...... 877-477-7627 Aria .......................................................590-7111 ...... 866-359-7757 Arizona Charlie’s Boulder .....................951-5800 ...... 800-362-4040 REWARDS Arizona Charlie’s Decatur .....................258-5200 ...... 800-342-2695 Bally’s ...................................................739-4111 ...... 877-603-4390 Bellagio .................................................693-7111 ...... 888-987-7111 DINING, INCLUDING Binion’s .................................................382-1600 ...... 800-937-6537 “LOCAL CORNER”, DRINKS, Boulder Station .....................................432-7777 ...... 800-683-7777 Caesars Palace.....................................731-7110 ...... 866-227-5938 ATTRACTIONS, AND California ..............................................385-1222 ...... 800-634-6505 Cannery ................................................507-5700 ...... 866-999-4899 GAMBLING Casino Royale (Best Western Plus) ......737-3500 ...... 800-854-7666 Circa .....................................................247-2258 ...... 833-247-2258 Circus Circus ........................................734-0410 -

Tourism Corridor Redevelopment Opportunity Commercialsun Real Estate, Inc

Tourism Corridor Redevelopment Opportunity CommercialSun Real Estate, Inc. RAIDERS STADIUM MANDALAY BAY LUXOR EXCALIBUR HOTEL BALI HAI GOLF CLUB NEW YORK NEW YORK TROPICANA LAS VEGAS MONTE CARLO Las Vegas Blvd. MGM MGM GRAND GARDEN ARENA ATLANTIC AVIATION (PRIVATE HANGARS) MGM CONVENTION CENTER/ MARQUEE BALLROOM DECKOW LANE TOP GOLF SUBJECT PROPERTY TROPICANA AVENUE See Master Plan Map BLUEGREEN VACATIONS CLUB 36 (TIMESHARE) TOMPKINS AVENUE Hospitality/Multifamily | 4735 & 4755 Deckow Lane | Las Vegas, Nevada 89169 CONTACT TEAM Redevelopment Opportunity Cathy Jones, CPA, SIOR, CCIM Roy Fritz CEO Senior Vice President P (702) 968-7320 P (702) 968-7322 [email protected] [email protected] Jessica Cegavske Jennifer Lehr Vice President Senior Associate P (702) 968-7321 P (702) 968-7329 [email protected] [email protected] Prepared by Sun Commercial Real Estate, Inc.: 6140 Brent Thurman Way, Suite 140, Las Vegas, Nevada 89148 702 | 968 | 7300 Ph • 702 | 968 | 7301 Fax www.SunCommercialRE.com The above information has been obtained from sources we believe to be reliable, however we do not take responsibility for its correctness. CONFIDENTIALITY & DISCLOSURE Redevelopment Opportunity SUN COMMERCIAL REAL ESTATE, INC. (the “Broker”) has been authorized by the Seller of the Property (the “Seller”) to prepare and distribute the enclosed information (the “Material”) for the purpose of soliciting offers to purchase from interested parties. More detailed financial, title and tenant lease information may be made available upon request following the mutual execution of a letter of intent or contract to purchase between the Seller and a prospective purchaser. You are invited to review this opportunity and make an offer to purchase based upon your analysis. -

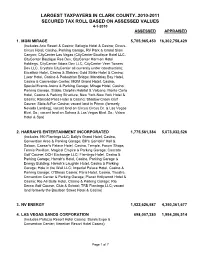

Largest Taxpayer Secured Values 2010-11

LARGEST TAXPAYERS IN CLARK COUNTY..2010-2011 SECURED TAX ROLL BASED ON ASSESSED VALUES 4-1-2010 ASSESSED APPRAISED 1. MGM MIRAGE 5,705,965,450 16,302,758,429 (Includes Aria Resort & Casino; Bellagio Hotel & Casino; Circus- Circus Hotel, Casino, Parking Garage, RV Park & Grand Slam Canyon; CityCenter Las Vegas (CityCenter Boutique Hotel LLC, CityCenter Boutique Res Dev, CityCenter Harmon Hotel Holdings, CityCenter Vdara Dev LLC, CityCenter Veer Towers Dev LLC, Crystals CityCenter all currently under construction); Excalibur Hotel, Casino & Stables; Gold Strike Hotel & Casino; Luxor Hotel, Casino & Pedestrian Bridge; Mandalay Bay Hotel, Casino & Convention Center; MGM Grand Hotel, Casino, Special Events Arena & Parking Garage; Mirage Hotel, Casino, Parking Garage, Stable, Dolphin Habitat & Volcano; Monte Carlo Hotel, Casino & Parking Structure; New York-New York Hotel & Casino; Railroad Pass Hotel & Casino; Shadow Creek Golf Course; Slots-A-Fun Casino; vacant land in Primm (formerly Nevada Landing); vacant land on Circus Circus Dr. & Las Vegas Blvd. So.; vacant land on Sahara & Las Vegas Blvd. So.; Vdara Hotel & Spa) 2. HARRAH'S ENTERTAINMENT INCORPORATED 1,775,561,384 5,073,032,526 (Includes 190 Flamingo LLC; Bally's Grand Hotel, Casino, Convention Area & Parking Garage; Bill's Gamblin' Hall & Saloon; Caesar's Palace Hotel, Casino, Temple, Forum Shops, Tennis Pavillion, Magical Empire & Parking Garage; Cascata Golf Course; DCH Exchange LLC; Flamingo Hotel, Casino & Parking Garage; Harrah's Hotel, Casino, Parking Garage & Energy Building; Harrah's Laughlin Hotel, Casino & Parking Garage; Hole in the Wall LLC; Imperial Palace Hotel, Casino & Parking Garage; O'Sheas Casino; Paris Hotel, Casino, Theatre, Convention Center & Parking Garage; Planet Hollywood Hotel & Casino; Rio All-Suite Hotel, Casino & Parking Garage; Rio Secco Golf Course, Club & School; TRB Flamingo LLC; vacant land formerly the Bourbon Street Hotel & Casino) 3. -

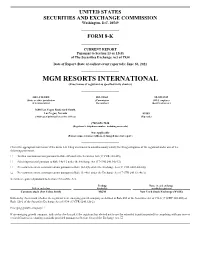

MGM RESORTS INTERNATIONAL (Exact Name of Registrant As Specified in Its Charter)

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 8-K CURRENT REPORT Pursuant to Section 13 or 15(d) of The Securities Exchange Act of 1934 Date of Report (Date of earliest event reported): June 30, 2021 MGM RESORTS INTERNATIONAL (Exact name of registrant as specified in its charter) DELAWARE 001-10362 88-0215232 (State or other jurisdiction (Commission (I.R.S. employer of incorporation) file number) identification no.) 3600 Las Vegas Boulevard South, Las Vegas, Nevada 89109 (Address of principal executive offices) (Zip code) (702) 693-7120 (Registrant’s telephone number, including area code) Not Applicable (Former name or former address, if changed since last report.) Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions: ☐ Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) ☐ Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) ☐ Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) ☐ Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) Securities registered pursuant to Section 12(b) of the Act: Trading Name of each exchange Title of each class Symbol(s) on which registered Common stock (Par Value $0.01) MGM New York Stock Exchange (NYSE) Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (17 §CRF 230.405) or Rule 12b-2 of the Securities Exchange Act of 1934 (17 CFR §240.12b-2). -

An Analysis of the Environmental Content of Las Vegas Strip Hotels

UNLV Theses, Dissertations, Professional Papers, and Capstones 12-2007 An Analysis of the environmental content of Las Vegas Strip hotels Andrew M. Levey Follow this and additional works at: https://digitalscholarship.unlv.edu/thesesdissertations Part of the Gaming and Casino Operations Management Commons, and the Sustainability Commons Repository Citation Levey, Andrew M., "An Analysis of the environmental content of Las Vegas Strip hotels" (2007). UNLV Theses, Dissertations, Professional Papers, and Capstones. 613. http://dx.doi.org/10.34917/1752239 This Professional Paper is protected by copyright and/or related rights. It has been brought to you by Digital Scholarship@UNLV with permission from the rights-holder(s). You are free to use this Professional Paper in any way that is permitted by the copyright and related rights legislation that applies to your use. For other uses you need to obtain permission from the rights-holder(s) directly, unless additional rights are indicated by a Creative Commons license in the record and/or on the work itself. This Professional Paper has been accepted for inclusion in UNLV Theses, Dissertations, Professional Papers, and Capstones by an authorized administrator of Digital Scholarship@UNLV. For more information, please contact [email protected]. AN ANALYSIS OF THE ENVIRONMENTAL CONTENT OF LAS VEGAS STRIP HOTELS Andrew M. Levey Bachelor of Science in Management Tulane University, New Orleans, Louisiana 2001 A professional paper submitted in partial fulfillment of the requirements for the Master Degree in Business Administration Department of College of Business College of Business Master of Science in Hotel Administration Department of William F. Harrah College of Hotel Administration William F. -

Las Vegas Casino & Hotel Market Outlook 2009

Las Vegas Casino & Hotel Market Outlook 2009 Shannon Okada, Associate Director, HVS Gaming Services HVS — Las Vegas HVS — LAS VEGAS 8170 W. Sahara Avenue, Suite 201 Las Vegas, NV 89117 United States of America +1 (702) 242-6723 OFFICE MAIN TELEPHONE HTTP://WWW.HVS.COM January 2009 New York San Francisco Boulder Denver Atlanta Miami Dallas Las Vegas Chicago Washington, D.C. Weston, CT Boston Mt. Lakes, NJ Mexico City Vancouver Toronto London Moscow Madrid Athens Dubai Mumbai New Delhi Singapore Hong Kong Beijing Shanghai São Paulo Buenos Aires Las Vegas Casino and Hotel Market Outlook 2009 Shannon S. Okada Associate Director Gaming Services Division, Vice President Consulting & Valuation HVS – Las Vegas Any previously held notion that the Las Vegas gaming-tourism industry is recession-proof was dispelled in 2008 as, to quote the Las Vegas Review Journal, “the imploding economy drove a stake though the heart of the Strip.” The downturn in the national and worldwide economies, and the resulting decrease in consumer consumption, has reduced visitation to the Las Vegas market in 2008 to levels not seen since 2004, which was prior to the opening of major properties including the Wynn Las Vegas, South Point, Red Rock Station, Palazzo, and Encore. As quality new supply is absorbed and operators have implemented strategies to compete for overnight guests to support gaming and other amenities, average daily room rate has dropped. The recession is prompting visitors and locals to gamble less. Challenging economic conditions, including the turmoil in the credit markets, have also resulted in a scaled-back development pipeline. -

18 Tommy Bridges, Industry Connector 22 the Theme Park Brains Behind Caesars’ High Roller 24 Las Vegas Reinvents Itself

New tech for museums, parks & rides #53 • volume 10, issue 3 • 2014 www.inparkmagazine.com 18 Tommy Bridges, industry connector 22 The theme park brains behind Caesars’ High Roller 24 Las Vegas reinvents itself www.inparkmagazine.com 1 © SHOW: ECA2 - PHOTOS: JULIEN PANIE THINK SPECTACULAR! SPECIAL EVENTS I THEME PARKS & PERMANENT SHOWS I EXPOS & PAVILIONS “WINGS OF TIME” I SENTOSA ISLAND, SINGAPORE. STARTED IN JUNE 2014. TEL: +33 1 49 46 30 40 I CONTACT: [email protected] I WWW.ECA2.COM I FACEBOOK.COM/ECA2PARIS www.inparkmagazine.com #53• volume 10, issue 3 Wings of Time 6 ECA2 creates new Sentosa spectacular• by Martin Palicki IAAPA Beijing 10 Asian Attractions Expo: Martin Palicki reports Civil war surround 13 BPI produces video diorama for Kenosha museum • by Martin Palicki Leave it to Holovis 16 Modern tools of simulation & visualization• by Stuart Hetherington Building Bridges 18 Tommy Bridges = technology + opportunity • by Judith Rubin Caesars’ High Roller 22 Theme park savvy reinvents the wheel Tomorrow’s Vegas 24 The new investments: Joe Kleiman reports RFID changes everything 29 Disney’s MyMagic+ gets off to a strong start • by Martin Palicki The museum network 31 Artifact Technologies introduces Mixby platform• by Joe Kleiman Immersion with dinosaurs 33 Movie Park Germany opens The Lost Temple • by Judith Rubin Gamification and dark rides 36 Innovations from Triotech, Sally & Alterface Projects • by Joe Kleiman staff & contributors advertisers EDITOR DESIGN Alcorn McBride 35 © SHOW: ECA2 - PHOTOS: JULIEN PANIE Martin Palicki mcp, llc Alterface Projects 29 Artifact Technologies 34 CO-EDITOR CONTRIBUTORS Judith Rubin Stuart Hetherington All Things Integrated 19 Super 78 Boston Productions Inc. -

Disposition: Approved

D I S P O S I T I O N * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * A G E N D A * NEVADA GAMING COMMISSION MEETING **(STATE GAMING CONTROL BOARD) State Gaming Control Board Offices Conference Room 2450 555 East Washington Avenue Las Vegas, Nevada July 23, 2009 10:00 A.M. • Pledge of Allegiance • Nonrestricted Agenda Items • Restricted Agenda Items • Administrative Matters • Complaint(s) • Public Comments • Gaming Employee Registrations Pursuant to NRS 463.335(13) • Gaming Employee Registrations Pursuant to NGC Regulation 5.109 • Informational Items Nevada Gaming Commission July 23, 2009 Page 2 10:00 A.M. ADMINISTRATIVE MATTERS 1. CONSIDERATION OF: Administrative Reports . Board Chairman . Pending Applications . Commission Chairman . Attorney General . Senior Research Specialist COMPLAINT(S) 2. CONSIDERATION OF: Settlement Agreement received Settling Complaint filed in the Matter of the STATE GAMING CONTROL BOARD vs. CONVENIENCE MART OF NEVADA, INC., dba ST. TROPEZ CONVENIENCE MART; CONVENIENCE MART OF NEVADA, INC., dba, ST. TROPEZ LIQUOR STORE; RICHARD CARL RITZO; JOELLEN DARLING RITZO; KIMBERLY ANN ANTONACCI; BERNICE E ANTONACCI TRUST; BERNICE ELIZABETH ANTONACCI, Case No. 08-15. STIPULATION ADOPTED AS THE ORDER OF THE NGC. 3. CONSIDERATION OF: Settlement Agreement received Settling Complaint filed in the Matter of the STATE GAMING CONTROL BOARD vs. OPBIZ, LLC, dba PLANET HOLLYWOOD RESORT & CASINO, Case No. 08-18. STIPULATION ADOPTED AS THE ORDER OF THE NGC. 4. PUBLIC COMMENTS: This public comment agenda item is provided in accordance with NRS 241.020(2)(c)(3) which requires an agenda provide for a period devoted to comments by the general public, if any, and discussion of those comments. -

Annual Report 2006

ANNUAL REPORT 2006 The Venetian Macao on the Cotai StripTM ~ Coming Summer 2007 The Venetain The Palazzo Sands Bethworks Sands Macao Marina Bay Sands Las Vegas ~ May 3, 1999 Las Vegas ~ 2007 Pennsylvania ~ 2008 Macao ~ May 18, 2004 Singapore ~ 2009 ellow Shareholders: I am pleased to present to you our third Annual Report. The Year 2006 was another record-setting year for our company as we executed on our operating and development plans around the globe. Our strong financial and operating performance, coupled with our victory in the global competition to build Singapore’s first Integrated Resort at Marina Bay, has clearly cemented our position as the preeminent worldwide developer and operator of premium convention-based destination hotel casino resorts. We again set occupancy and financial records at our flagship resort, The Venetian in Las Vegas. We also delivered record financial results at the Sands Macao, the first Las Vegas-style casino in The People’s Republic of China’s Special Administrative Region of Macao. In addition, we made substantial progress toward the completion of construction of two new mega-resorts, The Palazzo™, adjacent to The Venetian on the Las Vegas Strip, and The Venetian Macao, which will anchor our Cotai Strip™ development in Macao. Each of these resorts will open in 2007. In addition to our progress on The Venetian Macao, we continued to execute our master plan to develop the Cotai Strip into Asia’s premier leisure and convention destination. We began the development of six additional Cotai Strip properties, three of which will open in 2008, with the remainder to open in 2009. -

Recommended Hotel Guide

RECOMMENDED HOTEL GUIDE SOUTH LAS VEGAS HOTELS HOTELS NEAR PFC HEADQUARTERS HOTELS NEAR NELLIS AFB/LAS VEGAS MOTOR SPEEDWAY CENTRALIZED LAS VEGAS HOTELS 1 SOUTH LAS VEGAS HOTELS The following hotel properties are a 10-20 minute drive from PFC-HQ and 30-35 minute drive from PFC’s Pioneer Annex Range Complex (PARC) in Goodsprings, NV M Resort 12300 Las Vegas Blvd S. Henderson, NV 89044 Hotel (702) 797-1000 Reservations (877) 673-7678 http://www.themresort.com/ Gold Strike Hotel & Gambling Hall 1 Main St. Jean, NV 89019 Hotel (702) 477-5000 Reservations (800) 634-1359 http://www.goldstrikejean.com/ * Gold Strike is approximately 10 minutes from the PFC range complex, but a 20-minute drive from South Las Vegas. South Point Hotel Casino 9777 Las Vegas Blvd S. Las Vegas, NV 89183 Hotel (702) 797-8075 Reservations (866)-791-7626 http://southpointcasino.com/ Silverton Casino Hotel 3333 Blue Diamond Rd. Las Vegas, NV 89139 Hotel (702) 263-7777 Reservations (866) 722-4608 http://silvertoncasino.com/ 2 Baymont Inn & Suite LV Strip South 55 E Robindale Road Las Vegas, NV 89123 Hotel (702) 273-2500 Reservations (800) 337-0550 https://www.wyndhamhotels.com/baymont/las-vegas-nevada/baymont-inn- and-suites-airport-south-las- vegas/overview?CID=LC:BU:20160927:RIO:Local:SM-bumotn Diamond Resorts International Cancun Resort 8335 Las Vegas Boulevard South Las Vegas, Nevada, 89123 Hotel (702) 614-6200 Reservations (888) 249-8810 https://www.diamondresorts.com/destinations/property/Cancun-Resort-Las- Vegas Best Western Plus St. Rose Pkwy/Las Vegas South Hotel 3041 Saint Rose Pkwy. -

The Shrw Eagle

RSVP to the September Luncheon now: https://www.eventbrite.com/e/shrw- THE SHRW EAGLE luncheon-september-22-2020-tickets- Monthly Newsletter of Southern Hills Republican Women Visit Our Website: www.shrwhendersonrepublicanwomen.com AUGUST 2020 PRESIDENT’S LETTER Monthly GOP Events Around Town Honoring the Great American Story Active Republican Women (ARW) - He did it again! www.arwlv.com - Meets the 3rd Thursday of each month at Red Rock Country Club at President Trump proved once again that he can quickly adapt to difficult, ever- 5:30pm changing situations and not just come up with Plan B but create a vision of some- Boulder City Republican Women - thing even www.chamberorganizer.com/bouldercity/ greater, all while staying one-step ahead of everyone trying to take him down. Cancellation of the RNC mem_bcrw - Meets the 3rd Thursday at convention in Jacksonville, FL due to Covid 19 only created a new opportunity. Railroad Pass Hotel/Casino at 11am Mesquite Republican Women - While the Democrats were painting a picture of America as a dark, racist country that that will only get www.mesquiterepublicanwomen.org - Meets the 2nd Wednesday at Mesquite worse unless you vote for Biden/Harris, President Trump was jetting overhead in Air Force One cam- Veterans Center at 5pm paigning in key battleground states! That’s right, President Trump was speaking in front of enthusiastic Nevada Republican Club - crowds in Minnesota, Wisconsin and Arizona. And the piece de resistance was….. campaigning right in www.nevadarepublicanclub.com - Meets Biden’s