HALYK AR English Version Final 28 04 18.Cdr

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

LEGAL REGULATION of Npos' FUNDRAISING ACTIVITIES USING

An Analytical Overview LEGAL REGULATION OF NPOs’ FUNDRAISING ACTIVITIES USING NON-CASH PAYMENT SYSTEMS IN THE REPUBLIC OF KAZAKHSTAN1 PREPARED FOR International Center for Not-for-Profit Law (ICNL) PREPARED BY Roza Salibekova 1 This overview is made possible by the support of the American people through the United States Agency for International Development (USAID). The contents are the sole responsibility of ICNL and do not necessarily reflect the views of USAID or the United States Government. © ICNL, 2018 Translated from Russian Written and compiled by Roza Salibekova Legal Regulation of NCOs’ Fundraising Activities Using Non-Cash Payment Systems in the Republic of Kazakhstan / Written and compiled by Roza Salibekova. This overview is designed to inform private individuals and not-for-profit organizations about the key provisions of the Kazakh legislation that NCOs have to comply with in raising funds from legal and physical persons via non-cash payment facilities. Based on a comprehensive analysis of applicable Kazakh legislation, the study contains information of educational and practical value. Intended for a broad readership. DISCLAIMER. The materials presented in this handbook are intended for general use. No action or inaction should be taken based solely on the contents of this information, which cannot be regarded as legal advice. ICNL shall not be responsible for the accuracy and completeness of information in this handbook or any consequences of its use. Readers should consult with a legal professional on any specific legal matter before acting on any of the information presented. © International Center for Not-for-profit Law, 2018 © ICNL, 2018 2 Contents Goals and Objectives 4 Facts and Background 4 1. -

ADC Memorial Input for Report on Declaration on Minorities 31

www.adcmemorial.org Rue d’Edimbourg, 26, 1050 Brussels Anti-Discrimination Centre Memorial works on protection of the rights of discriminated minorities and migrants in Eastern Europe and Central Asia, carrying out monitoring, reporting, advocacy on local and international level, opposing discrimination by litigation and human rights education. Input to the report on "Effective promotion of the Declaration on the Rights of Persons Belonging to National or Ethnic, Religious and Linguistic Minorities" 31 March 2021 In the present submission Anti-Discrimination Centre Memorial provides brief information regarding violation of the rights of some ethnic minorities in the region of Eastern Europe and Central Asia, namely Crimean Tatar people in the annexed Crimea Peninsula; Roma in Russia; linguistic and indigenous peoples in Russia; Mugat (Roma-like community living in ex-USSR Central Asian countries); ethnic minorities of Tajikistan (Pamiri, a group of peoples living in Gorno-Badakhshan Autonomous Oblast, and a small minority of Yaghnobi); Dungan minority in Kazakhstan; Uzbeks in Kyrgyzstan. Main Conclusion In all the situations considered, violations of the rights of ethnic minorities occur due to the state's "national policy", contrary to the guarantees and agreements listed in the Declaration on the Rights of Minorities, the Convention on the Elimination of All Forms of Racial Discrimination and other respective international documents. These violations are systemic in nature, so the UN Human Rights bodies should call on the authorities of these countries to respect the rights of ethnic, linguistic and religious minorities. Special attention should be paid to the rights of indigenous peoples and those minorities who do not have statehood / autonomy and are therefore not sufficiently recognized by the authorities of the countries where they live. -

Central Securities Depository JSC

Central Securities Depository JSC AAAnnnnnnuuuaaalll RRReeepppooorrrttt 222000000666 Almaty 2007 Annual 2006 Report of Central Securities Depository JSC Table of Contents I. SHAREHOLDERS AND CHARTER CAPITAL ............................................................. 3 SHAREHOLDERS ...................................................................................................................... 3 CHARTER CAPITAL.................................................................................................................. 4 II. DEPOSITORY ACTIVITIES............................................................................................ 5 CLIENTS .................................................................................................................................. 5 CLIENT ACCOUNTS AND SUB-ACCOUNTS ................................................................................ 7 NOMINAL HOLDING ................................................................................................................ 7 Summary............................................................................................................................. 7 State Securities ................................................................................................................... 9 Non-State Securities ........................................................................................................... 9 Securities Issued Under Foreign Laws ............................................................................ 10 -

From Two to Six People of 350-550 Kilograms

1 BOLD ACCOMPLISHMENTS from two to six people of 350-550 kilograms The first woman to fly in a hot air balloon was1784 the 19-year-old Frenchwoman Elisabeth Thible. The flight was made in a hot air balloon called La Gustave in 1784 and lasted 45 minutes. The opera singer dressed as the goddess Minerva bravely climbed into it, amazing the crowd. A confident ascent Hot air balloons lift from two to six people into the air with a maximum payload of 350-550 kilograms. The world record holder is a 35-seat balloon with a two-story gondola. 2 2 4 Glossary 6 Chairman of the Board of Directors 8 Board of Directors 12 Chairman of the Bank's Management Board 14 Management Board of the Bank 21 Executive Summary 23 Shareholders and Capital. Dividend Policy 25 A Brief History of Bank CenterCredit 27 Overview of the macroeconomics and banking sector of the Republic of Kazakhstan 30 Review of Financial Performance 38 Overview of Core Operations 56 Risk Management System 60 Internal Control and Audit System 63 Information on the amount and composition of remuneration for members of the Board of Directors and the Management Board of the Bank for 2017. 64 Social Responsibility and Environmental Protection 69 Corporate Governance 77 Subsidiaries 79 Key Goals and Objectives for 2018 80 Information for Shareholders 83 Independent Auditors Report 2 3 1 ADB Asian Development Bank 2 ABS Automated banking system 3 Colvir ABS/Colvir Banking System Colvir is the Bank's current IT platform 4 AIS LEA Automated Information System for Law Enforcement Agencies 5 Damu EDF JSC / Damu Fund Damu Enterprise Development Fund JSC 6 ATM (Eng. -

US General Purpose Brands Purchase Volume In

FOR 46 YEARS, THE LEADING PUBLICATION COVERING PAYMENT SYSTEMS WORLDWIDE FEBRUARY 2017 / ISSUE 1103 Mastercard and Visa — U.S. 2016 Mastercard and Visa credit, debit, and prepaid cards issued in the U.S. General Purpose Brands U.S. generated $4.326 trillion in purchase volume (spending at merchants) in 2016, an increase of 9.5% over 2015. All consumer Purchase Volume in 2016 (Tril.) and commercial card products are included in that amount. > see p. 9 with Change vs. 2015 Alipay QR Code Payments to the U.S./Canada up $1.549 Visa Alipay, the largest processor of online and mobile payments in 15% Credit China, is building brick and mortar merchant acceptance networks for its mobile wallet product in the U.S. and Canada to serve up Visa $1.465 visiting Chinese consumers. The company says that more than Debit 7% > see p. 5 Sionic Mobile’s Rewards Marketplace down American $0.695 Airlines, hotels, car manufacturers, mobile network operators, 3% Express large retailers, and other enterprises that offer mobile apps for customer loyalty see opportunities to “earn and burn” rewards Mastercard up $0.693 points at each other’s locations. One example of earn and burn Credit 6% > see p. 12 Overdraft Credit for Millennials up $0.619 Mastercard Debit The Consumer Financial Protection Bureau says that revenues to 7% financial institutions in the U.S. from overdrafts consumers made from their demand deposit accounts (DDA), commonly known up Discover $0.121 as checking accounts, totaled $17 billion in 2016. The typical 3% > see p. 7 ID Insight Fights Account Takeover Fraud © 2017 The Nilson Report When ID Insight started offering products in 2003 to combat takeover of an existing account as well as fraud tied to opening a new account in the name of an unsuspecting existing cardholder, General Purpose Cards — U.S. -

![Cascacentre for Anthropoligical Studies on Central Asia [Eds Peter Finke and Günther Schlee]](https://docslib.b-cdn.net/cover/0218/cascacentre-for-anthropoligical-studies-on-central-asia-eds-peter-finke-and-g%C3%BCnther-schlee-2050218.webp)

Cascacentre for Anthropoligical Studies on Central Asia [Eds Peter Finke and Günther Schlee]

CASCACENTRE FOR ANTHROPOLIGICAL STUDIES ON CENTRAL ASIA [Eds Peter Finke and Günther Schlee] FRAMING THE RESEARCH, INITIAL PROJECTS HALLE (SAALE) 2013 MAX PLANCK INSTITUTE FOR SOCIAL ANTHROPOLOGY DEPartment ‘IntegraTION AND CONFLICt’ FIELD NOTES AND RESEARCH PROJECTS VI In the FIELD NOTES AND RESEARCH PROJECTS Series the following titles have been published so far: (I) Schlee, Günther (ed.): Pastoralism in Interaction with other Forms of Land Use in the Blue Nile Area of the Sudan: Project Outline and Field Notes 2009–10 (Halle, 2012) (II) Schlee, Isir, Beleysa Hambule, and Günther Schlee: The Moiety Division and the Problem of Rendille Unity: A Discussion among Elders, Korr, 21st January, 2008 (Halle, 2012) (III) Awad Alkarim and Günther Schlee (eds): Pastoralism in Interaction with other Forms of Land Use in the Blue Nile Area of the Sudan II: Herbarium and Plant Diversity in the Blue Nile Area, Sudan (Halle, 2013) (IV) Lenart, Severin: The Complexity of the Moment – Picturing an Ethnographic Project in South Africa and Swaziland: Vol. I: Photo Essays and Fieldwork Reports, 2007–11 (Halle, 2013) (V) Lenart, Severin: The Complexity of the Moment – Picturing an Ethnographic Project in South Africa and Swaziland: Vol. II: Photo Essays and Court Cases, 2007–11 (Halle, 2013) (VI) Finke, Peter, and Günther Schlee (eds): CASCA – Centre for Anthropological Studies on Central Asia: Framing the Research, Initial Projects (Halle, 2013) For teaching purposes, selected volumes are available as online PDFs under www.eth.mpg.de/dept_schlee_series_fieldnotes/index.html MAX PLANCK INSTITUTE FOR SOCIAL ANTHROPOLOGY DEPARTMent ‘IntegraTION AND CONFLICT’ FIELD NOTES AND RESEARCH PROJECTS VI CASCA – Centre for Anthropological Studies on Central Asia: Framing the Research, Initial Projects Published by Max Planck Institute for Social Anthropology, Halle (Saale) P. -

'Halyk Savings Bank of Kazakhstan' Consolidated

17 November 2017 Joint Stock Company ‘Halyk Savings Bank of Kazakhstan’ Consolidated financial results for the nine months ended 30 September 2017 Joint Stock Company ‘Halyk Savings Bank of Kazakhstan’ and its subsidiaries (together “the Bank”) (LSE: HSBK) releases its condensed interim consolidated financial information for the nine months ended 30 September 2017. Umut Shayakhmetova, the Bank’s CEO commented: “The third quarter has been marked by the acquisition of Kazkommertsbank. In the past few months, we have been working intensively on integration of our new subsidiary, bringing all policies, risk and cost control to Halyk Bank’s standard and making necessary changes in KKB management team. The strategy for the enlarged Halyk Group is under development and to be announced by the end of the year. However, we believe our first joint consolidated results with KKB look promising.” Statement of profit or loss review Change, Change, 9m 2017 9m 2016 abs Y-o-Y, % 3Q 2017 3Q 2016 abs Y-o-Y, % Interest income 339,052 244,046 95,006 38.9% 154,347 86,175 68,172 79.1% Interest expense -172,236 -118,844 -53,392 44.9% -86,314 -40,092 -46,222 2.2x Net interest income before impairment 166,816 125,202 41,614 33.2% 68,033 46,083 21,950 47.6% charge Fee and commission 58,880 42,292 16,588 39.2% 28,893 14,700 14,193 96.6% income Fee and commission -16,029 -8,427 -7,602 90.2% -9,922 -2,324 -7,598 4.3x expense Net fee and 42,851 33,865 8,986 26.5% 18,971 12,376 6,595 53.3% commission income Insurance income(1) 3,560 1,899 1,661 87.5% 2,358 759 1,599 -

Joint Stock Company 'Halyk Savings Bank Of

18 May 2018 Joint Stock Company ‘Halyk Savings Bank of Kazakhstan’ Consolidated financial results for the three months ended 31 March 2018 Joint Stock Company ‘Halyk Savings Bank of Kazakhstan’ and its subsidiaries (together “the Bank”) (LSE: HSBK) releases its condensed interim consolidated financial information for the three months ended 31 March 2018. Statement of profit or loss review Change, 1Q 2018 4Q 2017 abs Q‐o‐Q, % Interest income 162,005 167,276 ‐5,271 ‐3.2% Interest expense ‐87,617 ‐ 85,569 ‐2,048 2.4% Net interest income before credit loss expense 74,388 81,707 ‐7,319 ‐9.0% Fee and commission income 26,374 28,760 ‐2,386 ‐8.3% Fee and commission expense ‐9,680 ‐10,703 1,023 ‐9.6% Net fee and commission income 16,694 18,057 ‐1,363 ‐7.5% Insurance income(1) 292 2,933 ‐2,641 ‐90.0% FX operations(2) 55,425 43,216 12,209 28.3% Loss from derivative operations and securities (3) ‐42,546 ‐27,877 ‐14,669 52.6% Other non‐interest income 15,764 14,179 1,585 11.2% Credit loss expense (4) ‐5,197 ‐43,149 37,952 ‐88.0% Recoveries of other credit loss expense(5) 1,355 1,275 80 6.3% Operating expenses ‐36,084 ‐46,216(6) 10,132 ‐21.9% Income tax expense ‐10,159 ‐8,167 -1,992 24.4% Profit from discontinued operations 2,585 2,134 451 21.1% Non‐controlling interest in net income ‐10,464 ‐51 ‐10,413 205.2x Net income 62,053 38,041 24,012 63.1% Net interest margin, p.a. -

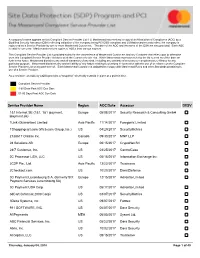

Service Provider Name Region AOC Date Assessor DESV

A company’s name appears on this Compliant Service Provider List if (i) Mastercard has received a copy of an Attestation of Compliance (AOC) by a Qualified Security Assessor (QSA) reflecting validation of the company being PCI DSS compliant and (ii) Mastercard records reflect the company is registered as a Service Provider by one or more Mastercard Customers. The date of the AOC and the name of the QSA are also provided. Each AOC is valid for one year. Mastercard receives copies of AOCs from various sources. This Compliant Service Provider List is provided solely for the convenience of Mastercard Customers and any Customer that relies upon or otherwise uses this Compliant Service Provider list does so at the Customer’s sole risk. While Mastercard endeavors to keep the list current as of the date set forth in the footer, Mastercard disclaims any and all warranties of any kind, including any warranty of accuracy or completeness or fitness for any particular purpose. Mastercard disclaims any and all liability of any nature relating to or arising in connection with the use of or reliance on the Compliant Service Provider List or any part thereof. Each Mastercard Customer is obligated to comply with Mastercard Rules and other Standards pertaining to use of a Service Provider. As a reminder, an AOC by a QSA provides a “snapshot” of security controls in place at a point in time. Compliant Service Provider 1-60 Days Past AOC Due Date 61-90 Days Past AOC Due Date Service Provider Name Region AOC Date Assessor DESV 1&1 Internet SE (1&1, 1&1 ipayment, Europe 05/08/2017 Security Research & Consulting GmbH ipayment.de) 1Link (Guarantee) Limited Asia Pacific 11/14/2017 Foregenix Limited 1Shoppingcart.com (Web.com Group, lnc.) US 04/29/2017 SecurityMetrics 2138617 Ontario Inc. -

Taxonomic Corrections and New Records in Vascular Plants of Kyrgyzstan, 4

Memoranda Soc. Soc. Fauna Fauna Flora Flora Fennica Fennica 91, 91: 2015 67–83. • Lazkov 2015 & Sennikov 67 Taxonomic corrections and new records in vascular plants of Kyrgyzstan, 4 Georgy A. Lazkov & Alexander N. Sennikov* Lazkov, G.A., Laboratory of Flora, Institute of Biology and Soil Science, Kyrgyz Academy of Sciences, 720071 Bishkek, Kyrgyzstan. E-mail: [email protected] Sennikov, A.N., Botanical Museum, Finnish Museum of Natural History, P.O. Box 7, 00014 University of Helsinki, Finland; & Herbarium, Komarov Botanical Institute of Russian Academy of Sciences, Prof. Popov str. 2, 197376 St Petersburg, Russia. E-mail: alexander.sennikov@ helsinki.fi (*Author for correspondence) A new series of notes on distribution, taxonomy, morphology and nomenclature of some vascular plants in Kyrgyzstan is presented. Carex subphysodes Popov ex V.Krecz., Astragalus sogdianus Bunge, Oxytropis ferganensis Vass. and Iris maracandica (Vved.) Wendelbo (all native), and also Delphinium orientalis J.Gay (alien) are reported as new to Kyrgyzstan. Sedum tetramerum Trautv. is new to Northern Tian-Shan, and Scirpoides holoschoenus (L.) Soják is new to Chatkal Range and Western Tian-Shan within Kyrgyzstan. The distribution area of Torilis arvensis (Huds.) Link is revised and expanded, and the distribution of Eremurus zoae Vved. (endemic to Kyrgyzstan) is verified and mapped. New names and combinations, Betonica sect. Foliosae (Krestovsk. & Laz- kov) Lazkov, Eriophyton anomalum (Juz.) Lazkov & Sennikov, Kudrjaschevia sect. Jacubianae Lazkov, Lagochilus sect. Chlainanthus (Briq.) Lazkov, Leonurus sect. Panzerioidei (Krestovsk.) Lazkov, Phlomoides sect. Pseuderemostachys (Popov) Lazkov, and Scutellaria sect. Ramosissi- mae Lazkov, are provided as a result of the forthcoming monographic revision of Lamiaceae. Two hybrids are described in Eremurus, E. -

CAUSES of ETHNIC CLASHES in KAZAKHSTAN.Pdf

THESIS APPROVAL FORM NAZARBAYEV UNIVERSITY SCHOOL OF HUMANITIES AND SOCIAL SCIENCES CAUSES OF ETHNIC CLASHES IN KAZAKHSTAN ПРИЧИНЫ ЭТНИЧЕСКИХ КОНФЛИКТОВ В КАЗАХСТАНЕ ҚАЗАҚСТАНДАҒ Ы ЭТНИКАЛЫҚ ҚАҚТЫҒ ЫСТАРДЫҢ СЕБЕПТЕРІ BY Vlad Lim NU Student Number: 201950507 APPROVED BY Dr. Hélène Thibault ON 27 May, 2021 Signature of Principal Thesis Adviser In Agreement with Thesis Advisory Committee Second Adviser: Dr. Karol Czuba External Reader: Dr. Barbara Junisbai CAUSES OF ETHNIC CLASHES IN KAZAKHSTAN ПРИЧИНЫ ЭТНИЧЕСКИХ КОНФЛИКТОВ В КАЗАХСТАНЕ ҚАЗАҚСТАНДАҒЫ ЭТНИКАЛЫҚ ҚАҚТЫҒЫСТАРДЫҢ СЕБЕПТЕРІ by Vlad Lim A thesis submitted in partial fulfillment of the requirements for the degree of Master of Arts in Political Science and International Relations at NAZARBAYEV UNIVERSITY SCHOOL OF SCIENCE AND HUMANITIES 2021 © 2021 Vlad Lim All Rights Reserved CAUSES OF ETHNIC CLASHES IN KAZAKHSTAN ПРИЧИНЫ ЭТНИЧЕСКИХ КОНФЛИКТОВ В КАЗАХСТАНЕ ҚАЗАҚСТАНДАҒЫ ЭТНИКАЛЫҚ ҚАҚТЫҒЫСТАРДЫҢ СЕБЕПТЕРІ by Vlad Lim Principal adviser: Dr. Hélène Thibault Second reader: Dr. Karol Czuba External reviewer: Dr. Barbara Junisbai iii Abstract In this research, I analyze the causes of violent confrontations that have taken place in Kazakhstan since independence. In particular, I close an important gap in the literature: most works have focused on certain aspects of ethnic problems in the country, such as language, migration, and Kazakhization, while the causes of violent clashes themselves have been understudied. Thus, my research demonstrates the roots of grievances that lead to mobilization of the titular ethnic group along ethnic lines. I studied the conducive role of Kazakhization on the perception of ethnic superiority among Kazakhs, demonstrating how the government promotes Kazakhness among population. Kazakhization has played an important role contributing to the level of grievances among ethnic Kazakhs. -

Annual Report Contents

2019 annual report Contents: 1. GLOSSARY 3 2. AT A GLANCE 5 3. BUSINESS MODEL 8 4. CHAIRMAN OF THE BOARD’S STATEMENT 10 5. CHAIRPERSON OF THE MANAGEMENT BOARD’S REVIEW 14 6. BOARD OF DIRECTORS 18 7. MANAGEMENT BOARD 23 8. KEY EVENTS 29 9. AWARDS 32 10. MACROECONOMIC AND BANKING REVIEW 34 11. FINANCIAL REVIEW 38 12. BUSINESS REVIEW 42 13. RISK MANAGEMENT 51 14. CORPORATE GOVERNANCE 58 15. SOCIAL REPORT 67 16. RESPONSIBILITY STATEMENT 75 17. OUTLOOK 77 18. AUDITED CONSOLIDATED FINANCIAL STATEMENTS FOR 2019 79 (iNCLUDING INDEPENDENT AUDITORS’ REPORT), NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS FOR 2019 19. INFORMATION FOR SHAREHOLDERS 174 HALYK BANK ANNUAL REPORT 2019 1 glossary 4 Glossary Glossary 1 Altyn Bank Altyn Bank JSC (SB of China Citic Bank Corporation Ltd) 2 AML/CTF Anti-Money Laundering and Countering Financing of Terrorism 3 BCC Branch credit committee 4 BNCC Branch network credit committee 5 Business Roadmap – 2020 The “Road Map for Business 2020” Unified Programme for Supporting Entrepreneurship and Business Development 6 CITIC Bank China CITIC Bank Corporation Limited 7 GDR Global Depositary Receipt 8 Halyk Bank, the Bank Halyk Bank of Kazakhstan 9 Halyk Group, the Group Halyk Bank Group of Companies 10 IS Information security 11 IT Information technology 12 KASE Kazakhstan Stock Exchange 13 KKB Kazkommertsbank 14 Retail Credit Committee Retail Credit Committee of the Head Bank 15 RK Republic of Kazakhstan 16 SCC Small credit committee of the regional branch 17 SME Small and medium enterprises 18 SPV Special purpose vehicle