Glencore-Prospectus.Pdf

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

We Want to Help the World Reach Net Zero and Improve People's Lives

BP Sustainability Report 2019 Our purpose is reimagining energy for people and our planet. We want to help the world reach net zero and improve people’s lives. We will aim to dramatically reduce carbon in our operations and production and grow new low carbon businesses, products and services. We will advocate for fundamental and rapid progress towards Paris and strive to be a leader in transparency. We know we don’t have all the answers and will listen to and work with others. We want to be an energy company with purpose; one that is trusted by society, valued by shareholders and motivating for everyone who works at BP. We believe we have the experience and expertise, the relationships and the reach, the skill and the will, to do this. Introduction Message from Bernard Looney 2 Our ambition 4 2019 at a glance Energy in context 8 Sustainability at BP UN Sustainable Development Goals 11 Sustainability at BP 11 Key sustainability issues 14 Our focus areas Climate change and the energy transition 16 Our role in the energy transition 18 Our ‘reduce, improve, create’ framework 20 Accrediting our lower carbon activities 22 Reducing emissions in our operations 23 Improving our products 26 Creating low carbon businesses 30 Safety 36 Process safety 38 Personal safety 39 Safety performance 41 Our value to society 42 Creating social value 44 Social investment 45 Local workers and suppliers 46 Human rights 47 Community engagement 48 Our impact on communities 49 Labour rights 50 Doing business responsibly Environment 54 People 60 Business ethics 68 Navigating our reports Governance Our quick read Human rights governance 74 provides a summary of the Executive oversight of sustainability 74 Sustainability Report, including key Managing risks 75 highlights and performance in 2019. -

FTSE Factsheet

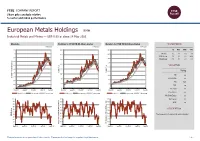

FTSE COMPANY REPORT Share price analysis relative to sector and index performance European Metals Holdings EMH Industrial Metals and Mining — GBP 0.69 at close 14 May 2021 Absolute Relative to FTSE UK All-Share Sector Relative to FTSE UK All-Share Index PERFORMANCE 14-May-2021 14-May-2021 14-May-2021 1.1 450 900 1D WTD MTD YTD 1 Absolute 0.0 -6.8 -4.2 7.8 400 800 Rel.Sector 1.2 -2.9 -7.5 -20.3 0.9 700 Rel.Market -1.1 -5.5 -4.8 -1.3 350 0.8 600 300 0.7 VALUATION 500 0.6 250 400 Trailing Relative Price Relative 0.5 Price Relative 200 300 PE -ve 0.4 Absolute Price (local currency) (local Price Absolute 150 EV/EBITDA -ve 200 0.3 PB 12.3 100 0.2 100 PCF -ve 0.1 50 0 Div Yield 0.0 May-2020 Aug-2020 Nov-2020 Feb-2021 May-2021 May-2020 Aug-2020 Nov-2020 Feb-2021 May-2021 May-2020 Aug-2020 Nov-2020 Feb-2021 May-2021 Price/Sales +ve Absolute Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Net Debt/Equity 0.0 100 90 90 Div Payout 0.0 90 80 80 ROE -ve 80 70 70 70 Index) Share Share Sector) Share - - 60 60 60 DESCRIPTION 50 50 50 40 40 40 The Company is focusing in tin mining industry. -

OIL COUNCIL Exploration Director, WORLD ASSEMBLY Tullow Oil

Oil & Gas Company Executives Register Today for only £1,995! Special Industry Delegation Discounts Also Available! 70 renowed speakers including: Angus McCoss OIL COUNCIL Exploration Director, WORLD ASSEMBLY Tullow Oil The World’s Premier Meeting Ashley Heppenstall President and CEO, Point for Energy, Finance Lundin Petroleum and Investment Charles ‘Chuck’ Davidson Chairman and CEO, Noble Energy John Knight EVP, Global Strategy and Business Development, Statoil Dr Mike Watts Deputy CEO, 26 – 27 November 2012 Cairn Energy Old Billingsgate, London, UK Ian Henderson Senior Advisor, J.P Morgan Asset Management • Europe’s largest O&G business meeting with 1,200 senior executives • Global participation from international O&G companies, investors and financiers • Delegations attending from NOCs, IOCs, small-cap, mid-cap and large cap independents • Direct access to energy focussed debt providers, equity capital, private equity Ian Taylor and strategic investors President and CEO, • Focuses on E&P funding, corporate development strategies, joint ventures, Vitol Group deepwater, the future of the North Sea and NCS, the new MENA landscape and the new regulatory environment Julian Metherell Lead Partners: CFO, Genel Energy Ronald Pantin CEO, Pacific Rubiales Partners: PR OG RE SS IV E Toronto Stock TSX Venture Toronto Stock TSX Venture Toronto Stock TSX Venture Exchange Exchange Exchange Exchange Exchange Exchange Bourse de Bourse de Bourse de Bourse de Bourse de Bourse de www.oilcouncil.com/event/wecaToronto Croissance TSX Toronto Croissance TSX -

Boards Fall Behind in the Drive to Appoint Women Alex Spence: the Times February 6 2012

Boards fall behind in the drive to appoint women Alex Spence: The Times February 6 2012 Britain's biggest companies will miss a deadline to have a quarter of their boardroom positions filled by women unless more is done to move talented female executives up the corporate ladder, recruiters have warned. As things stand, the target of having 25 per cent of FTSE 100 directorships held by women will be met two years late, in 2017, the search firm Norman Broadbent said. Although the female composition of FTSE 100 boards has risen from 13.6 per cent at the start of last year to almost 15 per cent, the supply of women executives and senior managers remained limited, it said. According to Neil Holmes, a consultant at Norman Broadbent: "Women are appearing on short-lists but the supply on the executive side is still lower than it should be and this requires companies to invest in long-term cultural changes." In a report last year, Lord Davies of Abersoch challenged corporate leaders to cast the net wider in the search for directors and to break their dominance of their boardrooms. Twenty-six per cent of the non-executive directors appointed to FTSE 100 boards last year were women, with 24 per cent in the FTSE 250 and 17 per cent in smaller listed companies. Women still lagged well behind their male counterparts in the top executive jobs at the biggest companies, accounting for 9 per cent of FTSE 100 executive positions last year, Norman Broadbent said. There was also a vast disparity between different industries, with women making up 17 per cent of boards in the health sector at the end of the year. -

Annex 1: Parker Review Survey Results As at 2 November 2020

Annex 1: Parker Review survey results as at 2 November 2020 The data included in this table is a representation of the survey results as at 2 November 2020, which were self-declared by the FTSE 100 companies. As at March 2021, a further seven FTSE 100 companies have appointed directors from a minority ethnic group, effective in the early months of this year. These companies have been identified through an * in the table below. 3 3 4 4 2 2 Company Company 1 1 (source: BoardEx) Met Not Met Did Not Submit Data Respond Not Did Met Not Met Did Not Submit Data Respond Not Did 1 Admiral Group PLC a 27 Hargreaves Lansdown PLC a 2 Anglo American PLC a 28 Hikma Pharmaceuticals PLC a 3 Antofagasta PLC a 29 HSBC Holdings PLC a InterContinental Hotels 30 a 4 AstraZeneca PLC a Group PLC 5 Avast PLC a 31 Intermediate Capital Group PLC a 6 Aveva PLC a 32 Intertek Group PLC a 7 B&M European Value Retail S.A. a 33 J Sainsbury PLC a 8 Barclays PLC a 34 Johnson Matthey PLC a 9 Barratt Developments PLC a 35 Kingfisher PLC a 10 Berkeley Group Holdings PLC a 36 Legal & General Group PLC a 11 BHP Group PLC a 37 Lloyds Banking Group PLC a 12 BP PLC a 38 Melrose Industries PLC a 13 British American Tobacco PLC a 39 Mondi PLC a 14 British Land Company PLC a 40 National Grid PLC a 15 BT Group PLC a 41 NatWest Group PLC a 16 Bunzl PLC a 42 Ocado Group PLC a 17 Burberry Group PLC a 43 Pearson PLC a 18 Coca-Cola HBC AG a 44 Pennon Group PLC a 19 Compass Group PLC a 45 Phoenix Group Holdings PLC a 20 Diageo PLC a 46 Polymetal International PLC a 21 Experian PLC a 47 -

Ftse4good UK 50

2 FTSE Russell Publications 19 August 2021 FTSE4Good UK 50 Indicative Index Weight Data as at Closing on 30 June 2021 Index weight Index weight Index weight Constituent Country Constituent Country Constituent Country (%) (%) (%) 3i Group 0.81 UNITED GlaxoSmithKline 5.08 UNITED Rentokil Initial 0.67 UNITED KINGDOM KINGDOM KINGDOM Anglo American 2.56 UNITED Halma 0.74 UNITED Rio Tinto 4.68 UNITED KINGDOM KINGDOM KINGDOM Antofagasta 0.36 UNITED HSBC Hldgs 6.17 UNITED Royal Dutch Shell A 4.3 UNITED KINGDOM KINGDOM KINGDOM Associated British Foods 0.56 UNITED InterContinental Hotels Group 0.64 UNITED Royal Dutch Shell B 3.75 UNITED KINGDOM KINGDOM KINGDOM AstraZeneca 8.25 UNITED International Consolidated Airlines 0.47 UNITED Schroders 0.28 UNITED KINGDOM Group KINGDOM KINGDOM Aviva 1.15 UNITED Intertek Group 0.65 UNITED Segro 0.95 UNITED KINGDOM KINGDOM KINGDOM Barclays 2.1 UNITED Legal & General Group 1.1 UNITED Smith & Nephew 0.99 UNITED KINGDOM KINGDOM KINGDOM BHP Group Plc 3.2 UNITED Lloyds Banking Group 2.39 UNITED Smurfit Kappa Group 0.74 UNITED KINGDOM KINGDOM KINGDOM BT Group 1.23 UNITED London Stock Exchange Group 2.09 UNITED Spirax-Sarco Engineering 0.72 UNITED KINGDOM KINGDOM KINGDOM Burberry Group 0.6 UNITED Mondi 0.67 UNITED SSE 1.13 UNITED KINGDOM KINGDOM KINGDOM Coca-Cola HBC AG 0.37 UNITED National Grid 2.37 UNITED Standard Chartered 0.85 UNITED KINGDOM KINGDOM KINGDOM Compass Group 1.96 UNITED Natwest Group 0.77 UNITED Tesco 1.23 UNITED KINGDOM KINGDOM KINGDOM CRH 2.08 UNITED Next 0.72 UNITED Unilever 7.99 UNITED KINGDOM KINGDOM -

Participating Organizations

PARTICIPATING ORGANIZATIONS Company Name Company Name Company Name Company Name Company Name ABB City and County of Denver Hewlett Packard Enterprise Nextworld Shell ABS Cobham Semiconductor Solutions Hitachi Consulting NLMK Shimmick Construction Advanced Micro Devices Coeur Mining Holland & Hart LLP Noble Energy Sierra Nevada Corporation AECOM CollegeDrive Test Prep and Tutoring HollyFrontier Northrop Grumman Corporation SM Energy Aera Energy LLC Collimare LLC HomeAdvisor Northwestern Mutual Solar Turbines, Inc Colorado Department of Transporta- Alarm.com Hunting Titan Nucor Steel Southwestern Energy tion Alight, Inc. Colorado Law Illinois Institute of Technology Oasis Petroleum Spectranetics Allegion Colorado Lighting, Inc IM Flash Occidental Petroleum Corporation Stanley Consultants, Inc. AMERICAN Cast Iron Pipe Company CO School of Mines Graduate Studies IMERYS Olin Corporation Statoil Ames Construction Computronix, Inc. IMI Precision Engineering Olsson Associates Stillwater Mining Company Anadarko Petroleum Corporation Condon - Johnson & Associates, Inc. Intelligent Software Solutions OppenheimerFunds Summit Materials Andeavor Connexta J.R. Butler, Inc. ORAU - Maryland Office SUNDT Apache Corp. ConocoPhillips Jacobs Orbital ATK TEAM-UP: Teacher Education Alliance Apex Engineers, Inc. Covenant Testing Technologies, LLC. Johns Manville Orica Tenaris Applied Control Equipment, LLLP Credera Jviation, Inc. OSIsoft Texas Instruments Arcadis, Inc. CTL Thompson, Inc. Kahuna Ventures LLC Parsons The RMH Group Inc. ArcelorMittal Daily Thermetrics Kansas Department of Transportation Pathfinder Systems Inc The Trade Desk Arch Coal, Inc. Dal-Tile Corp. Keane Group PDC Energy The Vertex Companies, Inc. ARCO/Murray National Construction Davidson Technologies Inc. Kenzan Peabody Energy Tierra Group International, Ltd. Arista Networks DENSO International America, Inc. Kiewit Peace Corps TimkenSteel Corporation APS- Palo Verde Generating Station DPS - Denver Teacher Residency Kimley-Horn Pearl Harbor Naval Shipyard Traylor Bros., Inc. -

Constituents & Weights

2 FTSE Russell Publications 19 August 2021 FTSE 100 Indicative Index Weight Data as at Closing on 30 June 2021 Index weight Index weight Index weight Constituent Country Constituent Country Constituent Country (%) (%) (%) 3i Group 0.59 UNITED GlaxoSmithKline 3.7 UNITED RELX 1.88 UNITED KINGDOM KINGDOM KINGDOM Admiral Group 0.35 UNITED Glencore 1.97 UNITED Rentokil Initial 0.49 UNITED KINGDOM KINGDOM KINGDOM Anglo American 1.86 UNITED Halma 0.54 UNITED Rightmove 0.29 UNITED KINGDOM KINGDOM KINGDOM Antofagasta 0.26 UNITED Hargreaves Lansdown 0.32 UNITED Rio Tinto 3.41 UNITED KINGDOM KINGDOM KINGDOM Ashtead Group 1.26 UNITED Hikma Pharmaceuticals 0.22 UNITED Rolls-Royce Holdings 0.39 UNITED KINGDOM KINGDOM KINGDOM Associated British Foods 0.41 UNITED HSBC Hldgs 4.5 UNITED Royal Dutch Shell A 3.13 UNITED KINGDOM KINGDOM KINGDOM AstraZeneca 6.02 UNITED Imperial Brands 0.77 UNITED Royal Dutch Shell B 2.74 UNITED KINGDOM KINGDOM KINGDOM Auto Trader Group 0.32 UNITED Informa 0.4 UNITED Royal Mail 0.28 UNITED KINGDOM KINGDOM KINGDOM Avast 0.14 UNITED InterContinental Hotels Group 0.46 UNITED Sage Group 0.39 UNITED KINGDOM KINGDOM KINGDOM Aveva Group 0.23 UNITED Intermediate Capital Group 0.31 UNITED Sainsbury (J) 0.24 UNITED KINGDOM KINGDOM KINGDOM Aviva 0.84 UNITED International Consolidated Airlines 0.34 UNITED Schroders 0.21 UNITED KINGDOM Group KINGDOM KINGDOM B&M European Value Retail 0.27 UNITED Intertek Group 0.47 UNITED Scottish Mortgage Inv Tst 1 UNITED KINGDOM KINGDOM KINGDOM BAE Systems 0.89 UNITED ITV 0.25 UNITED Segro 0.69 UNITED KINGDOM -

Nayara Energy Annual Report 2016-17

Essar Oil Limited Annual Report 2016-17 Essar Oil Limited Contents Corporate Overview Reports Financial Statement Scaling New Heights 01 Directors’ Report 11 Standalone The World of Essar Oil 02 Independent Auditor’s Report 44 Snapshot of FY 2016-17 04 Balance Sheet 50 Message from the Former Chairman 06 Statement of Profit and Loss 51 Message from the Former Managing Cash Flow Statement 52 Director & CEO 08 Notes 55 Corporate Information 10 Consolidated Independent Auditor’s Report 123 Balance Sheet 128 Statement of Profit and Loss 129 Cash Flow Statement 130 Notes 133 Form AOC-1 206 Notice AGM Notice 208 2 Annual Report 2016-17 | Scaling New Heights Corporate Overview Reports Financial Statements Scaling New Heights Crude and product storage facility at the Refinery Keeping up with its tradition of setting new records, Essar Oil Given the Company’s commitment to superior performance, continued its streak of stellar performance for yet another year we have been regularly investing in the process and technology in FY 2016-17. The Company clocked its highest-ever crude improvement. Through a slew of proactive strategies, we have throughput of 20.94 MMT in FY 2016-17, while production of been able to achieve three-fold increase in sales of petcoke to HSD and MS also stood at its best 10,053 kT and 3,498 kT, small-scale customers. As a result of these efforts, our petcoke respectively. Essar Oil’s crude receipt through SPM also hit its sales grew by 11% in FY 2016-17 while sulphur sales grew by peak at 18.8 MMT for the first time in the Company’s history. -

1 Modelling Oil and Gas Stock Returns Using Multi Factor Asset Pricing

Modelling oil and gas stock returns using multi factor asset pricing model including oil price exposure Abstract Oil and gas is one of the most important sectors in every economy and the valuation of oil and gas companies becomes quite challenging due to the volatility of crude oil price. The paper investigates the determinants of the UK oil and gas stock returns using multi factor asset pricing model and the existence of asymmetric effects in the Brent crude oil price. Our results show that market risk, oil price risk, size and book-to-market related factors are all relevant in the determination of asset returns of the oil and gas companies quoted on the London stock exchange. Oil price increases and decreases decomposed separately have more effect on the oil companies’ stock returns than the normal log changes of the price which shows the presence of asymmetric effect. However, the oil price shocks in general do not seem to strongly affect stock returns in oil and gas sector possibly due to horizontal and vertical integration of bigger companies in the sector. Keywords: asset pricing models, Brent crude oil, asymmetry in oil price, size effect, book to market ratio, oil and gas sector, oil price exposure, structural breaks. JEL Classification Codes: G12 1 1. Introduction One of the biggest challenges in the field of finance is how to effectively model the risk and return of financial securities. Researchers have formulated various asset pricing models that tend to explain the determinants of asset returns. Markowitz’s (1952) mean-variance analysis provides the foundations of portfolio optimisation. -

General Presentation

Glencore CEO – Ivan Glasenberg Miami, 15th May, 2012 Why invest in Glencore? 1. Unique market position in global commodities 2. Strong track record of value creation driven by capital discipline and a focus on returns 3. Management are owners not renters of assets 4. Strong pipeline of high quality production growth with low capital cost 5. Marketing operations are scale-able at low incremental capital cost 6. Robust balance sheet 7. Xstrata merger and Viterra acquisition create unique natural resources group Glencore - a uniquely compelling way for investors to benefit from commodity demand growth I 2 What does Glencore do? . Position throughout the value chain allows Glencore to capture value at each stage . Producers typically solely focused on sale of own products while other marketing peers do not have Glencore’s scale and access to own supply Upstream Marketing, Processing / Marketing, production Storage and freight refining Storage and freight Zinc / copper / lead Alumina / aluminium Ferroalloys / Metals and Minerals nickel / cobalt / iron ore Oil Coal / coke n/a n/a Energy Products Energy Agricultural products Agri. Agri. Products Key: I 3 Significant presence Lesser presence How is Glencore’s business model unique? Scale Strong competitive positions in core activities Unique breadth of local presence with critical mass: more than 50 offices in more than 40 countries Largest global user of letters of credit 98 active banking relationships Diversification 54 geographies 18 major commodity groups Vertical integration Production to delivery to customer No single competitor in all markets Human capital Culture and high retention rates Long-term customer/supplier relationships 7 000 customer and supplier relationships Supplier relationships provide unique access to compelling asset deals I 4 Strong track record of value creation… 1974 1987 / 1988 . -

Entrepreneurialism Fully Priced Target Price HKD 70.40 Starts At70.40 Closing Price HKD 67.40 May 30, 2011 Potential Upside +4.5%

Glencore 0805.HK 805 HK BASIC MATERIALS EQUITY RESEARCH May 31, 2011 Initiating at NEUTRAL with TP of HKD70.40 Rating Starts at Neutral Entrepreneurialism fully priced Target price HKD 70.40 Starts at70.40 Closing price HKD 67.40 May 30, 2011 Potential upside +4.5% Action/Valuation: Expensive relative to mining peers; NEUTRAL Anchor themes Glencore is evolving from a trading house whose mining assets principally We expect the mining sector to served to feed its marketing business into one whose mining assets outperform in 2011, with become the key driver of group earnings. Although we find Glencore's thermal coal being our management to be the most entrepreneurial team in the sector, we think preferred commodity pick. valuations are expensive relative to mining peers. Our HKD70.40 TP represents a 10% holding company discount to our SOTP NPV valuation. Nomura vs consensus Coverage on the street is Mining assets: higher volume growth, but with higher risk and costs currently sparse. Excluding Xstrata, we estimate an attributable copper equivalent CAGR for Glencore of 7.5% over 2011-2015E (vs an average of 5.2% for the Research analysts diversified miners). Glencore’s high growth is partly offset by higher geographical risk and a higher cost profile, with average costs mostly in Singapore Basic Materials the third quartile of industry cost curves. Tanuj Shori - NSL [email protected] A high-quality and counter-cyclical marketing business +65 6433 6981 Glencore’s marketing business has dominant market shares, high barriers to entry and counter-cyclical cash generation, and we believe it should European Metals & Mining trade in line with or at a small discount to Noble (because of Noble’s Paul Cliff - NI plc [email protected] greater exposure to agriculture, which tends to be less cyclical, and its +44 20 7102 4349 faster earnings growth, offset to some extent by Glencore’s higher RoCE).