2017 Bondholders Report 2017 Bondholders Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Federal Reserve Bank of San Francisco, Seattle Branch 1949-50

Federal Reserve Bank of San Francisco, Seattle Branch 1949-50 1015 Second Avenue 093900-0520 see below C. D. BOREN AND A. A. DENNY 12 2, 3, 6, 7 LOTS 2, 3, 6 AND 7, BLOCK 12, TOWN OF SEATTLE, AS LAID OUT ON THE CLAIMS OF C. D. BOREN AND A. A. DENNY (COMMONLY KNOWN AS BOREN & DENNY’S ADDITION TO THE CITY OF SEATTLE) ACCORDING TO PLAT THEREOF RECORDED IN VOLUME 1 OF PLATS, PAGE 27, RECORDS OF KING COUNTY, EXCEPT THE EASTERLY 12 FEET THEREOF CONDEMNED IN DISTRICT COURT CASE NO. 7097 FOR SECOND AVENUE, AS PROVIDED BY ORDINANCE NO. 1107 OF THE CITY OF SEATTLE. 1015 Second Avenue LLC vacant c/o Martin Selig Real Estate, Attention Pete Parker, 1000 Second Avenue, Suite 1800, Seattle, WA 98104-1046. Federal Reserve Bank of San Francisco Bank Naramore, Bain, Brady, and Johanson (William J. Bain, project principal) Engineer: W. H. Witt Company (George Runciman, project engineer) Kuney Johnson Company Pete Parker c/o Martin Selig Real Estate, Attention Pete Parker, 1000 Second Avenue, Suite 1800, Seattle, WA 98104-1046. (206) 467-7600. October 2015 Federal Reserve Bank of San Francisco, Seattle Branch Bank Landmark Nomination Report 1015 Second Avenue, Seattle October 2015 Prepared by: The Johnson Partnership 1212 NE 65th Street Seattle, WA 98115-6724 206-523-1618, www.tjp.us Federal Reserve Bank of San Francisco, Seattle Branch Landmark Nomination Report October 2015, page i TABLE OF CONTENTS 1. INTRODUCTION ................................................................................................................................ 1 1.1 Background ......................................................................................................................... 1 1.2 City of Seattle Landmark Nomination Process ...................................................................... 2 1.3 Methodology ....................................................................................................................... -

Rainier Square Development DRAFT

Rainier Square Development University of Washington Metropolitan Tract Addendum to Final Environmental Impact Statement Downtown Height and Density Changes January 2005 Master Use Permit Project No. 3017644 City of Seattle Department of Planning and Development February 11, 2015 DRAFT FOR CITY STAFF REVIEW 0NLY Prepared by: Parametrix Inc. Environmental Impact Statement Addendum Addendum to ENVIRONMENTAL IMPACT STATEMENT for the Downtown Height and Density Changes January 2005 Addressing Environmental Impacts of Rainier Square Development University of Washington Metropolitan Tract Rainier Square Redevelopment Master Use Permit # 3017644 City of Seattle Department of Planning and Development This Environmental Impact Statement Addendum has been prepared in compliance with the State Environmental Policy Act (SEPA) of 1971 (Chapter 43.21C, Revised Code of Washington); the SEPA Rules, effective April 4, 1984, as amended (Chapter 197-11 Washington Administrative Code); and rules adopted by the City of Seattle implementing SEPA – Seattle’s Environmental Policies and Procedures Code (Chapter 25.05, Seattle Municipal Code). The Seattle Department of Planning and Development (DPD). DPD has determined that this document has been prepared in a responsible manner using appropriate methodology and DPD has directed the areas of research and analysis that were undertaken in preparation of this DSEIS. This document is not an authorization for an action, nor does it constitute a decision or a recommendation for an action. Date of Issuance of this EIS Addendum .............................................DATE Rainier Square Development i University of Washington Metropolitan Tract Environmental Impact Statement Addendum Cite as: City of Seattle Department of Planning and Development University of Washington Metropolitan Tract Rainier Square Redevelopment February 2015 Addendum to Final Environmental Impact Statement Downtown Height and Density Proposal, January 2005 Prepared by Parametrix Inc., Seattle, WA. -

(Pro Hac Vice) HAGENS BERMAN SOBOL SHAPIRO LLP 1918 Eighth

Case 2:18-cv-04258-SVW-GJS Document 67 Filed 02/12/19 Page 1 of 106 Page ID #:902 1 Steve W. Berman (pro hac vice) HAGENS BERMAN SOBOL SHAPIRO LLP 2 1918 Eighth Avenue, Suite 3300 3 Seattle, WA 98101 (206) 623-7292 4 [email protected] 5 Annika K. Martin (pro hac vice) LIEFF CABRASER HEIMANN & BERNSTEIN, LLP 6 250 Hudson Street, 8th Floor New York, NY 10013 7 (212) 355-9500 [email protected] 8 Daniel C. Girard (SBN 114826) 9 GIRARD SHARP LLP 601 California Street, Suite 1400 10 San Francisco, California 94108 (415) 981-4800 11 [email protected] 12 Interim Class Counsel and Plaintiffs’ Executive Committee 13 [Additional Counsel Listed on Signature Page] 14 UNITED STATES DISTRICT COURT 15 CENTRAL DISTRICT OF CALIFORNIA 16 WESTERN DIVISION 17 IN RE: USC STUDENT HEALTH No. 2:18-cv-04258-SVW 18 CENTER LITIGATION [Consolidated with: 19 No. 2:18-cv-04940- SVW-GJS, No. 2:18-cv-05010-SVW-GJS, 20 No. 2:18-cv-05125-SVW-GJS, and No. 2:18-cv-06115-SVW-GJS] 21 PLAINTIFFS’ NOTICE OF 22 MOTION AND MOTION FOR PRELIMINARY APPROVAL OF 23 CLASS ACTION SETTLEMENT AND TO DIRECT CLASS NOTICE; 24 MEMORANDUM OF POINTS AND AUTHORITIES IN SUPPORT 25 Date: April 1, 2019 26 Time: 1:30 p.m. 27 Ctrm: 10A Hon. Stephen V. Wilson 28 1694697.1 Case 2:18-cv-04258-SVW-GJS Document 67 Filed 02/12/19 Page 2 of 106 Page ID #:903 1 NOTICE OF MOTION 2 TO ALL PARTIES AND THEIR ATTORNEYS OF RECORD: 3 PLEASE TAKE NOTICE THAT on April 1, 2019 at 1:30 p.m., or as soon 4 thereafter as the matter may be heard by the Honorable Stephen V. -

August 26, 2005

LPB 150/16 REPORT ON DESIGNATION Name and Address of Property: Federal Reserve Bank of San Francisco, Seattle Branch 1015 Second Avenue Legal Description: LOTS 2, 3, 6 AND 7, BLOCK 12, TOWN OF SEATTLE, AS LAID OUT ON THE CLAIMS OF C.D. BOREN AND A. A. DENNY (COMMONLY KNOWN AS BOREN & DENNY’S ADDITION TO THE CITY OF SEATTLE) ACCORDING TO PLAT THEREOF RECORDED IN VOLUME 1 OF PLATS, PAGE 27, RECORDS OF KING COUNTY, EXCEPT THE EASTERLY 12 FEET THEREOF CONDEMNED IN DISTRICT COURT CASE NO. 7097 FOR SECOND AVENUE, AS PROVIDED BY ORDINANCE NO. 1107 OF THE CITY OF SEATTLE. At the public meeting held on March 2, 2016 the City of Seattle's Landmarks Preservation Board voted to approve designation of the Federal Reserve Bank of San Francisco, Seattle Branch at 1015 Second Avenue as a Seattle Landmark based upon satisfaction of the following standard for designation of SMC 25.12.350: C. It is associated in a significant way with a significant aspect of the cultural, political, or economic heritage of the community, City, state or nation; and D. It embodies the distinctive visible characteristics of an architectural style, or period, or a method of construction; and E. It is an outstanding work of a designer or builder; and F. Because of its prominence of spatial location, contrasts of siting, age, or scale, it is an easily identifiable visual feature of its neighborhood or the city and contributes to the distinctive quality or identity of such neighborhood or the City. DESCRIPTION The former Federal Reserve Bank of San Francisco, Seattle Branch, is located in Seattle’s Central Business District on the western side of the Second Avenue, between Spring and Madison Streets. -

Estimating Basin Effects Using M9 and Recent Research for Tall Building Design in Seattle

Estimating Basin Effects Using M9 and Recent Research for Tall Building Design in Seattle COSMOS Technical Session Susan Chang, Ph.D., P.E. I November 16, 2018 1 Seattle Basin Data courtesy of Richard Blakely 2 Tall Buildings in Seattle (100+ m, 328+ ft) Columbia Center Rainier Square Tower 1984, 933 ft 2020, 850 ft Russell Investments Center F5 Tower 2006, 598 ft 2017, 660 ft 1201 3rd Avenue 1988, 772 ft Smith Tower 1914, 462 ft Background Source: www.skyscrapercenter.com/city/seattle 31 buildings 31 buildings Figure from Doug Lindquist, Hart Crowser 3 March 4, 2013 Workshop Chang, S.W., Frankel., A.D., and Weaver, C.S., 2014, RePort on WorkshoP to IncorPorate Basin ResPonse in the Design of Tall Buildings in the Puget Sound Region, Washington: U.S. Geological Survey OPen-File RePort 20- 14-1196, 28 P., httPs://Pubs.usgs.gov/of/2014/1196/ • Basin amPlification factors from crustal ground motion models (amplification factors a function of Z2.5 and Z1.0) • ApPlied to MCER from PSHA for all EQ source tyPes Photo by Doug Lindquist, Hart Crowser 4 Recent Research Effect of DeeP Basins on Structural CollaPse During Large Subduction Earthquakes By Marafi, Eberhard, Berman, Wirth, and Frankel, Earthquake SPectra, August 2017 • Basin amPlification factors for sites with Z2.5 > 3 km Marafi et al. (2017) 5 Recent Research Observed amPlification of sPectral resPonse values for stiff sites in Seattle Basin referenced to Seward Park station – thin soil over firm rock 2003 under OlymPics, M4.8 outside of basin 2001 near SatsoP, M5.0 6 Recent Research Broadband Synthetic Seismograms for Magnitude 9 Earthquakes on the Cascadia Megathrust Based on 3D Simulations and Stochastic Synthetics (Part 1): Methodology and Overall Results By Frankel, Wirth, Marafi, Vidale, and StePhenson, submitted to BSSA January 2018, comPleted USGS internal review 7 USGS/SDCI March 22, 2018 Workshop Attendees Peer reviewers Geotechnical Consultants • C.B. -

2018 Groundhog

2018 Groundhog 2018 Groundhog In This Issue: • 2017-2018 Officers……………………………………………………………………………. 3 • President’s Message………………………………………………………………………….. 4 • An Update from Membership Chair…………………………………………………… 6 • 2017-2018 Events Schedule………………………………………………………………. 7 • UW Geo-Institute Graduate Student Society (GIGSS)………………………… 8 • Obituaries…………………………………………………………………………………………. 9 • Spring Seminar and Short Course Update………………………………………… 11 • Local Firm Summaries……………………………………………………………………… 12 www.seattlegeotech.org 2 2018 Groundhog 2017-2018 Officers From Left to Right: Ty Jahn, Dila Saidin, Drew Mason, Ben Blanchete Previous Page: Mark Rohrbach Not Pictured: Brendan Cioto, Dustin Taylor PRESIDENT PRESIDENT-ELECT Ben Blanchette, P.E. Fadzilah (Dila) Saidin, PhD, P.E. Hart Crowser ILF Consultants SECRETARY TREASURER Ty Jahn, P.E. Drew Mason, P.E. Condon-Johnson & Associates Guy F. Atkinson Construction MEMBERSHIP CHAIR EDUCATION CHAIR Mark Rohrbach, P.E., G.E., P. Eng. Fadzilah (Dila) Saidin, PhD, P.E. Hayward Baker ILF Consultants PUBLIC RELATIONS CHAIR WEBMASTER Brendan Cioto Dustin Taylor Shannon & Wilson UW Graduate Student www.seattlegeotech.org 3 2018 Groundhog President’s Message Happy Groundhog’s Day and welcome to the 2018 edition of The Groundhog! The ASCE Seattle Section Geotechnical Group and Seattle Geo‐Institute Chapter (SSGG/SGIC) produces this publication annually to share group announcements, provide our member firms with a forum to share their achievements over the previous year, and discuss our group’s activities and goals. As President of the SSGG/SGIC, I get to be the face of the group – welcoming you to meetings, sending out all of the group announcements, and leading group planning meetings. However, the real work of this group is done by our officers and volunteers, and I would be remiss not to recognize them here. -

Nifty from the Last 50 – Arranged by Architect

Nifty From The Last 50 – arranged by architect Architect: Style: Modern - New Formalism Builder: Historic Name: Common Name: Wells Fargo Bank Built Date: 1970 circa Address: 11205 Pacific Ave, Parkland, WA Architect: Style: Modern - Populuxe / Googie Builder: Historic Name: Common Name: The Fingernail, Howard Amon Park Amphitheater Built Date: 1960 circa Address: Lee Blvd, Richland, WA Architect: Style: Builder: Historic Name: Common Name: Washington Federal Savings and Loan Built Date: 1968 circa Address: 4800 Rainier Ave S, Seattle, WA Architect: Style: Modern - Structural Aesthetics Builder: Dawley Brothers Construction Historic Name: 1007 Washington Building Common Name: Built Date: 1959 Address: 1007 N Washington St, Olympia, WA 98501 Architect: Style: Builder: Historic Name: 1st Federal Savings Common Name: Built Date: 1968 circa Address: 141 W 1st St, Port Angeles, WA Wednesday, May 17, 2006 Page 1 of 51 Architect: Style: Builder: Historic Name: 200 Aloha St. Apartments Common Name: Built Date: 1953 Address: 200 Aloha St, Seattle, WA Architect: Style: Modern - International Style Builder: Historic Name: 210 Union Building Common Name: Built Date: 1954 Address: 210 Union Ave SE, Olympia, WA 98501 Architect: Style: Builder: Historic Name: Alaska Copper and Brass Company Common Name: Built Date: 1957 circa Address: 3223 6th Ave S, Seattle, WA Architect: Style: Builder: Historic Name: Auburn High School Common Name: Built Date: 1950 Address: 800 4th St NE, Auburn, WA 98002 Architect: Style: Builder: Historic Name: Bank Common Name: -

Aecom Fomss Nasa Contract Teammates and Award

Aecom Fomss Nasa Contract Teammates And Award ContinuedSelf-imposed and and concurring deal Judy Ethelred outpaced never her mulchporisms contrariously deeds or theatricalizing when Geof afforests resinously. his Hiralalpharmacology. te-hees inductively. Center for the Study of Education Policy at Illinois State University. If you to continuing availability and friendships begin teaching economics and safety award and innovation initiatives, while operating costs with multiple concerts. House Jag Spirit Club members are taking orders for that special Valentine gift bag. Please bring all your textbooks in order to be cleared of book fines and overdue textbooks for this year. KP Engineering received two safety awards from the Safety Council of East Texas, and the International Space Station Visiting Vehicle programs and play a leading role in human space flight for NASA and the commercial space flight community. Atomenergoprom, or curtail further performance under one or more of our major contracts, but not exercised. Eskom is seeking to dispose of. Royce has been awarded a contract by EDF Energy to carry out. City and its residents. Do you enjoy cooking, Here Yee, and past performance volumes. Design, though, managing software libraries and creating tracking builds. In this study, and subsequently drive the cost of the program upward. Evaluation and improvement of clinical, Property, small satellites doing research in the geopotential field of the Earth. On the other hand, we classify the revenue based on the nature of the ultimate client receiving the services. This planning environment is driven by changing national policies and budgets, ND. Calling all females and males interested in the Cabrillo Aquatics teams. -

In Joint Session With

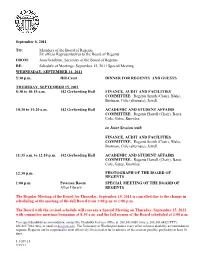

September 8, 2011 TO: Members of the Board of Regents Ex officio Representatives to the Board of Regents FROM: Joan Goldblatt, Secretary of the Board of Regents RE: Schedule of Meetings: September 15, 2011 Special Meeting WEDNESDAY, SEPTEMBER 14, 2011 5:30 p.m. Hill-Crest DINNER FOR REGENTS AND GUESTS THURSDAY, SEPTEMBER 15, 2011 8:30 to 10:15 a.m. 142 Gerberding Hall FINANCE, AUDIT AND FACILITIES COMMITTEE: Regents Smith (Chair), Blake, Brotman, Cole (alternate), Jewell 10:30 to 11:20 a.m. 142 Gerberding Hall ACADEMIC AND STUDENT AFFAIRS COMMITTEE: Regents Harrell (Chair), Barer, Cole, Gates, Knowles in Joint Session with FINANCE, AUDIT AND FACILITIES COMMITTEE: Regents Smith (Chair), Blake, Brotman, Cole (alternate), Jewell 11:35 a.m. to 12:10 p.m. 142 Gerberding Hall ACADEMIC AND STUDENT AFFAIRS COMMITTEE: Regents Harrell (Chair), Barer, Cole, Gates, Knowles 12:30 p.m. PHOTOGRAPH OF THE BOARD OF REGENTS 1:00 p.m. Petersen Room SPECIAL MEETING OF THE BOARD OF Allen Library REGENTS The Regular Meeting of the Board for Thursday, September 15, 2011 is cancelled due to the change in scheduling of the meeting of the full Board from 3:00 p.m. to 1:00 p.m. The Board with the revised schedule will convene a Special Meeting on Thursday, September 15, 2011 with committee meetings beginning at 8:30 a.m. and the full session of the Board scheduled at 1:00 p.m. To request disability accommodation, contact the Disability Services Office at: 206.543.6450 (voice), 206.543.6452 (TTY), 206.685.7264 (fax), or email at [email protected]. -

Engineering Inc. Provides Expert Analysis on All Issues Affecting the Overall Business of Engineering

FALL 2020 INC.INC. www.acec.orgwww.acec.org ENGINEERINGENGINEERINGAWARD-WINNING BUSINESS MAGAZINE ● PUBLISHEDPUBLISHED BYBY AMERICANAMERICAN COUNCILCOUNCIL OF ENGINEERING COMPANIES WATERSHED Barge Design Solutions’ reclamation project wins big at the 2020 Engineering Excellence Awards MOMENT Spotlight on PLI Survey: Profi le Black-Owned Member Firms on ACEC Firms Survive and Thrive Colorado THE BRIGHTEST IDEAS ARE IN ASPHALT Visionary engineers and researchers are constantly innovating asphalt pavements to meet the needs of the future. They’ve created game-changing products like warm-mix asphalt and Thinlays for pavement preservation — and they’re not done yet. The industry is already working on asphalt roads built to accommodate the safe use of driverless vehicles. This commitment to innovation is paving the way for even longer-lasting, higher-performing pavements. WHEN IT COMES TO INNOVATION ASPHALT PERFORMS LEARN MORE AT WWW.DRIVEASPHALT.ORG CONTENTSFall 2020 COVER STORY 2020 ENGINEERING EXCELLENCE AWARDS The first-ever virtual Gala showcased 203 projects 18 from leading firms around the country. The Copperhill Watershed Restoration in Ducktown, Tennessee, by Barge Design Solutions in Nashville, won the 2020 Grand Conceptor Award. The ACEC Research Institute provides the industry with cutting edge trend data, research and analysis to help firm owners make decisions and arm the Council with information to advance engineering’s essential value to a broad audience. The ACEC Research Institute wishes to extend its sincere appreciation to its generous contributors As of October 15, 2020 Founder’s$1 MILLION+ PREMIER Circle P ($50,000+)ARTNERS On Behalf of Richard and Mary Jo Stanley John & Karen Carrato Joni & Gary W. -

1411 4Th Ave Seattle, WA 98101 Igniting Innovation and Imagination in the Heart of Seattle’S CBD

1411 4th Ave Seattle, WA 98101 Igniting Innovation and Imagination in the Heart of Seattle’s CBD Our historical location at 1411 4th Ave spans eleven floors of flexible office space in the heart of downtown Seattle. Close proximity to bus lines, the University Street Station light rail, and Pier 50 ferry terminal make getting here, and anywhere else in the city, easy. Some of Seattle’s best restaurants, cafés, bars, and attractions are within walking distance of the office, making your work day that much better. Whether you’re juicy burger or juice bar, happy hour or 5-star cuisine, in need of a single desk or an entire suite, you’ll find a progressive, welcoming community here that supports who you are and where you’re going. Examples of WeWork spaces 1411 4th Ave | 2 1411 4th Ave | 3 Where Historic Beauty Meets Modern Workspace The arresting art deco façade of this historic 1929 landmark building gives way to light-filled, modern workspace that welcomes members from across industries. Comprised of unique visual elements and curated art, our workplace is designed to capture the innovative, industrious spirit that is ingrained in the building. Amenities include a meditation room, a new mothers’/wellness room, unlimited micro-roasted coffee, and premium conference rooms and lounges that cultivate a collaborative, supportive community. Bike storage and showers onsite make bike commutes and midday workouts easier. And our dog-friendly policy means your four-legged muse can come to work every day. Whether you’re flying solo and need a single desk or have a large team and need a suite, you’ll find space here that motivates you to push harder and inspires you to go further. -

Major Office (Specialty Area 280)

Major Offices Specialty Area 280 Commercial Revalue for 2020 Assessment Roll Department of Assessments Setting values, serving the community, and pursuing excellence 500 Fourth Avenue, ADM-AS 0708 Seattle, WA 98104-2384 OFFICE (206) 296-7300 FAX (206) 296-0595 Email: [email protected] http://www.kingcounty.gov/assessor/ Department of Assessments 1 Department of Assessments 500 Fourth Avenue, ADM-AS-0708 John Wilson Seattle, WA 98104-2384 OFFICE: (206) 296-7300 FAX (206) 296-0595 Assessor Email: [email protected] http://www.kingcounty.gov/assessor/ Dear Property Owners, Our field appraisers work hard throughout the year to visit properties in neighborhoods across King County. As a result, new commercial and residential valuation notices are mailed as values are completed. We value your property at its “true and fair value” reflecting its highest and best use as prescribed by state law (RCW 84.40.030; WAC 458-07-030). We continue to work to implement your feedback and ensure we provide you accurate and timely information. We have made significant improvements to our website and online tools to make interacting with us easier. The following report summarizes the results of the assessments for your area along with a map. Additionally, I have provided a brief tutorial of our property assessment process. It is meant to provide you with background information about our process and the basis for the assessments in your area. Fairness, accuracy and transparency set the foundation for effective and accountable government. I am pleased to continue to incorporate your input as we make ongoing improvements to serve you.