Regulatory Stress Tests and Bank Responses CAMA Working Paper

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Fitch Places 31 EMEA Bank ST Issuer Ratings Under Criteria Observation

5/7/2019 [ Press Release ] Fitch Places 31 EMEA Bank ST Issuer Ratings Under Criteria Observation Fitch Places 31 EMEA Bank ST Issuer Ratings Under Criteria Observation Fitch Ratings-London-07 May 2019: Fitch Ratings has placed 31 Short-Term (ST) Issuer Default Ratings (IDR) and related ST debt level ratings of EMEA-based banks Under Criteria Observation (UCO) following the publication of its cross-sector criteria for Short-Term Ratings on 2 May 2019. A full list of rating actions is below. Fitch intends to conclude full implementation of the criteria, and resolution of all UCO designations within six months of the designation. KEY RATING DRIVERS The ST ratings of the affected banks are determined primarily by correspondence tables linking short-term to long-term ratings. The new ST rating criteria introduced changes to our correspondence table between long-term and ST ratings. Two new cusp points at 'A' and 'BBB+' have been added to the existing three cusp points ('A+', 'A-' and 'BBB'), where baseline or higher ST ratings can be assigned. For banks with Long-Term IDRs driven by their standalone profile, as reflected by their Viability Ratings (VR), Fitch uses the funding and liquidity factor score as the principal determinant of whether the 'baseline' or 'higher' ST IDR is assigned at each cusp point. The ST IDRs and, where relevant, associated ST debt/deposit ratings of the following issuers have been placed UCO because the ratings could be upgraded by one notch under the new criteria. This is because the latest funding and liquidity scores that feed into their VRs are at least in line with the minimum levels required for a higher ST rating under the new criteria: - Banco Cooperativo Espanol, S.A. -

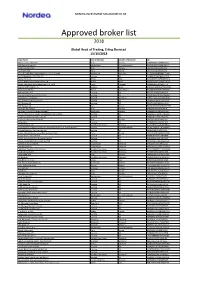

External Borkers List

NORDEA INVESTMENT MANAGEMENT AB Approved broker list 2018 Global Head of Trading, Erling Skorstad 15/10/2018 Legal Name City of Domicile Country of Domicile LEI ABG Sundal Collier ASA Oslo Norway 2138005DRCU66B8BNY04 ABN Amro Group NV Amsterdam The Netherlands BFXS5XCH7N0Y05NIXW11 Arctic Securities AS Oslo Norway 5967007LIEEXZX4RVS72 Aurel BGC SAS Paris France 5RJTDGZG4559ESIYLD31 Australia and New Zealand Banking Group Limited Melbourne Australia JHE42UYNWWTJB8YTTU19 AUTONOMOUS RESEARCH LLP London UK 213800LBM6PT85IGM996 Banca IMI S.p.A Milan Italy QV4Q8OGJ7OA6PA8SCM14 Banco Bilbao Vizcaya Argentaria S.A Bilbao Spain K8MS7FD7N5Z2WQ51AZ71 Banco Português de Investimento, S.A. (BPI) Porto Portugal 213800NGLJLXOSRPK774 BANCO SANTANDER S.A Madrid Spain 5493006QMFDDMYWIAM13 Bank Vontobel AG Zurich Switzerland 549300L7V4MGECYRM576 Barclays Bank PLC London UK G5GSEF7VJP5I7OUK5573 Barclays Capital Securities Limited London UK K9WDOH4D2PYBSLSOB484 Bayerische Landesbank Munich Germany VDYMYTQGZZ6DU0912C88 BCS Prime Brokerage Limited London UK 213800UU8AHE2B6QUI26 BGC Brokers LP London UK ZWNFQ48RUL8VJZ2AIC12 BNP Paribas SA Paris France R0MUWSFPU8MPRO8K5P83 Carnegie AS Norway Oslo Norway 5967007LIEEXZX57BC18 Carnegie Investment Bank AB (publ) Stockholm Sweden 529900BR5NZNQZEVQ417 China International Capital Corporation (UK) Limited London UK 213800STG3UV87MDGA96 Citigroup Global Markets Limited London UK XKZZ2JZF41MRHTR1V493 Clarksons Platou Securities AS Oslo Norway 5967007LIEEXZXA40G44 CLSA (UK) London UK 213800VZMAGVIU2IJA72 Commerzbank AG Frankfurt -

Oversikt Over Bøker Til Salgs På Historielagets Hus Prisliste Fra 1.12.2018

Romerike Historielag Oversikt over bøker til salgs på Historielagets Hus Prisliste fra 1.12.2018 Bøkene selges på Historielagets Hus i kontortiden hver torsdag fra kl. 10.00 - 17.00. De kan også bestilles på e-post til [email protected] eller på SMS til tlf. 482 97 462, og kan betales med faktura eller Vipps nr. 109 338. Vipps-gebyr kr 10 for hver 500 kr. Porto kommer i tillegg ved postforsendelse. SPESIALTILBUD: Hele serien om Romerikes historie, fra middelalderen fram til og med dampens tid, består av 5 bøker. De 4 tidligere bøkene selges nå for kr 200,- pr. bok, siste bok koster kr 400,-. Hele serien samlet selges til spesialpris kr 1000,-! Det er også tilbud på 7 bøker fra Eidsvoll Historielag, se tilbudspriser i rødt. Boktittel (i alfabetisk rekkefølge) Forfatter Utgiver Årstall Pris/stk. Andelva, treforedlingsindustrien og Nygård L. Eriksen Eidsvoll Historielag 2005 100 Anna Monrads fortellinger Astrid R. Skedsmo (red.) MiA, KiA, RH 2017 350 Arne Ekeland og Eidsvoll Rune Westengen Eidsvoll Historielag 2018 390 August Krogh Folkeminner "fra Sør-Høland aa der omkring" Høland Historielag 2006 150 Bildehefte fra Lillestrøm Lillestrøm Historielag 1998 50 Bowitz-ætten. Mennesker og miljø. (Løsblad) I. Mehus Oslo 1953 50 Bygdebok for Sørum, bind 1-5, pris pr. bind Jan Erik Horgen Sørum kommune 2003-2013 850 Bygdebok for Sørum, bind 6, søndre del av Blaker Håvard Kongsrud Sørum kommune 2018 850 Dammer i Gjerdrum Gjerdrum Historielag 2009 100 De beste blir alltid igjen Knut Tornaas Blaker og Sørum Historielag 2016 250 De dansk-norske Dragonregimenters rolle under den Alf R. -

Etterkrigstid Og Gjenoppbygging

Kapittel XI ETTERKRIGSTID OG GJENOPPBYGGING En ny hverdag hånd, selv måtte ta opp sine erstatnings- De første år etter 1945 var preget av krav.3 Det kan bemerkes at Erstatningsdirek- krigsoppgjør, krisetiltak, rasjonering toratet på slutten av 1947 hadde fått inn og gjen opp bygging. Også i Rømskog 89,5 millioner kroner fra dømte lands- var det arrestasjoner, og noen av de ble svikere, og hadde selv brukt 7,2 millioner dømt til straffarbeid i opptil seks år. De kroner til administrasjon.4 so net i arbeidsleire på Bjørkelangen og Kommunen var mest opptatt av den ma- Havn ås i Trøgstad. terielle situasjon. Det var her som el lers i Krigsoppgjøret innebar også utbedring landet stor varemangel, og sen trale myn- av skader, fjer ning av piggtrådsperringer dig heter innførte en rekke bestem melser og registrering av falne. Ifølge kommunens og forordninger som gjaldt materiell, mat gjennomgang had de bygda hverken falne el- og brensel. Rømskog ble på linje med an- ler graver etter tyske soldater.1 Medlemmer dre skogrike kommuner pålagt å levere av hjemme styr kene fikk for sin innsats et- ved til Oslo. I flere år etter krigen var det tergitt skatt. En kommunal nemnd ble ned- ra sjonering på olje og bensin, og ved var satt for å be handle krigsskadesaker, og den eneste brensel. Rømskogs tømmerkvantum var i virksomhet helt til slutten av 1950-åra. var i 1945 26 000 kubikkmeter, og på nyåret Ikke mange krav ble fremsatt, og resultatet 1946 var det hugget en tredjedel av denne var som regel avslag for dem som søkte om mengden. -

Global Finance Names the World's Best Investment Banks 2020

Global Finance Names The World’s Best Investment Banks 2020 NEW YORK, February 10, 2020 – Global Finance magazine has named the 21st annual World’s Best Investment Banks in an exclusive survey to be published in the April 2020 issue. Winning organizations will be honored at an awards ceremony on the evening of March 26 at Sea Containers London. J.P. Morgan was honored as the Best Investment Bank in the world for 2020. About Global Finance “Investment banking is a critical factor driving global growth. Global Finance’s Best Global Finance, founded in Investment Bank awards identify the financial institutions that deliver innovative and 1987, has a circulation of practical solutions for their clients in all kinds of markets,” said Joseph D. Giarraputo, 50,000 and readers in 188 publisher and editorial director of Global Finance. countries. Global Finance’s audience includes senior Global Finance editors, with input from industry experts, used a series of criteria— corporate and financial including entries from banks, market share, number and size of deals, service and officers responsible for making investment and strategic advice, structuring capabilities, distribution network, efforts to address market decisions at multinational conditions, innovation, pricing, after-market performance of underwritings and companies and financial market reputation—to score and select winners, based on a proprietary algorithm. institutions. Its website — Deals announced or completed in 2019 were considered. GFMag.com — offers analysis and articles that are the legacy For editorial information please contact Andrea Fiano, editor: [email protected] of 33 years of experience in international financial markets. Global Finance is headquartered in New York, with offices around the world. -

Competition Commission Addresses Exclusionary Conveyancing Practices in the Banking Industry

Media Statement For Immediate Release 17 July 2020 COMPETITION COMMISSION ADDRESSES EXCLUSIONARY CONVEYANCING PRACTICES IN THE BANKING INDUSTRY The Competition Commission (Commission) is pleased to announce commitments made by Standard Bank, Investec, FNB and Nedbank, to reform their conveyancing practices, following advocacy engagements over the past two years. The banks’ renewed commitment is in response to concerns raised by the Commission on the relationship between banks and conveyancers, which is governed through Service Level Agreements (SLAs) and structured in an exclusionary and anti-competitive manner. In February 2018, the Commission conducted the advocacy engagements following a complaint that was filed by Mr Michael Monthe (Mr Monthe) against Standard Bank. In the complaint, Mr Monthe alleged that he had approached about several law firms in the area where he resides for assistance to institute legal action against Standard Bank. Mr Monthe alleged all the law firms that he had approached refused to take on his matter on the basis that they are part of the SBSA’s panel of attorneys and that they are conflicted in terms of their Service Level Agreements (“SLA’s”) with Standard Bank. Further, the Commission established that the practice of restrictive SLAs for conveyancing services extended to other major banks, namely, Investec, FNB and Nedbank. Following the engagements between the Commission, Standard Bank, Investec, FNB and Nedbank, it was agreed that contractual clauses that prevented law firms appointed to provide conveyancing services from acting against the banks on any matter should be removed. These exclusionary clauses created barriers for small and particularly firms owned by historically disadvantaged persons to expand in the market. -

Standard Settlement Instructions

STANDARD SETTLEMENT INSTRUCTIONS For Account of: Bank Leumi (UK) PLC SWIFT: LUMIGB22WES Further Credit to: Your beneficiary account name & number in full AUD - AUSTRALIAN DOLLAR Pay to Bank: JPMorgan Chase Bank, N.A. London SWIFT: CHASGB2LXXX Cover Through: Australia and New Zealand Banking Group SWIFT: ANZBAU3MXXX CAD – CANADIAN DOLLAR Pay to Bank: JPMorgan Chase Bank, N.A. London SWIFT: CHASGB2LXXX Cover Through: Royal Bank of Canada, Toronto SWIFT: ROYCCAT2XXX CHF – SWISS FRANC Pay to Bank: JPMorgan Chase Bank, N.A. London SWIFT: CHASGB2LXXX Cover Through: UBS Switzerland AG, Zurich SWIFT: UBSWCHZH80A CNY - CHINESE YUAN RENMINBI Pay to Bank: Hongkong & Shanghai Banking, Hong Kong SWIFT: HSBCHKHHHKH CZK – CZECH KORUNA Pay to Bank: JPMorgan Chase Bank, N.A. London SWIFT: CHASGB2LXXX Cover Through: Ceskoslovenska Obchodni Banka AS, Prague SWIFT: CEKOCZPPXXX DKK – DANISH KRONE Pay to Bank: JPMorgan Chase Bank, N.A. London SWIFT: CHASGB2LXXX EUR – EURO Pay to Bank: J.P. Morgan AG. Frankfurt SWIFT: CHASDEFXXXX EUR – EURO Pay to Bank: J.P. Morgan AG. Frankfurt SWIFT: CHASDEFXXXX 1 STANDARD SETTLEMENT INSTRUCTIONS For Account of: Bank Leumi (UK) PLC SWIFT: LUMIGB22WES Further Credit to: Your beneficiary account name & number in full GBP – STERLING (CHAPS / UK SETTLEMENTS) Sort Code: 30-14-95 GBP – STERLING (INTERNATIONAL) Pay to Bank: HSBC, London SWIFT: MIDLGB22XXX HKD – HONG KONG DOLLAR Pay to Bank: JPMorgan Chase Bank, N.A. London SWIFT: CHASGB2LXXX Cover Through: JPMorgan Chase Bank, Hong Kong Branch SWIFT: CHASHKHHXXX HUF – HUNGARIAN FORINT Pay to Bank: JPMorgan Chase Bank, N.A. London SWIFT: CHASGB2LXXX Cover Through: UniCredit Bank Hungary SWIFT: BACXHUHBXXX ILS – ISRAELI SHEKEL Pay to Bank: Bank Leumi Le-Israel BM, Tel Aviv SWIFT: LUMIILITXXX JPY – JAPANESE YEN Pay to Bank: JPMorgan Chase Bank, N.A. -

Brown Brothers Harriman Global Custody Network Listing

BROWN BROTHERS HARRIMAN GLOBAL CUSTODY NETWORK LISTING Brown Brothers Harriman (Luxembourg) S.C.A. has delegated safekeeping duties to each of the entities listed below in the specified markets by appointing them as local correspondents. The below list includes multiple subcustodians/correspondents in certain markets. Confirmation of which subcustodian/correspondent is holding assets in each of those markets with respect to a client is available upon request. The list does not include prime brokers, third party collateral agents or other third parties who may be appointed from time to time as a delegate pursuant to the request of one or more clients (subject to BBH's approval). Confirmations of such appointments are also available upon request. COUNTRY SUBCUSTODIAN ARGENTINA CITIBANK, N.A. BUENOS AIRES BRANCH AUSTRALIA CITIGROUP PTY LIMITED FOR CITIBANK, N.A AUSTRALIA HSBC BANK AUSTRALIA LIMITED FOR THE HONGKONG AND SHANGHAI BANKING CORPORATION LIMITED (HSBC) AUSTRIA DEUTSCHE BANK AG AUSTRIA UNICREDIT BANK AUSTRIA AG BAHRAIN* HSBC BANK MIDDLE EAST LIMITED, BAHRAIN BRANCH FOR THE HONGKONG AND SHANGHAI BANKING CORPORATION LIMITED (HSBC) BANGLADESH* STANDARD CHARTERED BANK, BANGLADESH BRANCH BELGIUM BNP PARIBAS SECURITIES SERVICES BELGIUM DEUTSCHE BANK AG, AMSTERDAM BRANCH BERMUDA* HSBC BANK BERMUDA LIMITED FOR THE HONGKONG AND SHANGHAI BANKING CORPORATION LIMITED (HSBC) BOSNIA* UNICREDIT BANK D.D. FOR UNICREDIT BANK AUSTRIA AG BOTSWANA* STANDARD CHARTERED BANK BOTSWANA LIMITED FOR STANDARD CHARTERED BANK BRAZIL* CITIBANK, N.A. SÃO PAULO BRAZIL* ITAÚ UNIBANCO S.A. BULGARIA* CITIBANK EUROPE PLC, BULGARIA BRANCH FOR CITIBANK N.A. CANADA CIBC MELLON TRUST COMPANY FOR CIBC MELLON TRUST COMPANY, CANADIAN IMPERIAL BANK OF COMMERCE AND BANK OF NEW YORK MELLON CANADA RBC INVESTOR SERVICES TRUST FOR ROYAL BANK OF CANADA (RBC) CHILE* BANCO DE CHILE FOR CITIBANK, N.A. -

Fylkesmannens Tilråding

Miljøvernavdelingen FYLKESMANNEN I OSLO OG AKERSHUS SIN TILRÅDING TIL MILJØDIREKTORATET OM VERNEPLAN FOR SKOG UTVIDELSE AV FIRE NATURRESERVAT I AKERSHUS OG BUSKERUD AUGUST 2016 Innhold 1. Tilråding ......................................................................................................................................... 2 2. Hjemmelsgrunnlag .......................................................................................................................... 3 3. Saksbehandling ............................................................................................................................... 4 4. Viktige endringer under behandlingen av verneplanen .................................................................. 5 5. Forvaltning, økonomiske og administrative konsekvenser ............................................................ 6 6. Høring ............................................................................................................................................. 6 6.1. Generelle merknader til verneplanen .......................................................................................... 7 7. Beskrivelser og merknader til de enkelte områdene ..................................................................... 11 7.1. Rundkollen og Sortungsbekken, Nittedal kommune, Akershus fylke .................................. 11 7.2. Furuåsen og Hagahogget naturreservat, Asker kommune, Akershus fylke .......................... 14 7.3. Fagermåsan naturreservat, Aurskog-Høland kommune, Akershus -

Quarterly Report for Q1 2008 for Spar Nord Bank DKK 183 Million in Pre-Tax Profits - Forecast for Core Earnings for the Year Repeated

To Stock Exchange Announcement OMX The Nordic Exchange Copenhagen No. 5, 2008 and the press For further information, contact: Lasse Nyby Chief Executive Officer Tel. +45 9634 4011 30 April 2008 Ole Madsen, Communications Manager Tel. +45 9634 4010 Quarterly report for Q1 2008 for Spar Nord Bank DKK 183 million in pre-tax profits - forecast for core earnings for the year repeated • Annualized 18% return on equity before tax • Net interest income up 15% to DKK 313 million • Net income from fees, charges and commissions down 20% to DKK 104 million • Market-value adjustments reduced to DKK 8 million • Costs grew 11% • DKK 8 million recognized as net income due to reversed impairment of loans and advances and related items • Earnings from the trading portfolio and an extra payment regarding Totalkredit amount to DKK 37 million in total • Lending up 15%, and a 26% hike in deposits • Forecast for core earnings for the year repeated Spar Nord Bank A/S • Moody’s rating: C, A1, P-1 (unchanged, outlook stable) Skelagervej 15 Developments in Q1 2008 P. O. Box 162 • 13 consecutive quarterly periods with net growth in customers DK-9100 Aalborg • Net interest income DKK 13 million up on Q4 2007 • Net income from fees, charges and commissions in line with Q3 and Q4 2007 results Reg. No. 9380 • Sustained strong credit quality level – reporting recognition of net income from Telephone +45 96 34 40 00 impairment of loans, advances, etc. for the 10th consecutive quarterly period Telefax + 45 96 34 45 60 • Business volume at same level as at end-2007 Swift spno dk 22 • Leasing activities continue to develop on a very satisfactory note • Interest margin widening at a moderate pace www.sparnord.dk • Wider yield spread between Danish mortgage-credit bonds and government bonds means distinctively lower market-value adjustments and loss on earnings from invest- [email protected] ment portfolios • Improved excess coverage relative to strategic liquidity target CVR-nr. -

Stavanger Kommunes Eierskapsmelding

Stavanger kommunes eierskapspolitikk Eierskapsmelding 2013 Foto: Siv Egeli Innhold Forord ...................................................................................................... 3 1. Stavanger kommunes eierskapsmelding ......................................... 4 1.1 Eierskapsmelding 2013 .................................................................................................... 4 1.2 Eier- og selskapsdokumenter ......................................................................................... 5 1.3 Leseveiledning ................................................................................................................... 6 1.4 Eier-/selskapsprosesser i valgperioden 2011-2015 .................................................... 7 2. Omfang og utvikling av kommunens eierskap ................................ 9 2.1 Stavanger kommunes eierskap ...................................................................................... 9 2.2 Utviklingen i eierskapet siden 2000 ............................................................................. 10 2.3 Selskapsorganisering i kommunal sektor ................................................................... 10 3. Stavanger kommunes eierskapspolitikk ........................................ 13 3.1 Stavanger kommunes eierskapspolitikk ...................................................................... 13 3.2 Motiver for kommunens selskapsorganisering ........................................................... 13 3.3 Politisk og administrativ eieroppfølging -

Oversikt Over Merkur-Butikkar, Fordelt På Fylke Og Kommune (586 Butikkkar Pr

Oversikt over Merkur-butikkar, fordelt på fylke og kommune (586 butikkkar pr. 22.02. 2019) Firmanamn Postnr. Adresse Kommune Fylke JOKER GAN 1903 GAN 0227 Fet Akershus JOKER SETSKOG 1954 SETSKOG 0221 Aurskog-Høland Akershus TB DRIFT AS 1963 Fosser 0221 Aurskog-Høland Akershus ASDAL MAT ANS 4824 BJORBEKK 0906 Arendal Aust-Agder BYGLAND MATSENTER AS 4745 BYGLAND 0938 Bygland Aust-Agder COOP PRIX VALLE 4747 VALLE 0940 Valle Aust-Agder COOP SØRVEST SA 4745 BYGLAND 0938 Bygland Aust-Agder COOP SØRVEST SA 4754 BYKLE 0941 Bykle Aust-Agder COOP SØRVEST SA 4741 BYGLANDSFJORD 0938 Bygland Aust-Agder COOP SØRVEST SA 4748 RYSSTAD 0940 Valle Aust-Agder DÅSNES MAT AS 4737 HORNNES 0937 Evje og Hornnes Aust-Agder DØLEMO MAT AS 4869 DØLEMO 0929 Åmli Aust-Agder ENGESLAND HANDEL AS 4768 ENGESLAND 0928 Birkenes Aust-Agder GJEVING BUTIKKDRIFT AS 4912 GJEVING 0914 Tvedestrand Aust-Agder GJØVDAL HANDEL AS 4865 ÅMLI 0929 Åmli Aust-Agder Herefoss Mat AS 4766 HEREFOSS 0928 Birkenes Aust-Agder HOMBORSUND LANDHANDEL AS 4888 HOMBORSUND 0904 Grimstad Aust-Agder HOPESTRAND VAREHANDEL AS 4950 RISØR 0901 Risør Aust-Agder JOKER VALLE 4747 VALLE 0940 Valle Aust-Agder LYNGØR HANDELSHUS AS 4910 LYNGØR 0914 Tvedestrand Aust-Agder MATKROKEN BYGLAND AVD 7482 4745 BYGLAND 0938 Bygland Aust-Agder MATKROKEN INDRE ÅRSNES AVD 7406 4770 HØVÅG 0926 Lillesand Aust-Agder Mykland Mat AS 4832 Mykland 0919 Froland Aust-Agder NELAUG DAGLIGVARE AS 4863 NELAUG 0929 Åmli Aust-Agder NES VERK HANDEL AS 4900 TVEDESTRAND 0914 Tvedestrand Aust-Agder RYKENE NÆRKJØP AS 4821 RYKENE 0906 Arendal Aust-Agder SANDØYA MAT AS 4915 VESTRE SANDØYA 0914 Tvedestrand Aust-Agder 1 Oversikt over Merkur-butikkar, fordelt på fylke og kommune (586 butikkkar pr.